by jqm | Jul 5, 2026 | Insurance

Did you know that digital marketing services now represent 31% of freelance job postings worldwide? As the demand for your expertise grows, so does the complexity of the risks you face in an AI-driven market. Securing the right freelance marketing consultant insurance is no longer just a box-ticking exercise for contracts; it’s a fundamental shield for your professional reputation. The line between a successful campaign and a costly legal dispute has never been thinner.

You likely feel the pressure of satisfying strict client contracts while worrying if your current cover actually handles modern digital risks like defamation or intellectual property claims. It’s common to feel frustrated by generic policies that use confusing jargon to hide what they don’t cover. We understand that you need a pragmatic, straightforward solution that lets you focus on delivering results for your clients without the constant anxiety of a potential lawsuit for lost revenue, especially with new Right to Work requirements for subcontractors taking effect in October 2026.

This guide promises to demystify the insurance process by identifying the exact policies you need to stay compliant and protected in 2026. We’ll preview the core requirements for professional indemnity and public liability, explain how to handle new digital risks, and show you how to find cost-effective, tailored cover. When you’re ready to secure your business, Just Quote Me to handle the complexities so you can get back to your clients.

Key Takeaways

- Identify why Professional Indemnity is the non-negotiable foundation for your business, protecting you against claims of professional negligence or unfit advice.

- Discover how to tailor your freelance marketing consultant insurance to cover modern digital risks and the specific requirements of performance-based contracts.

- Learn the importance of bundling Public Liability and Cyber Liability to safeguard your consultancy against data breaches and physical accidents during client visits.

- Evaluate your “Value at Risk” to ensure your coverage limits accurately reflect your largest client contracts and your specific marketing niche.

- Understand the advantage of using an independent broker to secure bespoke, cost-effective protection that automated comparison sites often overlook.

Why Freelance Marketing Consultants Need Specialist Insurance in 2026

Operating as a consultant in 2026 means you’re managing more than just brand awareness. You’re handling complex data sets, AI-driven automation, and performance-based contracts that tie your fees directly to measurable outcomes. This shift has turned marketing advice into a high-stakes deliverable. If a campaign fails to meet specific KPIs or a data error leads to a client’s financial loss, you could be held liable. Standard home insurance policies simply don’t cover these professional risks; they’re designed for domestic incidents, not the legal complexities of a digital consultancy.

Effective freelance marketing consultant insurance acts as a bespoke bundle of protections. It isn’t just about “having cover”; it’s about having the right specific protections that satisfy modern procurement departments. High-value corporate and public sector clients now view insurance as a non-negotiable prerequisite. Without it, you’re often disqualified from the bidding process before you’ve even presented your strategy. It serves as a badge of professionalism that tells Tier 1 clients you’re a stable, reliable partner who understands the commercial realities of the UK market.

The Shift in Marketing Liability: From Creative to Data-Driven

With 78% of freelancers now using AI tools to enhance productivity, the nature of liability has changed. While AI improves efficiency, it introduces new risks regarding copyright, algorithmic bias, and data accuracy. In 2026, your “advice” is treated with the same legal scrutiny as a physical product. If a flaw in your data analytics leads to a client wasting their entire quarterly budget, they’ll look to your Professional Indemnity Insurance to recover those losses. Because these risks are technical, it’s vital to seek FCA-authorised advice from an independent broker who understands these digital nuances rather than relying on a generic algorithm.

Satisfying Client Contracts and Procurement Requirements

Most Tier 1 UK clients now demand a minimum of £1 million in cover for Professional Indemnity Insurance. This isn’t just red tape. It’s a risk management strategy for the client. Many consultants fall for the “working from home” myth, believing that because they don’t have a physical office, they don’t need business-grade liability. However, from October 1, 2026, the requirement for clients to conduct “Right to Work” checks on subcontractors further formalises these freelance relationships. Having your insurance in order simplifies this onboarding process, proving you’re a fully compliant business entity rather than just a casual worker.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Professional Indemnity: The Core Protection for Marketing Advice

For marketers, Professional Indemnity insurance provides protection against the financial consequences of their professional errors. If your strategy leads to a client’s financial downturn, you’re potentially liable for the loss of income. This is why freelance marketing consultant insurance prioritises Professional Indemnity (PI) above all else. It’s the “must-have” policy because it addresses the core of your business: your expertise. Whether you’ve missed a critical deadline that caused a product launch to fail or provided “unfit” advice regarding a market entry, PI covers the legal fees and compensation costs that follow.

Defending your reputation in court is prohibitively expensive. Even if a claim is completely baseless, the cost of solicitors and expert witnesses can quickly reach tens of thousands of pounds. While some assume only large corporations face these issues, the federal government requires certain business structures to maintain specific protections, and UK clients often follow suit by making PI a contractual obligation. It ensures that a single professional error doesn’t end your career before it has truly begun. It’s a pragmatic safety net that allows you to give bold, effective advice with confidence.

Intellectual Property and Copyright Infringement

In a world of rapid content creation, accidental copyright infringement is a constant threat. You might use a font that requires a different tier of licensing or an image that looks like public domain but isn’t. If a brand sues your client for “copycat” branding or slogan theft because of your work, they’ll likely pursue you for the damages. Having robust professional indemnity insurance means you have the financial backing to handle these intellectual property disputes without liquidating your personal assets. It’s an essential safeguard for anyone producing creative assets or brand strategies.

Defamation, Libel, and Slander in Social Media Management

Social media management moves at the speed of light, which increases the risk of “off-the-cuff” remarks that could be deemed defamatory. A single misplaced tweet or a poorly judged response to a competitor can lead to expensive libel claims. Even if your advice is factually correct, a client might still face a PR crisis that they blame on your communication strategy. PI cover often includes the costs of a PR crisis management response, helping to mitigate the damage to your client’s brand and your own standing. If you’re unsure about your specific risk level, you can speak with a specialist to review your current contracts and ensure your freelance marketing consultant insurance is fit for purpose.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Beyond Advice: Public Liability, Cyber, and Equipment Cover

While your professional advice is the foundation of your business, your physical presence and digital interactions carry distinct risks that Professional Indemnity doesn’t address. A comprehensive freelance marketing consultant insurance strategy must account for the tangible world and the invisible data you manage daily. Public Liability covers third-party injury or property damage caused by your business activities. Even if you operate primarily from a home office, any interaction with the public or clients creates a potential for liability that could derail your consultancy.

Understanding the nuances of liability insurance for freelancers is essential for protecting your personal assets. Many consultants overlook the fact that a single accident during a client workshop or a data breach involving a subscriber list can lead to costs far exceeding their annual turnover. Safeguarding your livelihood also means considering equipment cover for your hardware and business interruption insurance to protect your income if a fire or flood prevents you from working. These protections ensure you aren’t paying out of pocket for unforeseen disasters.

Beyond insurance, maintaining your essential work tools is just as important for daily operations. For consultants who rely on mobile technology to stay connected, iRepairMan London provides the specialized phone and tablet repair services needed to keep a digital consultancy running without interruption.

Public Liability for Modern Consultants

Imagine you’re in a high-stakes strategy meeting at a client’s headquarters. If you accidentally spill coffee on their high-end server or a client trips over your laptop charging cable and suffers an injury, you’re responsible for the damages. Most UK corporate contracts require a minimum of £1 million in public liability insurance. It’s a standard benchmark that proves you’re prepared for the physical risks of doing business in professional environments. Without it, you might find yourself barred from visiting the very offices you’re meant to be advising.

Cyber Insurance and Marketing Data Security

Marketing consultants often have “god-mode” access to client CRMs, email lists, and sensitive performance data. This responsibility carries significant weight under GDPR. If your systems are compromised and a client’s data is leaked, the legal and notification costs are staggering. A robust cyber insurance policy assists with data recovery, legal fees, and the costs of notifying affected parties. In 2026, where digital marketing services represent 31% of freelance job postings, data security isn’t just an IT issue; it’s a core business liability.

Employers’ Liability: When Do You Need It?

