by jqm | Aug 5, 2026 | Insurance

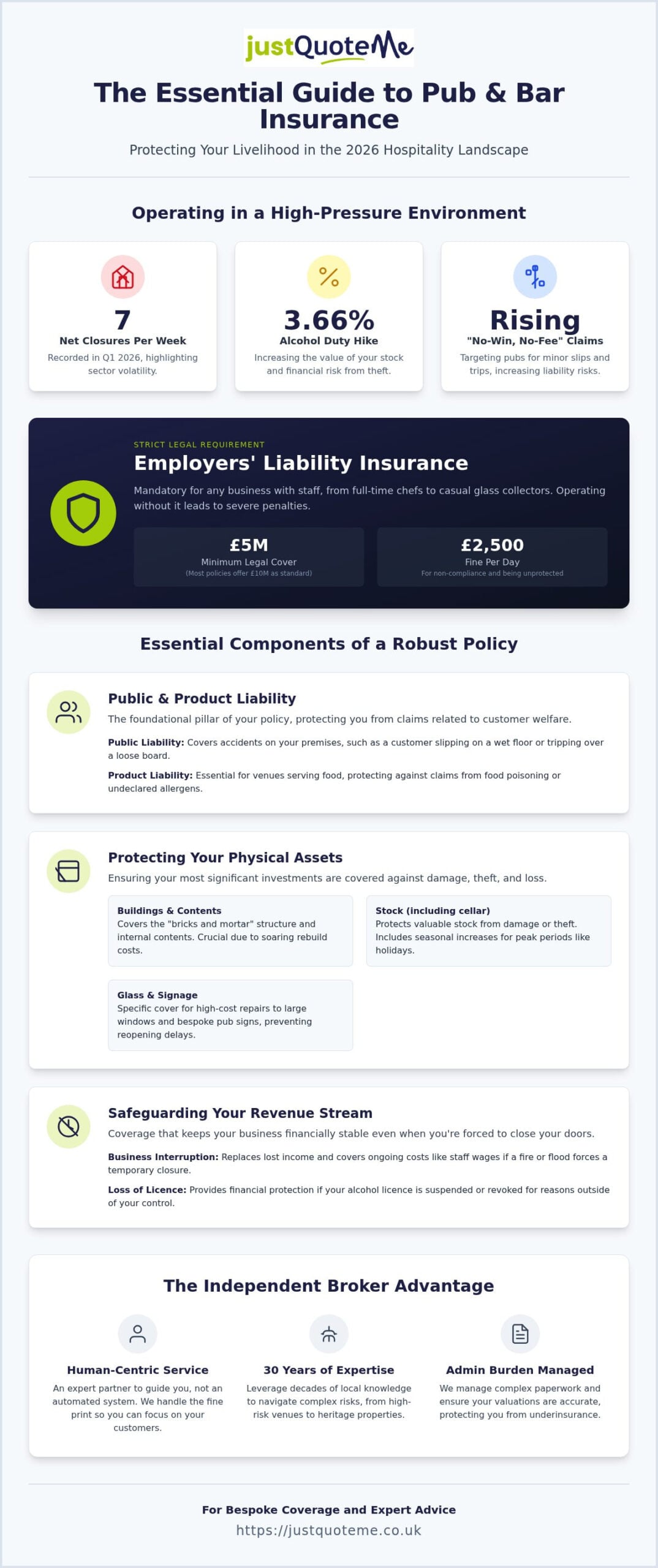

With seven net closures per week recorded in the first quarter of 2026, the UK hospitality sector is operating in a high-pressure environment where securing the right Pub and Bar Insurance is essential for survival. You’re likely feeling the weight of the 3.66% alcohol duty hike from earlier this year, alongside the persistent anxiety that a single public liability claim from a slip or trip could jeopardize everything you’ve built. It’s frustrating when high premiums feel like a penalty for the inherent risks of the trade, especially when combined with the confusion surrounding specialized covers like “Loss of Licence.”

We believe that protecting your livelihood shouldn’t be a source of stress. This guide is designed to help you secure bespoke coverage that addresses your specific needs, from regulatory compliance to financial protection against theft and damage. You’ll learn exactly which covers are legal requirements, such as the £5 million minimum for employers’ liability, and how to safeguard your premises against evolving risks. We’ll preview the essential steps to simplify your admin and provide the peace of mind you need to focus on your customers, not your paperwork.

Key Takeaways

- Learn why generic business insurance often leaves hospitality venues exposed and how a bespoke policy fills those critical gaps.

- Understand the fundamental components of comprehensive Pub and Bar Insurance, including public and product liability to protect against customer accidents and food safety claims.

- Discover tailored solutions for high-risk or heritage premises, such as thatched pubs and nightclubs, where fire risks and unique underwriting are required.

- Identify proactive risk management strategies and safety documentation practices that can help stabilize and lower your insurance premiums over time.

- Find out how partnering with an independent broker provides a human-centric alternative to automated systems, leveraging 30 years of local expertise to handle your administrative burdens.

Navigating the Risks of the UK Hospitality Sector in 2026

Operating a licensed venue in 2026 involves more than just pulling pints and managing bookings. Pub and Bar Insurance is a multi-layered commercial policy designed to protect your livelihood from the specific hazards of the hospitality trade. While a standard business policy might suffice for a quiet retail shop, it often fails the hospitality sector because it doesn’t account for the volatile nature of alcohol-led environments. From broken glass and late-night altercations to the complexities of UK alcohol licensing laws, your risks are unique. A bespoke policy ensures that you aren’t paying for generic cover you don’t need, while simultaneously plugging the dangerous gaps that “off-the-shelf” insurance leaves wide open.

The Legal Requirements for UK Licensees

Compliance isn’t optional. If you have any staff, whether they’re full-time chefs or casual weekend glass collectors, Employers Liability Insurance is a strict legal requirement under the 1969 Act. You must have at least £5 million in cover, though most insurers provide £10 million as a standard. Failing to display a valid certificate or operating without this cover can result in fines of up to £2,500 for every single day you’re unprotected. This legal framework ties directly into the Health and Safety at Work Act, which mandates a safe environment for everyone on your premises. Underinsurance is a common pitfall; if your cover limits don’t reflect the true scale of a potential claim, you could be held personally liable for the shortfall, which often leads to business insolvency.

Why 2026 Demands More Than Basic Coverage

The economic landscape of 2026 has introduced new pressures that basic policies simply can’t handle. Inflation has caused rebuild costs for historic and commercial properties to soar, meaning a policy written two years ago might now leave you significantly underinsured if a fire occurs. Additionally, the 3.66% increase in alcohol duty seen in February 2026 means your stock is more valuable than ever. Theft or cellar damage now represents a much larger financial blow to your bottom line. We’ve also seen a rise in “no-win, no-fee” litigation targeting pubs for minor slips or trips. Just Quote Me acts as your professional partner, managing these complex administrative burdens and ensuring your valuations are accurate. We move you quickly from uncertainty to total protection, so you can focus on running your venue while we handle the fine print.

