Would your current insurance policy hold up if a routine transit for a high-net-worth client turned into a high-stakes security incident? You understand that close protection work is fundamentally different from standard security roles, yet many generalist brokers fail to grasp the high-risk nature of your environment. It’s frustrating to find that your Close Protection insurance contains hidden exclusions for hostile zones or lacks the necessary cover for the carriage of firearms just when you need it most.

We agree that your professional liability shouldn’t be left to chance or buried under layers of complex corporate jargon. This article will show you how to secure comprehensive, SIA-compliant cover that protects your career, your clients, and your reputation. You’ll discover the essential requirements for 2026, including the mandatory refresher training and Level 3 First Aid qualifications now required for licence renewals. We will also clarify the critical differences between personal and corporate liability to ensure you have total peace of mind on every contract. Just Quote Me simplifies this complex administrative process, acting as your trusted advisor so you can stay focused on the task at hand.

Key Takeaways

- Learn the critical distinction between generic bodyguard policies and specialist professional wording to ensure your cover meets high-end contract requirements.

- Understand how to balance Public Liability and Professional Indemnity to protect against both physical incidents and advice-based liability.

- Discover the specific endorsements needed for high-risk scenarios, including hostile environment work and the legal carriage of firearms.

- Master the process of verifying your ‘Statement of Fact’ to guarantee that your Close Protection insurance remains valid across all operational zones.

- Gain peace of mind by partnering with a trusted advisor who understands the nuances of the security industry and simplifies complex administrative tasks.

What is Close Protection Insurance and Why is it Critical?

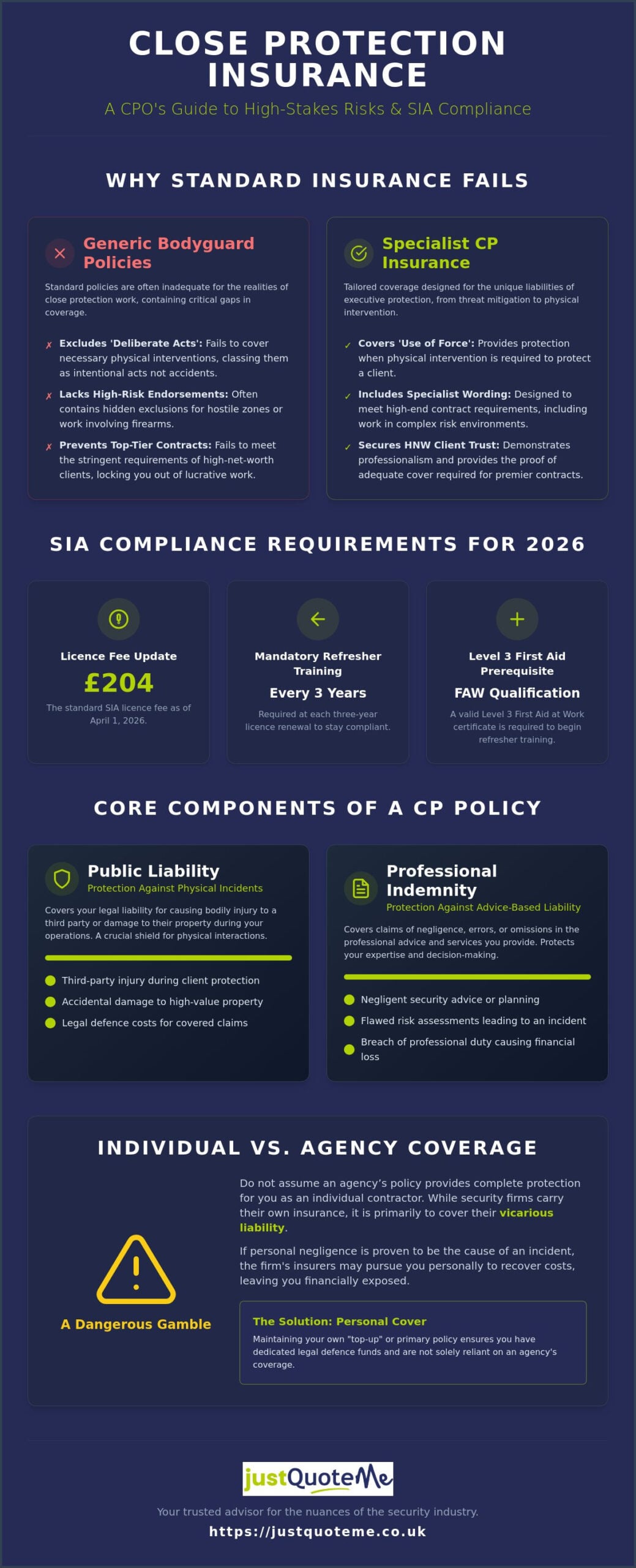

Many people use the terms “bodyguard” and “Close Protection Officer” interchangeably, but in the insurance market, the distinction is vital. A bodyguard might imply a generic physical presence, whereas a What is a Close Protection Officer? is a trained professional managing complex, fluid risk environments. Close Protection insurance is a calibrated suite of protections designed specifically for these high-stakes scenarios. It goes beyond basic coverage to address the unique liabilities of executive protection, from threat mitigation to physical intervention.