If you hire a virtual assistant, a summer intern, or even a part-time researcher, you’re likely legally required to have employers liability insurance. In the UK, the law is strict: if you have employees, you must have EL cover of at least £5 million. The fines for operating without it can reach £2,500 for every single day you’re unprotected. Even if your team is remote or temporary, the “master and servant” relationship often triggers this requirement, making it a vital component of your freelance marketing consultant insurance package.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Determining Your Coverage: Factors That Influence Costs and Limits

Calculating the cost of your freelance marketing consultant insurance requires a pragmatic look at your “Value at Risk.” You shouldn’t simply choose the cheapest policy available; you need to evaluate the potential financial impact if your advice leads to a total campaign failure. A sensible starting point is to look at your largest client contract. If a client is paying you £50,000 for a strategy they expect to generate £500,000, your professional liability is tied to that higher figure, not just your fee. Your annual turnover also plays a role. With Making Tax Digital requirements for those earning over £50,000 starting in April 2026, many freelancers are tracking their revenue more closely, which helps in providing accurate figures to insurers.

Your specific niche within the marketing sector heavily influences your premiums. A PR consultant faces higher risks regarding defamation and libel, while an SEO specialist might be more exposed to technical errors or algorithm-related losses. For example, in 2026, average day rates for copywriters stand at £480, while social media managers average £350. These differing income levels and the nature of the deliverables change the risk profile. When selecting a policy, pay close attention to whether the limit is “Any One Claim” or “In the Aggregate.” An “Any One Claim” policy is more robust because it provides the full limit for every individual claim made during the year, whereas an aggregate limit is the maximum the insurer will pay for all claims combined.

Contractual Obligations and IR35 Implications

Client contracts often contain “hold harmless” clauses or specific indemnity requirements that you must meet to stay compliant. Beyond simple protection, having your own freelance marketing consultant insurance is a vital indicator of your IR35 status. To be considered “outside IR35,” you must demonstrate that you carry genuine financial risk. Paying for your own professional indemnity and public liability insurance is a classic “badge of business” that HMRC looks for. If you are unsure if your current cover meets the specific demands of a new Tier 1 contract, you can compare specialist indemnity options to ensure you aren’t left exposed.

Ways to Reduce Your Marketing Insurance Premiums

You can lower your insurance costs without sacrificing essential protection by implementing robust “Terms of Business.” Clear contracts that define the scope of your work and limit your liability can make you more attractive to insurers. You might also consider increasing your voluntary excess; however, you must ensure you have the cash reserves to pay that excess if a claim arises. Choosing an annual payment structure rather than monthly instalments often results in a lower total cost. If you need a policy that fits your specific business model, get a tailored quote that reflects your actual risk rather than a generic industry average.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Navigating the Market with an Independent Insurance Broker

Choosing the right freelance marketing consultant insurance shouldn’t feel like a gamble with an automated form. While comparison sites are designed for high-volume, generic risks, they often fail to capture the nuances of a specialist marketing consultancy. An independent broker acts as your advocate, looking beyond the surface to find a policy that matches your specific contractual needs and digital risk profile. This personalised approach ensures you aren’t paying for redundant cover while simultaneously closing any dangerous gaps in your protection.

Just Quote Me brings 30 years of independent brokerage expertise to your business. We’ve spent three decades building relationships with a broad network of top UK insurers, giving us access to competitive rates that aren’t always available to the general public. This history allows us to negotiate on your behalf, ensuring that your premiums reflect your actual risk rather than a broad industry average. We understand that as a freelancer, your time is your most valuable asset, so we handle the heavy lifting of market research for you.

Our support doesn’t end once your policy is active. The freelance market is dynamic; your turnover might increase, or you might take on a high-stakes project that requires a mid-term adjustment to your indemnity limits. We provide ongoing assistance with these changes and offer a steady hand if you ever need to make a claim. Having a human advisor who knows your business history makes the administrative burden of insurance significantly lighter, allowing you to focus on your clients’ growth.

The Human Element: Expert Advice vs. Automated Quotes

Complex marketing risks, such as performance-based disputes or international IP claims, require a conversation rather than just a digital tick-box. Automated systems don’t ask about the specific nature of your SEO strategies or the depth of your social media influence. By speaking with an expert, you can clarify your GDPR responsibilities and ensure your cyber cover is actually fit for purpose. We aim to simplify the process, removing the jargon and providing clear, pragmatic advice that helps you make informed decisions with confidence.

Getting Started: Your Bespoke Quote Journey

Ready to protect your reputation? The journey to a bespoke policy is straightforward and efficient. You’ll only need to provide a few key details about your services, your estimated turnover, and any specific requirements from your current client contracts. We’ll then scan our network of insurers to present you with the most cost-effective and tailored options. It’s best to have your cover in place before your next big project starts to ensure you’re fully compliant from day one. Get Your Free Business Insurance Quote now to see how we can safeguard your consultancy.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Secure Your Consultancy’s Future Today

Protecting your professional reputation in 2026 requires more than just high-quality work. It demands a robust strategy that accounts for performance-based contracts, digital data security, and evolving regulatory requirements. By prioritising Professional Indemnity and tailoring your cover to include Cyber and Public Liability, you ensure that a single error or accident doesn’t jeopardise your livelihood. You’ve worked hard to build your brand; don’t leave it vulnerable to the complexities of modern litigation.

Finding the right freelance marketing consultant insurance shouldn’t be an administrative burden. As an FCA-authorised independent broker with over 30 years of industry experience, we provide the steady hand you need. We leverage our broad network of top UK insurers to find bespoke cover that satisfies even the most stringent Tier 1 contracts. You can Just Quote Me to secure your business and focus on what you do best: delivering exceptional results for your clients. We’re here to manage the risks so you can grow with confidence.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Frequently Asked Questions

Is professional indemnity insurance a legal requirement for UK marketing consultants?

Professional Indemnity insurance is not a legal requirement for UK marketing consultants, but it is almost always a contractual necessity. Most corporate and public sector clients will refuse to engage your services unless you provide proof of cover. While the law doesn’t mandate it, operating without PI leaves your personal assets vulnerable to claims of negligence or errors in your professional advice.

Does my home insurance cover my marketing equipment while working from home?

Standard home insurance typically does not provide adequate cover for professional marketing equipment like high-end laptops, cameras, or servers. Most domestic policies specifically exclude items used primarily for business purposes or have very low claim limits. You should check your policy wording carefully; however, most consultants find that adding dedicated equipment cover to their freelance marketing consultant insurance is the only way to ensure full replacement value.

How much professional indemnity cover do I need for a freelance marketing contract?

The amount of Professional Indemnity cover you need depends entirely on your client contracts, though £1 million is the industry standard for most UK freelancers. Some high-value projects or government tenders may require limits as high as £5 million. You should evaluate your “Value at Risk” by considering the potential financial loss a client could suffer if your marketing strategy fails or contains a critical error.

What is the difference between public liability and professional indemnity for consultants?

Professional Indemnity covers the advice and services you provide, while Public Liability covers physical accidents and property damage. If you give a client incorrect data that loses them money, PI handles the claim. If a client trips over your bag during a meeting and suffers an injury, PL provides the protection. Both are essential components of a balanced insurance portfolio for any active consultant.

Can I get insurance for a single short-term marketing project?

You can obtain insurance for short-term projects, though most consultants opt for an annual policy to maintain continuous protection. Since Professional Indemnity is usually “claims-made,” you need to be covered both when the work is done and when a claim is actually filed. An annual policy ensures you don’t have gaps in cover that could leave you exposed once a specific project ends.

Does marketing insurance cover me for work with international clients?

Most UK insurance policies can be extended to cover work for international clients, but you must specify this when requesting a quote. There is a significant difference between “territorial limits,” which cover where you work, and “jurisdiction,” which covers where legal action can be taken. Working with clients in the USA or Canada often requires specific endorsements due to the higher litigation risks in those regions.

What happens if a client sues me for a failed marketing campaign ROI?

If a client sues you for failed ROI, your Professional Indemnity insurance provides the funds to defend your reputation and pay any court-awarded compensation. Performance-based contracts are increasingly common in 2026, making the risk of being sued for “unfit” advice more prevalent. Your policy helps prove that you acted with professional care, even if the market didn’t respond as your strategy predicted.

How much does freelance marketing consultant insurance typically cost in 2026?