Essential Components of a Robust Pub and Bar Policy

A standard Pub and Bar Insurance policy acts as a safety net, but a robust one serves as a foundation for your entire business. It’s not just about meeting basic requirements; it’s about building a shield around your assets, your staff, and your reputation. Public Liability remains a primary pillar, protecting you from the financial fallout if a customer slips on a spilled drink or trips over a loose floorboard. Equally vital is Product Liability. As food offerings become more central to the UK pub model, this cover protects you if a patron falls ill due to contaminated food or an undeclared allergen. These components work together to ensure that a single accident doesn’t lead to a devastating legal bill.

Protecting Your Assets: Buildings, Stock, and Glass

Your physical venue is often your most significant investment. Commercial Property Insurance provides the necessary protection for the bricks and mortar of your establishment, whether you own the building or are responsible for it under a lease. Beyond the walls, you must consider your contents. In 2026, the value of spirits and cellar stock has risen significantly due to duty increases and supply chain shifts. Your policy should include seasonal increases to account for busier periods like the festive season or bank holidays, when your stock levels naturally peak. We also recommend specific glass and signage cover. Replacing a bespoke pub sign or large front windows after an incident is a high-cost repair that can stall your reopening if you’re not properly covered.

Safeguarding Your Revenue: Business Interruption and Licence

Physical damage is only part of the problem. Business Interruption cover is what keeps your business alive if a fire or flood forces you to close your doors. It replaces lost income and helps you cover ongoing costs like staff wages and utility bills while repairs are underway. Perhaps the most critical specific cover for licensees is Loss of Licence. If your ability to sell alcohol is revoked through no fault of your own, this cover provides a financial cushion to help you pivot or recover. Following the official government alcohol licensing guidance is your first line of defense, but insurance is your final safety net. For those working as venue consultants or specialists, Professional Indemnity Insurance is also a necessary consideration to protect against claims of professional negligence. Finding the right balance between these components is easier when you speak to an expert. You can explore tailored cover options that match your specific venue type to ensure no detail is overlooked.

Tailoring Cover for Niche Premises: Thatched Pubs and Nightclubs

A “one size fits all” approach often fails when your business doesn’t fit the standard commercial mold. While a local gastro-pub faces traditional risks, a 17th-century thatched inn or a multi-story city center nightclub operates under entirely different hazard profiles. Generic automated quote systems frequently struggle with these nuances, either rejecting the risk outright or inflating premiums to cover their lack of data. This is where the human element of an independent broker is vital. We use 30 years of experience to present your business to specialist underwriters who understand niche sectors. Securing the right Pub and Bar Insurance for a specialized venue requires a partner who knows how to articulate your risk management efforts to the market.

Heritage and Thatched Pub Insurance

Protecting a historical asset requires Thatched Pub Insurance that recognizes the specific fire hazards inherent in organic roofing materials. Insurers for these properties demand strict adherence to safety standards, including regular chimney sweeping and certified electrical testing. Because many of these venues are listed buildings, rebuild costs are significantly higher due to the requirement for specialist materials and traditional craftsmanship. We help you navigate these requirements, ensuring your policy reflects the true replacement value of your heritage site rather than a generic market average. Our deep roots in Staffordshire and the West Midlands mean we understand the local landscape and the specific challenges heritage licensees face.

Late-Night Venues and Nightclub Risks

Urban bars and venues operating into the early hours face a distinct set of challenges centered around security and public safety. Comprehensive Nightclub Insurance must prioritize door staff liability and crowd management. It is essential to have robust Security Insurance in place to protect your business from claims arising from altercations or ejectments. Adhering to Health and Safety Executive (HSE) guidance regarding workplace violence and slips is a prerequisite for securing favorable terms.

Many late-night venues also overlook the risks associated with specialized maintenance. If your venue features complex lighting rigs or high-end sound systems, you must account for Working at Height risks for your technicians. Whether it’s a fall during a rig setup or a dropped tool hitting a patron, these incidents can lead to massive liability claims. We manage these administrative burdens by identifying these gaps early, ensuring your bespoke policy covers every aspect of your late-night operation from the dance floor to the rafters.

Proactive Risk Management to Lower Your Premiums

Lowering your insurance costs isn’t just about shopping around; it’s about proving to underwriters that your venue is a low-risk environment. Insurers don’t just look at your postcode or your turnover; they look at your safety documentation and your history of claims. By implementing proactive risk management, you create a paper trail of diligence that can lead to significant premium stability over the long term. This approach transforms you from a generic statistic into a preferred client in the eyes of top UK underwriters. We help you identify these opportunities, ensuring your Pub and Bar Insurance reflects the hard work you put into venue safety.

Health, Safety, and Staff Training

The foundation of any risk reduction strategy starts with your team and your daily operations. Following a structured approach can help you mitigate the most common causes of claims:

- Step 1: Regular Risk Assessments. Slips, trips, and falls remain the most frequent cause of public liability claims in the hospitality sector. You should conduct and document regular walk-throughs to identify hazards like loose carpets, wet floors, or poorly lit stairwells.

- Step 2: Responsible Alcohol Service. Training your staff on “Challenge 25” and responsible service isn’t just a licensing requirement; it’s a liability shield. Well-trained staff are better equipped to handle intoxicated patrons safely, reducing the likelihood of altercations or accidents.

- Step 3: Equipment Maintenance. Kitchen fires and electrical faults are major threats to your premises. Regularly maintaining your Plant and Machinery ensures that fryers, extractors, and cellar cooling systems are operating safely and efficiently, preventing catastrophic losses.

Security and Technology Upgrades

Modernizing your venue’s security profile is another direct route to lower premiums. Insurers favor establishments that invest in high-quality, FCA-approved CCTV and alarm systems. These tools act as a deterrent to theft and provide invaluable evidence if a claim is made against you. As the industry moves toward digital booking and payment systems, you must also protect your virtual storefront. Implementing Cyber Insurance protects your business from the financial and reputational damage of data breaches or system hacks. A robust, independent security audit can serve as a powerful bargaining chip to secure lower quotes from underwriters who value proactive protection.

Managing these administrative burdens is where our 30 years of experience becomes your greatest asset. We understand the nuances of the Staffordshire and West Midlands hospitality markets and can help you present your risk management efforts in the best possible light. You can speak with our team for expert advice on how to optimize your venue’s safety profile and reduce your insurance overheads.

Why an Independent Broker is Your Best Asset in 2026

Choosing the right Pub and Bar Insurance shouldn’t feel like a battle against a faceless algorithm. In 2026, the hospitality market is too volatile for “off-the-shelf” solutions that fail to account for your venue’s specific character. While automated quote bots prioritize speed over accuracy, an independent broker offers a human-centric alternative that prioritizes protection. We act as your advocate, using our 30 years of industry experience to negotiate with the market on your behalf. This means we don’t just find you a policy; we build a bespoke shield that fits your business perfectly. This approach ensures you aren’t overpaying for unnecessary cover or, worse, left exposed when it matters most.

The Just Quote Me Difference: 30 Years of Expertise

Our deep roots in Staffordshire and the West Midlands give us a distinct advantage that national call centers simply can’t match. We understand the local trading conditions in Stone, Stafford, and Newcastle-under-Lyme because we’re part of the same community. This regional expertise allows us to provide a more accurate risk profile to our broad network of top-tier UK underwriters. Being an independent broker means we aren’t tied to a single insurance provider. We have the freedom to compare multiple options, ensuring you receive a competitive Pub and Bar Insurance quote that reflects the proactive risk management steps we discussed earlier. Our tone is always straightforward and reassuring, cutting through the legal jargon to give you the clear answers you need.