Standard public liability insurance often fails the modern CPO. Most general policies exclude “deliberate acts” or high-risk security activities, leaving you exposed if a routine task requires physical force. For professionals working with high-net-worth (HNW) individuals or celebrities, specialist insurance is a prerequisite for securing contracts. These clients require proof that your policy understands the nuances of their lifestyle and the specific threats they face. Without it, you aren’t just risking a claim; you’re effectively locked out of the most lucrative sectors of the industry.

SIA Compliance and Legal Requirements for 2026

Staying compliant is a moving target. As of April 1, 2026, the SIA licence fee is £204, and the regulatory requirements have become more stringent. You now must complete mandatory refresher training at every three-year renewal. To even begin this training, you’re required to hold a valid Level 3 First Aid at Work (FAW) qualification. Your Close Protection insurance must align with these standards to remain valid. Operating without adequate professional indemnity insurance can lead to severe legal repercussions, especially if a client alleges that your security advice or risk assessment was negligent. Just Quote Me ensures your policy reflects these current UK standards, keeping your career on solid legal ground.

Individual Operatives vs. Security Firms

If you’re a contractor, don’t assume an agency’s policy provides total protection. While firms often carry security insurance to cover vicarious liability, they may still pursue individual operatives for costs if personal negligence is proven. Many CPOs choose to maintain their own “top-up” or primary policies to ensure they have dedicated legal defence funds. Relying solely on a client’s or agency’s policy is a dangerous gamble that can leave you personally liable for damages. Just Quote Me provides the specialized expertise needed to identify these gaps, offering a human-centric approach to complex risks that automated platforms simply can’t match.

Request a Call back for free Expert advice

The Core Components of a Comprehensive CP Policy

A robust Close Protection insurance policy acts as a multi-layered shield. It doesn’t just tick boxes for Official UK Licensing Standards; it provides a financial safety net for the diverse risks encountered in the field. A professional policy isn’t a single product but a combination of several essential covers tailored to your specific role. Understanding how these components interact is the first step toward total career security.

Public Liability: Beyond the Basics

Standard Public Liability Insurance usually covers accidental slips and trips. In the world of close protection, however, you need cover that accounts for ‘use of force’. If you’re required to physically intervene to protect a client and a third party is injured, a generic policy might deny the claim. Specialist CP wording ensures you’re protected during these high-pressure moments. This cover also extends to property damage. Imagine you’re securing a perimeter at an HNW estate and a piece of expensive equipment or bespoke furniture is damaged. The repair bills for high-end assets can easily exceed an operative’s annual earnings, making this protection indispensable.

Professional Indemnity for Security Consultants

While liability covers the physical, Professional Indemnity Insurance covers your intellectual output. Senior operatives often provide detailed threat assessments or security planning. If a client believes your advice was negligent and led to a security breach, they may seek damages for financial or reputational loss. For high-profile individuals, a breach isn’t just a safety issue; it’s a massive PR crisis. PI is the most overlooked cover for senior CPOs, yet it’s vital for anyone moving into a consultancy or management capacity where risk assessments are the primary deliverable.

Beyond these, you must consider Employers’ Liability Insurance if you hire staff or use sub-contractors on a detail. It’s a legal necessity in the UK. Finally, Personal Accident and Medical Expenses cover provides a vital safety net for you. In a role where physical risk is a daily reality, ensuring you have financial support for medical costs or loss of income is essential. Building a policy with these components ensures your Close Protection insurance is fit for purpose. You can explore our specialized security options to see how these covers fit your specific operational profile.

Request a Call back for free Expert advice

Navigating High-Risk and Specialized CP Scenarios

Operational environments for Close Protection Officers (CPOs) aren’t limited to the safe streets of London. As you move into Hostile Environment Close Protection (HECP) or maritime security, the risk profile changes drastically. Standard Close Protection insurance often includes strict territorial limits that stop at the UK border or exclude specific “red-listed” conflict zones. If you’re operating in high-risk regions, your policy must be explicitly extended to include repatriation and emergency evacuation clauses. This ensures you aren’t left stranded or facing ruinous medical bills if a situation deteriorates rapidly. Under the Private Security Industry Act 2001, the legal burden of care and liability is significant, making it essential that your cover follows you wherever the contract leads.