The cost of freelance marketing consultant insurance in 2026 varies based on your turnover, the level of cover you choose, and your specific marketing niche. Factors like your claims history and the complexity of your digital risks also influence the final premium. While generic estimates exist online, the most accurate way to determine your cost is to get a tailored quote that reflects your actual business activities.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Article by

Just Quote Me

JustQuoteMe Ltd is an independent UK insurance brokerage specialising in business and personal insurance solutions. With over 35 years of industry experience, the company provides tailored insurance cover for businesses, landlords, tradespeople, hospitality venues, fleets, and individuals across the UK. Known for its personal service, expert advice, and competitive premiums, JustQuoteMe Ltd works with leading insurers to deliver bespoke policies designed around each client’s unique needs. The company is authorised and regulated by the Financial Conduct Authority (FCA No. 586607) and has built a reputation for trusted, straightforward insurance guidance and long-term client relationships.

by jqm | Jul 4, 2026 | Insurance

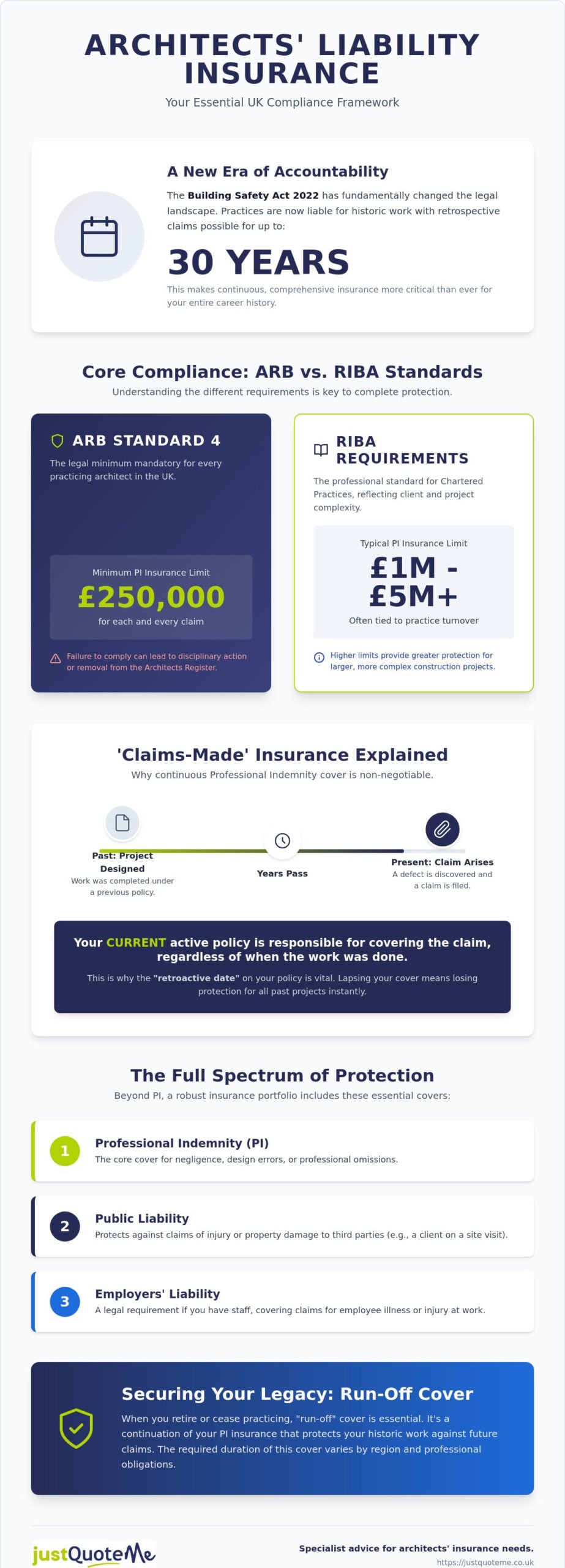

Did you know that the Building Safety Act 2022 now allows for retrospective claims dating back up to 30 years? For a practice owner, this shift transforms your insurance policy from a standard renewal into a vital shield for your entire career history. Meeting the mandatory architects liability insurance requirements isn’t just about ticking a box for the Architects Registration Board (ARB); it’s about protecting yourself against a legal landscape that’s shifted significantly. Since the new Architects Code of Conduct became effective on September 1, 2025, the pressure to maintain precise, compliant cover has never been higher.

It’s understandable if you feel overwhelmed by the hardening market or the conflicting advice between statutory ARB mandates and RIBA recommendations. We understand that you’d rather spend your time on site or at the drawing board than decoding policy fine print. This guide provides a clear compliance framework to help you navigate your professional obligations with confidence. You’ll learn how to distinguish between essential Professional Indemnity (PI) limits, Public Liability, and Employers’ Liability while ensuring your historic work remains fully protected.

Key Takeaways

- Understand the mandatory ARB Standard 4 mandates to ensure your practice remains fully compliant with current UK regulations.

- Learn how the ‘claims-made’ nature of Professional Indemnity insurance affects your long-term risk and why specific indemnity limits are essential.

- Navigate the full spectrum of architects liability insurance requirements by balancing statutory PI cover with Public and Employers’ Liability for comprehensive protection.

- Secure your legacy by identifying the specific run-off cover durations required in your region after you cease practice.

- Simplify the renewal process by working with a specialist who understands the nuances of RIBA recommendations versus mandatory statutory minimums.

Statutory and Professional Insurance Obligations for UK Architects

For any UK architect, professional survival depends on more than just design talent; it rests on maintaining your status on the Architects Register. The Architects Registration Board (ARB) oversees this through a strict set of rules known as the Architects Code: Standards of Conduct and Practice. Standard 4 explicitly mandates that all architects must have adequate and appropriate insurance. Failing to meet these architects liability insurance requirements isn’t a minor administrative slip. It can lead to formal disciplinary action, public reprimands, or even permanent removal from the Register.

The current regulatory climate, shaped by the new Architects Code that became effective on September 1, 2025, places the burden of proof on the practitioner. You must demonstrate that your cover is sufficient for the specific risks associated with your projects. While the ARB sets the legal floor, professional bodies like the RIBA often set the ceiling. These organisations frequently demand higher indemnity limits and broader policy terms to maintain chartered status, reflecting the increased complexity of modern construction projects.

Understanding ARB Standard 4 Requirements

The ARB defines “adequate and appropriate” cover based on the nature and value of your work. At its core, this means holding Professional Indemnity Insurance with a minimum limit of £250,000 for each and every claim. This mandatory minimum applies to every practicing architect in the UK, regardless of whether you’re a sole practitioner or part of a large firm.

During the annual retention process, you’re required to confirm that your policy meets these standards. It’s a proactive duty; you don’t just wait for a claim to happen. You must ensure your policy covers the full scope of your professional activities, including any historic work that might still be subject to legal action under the Building Safety Act 2022.

RIBA vs. ARB: Navigating Overlapping Standards

While the ARB’s £250,000 limit is the legal baseline, RIBA Chartered Practices usually face more rigorous demands. RIBA requirements are often tied to practice turnover, and for many, a limit of £1 million or £5 million is the standard expectation from clients and the institute alike.

A critical distinction in Professional Indemnity Insurance

Professional Indemnity Insurance: The Core Requirement

Professional Indemnity Insurance (PII) is the cornerstone of any practice’s risk management strategy. It addresses financial losses resulting from alleged negligence, design errors, or omissions in your professional advice. While earlier we discussed the ARB’s legal mandates, understanding the technical mechanics of Professional Indemnity Insurance is what actually keeps your practice solvent during a dispute.

Unlike most other insurance types, PI operates on a ‘claims-made’ basis. This means the policy you have active today must cover the claim, regardless of when the design work was originally completed. If you’ve been practicing for a decade, your 2026 policy is responsible for designs you drafted in 2016. This makes the continuity of cover and the “retroactive date” on your certificate vital. If you let your cover lapse, you lose protection for all past projects instantly.

In 2026, insurers remain cautious about specific risks. You’ll likely find strict exclusions or high deductibles regarding cladding and fire safety. Notably, the Wren Insurance Association’s shift away from cladding renewal terms in July 2026 illustrates how quickly the market can change. You must verify that your policy aligns with the latest Statutory and Professional Insurance Obligations to avoid gaps in coverage that could lead to personal liability. If you’re unsure how these exclusions affect your current policy, you can speak with a specialist to review your practice’s specific needs.