Simplifying Your Insurance Renewal

The administrative burden of insurance can be overwhelming for a busy licensee. We manage the entire process for you, from the initial inquiry through to the final policy setup. This support doesn’t end once your premium is paid. If the worst happens and you need to make a claim, we handle the complex paperwork and communication with the insurer. You won’t be stuck in a call center queue; you’ll have a dedicated partner who understands your business and works to resolve the claim as quickly as possible. This pragmatic approach saves you time and reduces the stress associated with renewals and unforeseen incidents. We move you quickly from a state of inquiry to total peace of mind, allowing you to focus on delivering the best experience for your patrons.

Securing Your Venue’s Future in 2026

Running a successful hospitality business is a balancing act between tradition and modern compliance. We’ve seen how moving beyond generic, off-the-shelf policies to secure bespoke Pub and Bar Insurance can protect your assets from rising costs and specialized risks like heritage roofing or late-night operations. It’s about total resilience. Proactive risk management isn’t just about safety; it’s a strategic move to stabilize your premiums and prove your venue is a preferred risk to top-tier underwriters.

With over 30 years of independent brokerage experience, Just Quote Me provides the regional expertise that West Midlands and Staffordshire licensees depend on. We offer a human-centric alternative to automated quote bots, giving you direct access to a broad network of insurers and expert advice tailored to your specific needs. Our team manages the complex administrative burdens so you can focus on serving your community with total peace of mind. You don’t have to navigate these challenges alone when you have a trusted advisor in your corner. You can explore our tailored solutions to see how we simplify the process for you.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Frequently Asked Questions

Is public liability insurance a legal requirement for UK pubs?

Public liability insurance isn’t a legal requirement under UK law, but it’s an essential safeguard for any hospitality business. Most commercial landlords and mortgage lenders will mandate this cover as part of your lease agreement. It protects your business from the financial impact of claims made by the public for injuries or property damage that occur on your premises.

What does “Loss of Licence” insurance actually cover?

Loss of Licence insurance provides financial compensation if your premises licence is revoked or suspended due to circumstances beyond your control. This cover typically accounts for the depreciation in the value of your business or the loss of gross profit during the period you’re unable to trade. It’s a vital safety net that helps you manage the administrative and financial fallout of licensing disputes.

How much does pub and bar insurance cost in 2026?

The cost of Pub and Bar Insurance in 2026 depends on several variables, including your venue’s location, annual turnover, and previous claims history. External factors like the standard 12% Insurance Premium Tax (IPT) also influence the final price. Because every establishment has a different risk profile, it’s best to get a tailored quote that reflects your specific operational needs rather than relying on industry averages.

Do I need different insurance if my pub has a thatched roof?

Yes, thatched properties require specialized underwriting because the fire risk is significantly higher than that of standard structures. Standard Pub and Bar Insurance policies often exclude these buildings or have very restrictive terms. You’ll need a dedicated thatched pub policy that accounts for specific safety requirements, such as regular chimney sweeping and certified electrical inspections, to ensure your heritage asset is fully protected.

Does my policy cover outdoor seating areas and beer gardens?

Most comprehensive policies will cover your outdoor seating and beer gardens, provided they’re included in your initial risk assessment. Your public liability protection should extend to these areas to cover slips or trips outside. You must ensure your policy documents explicitly mention these spaces and that you maintain them with the same diligence as your indoor areas to remain compliant with your insurer’s terms.

Can I get insurance for a nightclub or late-night bar?

You can secure specialized cover for late-night venues through dedicated nightclub insurance. These policies are built to handle the higher risks associated with late trading hours, including door staff liability and crowd management. It’s important to work with a broker who understands these nuances, as standard pub policies might not offer the depth of protection required for the nightclub environment.

What happens if I don’t have employers’ liability insurance?

Operating without employers’ liability insurance is a criminal offense if you employ anyone, even on a casual or part-time basis. You can be fined up to £2,500 for every single day you’re without cover under the Employers’ Liability (Compulsory Insurance) Act 1969. Additionally, failing to display a valid insurance certificate can result in a further fine of up to £1,000 from the Health and Safety Executive.

How can I reduce my bar insurance premiums?

The most effective way to reduce your premiums is to demonstrate proactive risk management to your underwriters. Installing FCA-approved CCTV systems, implementing “Challenge 25” staff training, and keeping meticulous safety logs can make your business a more attractive risk. You might also consider increasing your policy excess, which can lower your annual premium if you’re confident in your venue’s safety standards.

Article by

Just Quote Me

JustQuoteMe Ltd is an independent UK insurance brokerage specialising in business and personal insurance solutions. With over 35 years of industry experience, the company provides tailored insurance cover for businesses, landlords, tradespeople, hospitality venues, fleets, and individuals across the UK. Known for its personal service, expert advice, and competitive premiums, JustQuoteMe Ltd works with leading insurers to deliver bespoke policies designed around each client’s unique needs. The company is authorised and regulated by the Financial Conduct Authority (FCA No. 586607) and has built a reputation for trusted, straightforward insurance guidance and long-term client relationships.

by jqm | Aug 4, 2026 | Insurance

What if a single incident at your shop front could wipe out a year’s worth of profit? With average subsidence claims reaching £20,000 in 2026 and weather-related property damage hitting record levels, your choice of shop insurance is no longer just a box-ticking exercise. You’ve likely felt the sting of rising premiums while wondering if your policy actually covers the unique risks your business faces. It’s a complex landscape, especially as the FCA intensifies its focus on Consumer Duty to ensure firms deliver fair value and clearer information to every policyholder.

We understand that you need reliability and straightforward answers, not confusing fine print or automated responses. This guide provides a clear roadmap to securing your premises, stock, and staff while ensuring full compliance with UK law, including the mandatory £5 million employers’ liability cover. You will discover how tailored protection for business interruption and public liability can provide a vital safety net. We’ll help you navigate the difference between essential and optional covers so you can protect your livelihood with confidence. Just Quote Me for a pragmatic approach that manages the administrative burden so you can focus on your customers.

Key Takeaways

- Understand why modern retail risks require a bespoke shop insurance policy that goes beyond basic property protection to cover digital integration and evolving consumer habits.

- Identify the core legal requirements for staffing and the critical role of public liability in safeguarding your business against visitor accidents and third-party claims.

- Learn how to tailor your cover to your specific retail niche, whether you are managing high-value boutique stock or food safety risks in a cafe environment.

- Discover effective strategies for reducing your annual insurance costs through improved security protocols and strategic voluntary excess choices.

- Explore the benefits of working with an independent, human-centric broker to navigate complex FCA regulations and secure the best value from a broad network of UK insurers.

What is Shop Insurance and Why is it Essential in 2026?

At its core, shop insurance is a specialized insurance package designed to shield retail business owners from financial ruin. It isn’t just a single policy. It’s a strategic combination of protections that cover your physical assets, your legal responsibilities to the public, and your commitment to your staff. As we move through 2026, the retail environment has shifted. Physical stores now operate as hybrid hubs, blending in-person sales with digital click-and-collect services. This evolution introduces new risks, from data handling vulnerabilities to the increased complexity of supply chains.