International and Hostile Zone Coverage

Working overseas requires a deep dive into your policy’s fine print. Many operatives discover too late that their cover doesn’t extend to “local labour,” such as drivers or fixers hired on the ground. If a local contractor’s action leads to a claim, your policy needs to clearly define who is covered and to what extent. You should also verify that your evacuation cover includes political risk as well as medical emergencies. Just Quote Me acts as your steady hand in these complex markets, ensuring every operational nuance is disclosed in your Statement of Fact to prevent claim denials based on geographic exclusions.

Specialist Risks: Firearms and K9 Units

Carriage of firearms is perhaps the most sensitive area of specialist cover. Most insurers won’t touch armed details without a specific “Carriage of Firearms” endorsement. This requires a rigorous disclosure of your training, the legal framework of the host country, and the specific rules of engagement. Similarly, if your detail utilizes K9 units for explosive detection or patrol, your liability extends to the actions of the animal. A handler is only as protected as their policy’s wording allows. You can find more detail on these specific endorsements through our Security Insurance page, where we break down the requirements for specialized teams.

Asset protection often goes hand-in-hand with person protection. When you’re tasked with securing high-value goods, jewelry, or sensitive data alongside a client, your insurance must reflect this dual responsibility. This is where a human-centric approach to insurance pays off. By discussing your specific contract requirements with a broker who understands the industry, you can avoid the hidden exclusions that automated systems often miss. We help you navigate these high-stakes scenarios with clarity and professional restraint, ensuring your reputation remains as protected as your clients.

Request a Call back for free Expert advice

How to Choose the Right Close Protection Insurance

Selecting the right Close Protection insurance requires a tactical mindset similar to planning a security detail. You wouldn’t enter a high-risk zone without a reconnaissance report; you shouldn’t sign an insurance contract without a thorough audit of the terms. The process should be systematic, moving from a broad assessment of your needs to the fine print of your policy wording.

- Step 1: Conduct a thorough personal and operational risk assessment. This goes beyond your current contract. Consider the maximum potential loss you could face, including legal fees and compensation.

- Step 2: Verify the ‘Statement of Fact’. Ensure every risk is disclosed with absolute precision. Any undisclosed activity, such as a planned trip to a high-risk region, can void your cover entirely.

- Step 3: Compare policy exclusions as carefully as the premiums. A lower price often indicates broader exclusions, particularly regarding ‘use of force’ or specific territorial limits.

- Step 4: Check the insurer’s reputation for handling security-sector claims. A general insurer may lack the expertise to handle a complex claim involving professional negligence in a security context.

- Step 5: Review your limits of indemnity against your largest contract. High-net-worth clients often mandate specific minimum levels of cover, sometimes exceeding £5 million or £10 million.

Common Mistakes to Avoid When Quoting

Many operatives underestimate the ‘use of force’ risk in their declarations. They assume standard public liability insurance covers physical intervention, but this is rarely the case without specialist wording. Choosing ‘cheap’ over ‘comprehensive’ is another frequent error. The true cost of a rejected claim is far higher than any annual premium saving. You must also update your broker whenever your operational environment changes. A policy that covers you in London may not provide the same protection if your contract moves to a developing nation or involves higher-risk assets.

The Role of a Specialist Broker

Generic comparison sites fail the security industry because they rely on automated algorithms that don’t understand the nuances of close protection. A specialist broker provides access to exclusive Lloyds of London syndicates that specifically appetite security risks. This human-centric approach ensures your Close Protection insurance is bespoke rather than a generic template. You can secure specialist security cover that reflects your actual daily risks rather than a best-guess estimate. If you’re unsure how to align your policy with the new 2026 SIA standards, you should Request a Call back for free Expert advice to tailor your policy to your specific needs.

Request a Call back for free Expert advice

Secure Your Career with Just Quote Me

Securing the right Close Protection insurance shouldn’t feel like a second job. At Just Quote Me, we’ve spent over 30 years refining our approach to bespoke UK business insurance. We know that in the security sector, your reputation is your most valuable asset. That’s why we don’t rely on automated, one-size-fits-all systems. Instead, we provide a human-centric service that addresses the specific, high-risk nature of your work. Our team acts as a steady hand, navigating the complex administrative burdens so you can stay focused on protecting your clients.

The 2026 security landscape is more regulated than ever. With the SIA’s updated requirements for refresher training and first aid now in full effect, your insurance must be as current as your licence. As an FCA-authorised broker, we provide guidance that’s tailored to these shifts. We ensure your policy isn’t just a piece of paper but a tactical asset that stands up to scrutiny during contract negotiations with HNW individuals or corporate entities. We’re here to make sure your cover is as professional as the service you provide.