Determining the Right Limit for Your Practice

The ARB’s £250,000 minimum is often insufficient for modern projects. A minor design error in a residential block can easily exceed this limit once legal fees and remedial costs are tallied. When calculating your architects liability insurance requirements, look beyond turnover and consider the project scale; for example, architects working with high-end builders like Willmac Group must ensure their cover reflects the substantial value of such residential and commercial developments. The Building Safety Act 2022 has extended the liability period significantly, meaning your ‘worst-case scenario’ now has a much longer tail.

Common PI Clauses and Endorsements

The Liability Trinity: Public, Employers, and Cyber Cover

While Professional Indemnity (PI) is the most discussed aspect of your risk profile, it doesn’t exist in a vacuum. A robust approach to architects liability insurance requirements must account for the physical and digital risks that occur outside of your design software. Relying solely on PI is a dangerous gamble. If a member of the public trips over your equipment during a site survey, or if a disgruntled former employee steals your proprietary BIM data, a PI policy won’t offer a penny of protection.

Understanding this “Liability Trinity” is essential for modern practice management. While the Architects Registration Board PII Guidance focuses primarily on the indemnity needed for professional advice, your broader legal and commercial survival depends on addressing these three additional pillars.

Public Liability for Site Visits and Surveys

Every time you step onto a construction site or visit a client’s property, you’re exposed to physical risk. Public Liability insurance protects your practice if your actions cause injury to a third party or damage to their property. It isn’t just for large firms; even a sole practitioner conducting a simple measured survey needs this cover.

Standard indemnity limits usually start at £1 million, but many commercial contracts or local authority projects will insist on £2 million or £5 million as a minimum. It’s a relatively low-cost addition that prevents a single accident from becoming a practice-ending event. Learn more about Public Liability Insurance to see how it integrates with your existing design cover.

Employers Liability and Statutory Compliance

If you have any staff, Employers’ Liability (EL) is a legal requirement under the Employers’ Liability (Compulsory Insurance) Act 1969. This isn’t optional. The law mandates a minimum of £5 million in cover, though most insurers provide £10 million as standard.

This requirement isn’t limited to full-time architects. You must cover freelancers, interns, and even part-time administrative staff. Failing to hold EL can result in fines of up to £2,500 for every single day you’re without it. Understanding Employers Liability Insurance is the first step in ensuring your practice remains on the right side of UK law.

Cyber Risks in Modern Architectural Practices

Architectural design has moved almost entirely into the digital space, making Building Information Modelling (BIM) systems a prime target for cybercriminals. A data breach can lead to the loss of sensitive client blueprints or the theft of intellectual property. Cyber insurance covers the heavy costs of data recovery, legal fees, and the mandatory client notifications required under GDPR. It’s becoming an increasingly vital component of Bespoke Cyber Insurance for Professionals

Run-off Cover: Meeting Post-Practice Requirements

Retirement or the closure of a practice doesn’t signal the end of your professional exposure. In fact, for many, it’s the beginning of a decade-long period of “tail risk.” Because Professional Indemnity Insurance operates on a claims-made basis, you must have a policy active at the moment a claim is made, not just when the work was performed. If you cease practicing today but a design flaw is discovered in three years, you’ll be personally liable for the damages unless you’ve secured run-off cover.

Meeting the architects liability insurance requirements for run-off isn’t just a matter of professional prudence; it’s a regulatory mandate. The Architects Registration Board (ARB) requires architects to maintain run-off cover for a minimum of six years in England, Wales, and Northern Ireland. In Scotland, this requirement is five years. However, many legal experts suggest that 12 years of cover is the safer choice. This is because contracts signed “under seal” carry a 12-year limitation period, and the Building Safety Act 2022 has pushed some liability windows even further.

The Long Tail of Architectural Liability

The statute of limitations for contract and tort claims creates a significant lag between the completion of a project and the emergence of a dispute. If your practice merges or closes, your liability typically follows you. Without run-off protection, your personal assets could be at risk from projects you haven’t thought about in years. This is why the ARB views run-off cover as a non-negotiable part of the Architects Code. It ensures that clients aren’t left without recourse and that architects aren’t left financially devastated by historic errors.

Securing Cost-Effective Run-off Protection

Securing run-off cover in a hard insurance market can be challenging, as insurers have become more selective about the risks they’ll carry for inactive professionals. Premiums for run-off usually start at a percentage of your last full premium and often decrease annually as the likelihood of a claim from older projects diminishes. Some insurers offer a single “upfront” premium to cover the entire six or twelve-year period, which can simplify your financial planning as you exit the profession.

If you’re planning your retirement and need to understand how to structure your exit without leaving gaps in your cover, you can Request a Call back for free Expert advice. Managing these final architects liability insurance requirements

Simplifying Your Insurance with Just Quote Me

Meeting the complex architects liability insurance requirements in a hardening 2026 market doesn’t have to be a source of anxiety. While automated online platforms offer speed, they often lack the nuance required to ensure your policy actually stands up to ARB scrutiny or the extended liability periods of the Building Safety Act. Algorithms don’t understand the specific risks of your project history. We do. At Just Quote Me, we act as your steady hand, managing the administrative burden so you can focus on your designs.

We bring 30 years of experience to the table. This deep industry knowledge allows us to look beyond the surface of a standard application. We understand how the mandates discussed earlier in this guide impact your daily operations. By working with an independent broker, you gain an advocate who knows how to present your practice’s risk profile to insurers in the best possible light. This often results in more competitive premiums and broader coverage than a generic search engine could ever provide.

This principle of specialized advocacy applies to all areas of professional finance; for architects seeking to secure a mortgage or tailored loan solution, Quantum Brokers offers a similar level of expertise and personalized service.

Why a Bespoke Approach Beats ‘Off-the-Shelf’ Policies

Off-the-shelf policies frequently leave architects under-insured. This is a risk you can’t afford. Conversely, you might be paying for unnecessary extras that don’t apply to your specific sector. We take a different approach. By tailoring your Bespoke Professional Indemnity Insurance, we ensure every clause aligns with your turnover, project risk, and specific RIBA Chartered Practice obligations. We don’t just provide a certificate; we help you navigate the compliance documentation needed for your annual ARB retention. Our team assists with policy wordings to ensure you aren’t caught out by the fine print during a claim.

Start Your 2026 Compliance Journey Today

Securing your cover for the year ahead is a quick and efficient process. We pride ourselves on providing straightforward, jargon-free insurance advice that cuts through the noise of the current market. By leveraging our deep relationships with a panel of specialist UK insurers, we help you meet all architects liability insurance requirements without overcomplicating your overheads. We believe in a human-centric service that prioritizes your practice’s long-term security over a quick transaction. Whether you are a sole practitioner or a growing firm, we ensure your cover is as precise as your drawings.

Protect Your Professional Legacy

Adhering to architects liability insurance requirements is a career-long duty that safeguards your reputation and your financial future. The regulatory environment in 2026 is more demanding than ever, requiring a balance between mandatory ARB minimums and the long-term protections necessitated by the Building Safety Act. Whether you’re managing the daily risks of site visits or planning a secure exit from the profession with run-off cover, a precise policy is your most important tool.

Just Quote Me acts as your trusted advisor, drawing on 30 years of industry experience to simplify these complex requirements. As an FCA-authorised independent broker, we provide direct access to top UK insurers, ensuring you secure comprehensive protection tailored to your unique workload. We manage the administrative burdens so you can focus on the architectural excellence your clients expect. Get the peace of mind that comes from a steady hand in a hardening market.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Frequently Asked Questions

Is Professional Indemnity Insurance a legal requirement for UK architects?

Yes, holding Professional Indemnity Insurance is a mandatory requirement for all architects registered with the Architects Registration Board (ARB). Under Standard 4 of the Architects Code, you must have adequate and appropriate cover to practice. While it’s a professional mandate rather than a criminal law, failing to maintain cover will lead to your removal from the Register. This effectively ends your legal right to use the title ‘architect’ in the UK.

What is the minimum level of PI insurance required by the ARB?

The ARB mandates a minimum indemnity limit of £250,000 for each and every claim. This level is the absolute legal floor for any practicing architect. However, most commercial contracts and professional bodies like the RIBA suggest much higher limits. You should assess your architects liability insurance requirements based on your specific project values rather than just relying on this statutory minimum, as modern litigation costs can quickly exceed this amount.