The UK insurance market is currently navigating significant regulatory changes. The Financial Conduct Authority (FCA) implemented simplified insurance rules in mid-2026, specifically on June 26 and July 27. These updates require insurers to offer greater transparency and flexibility. Relying on a generic commercial policy often leaves gaps in coverage that only become apparent during a claim. Choosing a bespoke plan ensures that your specific business model is accurately reflected in your policy. In this shifting market, an independent broker acts as your advocate, scanning a broad network of insurers to find a policy that fits your needs rather than forcing you into a standard template.

The Core Components of a Retail Policy

A robust policy typically functions like a Business Owner’s Policy (BOP), bundling several essential covers into one manageable premium. This usually includes buildings insurance, stock protection, and liability cover. For Staffordshire small businesses, the local context matters. A shop in Stone or Newcastle-under-Lyme faces different environmental and footfall risks than a warehouse. One-size-fits-all policies frequently fail to account for these nuances, leaving local retailers underinsured. Our 30 years of experience as an independent broker allows us to identify these hidden risks, ensuring your stock levels are protected even during seasonal peaks.

Legal vs. Discretionary Insurance for Retailers

Distinguishing between what you must have and what you should have is vital for your budget. In the UK, Employers’ Liability Insurance is a legal requirement if you employ anyone, even on a seasonal or part-time basis. Failing to hold a minimum of £5 million in cover can result in severe penalties. While other covers are discretionary, their value is undeniable. Business Interruption insurance, for instance, covers lost income if a fire or flood forces you to close temporarily. In 2026, shop insurance is no longer just a legal hurdle but a strategic asset for retail resilience. It provides the financial stability needed to survive unexpected disruptions in an increasingly competitive market.

Understanding the Key Covers: From Liability to Stock

Selecting the right shop insurance requires a deep dive into the specific risks your business handles daily. In 2025, UK property insurance payouts reached a record £6.1 billion, with £1.6 billion of that being weather-related. These figures highlight why having a robust policy isn’t just about compliance; it’s about survival. Your covers should act as a multi-layered shield, protecting your finances when accidents happen or nature intervenes. Understanding these layers helps you build a policy that fits your budget while providing genuine security.

Public and Employers’ Liability Essentials

Public Liability Insurance is the foundation of any customer-facing business. It covers legal costs and compensation if a visitor is injured or their property is damaged while on your premises. Common retail scenarios include a customer slipping on a wet floor or a display rack falling unexpectedly. With the median cost of public liability in the UK sitting at approximately £104 per year in 2026, it’s a highly cost-effective way to avoid catastrophic legal bills.

If you have any staff, Employers’ Liability Insurance is non-negotiable. UK law requires most businesses with employees to have a minimum of £5 million in cover. This includes part-time workers, seasonal staff, and even some volunteers. You can verify the specific legal requirements for Employers’ Liability (EL) insurance through official government guidelines. Failing to secure this mandatory cover can lead to daily fines. If you’re unsure about your staffing status, you can speak with a local expert to clarify your obligations and avoid legal pitfalls.

Protecting Your Assets: Buildings and Stock

The way you approach Commercial Property Insurance depends on whether you own your shop or rent it. Tenants typically only need to cover their own fixtures and shop fittings, while owners must insure the entire structure. A frequent pitfall for retailers is ‘underinsurance.’ This happens when stock is valued at what you paid for it rather than the current replacement cost. If a fire or flood occurs, an undervalued policy won’t pay out enough to restock your shelves. High-value items or perishable goods require special consideration to ensure your shop insurance policy reflects their unique risk profiles.

Finally, Business Interruption cover ensures your income doesn’t stop if an insured event like a fire forces you to close. It covers your lost profits and ongoing costs, such as rent and wages, during the recovery period. Without it, even a well-insured shop might never reopen after a major incident. It’s the difference between a temporary closure and a permanent business failure.

Tailoring Cover for Your Specific Retail Niche

Every retail business has a unique risk profile that a standard policy might overlook. A high-street fashion boutique faces vastly different challenges than a local corner shop or a village cafe. For instance, boutiques must manage significant seasonal stock fluctuations. Your shop insurance needs to account for the periods before Christmas or summer sales when your inventory value might double. Additionally, fitting rooms introduce specific liability risks regarding both customer privacy and physical safety that require precise wording in your policy.

Food-led retail businesses require even more specialized integration. If you run a deli or a small bakery with seating, you often need to combine standard retail protection with elements of Restaurant Insurance. This ensures you are covered for product liability, which is essential if a customer claims they became ill from food purchased at your premises. For more complex setups, such as those involving Thatched Pub insurance or shops with residential quarters above them, the risk assessment becomes even more technical. These “non-standard” builds often require a broker’s eye to ensure the property is valued correctly and the fire risks are properly mitigated.

Bespoke Solutions for Unique Retailers

Many modern shops now offer services alongside products. Hair salons that sell professional products or bike shops that perform repairs need a hybrid approach. In these cases, Professional Indemnity Insurance may be necessary if you provide expert advice or specialized services that could lead to a financial loss for a client. Whether you are running a permanent store or a temporary pop-up space, consulting a comprehensive guide to business insurance can help you identify these overlapping needs. Just Quote Me for a policy that reflects these nuances rather than settling for a generic package.

The Staffordshire Advantage: Local Knowledge Matters

National insurance providers often use broad demographic data that can unfairly penalize businesses in certain postcodes. We take a different approach by focusing on regional expertise. Businesses in Stafford, Stone, and Newcastle-under-Lyme benefit from our understanding of local risk factors, such as specific flood-prone areas or varying crime statistics across the West Midlands. Having a broker who can physically visit your premises allows for more accurate risk profiling, often leading to more competitive premiums. This human-centric approach ensures that your shop insurance is built on real-world data rather than automated assumptions. Local expertise allows for more accurate risk profiling, often leading to more competitive premiums and a policy that truly stands up when you need to make a claim.

How to Reduce Your Shop Insurance Premiums

Reducing your shop insurance premiums is a matter of proactive risk management rather than just shopping around for the lowest headline figure. Insurers view a well-secured shop as a lower liability. Installing high-grade CCTV, police-monitored alarm systems, and physical shutters can lead to meaningful reductions in your annual costs. These measures don’t just protect your stock. They demonstrate to underwriters that you’re a responsible business owner who takes loss prevention seriously.

Choosing a higher voluntary excess is another direct way to lower your premium. By agreeing to pay a larger portion of any initial claim yourself, you take on more of the risk, which insurers reward with lower monthly or annual payments. You must ensure the excess remains affordable so it doesn’t strain your cash flow if an incident occurs. Accurate valuation of your stock and contents is equally critical. Paying for cover that exceeds your actual inventory levels is a common way businesses waste money. Consolidating your various protections into a single package policy is typically more cost-effective than purchasing separate liability and property covers. If you want to see how these adjustments affect your bottom line, you can request a tailored review of your current policy.

Risk Management Strategies for Retailers

Staff training plays a vital role in keeping costs down over the long term. Documented health and safety protocols reduce the likelihood of accidents that lead to public or employers’ liability claims. Since 43% of UK businesses experienced a cybersecurity breach in the past 12 months, according to the Government’s 2025/2026 survey, integrating Cyber Insurance into your risk strategy is now a pragmatic move. It prevents massive out-of-pocket losses from digital attacks that standard policies might ignore. Regular policy reviews ensure your coverage reflects your current business size rather than your setup from a previous year.