Why CPOs Trust Our Expertise

While we have deep roots in the West Midlands and Staffordshire, our reach is national. We understand the nuances of the regional security market but have the leverage to access a panel of top UK security underwriters. This means we can find cover for risks that other brokers often find difficult to place, such as hostile environment work or the specialized needs of maritime security. We support you through the entire lifecycle of your policy. From the initial quote to the event of a claim, we’re there to advocate for you and simplify the process, ensuring you’re never left to manage a crisis alone.

Get Started Today

You don’t have time for endless paperwork or confusing jargon. Our goal is to get you on-site quicker with a policy that actually works. We handle the heavy lifting, from verifying your operational risks to ensuring your limits of indemnity match your largest contracts. We take pride in being a knowledgeable and approachable partner in a complex market. You can explore our broader range of Business Insurance options to see how we protect various professional sectors. When you’re ready to secure your career with Close Protection insurance that offers genuine peace of mind, we make it easy to take the next step.

Request a Call back for free Expert advice

Secure Your Professional Reputation Today

Your role as a security professional requires constant vigilance and a proactive approach to evolving risks. We have covered how a tailored policy ensures SIA compliance for the 2026 landscape and why specialized endorsements for firearms or hostile zones are non-negotiable for high-end contracts. Don’t leave your career to the limitations of generic comparison sites that don’t understand the tactical nature of your work. Relying on standard wording can leave you exposed when your client needs you most.

Just Quote Me brings over 30 years of UK insurance expertise to your side. As an FCA-authorised and regulated broker, we provide access to a specialist security underwriting panel that understands the nuances of HNW and celebrity protection. We manage the administrative complexity so you can focus on your operational duties. It’s time to trade uncertainty for the confidence of a bespoke policy that reflects your daily reality. We are a human-centric partner in a complex market, ready to help you operate with total peace of mind.

Request a Call back for free Expert advice

Frequently Asked Questions

Is Close Protection insurance a legal requirement for individual CPOs?

No, it isn’t a legal requirement for individual operatives in the same way car insurance is, but it’s a professional necessity. Almost all high-net-worth clients and security agencies mandate that you carry your own liability cover before awarding a contract. Without it, you are personally liable for legal costs and damages, which can be financially ruinous even if you’re eventually found not at fault.

Does my policy cover me for work outside of the United Kingdom?

Your policy can cover international work, but it isn’t always automatic. Standard policies often limit cover to the UK or EU, so you must notify your broker if you’re heading to higher-risk regions. Operating in a hostile environment without a specific territorial extension will void your cover. We help you disclose these operational areas correctly to ensure your protection follows you across borders.

What is the difference between Public Liability and Professional Indemnity for a bodyguard?

Public Liability protects you against claims of physical injury or property damage caused during your work. Professional Indemnity, however, covers you if a client suffers a loss because of your security advice or threat assessments. While PL is essential for the physical side of being a bodyguard, PI is vital for the consultancy and planning aspects that senior operatives provide to high-profile clients.

Am I covered if I have to use physical force to protect a client?

You are covered for physical intervention only if your Close Protection insurance includes a specific “use of force” endorsement. Most general liability policies exclude deliberate acts, which can leave a security professional exposed during a crisis. Specialist policies are designed to account for necessary physical contact, provided it is lawful and falls within the scope of your professional duties and training.

How much does Close Protection insurance typically cost in 2026?

The cost of your policy depends on your specific risk profile, contract types, and required indemnity limits. Because close protection involves higher risks than standard guarding, premiums are calculated based on factors like international travel and the profile of your clients. We recommend getting a bespoke quote to ensure you’re paying for the exact level of protection your specific security detail requires.

Does insurance cover the carriage of firearms in hostile environments?

Insurance for the carriage of firearms is a highly specialized endorsement that requires full disclosure of your training and the host nation’s laws. It is not a standard feature and must be negotiated with specialist underwriters who understand armed protection details. You’ll need to demonstrate that your use of firearms is legal and follows strict rules of engagement within the specific hostile environment.

What happens if my SIA licence expires while I have an active policy?

An expired SIA licence will likely invalidate your insurance for any activities that legally require a licence to perform. Most policies include a condition that you must remain fully compliant with official licensing standards. With the 2026 mandatory refresher training rules now in place, it’s essential to stay ahead of your renewal dates to avoid any gaps in your professional protection.

Can I get short-term cover for a specific one-off contract?

Short-term Close Protection insurance is available for operatives who only work on specific, one-off contracts throughout the year. This allows you to buy cover for a set duration, such as a single month, rather than committing to an annual policy. It’s a cost-effective solution for contractors who need to meet the insurance requirements of a high-value detail without the overhead of a full year’s premium.

Request a Call back for free Expert advice