How long must an architect maintain run-off cover after retiring?

You are required to maintain run-off cover for a minimum of six years if you practice in England, Wales, or Northern Ireland. For those in Scotland, the requirement is five years. Because architectural liability has a ‘long tail’, many professionals choose to extend this cover to twelve years. This aligns with the limitation period for contracts signed under seal, providing a more robust safety net against delayed claims.

Does my PI insurance cover me for cladding and fire safety claims in 2026?

Coverage for cladding and fire safety is currently highly restricted in the UK insurance market. Many standard policies now include specific exclusions or much higher deductibles for these risks. Following the Building Safety Act 2022, insurers have become increasingly cautious. You must check your policy schedule carefully. If your current provider excludes these areas, you may need to seek a specialist endorsement to ensure your architects liability insurance requirements are fully met.

What is the difference between Public Liability and Professional Indemnity for architects?

Professional Indemnity covers financial losses caused by errors in your design or professional advice. In contrast, Public Liability protects you against claims for physical injury to third parties or accidental damage to their property. For example, if you provide a faulty structural design, PI responds. If you knock over a valuable vase or a client trips over your tripod during a site survey, Public Liability provides the necessary protection.

Can I practice as an architect without being registered with the ARB?

No, you cannot legally call yourself an architect or practice under that title in the UK without ARB registration. The title ‘architect’ is protected by the Architects Act 1997. To remain registered, you must comply with all professional standards, including mandatory insurance obligations. Practicing without registration is a criminal offence that can result in prosecution and significant fines, regardless of your qualifications or previous experience level.

What happens if I cannot find affordable PI insurance in the current market?

If you’re struggling with high premiums, don’t simply stop your cover, as this violates ARB rules. The ‘hardening’ market has made renewals difficult for many small practices. In these cases, it’s best to work with an independent broker who can access a wider panel of specialist insurers. They can often help reframe your risk profile or find alternative providers that don’t appear on standard automated comparison platforms.

Do I need insurance if I am only doing small residential extensions?

Yes, insurance is mandatory regardless of the size or complexity of your projects. Even a minor error in a residential extension can lead to significant remedial costs or structural issues that exceed your personal assets. The ARB doesn’t differentiate between large scale developments and small domestic works when it comes to insurance. Every registered architect must hold adequate cover to protect both themselves and their clients from potential financial loss.

Article by

Just Quote Me

JustQuoteMe Ltd is an independent UK insurance brokerage specialising in business and personal insurance solutions. With over 35 years of industry experience, the company provides tailored insurance cover for businesses, landlords, tradespeople, hospitality venues, fleets, and individuals across the UK. Known for its personal service, expert advice, and competitive premiums, JustQuoteMe Ltd works with leading insurers to deliver bespoke policies designed around each client’s unique needs. The company is authorised and regulated by the Financial Conduct Authority (FCA No. 586607) and has built a reputation for trusted, straightforward insurance guidance and long-term client relationships.

by jqm | Jul 3, 2026 | Insurance

What if the secret to lowering your premium isn’t just about your fee income, but how you present your firm’s internal risk hygiene to underwriters? It’s a common frustration for many practitioners who find the accountants professional indemnity insurance cost rising despite a clean claims history. You’ve likely spent hours trying to decode the latest ICAEW minimum indemnity requirements or worrying if your current cover actually protects your specific tax or probate work.

We understand that you’re looking for full compliance without the administrative burden or the “hard” market price tag. This guide explores the key factors driving premiums in 2026 and explains how to secure bespoke, compliant cover at a competitive price. We’ll examine the shifting regulatory landscape from the ACCA and ICAEW, and show you how to Just Quote Me to simplify your application while ensuring you meet every professional body standard. By focusing on specialized knowledge rather than generalist appeal, you can protect your practice with confidence.

Key Takeaways

- Understand why professional indemnity insurance is a mandatory regulatory requirement for ICAEW, ACCA, and CIMA members to maintain their practice licenses.

- Learn how underwriters calculate the accountants professional indemnity insurance cost based on your gross fee income and high-risk activities like audit or insolvency.

- Stay compliant with the latest 2026 minimum indemnity limits and ensure your policy is issued by a regulatory-approved participating insurer.

- Discover how implementing documented risk management procedures and providing full disclosure can help reduce your annual premiums.

- Find out why partnering with an experienced independent broker like Just Quote Me provides the specialized sector knowledge needed to navigate a complex market.

What is Accountants Professional Indemnity Insurance?

Accountants professional indemnity insurance serves as a mandatory shield designed to protect practitioners against claims of professional negligence, errors, or omissions. While many business owners view insurance as a discretionary expense, for those in the accountancy sector, it’s a regulatory lifeline. Professional bodies like the ICAEW and ACCA mandate specific levels of cover to ensure that both the firm and its clients are protected from financial loss. Without this protection, the accountants professional indemnity insurance cost would be the least of your worries; you could face the loss of your practicing certificate or personal bankruptcy.

When selecting a policy, you must understand the difference between “any one claim” and “aggregate” limits. Most UK professional bodies require “any one claim” wording. This means the full limit of indemnity is available for every individual claim made during the policy period. In contrast, an aggregate limit is a total cap on what the insurer will pay for all claims combined. Choosing the wrong structure could leave you underinsured if multiple clients bring actions against you in a single year. Professional liability insurance is the bedrock of a secure practice, shielding your personal assets and the long-term viability of your business.

Why Accountants Need Specific PI Cover

Accountants face unique risks that generic policies often overlook. Whether you’re providing complex tax advice, conducting statutory audits, or managing probate, the potential for a high-value error is constant. Even if you’ve done nothing wrong, defending yourself against a frivolous claim is incredibly expensive. Data shows the average accountants’ insurance claim was £4,314 between June 2025 and May 2026, but this figure doesn’t account for the much higher legal fees involved in complex disputes. A robust Professional Indemnity Insurance policy covers these legal defense costs, ensuring your cash flow remains stable while experts handle the dispute.

The ‘Claims-Made’ Nature of the Policy

It’s vital to remember that PI insurance operates on a “claims-made” basis. This means the policy must be active at the time a claim is formally made against you, regardless of when the work was actually performed. If you performed a tax return in 2023 but the client sues you in 2026, your 2026 policy handles the claim. This is why “retroactive dates” are so important; they tell the insurer how far back into your firm’s history the coverage extends. Additionally, if you decide to retire or close your practice, you must maintain “run-off” cover. This protects you against claims that emerge years after you’ve stopped working, which is a key factor in the total accountants professional indemnity insurance cost over the lifetime of a firm.

Key Factors Influencing Your PI Insurance Premium

Underwriters in 2026 take a granular approach to assessing your practice, moving far beyond simple turnover figures. While your gross fee income remains the primary baseline for calculating the accountants professional indemnity insurance cost, it’s the specific nature of your work that dictates the final rate. An underwriter views £100,000 in fees from basic bookkeeping very differently than £100,000 generated from statutory audits or insolvency appointments. This “activity split” is perhaps the most significant variable you can control through your business strategy.

Your claims history also carries immense weight, specifically within a rolling five-year window. Even if a claim was successfully defended, the legal costs incurred stay on your record. Insurers also look closely at your firm’s structure; they generally favor practices with a high ratio of qualified professionals to junior staff. This preference stems from the belief that rigorous oversight reduces the likelihood of the simple clerical errors that often lead to negligence claims.

Niche Services and High-Risk Areas

Certain areas of practice act as red flags in the current market. Advice regarding tax avoidance schemes, for instance, often results in a “declined to quote” from many standard insurers. Similarly, providing probate or investment advice requires specialized wording and often attracts a higher premium. You should also be aware of fee concentration. If a single client accounts for more than 20% of your annual turnover, underwriters perceive a higher risk of independence issues or pressure that could lead to errors. For more detailed regulatory context, you can consult the FCA guidance on Professional Indemnity Insurance to see how they view these professional risks.

The Impact of 2026 Technology Risks

In 2026, technology has fundamentally changed the risk landscape for accounting firms. Underwriters are now specifically asking about AI integration in accounting processes. While AI can improve accuracy, it also introduces risks related to algorithmic bias or data mishandling that a traditional PI policy might not fully cover. This creates a complex overlap between professional liability and Cyber Insurance. If an AI tool causes a data breach that leads to a professional error, you need to be certain which policy responds.