Working with an Independent Broker

Working with an independent broker provides access to broker-only rates that comparison sites simply cannot offer. We use a professional Statement of Fact to present your business in the best possible light to underwriters. This document provides a clear, accurate summary of your risks and safety measures, which often leads to more favorable terms and lower premiums. Our 30 years of experience allows us to negotiate these details on your behalf, managing the administrative burden so you don’t have to. To see how these strategies can impact your costs, Get Your Free Business Insurance Quote now and let our experts find the right balance of protection and value for your shop.

Why Choose Just Quote Me for Your Shop Insurance?

Choosing the right partner for your shop insurance shouldn’t feel like a transaction with an algorithm. After 30 years of navigating the UK insurance market, we’ve learned that retail owners value two things above all: reliability and time. We don’t just sell policies. We build bespoke protection plans that solve the administrative burdens often associated with commercial cover. Our approach is human-centric. You won’t find yourself trapped in an automated phone queue or forced to interact with a chatbot that doesn’t understand the nuances of your specific business model.

Our role extends far beyond the initial quote. We act as your advocate throughout the life of your policy, particularly when it matters most. If you need to make a claim, having an expert in your corner can be the difference between a swift resolution and a protracted dispute. We manage the dialogue with underwriters and handle the technical details, allowing you to focus on running your shop. This level of personalized service is why many West Midlands business owners view us as a steady hand in a complex market. We provide the clarity you need to make informed decisions without the corporate jargon.

Expertise You Can Trust

As an FCA-authorised firm, we provide advice that is both protected and compliant. We leverage our independent status to access a wide network of top UK insurers, ensuring you receive competitive pricing without sacrificing the quality of your cover. Our specialized knowledge of the retail sector allows us to spot potential gaps that generalist brokers might miss. Local business owners across Staffordshire and the West Midlands consistently highlight our straightforward communication and pragmatic attitude as key reasons for their long-term loyalty. We believe in plain, honest communication that builds lasting professional relationships.

Take the Next Step for Your Business

We’ve designed our process to be as frictionless as possible for busy retailers. Whether you’re a new startup or an established high-street name, we provide the expert guidance needed to secure your livelihood. Our local offices in Stone and Newcastle-under-Lyme mean we aren’t just a voice on the phone; we’re part of your community. We understand the regional retail landscape and use that expertise to your advantage. If you’re ready for a more personalized approach to your shop insurance, Request a Call back for free Expert advice today. Just Quote Me for a partnership built on transparency, speed, and three decades of industry expertise.

Secure Your Retail Future with Expert Guidance

Protecting your livelihood in 2026 requires a shift from viewing insurance as a fixed cost to seeing it as a strategic asset. You’ve learned that balancing mandatory covers like employers’ liability with discretionary protections like business interruption is the key to long-term stability. By implementing robust security measures and valuing your stock accurately, you can actively drive down your shop insurance costs without compromising on safety. Relying on generic comparison sites often leads to underinsurance, but a tailored approach ensures every corner of your business is shielded.

As an FCA-authorised firm with over 30 years of industry experience, Just Quote Me provides the specialized retail knowledge needed to navigate today’s complex market. We offer a human-centric partnership that manages the administrative burden for you, ensuring your policy reflects the unique risks of your specific niche. Take the first step toward total peace of mind by choosing a bespoke retail cover specialist who understands your world. Get Your Free Business Insurance Quote now or Request a Call back for free Expert advice to speak with a specialist today. Your business deserves a steady hand.

Frequently Asked Questions

Is shop insurance a legal requirement for UK businesses?

Employers’ Liability is the only part of shop insurance that is a legal requirement if you employ anyone. UK law mandates a minimum of £5 million in cover to protect staff against injury or illness resulting from their work. While public liability and buildings insurance aren’t legally compulsory, most commercial landlords require them as a condition of your lease agreement.

How much does shop insurance cost on average in 2026?

Basic policies for retail premises currently start at approximately £13 a month according to industry data from July 2026. For a more comprehensive package, small businesses in the UK typically pay between £220 and £350 per year. The median cost specifically for Public Liability insurance is around £104 annually, though your final premium depends on your location, turnover, and stock levels.

Does my shop insurance cover me for online sales and delivery?

Standard retail policies often focus on your physical premises, so you must specifically extend your cover for e-commerce activities. You’ll need to disclose your online turnover and ensure your product liability covers items sold digitally. It’s also vital to check if your stock is protected while in transit or stored at a third-party fulfillment center.

What happens if I under-insure my shop’s stock?

Under-insuring your stock triggers the “Condition of Average” clause during a claim, which reduces your payout proportionally. If you insure your stock for £50,000 but its true replacement value is £100,000, you’re 50% under-insured. Consequently, the insurer may only pay 50% of any claim, leaving you to cover the remaining costs yourself even for minor incidents.

Can I get shop insurance if my premises have a flat above them?

You can secure coverage for shops with residential flats above, though insurers view this as a higher fire risk. You must disclose the presence of the flat and whether it’s occupied by you, a staff member, or a third party. Accurate disclosure ensures your shop insurance remains valid if a domestic incident, such as a kitchen fire or water leak, damages your retail space.

What is business interruption insurance and do I really need it?

Business interruption insurance covers your lost income and ongoing expenses if an insured event like a fire forces you to close temporarily. It’s designed to keep your business afloat by covering rent, wages, and lost profits during the recovery period. Given that property insurance payouts for weather damage reached record highs in 2025, this cover is a vital survival tool for modern retailers.

How can an independent broker help me save money on my premium?

Independent brokers access exclusive “broker-only” rates that aren’t available on public comparison websites. We use our 30 years of experience to present your risk profile more accurately to underwriters, often securing better terms through a professional Statement of Fact. This human-centric approach identifies and removes unnecessary covers, ensuring you only pay for the protection your specific shop actually needs.

Does shop insurance cover theft by employees?

Standard shop policies don’t always include theft by staff, but you can add “Employee Dishonesty” or “Fidelity Guarantee” cover to your package. This specific protection guards your business against financial losses caused by fraudulent acts or theft committed by employees. It’s a pragmatic addition for shops handling significant cash volumes or high-value inventory.

Article by

Just Quote Me

JustQuoteMe Ltd is an independent UK insurance brokerage specialising in business and personal insurance solutions. With over 35 years of industry experience, the company provides tailored insurance cover for businesses, landlords, tradespeople, hospitality venues, fleets, and individuals across the UK. Known for its personal service, expert advice, and competitive premiums, JustQuoteMe Ltd works with leading insurers to deliver bespoke policies designed around each client’s unique needs. The company is authorised and regulated by the Financial Conduct Authority (FCA No. 586607) and has built a reputation for trusted, straightforward insurance guidance and long-term client relationships.

by jqm | Aug 3, 2026 | Insurance

If your startup faced a legal claim tomorrow, would your house and personal savings remain safe? Many founders mistakenly believe that “limited liability” provides a total shield for their private assets, but the reality in 2026 is far more complex. With the full implementation of the Economic Crime and Corporate Transparency Act and new “day-one” employment rights now in effect, your personal responsibility as a leader has never been higher. Securing directors and officers liability for startups is no longer just a box-ticking exercise; it’s a critical safety net for your personal financial future.