These technological shifts directly influence the accountants professional indemnity insurance cost, as insurers adjust their models to account for potential software-driven failures. Balancing these modern threats requires a partner who understands the nuances of the sector. You can explore our approach to specialist cover to see how we address these emerging risks while keeping your practice fully protected.

Regulatory Minimums: ICAEW, ACCA, and CIMA Requirements

Your professional body doesn’t just offer suggestions; it sets the legal floor for your coverage. To practice legally in the UK, your policy must be issued by a firm on the “Participating Insurer” list. This list represents an agreement between the regulatory body and the insurer to provide a minimum level of wording that meets strict professional standards. If you secure a policy from a non-approved provider, you aren’t just underinsured; you’re in breach of your professional regulations, which can lead to the immediate suspension of your practicing certificate.

The most common calculation used by bodies like the ICAEW and ACCA is the “2.5 times gross fee income” rule. For ICAEW firms with a gross fee income under £800,000, the minimum indemnity is 2.5 times that income, with an absolute floor of £250,000 as of the September 2024 updates. For larger firms, the requirement jumps to £2 million for any one claim. These mandates directly influence the accountants professional indemnity insurance cost, as they dictate the baseline risk an underwriter must accept regardless of your firm’s specific history.

Excess rules are equally strict to prevent firms from taking on more financial risk than they can handle. The ICAEW, for instance, limits the maximum permitted excess to the higher of £3,000 or 3% of your firm’s gross fee income. This ensures that you don’t artificially lower your premium by choosing an excess you can’t actually afford to pay out of pocket if a claim arises.

ICAEW vs. ACCA PI Standards

While both bodies prioritize protection, their specifics differ significantly. ACCA members with a total income over £600,000 must hold at least £1.5 million in cover on an “any one claim” basis. ACCA also mandates the inclusion of a fidelity guarantee, which protects the firm against losses arising from employee dishonesty. Failing to meet these standards doesn’t just create a coverage gap; it triggers disciplinary proceedings that can damage your reputation permanently.

CIMA and AAT: What Smaller Practices Need to Know

CIMA and AAT don’t always specify a hard minimum limit in the same way the ICAEW does, but they still mandate that all members in practice hold qualifying insurance. For smaller bookkeeping or management accounting firms, it’s tempting to opt for the lowest possible limit to minimize the accountants professional indemnity insurance cost. However, we always recommend a “safety buffer.” If you expect to grow or take on a high-value client mid-year, a higher limit prevents you from falling out of compliance. For a broader look at how these policies function across different sectors, see our What is Professional Indemnity Insurance? A Guide.

How to Manage and Reduce Your Insurance Costs

Managing your accountants professional indemnity insurance cost effectively requires a shift in perspective. You should view your proposal form as a marketing document rather than a simple administrative task. By demonstrating robust internal risk management procedures, you provide underwriters with the confidence needed to offer a more competitive rate. Documented peer reviews, strict diary systems for deadlines, and regular staff training are all indicators of a practice that is less likely to trigger a claim.

Transparency is your best tool during the application process. Full disclosure of your firm’s activities and history prevents future claims from being rejected and builds a rapport with insurers. While it’s tempting to select a high excess to reduce the immediate premium, you must balance these savings against the potential out-of-pocket costs of a claim. Remember to stay within the ICAEW or ACCA permitted excess limits discussed in the previous section. Consolidating your various covers with a single broker can also unlock multi-policy discounts that further optimize your annual spend.

Presenting Your Firm to Underwriters

When completing your proposal form, highlight your strengths like low staff turnover and the consistent use of robust engagement letters. These letters are your first line of defense in mitigating negligence claims because they clearly define the scope of your work and the limits of your liability. In 2026, a clean claims record is worth its weight in gold. If you’ve had past issues, provide a detailed explanation of the remedial actions you’ve taken to prevent a recurrence. This proactive approach often results in a more favorable assessment than simply leaving the underwriter to guess about your risk profile.

Why Cheap Isn’t Always Cheaper

It’s vital to avoid the trap of budget policies that appear attractive but fail to meet the standards of your professional body. Non-compliant policies can leave you exposed to significant regulatory fines and may not cover the specific risks of your practice. Many low-cost options contain hidden exclusions for high-value services like tax advice or probate, which could cost you thousands if a claim arises. For a broader view of what your practice needs to stay protected, you can review our Small Business Insurance Checklist.

Securing the right protection at the right price doesn’t have to be a complex or solo effort. You can speak with our specialist team to navigate these cost-saving strategies while ensuring your firm remains in total compliance with your regulatory body.

Why Use Just Quote Me for Your Accountants PI Insurance?

With over 30 years of experience as an independent broker, we’ve built a reputation for providing reliable, expert guidance to firms across Staffordshire and the West Midlands. We understand that your practice is unique, which is why we don’t rely on rigid algorithms or one-size-fits-all automated systems. Instead, we take the time to talk to you directly. This human-centric approach allows us to understand the nuances of your services, whether you specialize in high-stakes forensic accounting or complex insolvency cases. By presenting your specific “risk story” to our broad network of UK underwriters, we ensure the accountants professional indemnity insurance cost reflects your actual practice profile rather than a generic industry average.

This tailored approach is particularly beneficial for dedicated firms like small business accountants Alloa, where a clear presentation of their professional standards can lead to more accurate and competitive premium assessments.

Our status as an independent broker gives us access to a wide range of insurers, including those on the essential ICAEW participating list. This is critical for maintaining your regulatory compliance. We also provide expert advice on creating a comprehensive protection package by combining your PI with Public Liability and Employers Liability insurance. Consolidating these policies with a single, trusted partner simplifies your administration and often leads to more competitive overall premiums. We manage the complex paperwork and regulatory checks so you can focus on delivering value to your clients.

The Local Broker Advantage in Stafford and Stone

Regional expertise matters when you’re navigating a complex insurance market. For firms based in Stafford, Stone, and the wider West Midlands, having a local partner means you aren’t just a policy number in a distant database. We provide personalized support throughout the lifetime of your policy, which is especially vital during the claims process. You won’t be directed to a generic call center; you’ll speak with experts who understand the local business landscape and the specific pressures facing UK accountancy practices today. We handle the heavy lifting of insurance management, ensuring your firm remains protected and compliant without the usual administrative headaches.

Get Your Quote Today

It’s time to see how much you could save on your accountants professional indemnity insurance cost without compromising on the quality or compliance of your cover. Our team is ready to provide the bespoke service and specialized knowledge your practice deserves.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Securing a Compliant and Cost-Effective Practice

Staying ahead of regulatory shifts from the ICAEW and ACCA is no longer just about meeting a mandate; it’s about the long-term stability of your firm. By focusing on documented risk management and clear engagement letters, you can actively influence the accountants professional indemnity insurance cost while ensuring your personal assets remain shielded. The shift toward risk-based underwriting in 2026 means that your practice’s specific internal “hygiene” is more valuable than ever before.

At Just Quote Me, we bring over 30 years of industry experience and bespoke UK underwriter access to every policy we handle. As an FCA Authorised and Regulated broker, we move beyond automated systems to provide the straightforward, expert advice your practice requires. Whether you’re managing a small bookkeeping firm or a large multi-partner practice, we’re here to simplify the administrative burden and secure the most competitive terms available. You can explore our professional indemnity solutions to find a policy that fits your specific needs.

Ready to protect your practice?

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Take the next step toward a more secure and cost-effective future for your practice today. We look forward to helping you navigate the market with confidence.

Frequently Asked Questions

Is professional indemnity insurance tax-deductible for UK accountants?

Yes, professional indemnity insurance is considered a “wholly and exclusively” business expense by HMRC. This means you can deduct the full premium from your taxable income to reduce your overall tax liability. It’s one of the few ways to offset the necessary accountants professional indemnity insurance cost against your practice’s bottom line while ensuring you stay compliant with your regulatory body.

What is the minimum PI cover required for an ICAEW member in 2026?