We understand that the pressure to scale while managing shifting UK regulations can feel overwhelming. You’ve likely felt the push from investors to get cover in place or found yourself confused by the difference between professional indemnity and D&O. This guide will clarify exactly how D&O insurance protects you from management risks and why it’s a non-negotiable requirement for securing VC funding this year. We’ll break down the specific legal changes affecting you in 2026 and show you how to gain the peace of mind needed to make high-stakes decisions with confidence.

Key Takeaways

- Understand why limited company status doesn’t protect your personal bank account and how D&O insurance acts as a firewall for your private assets.

- Learn why securing directors and officers liability for startups is a mandatory requirement for most VC term sheets and angel investment rounds in 2026.

- Identify the specific regulatory and employment risks that could lead to personal legal claims against you under the Companies Act 2006.

- Discover how premiums are calculated and why the “claims-made” nature of these policies means you cannot afford any gaps in your coverage.

- Find out why a bespoke broker service provides more reliable protection than generic automated quote engines for high-growth businesses.

The Reality of Personal Liability for Startup Directors in 2026

The UK regulatory landscape has shifted significantly. As of 2026, Companies House has moved from a passive registry to an active gatekeeper. This change, driven by the full implementation of the Economic Crime and Corporate Transparency Act, means directors face unprecedented scrutiny regarding identity verification and financial accuracy. If you’re leading a high-growth firm, understanding directors and officers liability for startups is the difference between a successful exit and personal financial ruin. You can no longer rely on administrative distance to protect you from the consequences of management decisions.

A common misconception among founders is that the “limited” in a limited company protects their personal bank accounts. While the company is responsible for its own debts, you remain personally liable for your actions as a director under the Companies Act 2006. Directors and Officers (D&O) liability insurance is designed to shield your private wealth from claims of “wrongful acts.” In a startup environment, these acts often involve breach of duty, neglect, or errors in judgement during rapid scaling. It’s not just about fraud; it’s about the everyday mistakes made while moving fast and trying to hit aggressive milestones.

D&O vs Professional Indemnity: Clearing the Confusion

Many founders struggle to distinguish between management liability and service-related risks. Professional Indemnity Insurance covers the company if your product or service fails. For example, if a coding bug causes a client financial loss, PI steps in. In contrast, D&O covers you personally for management decisions. If a disgruntled employee sues for unfair dismissal following the 2026 employment law changes, or an investor claims they were misled during a seed round, D&O is what protects your personal assets. Tech startups often find that VCs require both D&O and Cyber Insurance before releasing Series A funds to ensure the leadership team is properly insulated.

The Personal Firewall for Founders

Without this protection, a single legal challenge can target your home, your savings, and your private investments. The cost of legal defence alone in the UK can easily reach six figures before a case even reaches court. Even if you’ve done nothing wrong, you still have to pay to prove it. D&O insurance acts as a personal firewall, ensuring that a professional mistake doesn’t escalate into a private catastrophe. It’s the essential personal safety net for any UK director.

Why UK Startups Face Unique Management Risks

Rapid growth is the primary goal for most founders, but it’s also a significant liability minefield. In 2026, UK startups operate in an environment where regulatory oversight is at an all-time high. Founders often focus on achieving product-market fit while neglecting the rigorous administrative compliance now required by the Economic Crime and Corporate Transparency Act. This specific gap in management focus is exactly why directors and officers liability for startups is so vital. When you scale from five to fifty employees in a single year, your internal systems for financial reporting and identity verification often lag behind, leaving you personally exposed to civil penalties.

The “insolvency trap” is a recurring danger for firms running on tight runways. With 1,744 company insolvencies recorded in England and Wales in January 2026 alone, the risk of business failure remains historically elevated. If you continue to incur debt while knowing the company has no reasonable prospect of avoiding liquidation, you risk being held personally liable for “wrongful trading.” Creditors can bypass the corporate veil to target your private bank accounts. Companies House suggests that founders should seriously consider investing in directors’ and officers’ cover to manage these high-stakes personal exposures.

The Companies Act 2006 and Your Duties

Your role as a leader is governed by strict statutory duties under the Companies Act 2006. You’re legally required to promote the success of the company for the benefit of its members and exercise reasonable care, skill, and diligence in every decision. These aren’t just suggestions; they’re legal mandates. While Professional Indemnity Insurance protects the company against errors in your professional services, it won’t shield you if a shareholder claims you breached your fiduciary duties during a strategic pivot or a botched funding round.

Employment Practices Liability (EPL)

Employment claims are the most frequent source of D&O litigation for firms with fewer than 100 employees. As of April 2026, new statutory sick pay rules and expanded “day-one” parental rights have significantly increased the complexity of HR management. If an employee feels they’ve been unfairly dismissed or discriminated against, they may name you personally in the legal action. Rapidly scaling teams often face “culture clashes” that lead to litigation. Ensuring your policy includes an EPL extension provides a critical layer of safety during these volatile growth phases. If you’re unsure about your current level of exposure, you can consult with an experienced broker to identify potential gaps in your protection.

D&O Insurance as a Prerequisite for Raising Venture Capital

Venture capital firms don’t just invest in your technology; they invest in the stability and integrity of your leadership team. In 2026, a term sheet without a mandatory D&O clause is almost unheard of in the UK market. Investors view directors and officers liability for startups as a fundamental component of their own risk management strategy. They know that high-growth environments are prone to “investor suits,” where shareholders claim they were misled by overly optimistic financial forecasts or aggressive growth projections during the funding round. Having this cover in place signals that your startup is “investment-ready” and takes corporate governance seriously.

Beyond protecting the founders, D&O insurance is a tool to attract and retain qualified executives who bring the expertise needed to scale. When a VC fund leads your Series A, they often appoint a non-executive director (NED) to your board. These experienced professionals rarely agree to serve without the guarantee that their personal assets are protected from the company’s management risks. By securing a robust policy early in the due diligence process, you remove a significant friction point that could otherwise delay or derail your funding.

Satisfying the Term Sheet

Most Series A and B funding rounds in the UK now stipulate a minimum of £1 million to £3 million in D&O coverage as a condition of closing. Investors specifically look for “Side C” or Entity Cover, which ensures the company itself is protected when it is named alongside directors in a lawsuit. It’s common for investors to also mandate Cyber Liability Insurance alongside D&O. This creates a comprehensive shield that satisfies the fund’s compliance requirements and demonstrates that you’ve accounted for both management and operational vulnerabilities.

D&O on Exit: IPOs and Acquisitions

Your liability doesn’t end when the business is sold or goes public. If your startup undergoes a “Delaware flip” for international expansion or prepares for an acquisition, your D&O policy becomes even more critical. During these transitions, “Run-off cover” is essential. This specific extension protects past directors for a set period, typically six years, after the company changes hands. It ensures that management decisions made today won’t lead to personal financial disaster years after you’ve exited the business. For those heading toward a public listing, D&O also forms the basis of Public Offering Securities Insurance (POSI), which is vital for managing the unique risks of an IPO.

Calculating the Real Cost and Level of Cover for Your Startup

Determining the right level of directors and officers liability for startups requires a clear understanding of your specific risk profile. Your policy must be active when a claim is filed, not just when the event occurred. This is known as “claims-made” coverage. If you cancel your policy or allow a gap to occur after a funding round, you lose protection for all management decisions made during that period. Maintaining continuous cover is the only way to ensure your personal assets remain shielded from historical decisions that might only come to light years later.

The limit of indemnity you choose should reflect the scale of your operations and the expectations of your board. While £1 million is often the entry-level baseline for seed-stage companies, Series A and B rounds frequently mandate limits of £2 million or £5 million. You must also distinguish between “Any One Claim” and “Aggregate” limits. An aggregate limit is the total amount the insurer will pay across the entire policy year, whereas an “Any One Claim” limit provides the full sum for every individual claim made. For startups in high-growth phases, the latter offers significantly more robust protection against multiple simultaneous legal challenges.

Factors That Drive Startup Premiums

Insurers look closely at your sector and financial stability when calculating your premium. High-risk industries like FinTech, MedTech, and DeepTech often face higher rates due to the complex regulatory environments they inhabit. Your management team’s previous experience also plays a vital role; a founder with a successful exit history is often viewed as a lower risk. Maintaining a clean claims history and transparent financial reporting are your best tools for securing more competitive rates during your annual renewal. If you want to ensure your broader coverage is equally robust, consult our Small Business Insurance Checklist for a complete overview of 2026 requirements.

Selecting Your Limit of Indemnity

Benchmarking is essential for making an informed choice. Startups in Staffordshire and the wider West Midlands should look at the typical settlement figures and legal defence costs in UK courts, which have risen alongside inflation to 2.6% in 2026. A £1 million limit can be exhausted surprisingly quickly by legal fees alone, even if the claim is eventually dismissed. You should account for the possibility of multiple directors being named in a single suit, which multiplies the defence costs. To find the right balance for your budget, you can get a tailored D&O quote that reflects your specific funding stage and industry risk.

Securing Bespoke D&O Protection with Just Quote Me

Automated quote engines often treat a high-growth AI startup the same as a traditional consultancy. This lack of nuance leaves you either underinsured or paying for coverage that doesn’t fit your specific risk profile. Just Quote Me provides a human-centric alternative to these impersonal systems. As an independent, FCA-authorised broker with over 30 years of experience, we understand that directors and officers liability for startups is too complex for a standard online form. We don’t just provide a policy; we provide a partnership that manages the administrative burden so you can focus on hitting your next milestone.

Our access to a broad network of top UK insurers allows us to find competitive pricing that matches your specific funding stage. We act as your steady hand in a volatile market, ensuring that every detail of your management protection is tailored to your unique risks. Whether you’re based in the West Midlands or scaling nationally, our regional expertise ensures you receive a level of service that larger, impersonal competitors simply cannot match. We handle the complex paperwork and negotiations with underwriters, providing you with a frictionless experience from the initial inquiry to the final policy issuance.

Why a Bespoke Approach Matters for Startups

Success in the startup world requires a holistic approach to risk. By customising your insurance portfolio, we can combine your D&O cover with Cyber Insurance and Professional Indemnity Insurance into one manageable package. This eliminates coverage gaps and ensures that your personal assets and company operations are shielded simultaneously. Founders in Newcastle-under-Lyme, Stafford, and Stone benefit from our local roots and straightforward communication. We avoid hyperbolic marketing speak, opting instead for plain, honest advice that helps you make informed choices with total confidence.

Your Next Steps to Secure Management Protection

Securing a quote is a straightforward process when you have the right information ready. You’ll need to provide clear financial forecasts and details about your senior leadership team’s professional background. Insurers value transparency and experience, so highlighting your board’s previous successes can help lower your premiums. We’ll guide you through the disclosure requirements, ensuring that your application presents your startup in the best possible light to our panel of insurers. Taking these steps today prevents a management error from becoming a personal financial disaster tomorrow.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Future-Proof Your Leadership Strategy

Protecting your startup means more than just securing your intellectual property; it’s about safeguarding the people who build it. We’ve explored how limited liability doesn’t stop legal claims from reaching your personal bank account and why investors won’t move forward without seeing a policy in place. In the regulatory environment of 2026, directors and officers liability for startups is the most effective way to manage these high-stakes personal risks while maintaining your focus on scaling. By addressing these management vulnerabilities now, you ensure that a single professional error doesn’t escalate into a private financial disaster.

Just Quote Me brings 30+ years of industry experience as an FCA-authorised independent broker to help you navigate these complexities. We specialise in bespoke startup insurance packages that combine management liability with other essential covers into one streamlined portfolio. Instead of wrestling with automated forms that don’t understand your unique growth trajectory, you can rely on our expert team for a personalised approach that prioritises your security. We’re here to handle the administrative burden so you don’t have to.

Take the first step toward securing your personal assets today. Get Your Free Business Insurance Quote now or Request a Call back for free Expert advice to speak with our knowledgeable team. You’ve worked hard to build your vision; let’s ensure your personal future is just as secure as your company’s next big exit.

Frequently Asked Questions

Is D&O insurance legally required for startups in the UK?

No, D&O insurance is not a statutory requirement in the UK, unlike Employers Liability insurance. However, it’s almost always a contractual requirement if you’re raising venture capital or angel investment. While the law doesn’t force you to have it, the Companies Act 2006 places significant personal duties on you that make this cover a practical necessity for any founder.

Does D&O insurance cover criminal acts or fraud committed by directors?

D&O insurance doesn’t cover proven criminal acts, deliberate fraud, or “dishonest” behaviour. It’s designed to protect you against “wrongful acts” like negligence, errors, or breaches of duty. Most policies will pay for your legal defence costs until a final adjudication or a guilty plea is reached, at which point the insurer will usually stop payments and may seek to recover the costs already paid.

What is the difference between D&O and Management Liability insurance?

Management Liability is an umbrella term that usually includes three distinct covers: D&O, Employment Practices Liability (EPL), and Corporate Legal Liability. While D&O specifically protects the individual managers’ personal assets, a full Management Liability package provides a broader shield for the company entity itself. Many founders find that a comprehensive directors and officers liability for startups policy is best structured within this wider Management Liability framework.

Can a startup director be sued by an employee personally?

Yes, employees can name individual directors personally in legal actions, particularly in cases of alleged discrimination or harassment. Following the expansion of “day-one” employment rights in April 2026, the risk of these personal claims has increased. Without the right cover, you could be forced to pay for your own legal defence even if the company is also named in the suit.

How much does D&O insurance typically cost for a UK startup in 2026?

The cost of your premium depends on several factors, including your industry sector, the amount of funding you’ve raised, and your company’s financial stability. High-growth firms in regulated sectors like FinTech often see higher premiums than those in less regulated industries. To get an accurate figure that reflects your specific risk profile, it’s best to request a bespoke quote from an independent broker.

What happens to my D&O cover if the startup goes into insolvency?

Your D&O policy is specifically designed to stay active and protect you during insolvency proceedings, provided the policy was in place before the insolvency began. This is when the cover is most valuable, as it protects you from claims made by liquidators or creditors regarding “wrongful trading.” With 1,744 company insolvencies recorded in January 2026, having this protection ensures your personal savings aren’t used to settle company debts.

Do I need D&O insurance if I am a sole trader?

No, sole traders don’t need D&O insurance because there is no separate legal entity or board of directors to protect. As a sole trader, you already have unlimited personal liability for your business actions. You should instead focus on Public Liability or Professional Indemnity insurance to manage your risks. Directors and officers liability for startups is specifically for those operating as a limited company.