For firms with a gross fee income under £800,000, the ICAEW requires a minimum indemnity of two and a half times that income, with an absolute floor of £250,000. For most other firms, the mandatory limit is £2 million for any one claim and in aggregate. These regulations, which were updated in September 2024, ensure practitioners maintain adequate protection tailored to their specific risk level.

How much does professional indemnity insurance cost for a sole trader accountant?

The premium for a sole trader is typically calculated as a percentage of your annual fee income, which often ranges from 0.3% to 1.5%. While minimum premiums apply, your specific rate depends on the high-risk services you offer and your past claims history. Seeking a bespoke quote from a specialist broker ensures you don’t pay for unnecessary cover while meeting all mandatory professional requirements.

Can I change my PI insurance broker mid-policy if costs are too high?

You can technically change brokers at any time, but it’s often more efficient to wait until your renewal date. Cancelling a policy mid-term may result in short-period cancellation rates or the loss of pro-rata refunds from your insurer. If you’re unhappy with your current service or costs, it’s best to start the quoting process with a new broker roughly 60 days before your policy expires.

Does PI insurance cover claims related to tax investigation fees?

Standard professional indemnity insurance covers you if a client sues for negligence regarding tax advice you provided. However, it doesn’t typically cover the professional fees incurred during a routine HMRC tax investigation into a client’s affairs. For that specific protection, you’ll need “Tax Fee Protection” insurance, which is often available as a separate add-on or a standalone policy.

What happens if I stop practicing? Do I still need to pay for insurance?

Yes, you must maintain “run-off” cover once you stop practicing to protect against claims arising from work done in the past. The ICAEW requires a minimum of two years of run-off cover, while the ACCA mandates a full six years. This is essential because PI insurance is “claims-made,” meaning the policy must be active when the claim is filed, regardless of when the error occurred.

Is cyber insurance included in a standard accountants professional indemnity policy?

Cyber insurance is usually not included in a standard PI policy and must be purchased as a separate product. While some PI policies offer limited extensions for data loss, they rarely cover the full costs of ransomware, data breach notifications, or business interruption. Given the sensitivity of financial data, many firms now combine their PI with a dedicated cyber policy for total security.

How do I calculate my gross fee income for the insurance proposal form?

You should calculate your gross fee income by totaling all fees billed to clients during your last full financial year, excluding VAT and disbursements. If you’re a new practice, you’ll need to provide a realistic estimate for the coming 12 months. Accuracy is vital during this process, as under-reporting your income can lead to the accountants professional indemnity insurance cost being miscalculated and claims being rejected.

Article by

Just Quote Me

JustQuoteMe Ltd is an independent UK insurance brokerage specialising in business and personal insurance solutions. With over 35 years of industry experience, the company provides tailored insurance cover for businesses, landlords, tradespeople, hospitality venues, fleets, and individuals across the UK. Known for its personal service, expert advice, and competitive premiums, JustQuoteMe Ltd works with leading insurers to deliver bespoke policies designed around each client’s unique needs. The company is authorised and regulated by the Financial Conduct Authority (FCA No. 586607) and has built a reputation for trusted, straightforward insurance guidance and long-term client relationships.

by jqm | Jul 2, 2026 | Insurance

Could one piece of misunderstood advice or a minor oversight in a high-value contract result in a claim that ends your career? As a consultant, your expertise is your product, but it’s also your greatest liability. We know that navigating the fine print of policy documents often feels like a distraction from your actual work. However, securing the right insurance for business consultants uk isn’t just about ticking a box. It’s about building a fortress around your professional reputation and your financial stability.

You’ve worked hard to establish yourself as a reliable expert, and you shouldn’t have to worry about the financial impact of a legal challenge or a strict contract clause. This guide clears away the jargon to show you exactly which covers are essential for your specific niche. We’ll explore the critical “Big Three” policies and look at the 2026 regulatory updates, including the latest Statutory Sick Pay rules and the increased legal duty to prevent workplace harassment. By the end of this article, you’ll have a clear roadmap to total compliance and the peace of mind to focus entirely on delivering results for your clients.

Key Takeaways

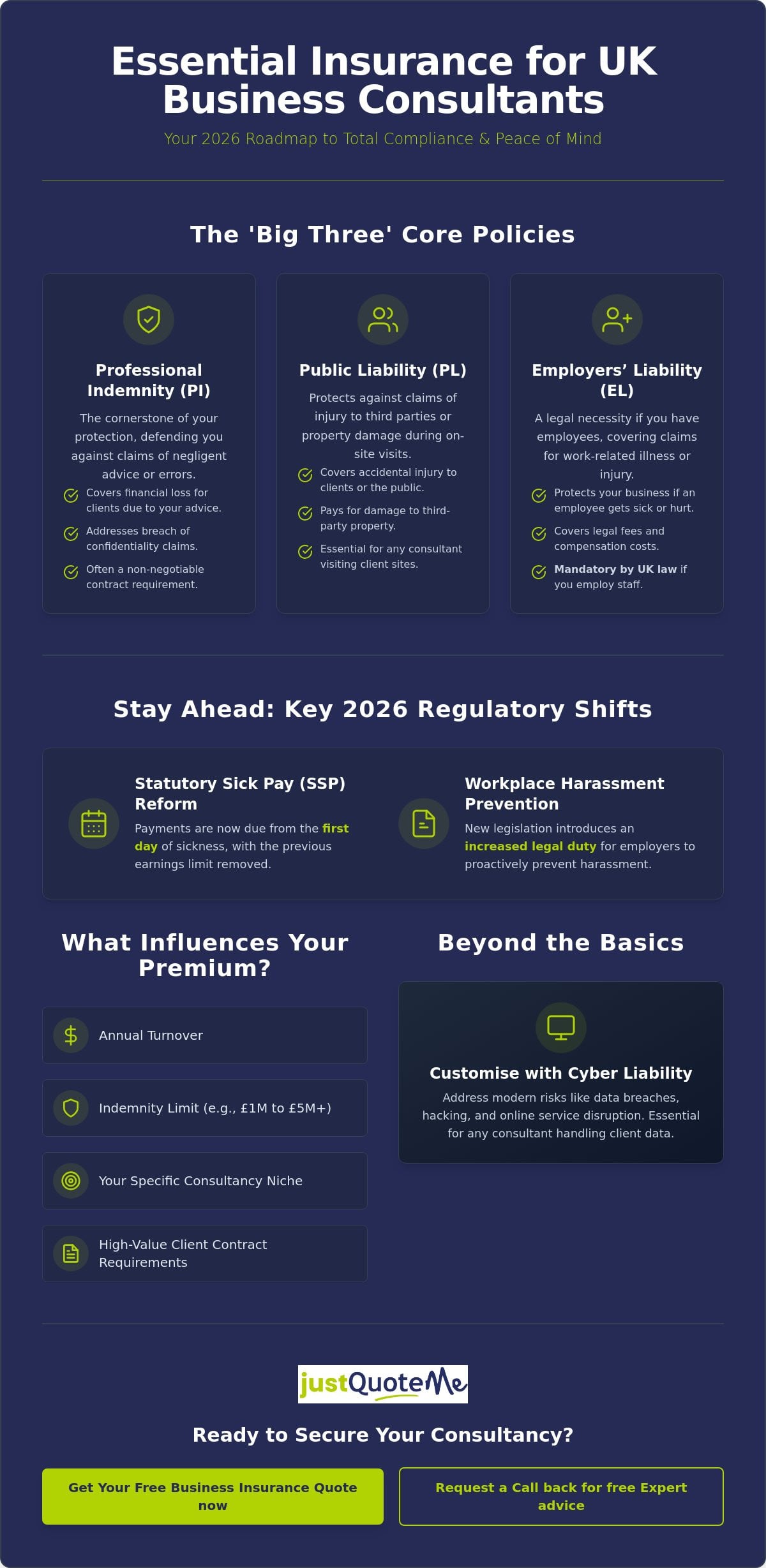

- Identify the essential “Big Three” policies—Professional Indemnity, Public Liability, and Employers’ Liability—that form the foundation of comprehensive insurance for business consultants uk.

- Learn how to customise your coverage based on your specific consultancy niche, ensuring you address modern risks like Cyber Liability without paying for unnecessary extras.

- Stay ahead of 2026 regulatory shifts, including new Statutory Sick Pay requirements and updated legal duties regarding workplace harassment prevention.

- Understand the specific factors that influence your premium costs, from your annual turnover to the indemnity limits required by high-value client contracts.

- Discover the benefits of working with an independent broker to secure a human-centric, flexible policy that adapts as your business grows.

Essential Insurance for Business Consultants in the UK: Why It Matters

Insurance for business consultants uk is more than just a defensive measure; it’s a strategic asset that safeguards your professional standing. While a traditional retailer might worry about physical stock or property damage, your primary risk lies in the intangible. You sell expertise, strategy, and advice. If a client follows your recommendation and suffers a financial loss, you are the one held accountable. This makes a tailored insurance package the foundation of a stable consultancy business.

The regulatory environment for 2026 has introduced several new pressures for UK firms that make robust cover even more critical. From April 2026, changes to Statutory Sick Pay (SSP) mean payments are now due from the first day of sickness, removing the previous earnings limit. Furthermore, new legislation regarding umbrella company liability and increased duties to prevent workplace harassment mean your administrative and legal risks have grown. Having the right protection in place ensures these shifting rules don’t derail your operations.

Beyond legal safety, insurance acts as a powerful trust signal. In a competitive market, being able to provide an insurance certificate immediately can be the difference between winning a contract or losing it to a rival. It demonstrates that you are a professional who understands risk management and has the financial backing to stand by your work.

The Risk of Professional Advice

Consultants occupy a unique position because their product is intellectual property. There’s a significant difference between “doing” work and “advising” on it. When you provide a report or a strategy, you’re essentially guaranteeing its validity. A single calculation error or a misinterpreted data point can lead to massive financial damages for your client. This is why Professional Indemnity Insurance is so vital for the industry. It covers your legal costs and any compensation payments if a client alleges your advice was flawed. Consider a management consultant whose cost-saving strategy inadvertently causes a client to breach a high-value contract. Without Professional Indemnity Insurance, the legal fees alone could be enough to bankrupt a small consultancy.

Meeting Contractual Obligations

Most UK corporate clients and local authorities won’t even consider signing a contract without seeing proof of cover. In 2026, it’s standard to see requirements for indemnity limits of at least £1 million, while larger firms often demand £5 million or more. High-value contracts frequently include strict clauses regarding Public Liability Insurance to cover any accidental damage or injury during on-site visits. Having these policies ready to go speeds up your onboarding process. It shows you’re prepared and reliable, allowing you to move from the proposal stage to delivery without administrative delays.

The ‘Big Three’ Covers: Professional Indemnity, Public Liability, and Employers’ Liability

While every firm has unique needs, most insurance for business consultants uk packages focus on three primary areas of risk. One is mandated by law, one is almost always required by clients, and the third protects your physical interactions with the world. Understanding the difference between a commercial necessity and a legal obligation is vital for your financial health. If you’re unsure which applies to your current project, you can speak with a specialist to clarify your needs.

Professional Indemnity (PI) Insurance

Professional Indemnity Insurance is the cornerstone of your protection. It’s the primary defense for consultants because it addresses the core of what you do: providing advice. If a client claims your strategy led to a breach of confidentiality or caused them a significant financial loss due to negligence, PI covers the legal fees and any resulting compensation. It’s often a non-negotiable requirement in UK management consultancy contracts. Even if you haven’t made a mistake, the cost of defending a meritless claim can be devastating without this cover in place.

Public Liability (PL) Insurance

While PI covers your advice, Public Liability Insurance covers your physical presence. This policy protects you against claims of third-party injury or property damage. You might think it’s unnecessary if you work from home, but even occasional site visits or hosting a client for coffee carries risk. A spilled drink over a client’s laptop or a trip over a loose cable in your office could lead to a claim. Most corporate sites and local authorities will require proof of PL before allowing you through the doors for a project.

Employers’ Liability (EL) Insurance

Unlike other covers, Employers’ Liability Insurance is a strict legal requirement for Employers’ Liability insurance if you employ at least one person. This includes part-time staff and temporary contractors. The law requires a minimum of £5 million in cover, though most policies provide £10 million as standard. Fines for non-compliance are severe; the Health and Safety Executive (HSE) can charge up to £2,500 for each day you operate without a certificate. Only sole traders and some family-run businesses are exempt from this requirement.

Finally, don’t overlook “Run-off cover” when setting up your insurance for business consultants uk. Professional Indemnity claims can arise years after a project ends. If you plan to retire or change careers, this extension ensures you remain protected against claims relating to past work, providing long-term security for your personal assets and professional reputation.

Beyond the Basics: Tailoring Your Policy to Your Consultancy Niche

A general policy might cover the basics, but it often leaves gaps or charges you for protection you’ll never use. Effective insurance for business consultants uk requires a granular look at your specific daily activities. For example, a marketing consultant needs protection against copyright infringement, while a management consultant focusing on strategy needs robust coverage for financial loss advice. By building a bespoke policy, you ensure every pound of your premium is working to protect a real-world risk rather than subsidising covers irrelevant to your niche.

The rise of digital threats in 2026 has made Cyber Insurance a critical addition for any consultant handling client data. If you manage digital assets or store sensitive information on your local devices, standard professional indemnity might not cover the full cost of a data breach. A dedicated cyber policy helps manage the fallout of a cyber attack, covering notification costs, system restoration, and even legal defense if you’re sued for losing third-party data. It’s a proactive way to maintain client trust even in a crisis.

IT and Tech Consultants

Tech-focused roles carry a heavy burden of responsibility regarding system integrity. If you’re implementing software or managing a cloud migration, a failure can cause immediate operational paralysis for your client. Because of this, professional indemnity limits for tech consultants are typically higher than in other sectors to account for these massive potential losses. You should also consider protecting your physical assets. If you’re frequently travelling to client sites with high-spec laptops or specialised testing equipment, ensuring your physical tools are protected against theft or accidental damage is a pragmatic step that prevents out-of-pocket replacement costs.

HR, Recruitment, and Management Consultants

If your work involves personnel advice or strategic restructuring, your risks are more human-centric. You deal with sensitive employment law and confidential corporate data daily. Claims in this sector often revolve around defamation, breach of confidentiality, or alleged errors in recruitment processes that lead to “wrongful hire” lawsuits. Additionally, the legal landscape for 2026 includes stricter IR35 enforcement and complex tax investigations. Adding “Legal Expenses” cover to your policy provides the financial backing to defend yourself during HMRC disputes or employment tribunals. This is especially vital given the new six-month time limit for tribunal claims introduced in October 2026, which gives disgruntled parties more time to initiate legal action against your business. Securing the right insurance for business consultants uk means accounting for these specific legal timelines.

Calculating the Real Cost of Consultant Insurance in 2026

Finding the right balance between cost and protection starts with understanding how insurers price your specific risk. When you search for insurance for business consultants uk, you’ll notice that premiums aren’t a flat rate. Instead, they reflect your business’s unique profile. Insurers look at the probability of a claim and the potential cost of settling it based on your sector and contract values. It’s a logical process that rewards transparency and a solid professional history.

Don’t fall for the trap of choosing the lowest headline price without checking the fine print. Very cheap policies often lack “any one claim” protection. This means your total indemnity limit might be an aggregate for the whole year, rather than applying to each separate claim. If you face more than one legal challenge in a single policy period, you could find your cover exhausted before the second claim is even heard. A robust policy ensures your limit resets for every new incident.

Factors Influencing Your Premium

Your annual turnover and the size of the contracts you advise on are the biggest influences on your premium. Advising a multinational on a strategy worth millions carries more risk than helping a local small business—such as those featured on Anglia Market—with their social media presence. Your level of experience also matters; insurers view a consultant with a decade of claims-free history as a lower risk than someone just starting out. The sector you consult for changes the math too. High-risk industries like Oil and Gas generally command higher premiums than lower-stakes sectors like Retail due to the potential scale of financial loss if something goes wrong.

Ways to Manage Insurance Costs

One of the best ways to keep costs down is to bundle your Professional Indemnity Insurance and other core covers into a single policy. This is often more efficient than managing multiple separate renewals. You might also consider increasing your voluntary excess. By agreeing to pay a slightly higher amount toward any claim, you can often secure a lower annual premium. However, always make sure you have the funds available to cover that excess at short notice. To see how these factors apply to your specific consultancy, you can get a personalised assessment of your insurance needs today.