What is “run-off” cover and why do I need it after an exit?

Run-off cover provides protection for claims that are filed after your company has been sold, merged, or closed down. Because D&O insurance is “claims-made,” the policy must be active at the time the claim is made, not when the event happened. Run-off cover typically lasts for six years, ensuring that management decisions you make today don’t come back to haunt your personal finances years after you’ve exited the business.

Article by

Just Quote Me

JustQuoteMe Ltd is an independent UK insurance brokerage specialising in business and personal insurance solutions. With over 35 years of industry experience, the company provides tailored insurance cover for businesses, landlords, tradespeople, hospitality venues, fleets, and individuals across the UK. Known for its personal service, expert advice, and competitive premiums, JustQuoteMe Ltd works with leading insurers to deliver bespoke policies designed around each client’s unique needs. The company is authorised and regulated by the Financial Conduct Authority (FCA No. 586607) and has built a reputation for trusted, straightforward insurance guidance and long-term client relationships.

by jqm | Aug 2, 2026 | Insurance

Your IT security is working perfectly — and your business still suffers a devastating data breach. That’s not a hypothetical; it’s the reality facing thousands of UK small businesses every year. Cybercriminals don’t just target the unprepared, and when they strike, the fallout goes far beyond fixing a compromised server.

If you’ve ever wondered whether your existing professional indemnity policy has you covered, or felt a knot of anxiety at the thought of an ICO investigation and GDPR fines landing on your desk, you’re not alone. Most small business owners feel exactly the same way, and the confusion is entirely understandable.

This guide cuts through that confusion. We’ll explain precisely what cyber insurance for small business data breach scenarios actually covers, why it functions as far more than a financial safety net, and how it acts as your outsourced emergency response team the moment something goes wrong. By the end, you’ll know exactly what protection you need, what costs a policy can absorb, and how to get bespoke cover that fits your business rather than a generic one-size-fits-all policy.

Key Takeaways

- Cyber security and cyber insurance serve entirely different purposes — one prevents breaches, the other funds your recovery when prevention isn’t enough.

- The right cyber insurance for small business data breach scenarios covers far more than financial losses, acting as an on-call response team that handles IT forensics, legal support, and GDPR notifications on your behalf.

- A data breach carries significant hidden costs — from customer notification expenses to long-term reputational damage — that standard professional indemnity policies typically won’t cover.

- Choosing the correct level of indemnity requires an honest assessment of the sensitive data your business holds and how that exposure maps to your annual turnover.

- Working with an independent broker like Just Quote Me gives you access to a panel of top UK insurers and bespoke advice tailored to your specific industry, rather than a generic off-the-shelf policy.

What is Cyber Insurance for Small Business Data Breaches?

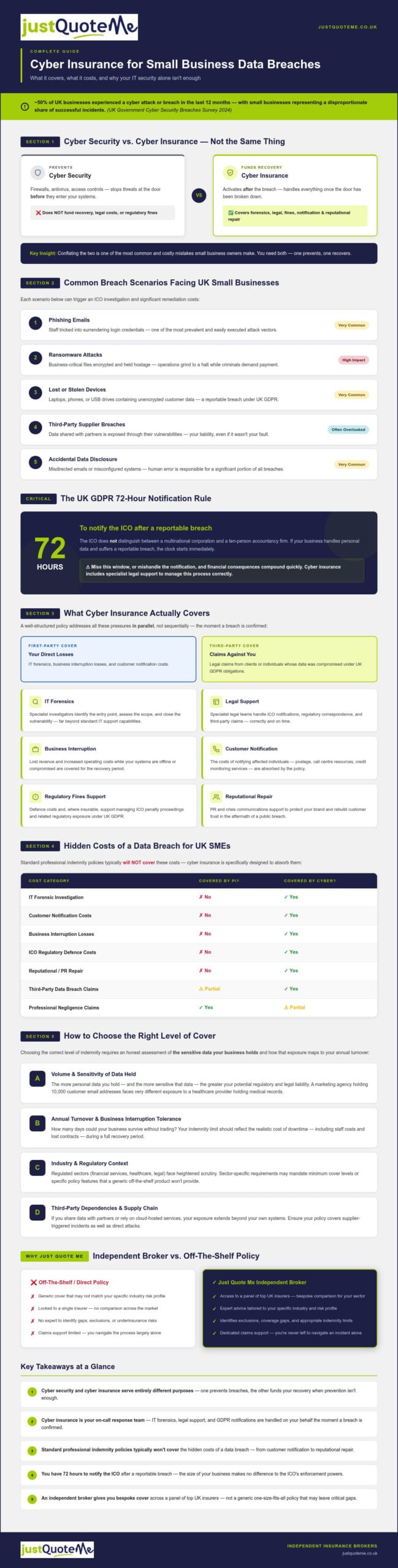

Cyber insurance is a specialist financial and operational product designed to fund your recovery when a digital incident occurs. Think of it as two things working in tandem: a financial backstop that absorbs costs you’d otherwise carry alone, and an on-call response team that activates the moment a breach is confirmed. It doesn’t prevent incidents from happening. That’s the job of your IT security. What it does is ensure that when prevention falls short, your business doesn’t face the aftermath alone and underfunded.

This distinction matters enormously. A firewall stops threats at the door. Cyber insurance for small business data breach scenarios handles everything that happens after the door has already been broken down: the forensic investigation, the regulatory notifications, the legal exposure, and the reputational repair. Conflating the two is one of the most common and costly mistakes small business owners make.

2026 is a particularly significant year for UK SMEs navigating digital risk. The post-Brexit data protection framework continues to evolve, with the ICO maintaining its authority to investigate breaches and issue substantial fines under the UK GDPR. Critically, the ICO doesn’t distinguish between a multinational corporation and a ten-person accountancy firm. If your business handles personal data and suffers a reportable breach, you have 72 hours to notify the ICO. Miss that window, or mishandle the notification, and the financial consequences compound quickly.

Cyber Liability vs. Data Breach Cover

In 2026, cyber liability insurance is broadly defined as protection against the financial and legal consequences of a data security failure, covering both your own losses and claims made against you by affected third parties under UK GDPR obligations. First-party cover addresses your direct costs: IT forensics, business interruption, and customer notification. Third-party cover responds to claims from clients or individuals whose data was compromised. A comprehensive cyber policy typically bundles both, but it’s essential to confirm the scope before you buy.

Why Small Businesses are the Primary Target

Cybercriminals operate on a straightforward logic: smaller businesses typically hold valuable data but invest less in defending it. According to the UK government’s Cyber Security Breaches Survey 2024, around half of UK businesses reported experiencing a cyber attack or breach in the preceding 12 months, with small businesses representing a disproportionate share of successful incidents.

The most common breach scenarios facing small businesses include:

- Phishing emails that trick staff into surrendering login credentials

- Ransomware attacks that encrypt business-critical files and demand payment

- Lost or stolen devices containing unencrypted customer data

- Third-party supplier breaches that expose data you’ve shared with partners

- Accidental data disclosure through misdirected emails or misconfigured systems

Each of these scenarios can trigger an ICO investigation and significant remediation costs. Understanding what cyber insurance for small business data breach events actually covers starts with recognising just how varied the threat landscape is. Explore your options with Just Quote Me’s cyber liability insurance to see how bespoke cover maps to your specific risk profile.

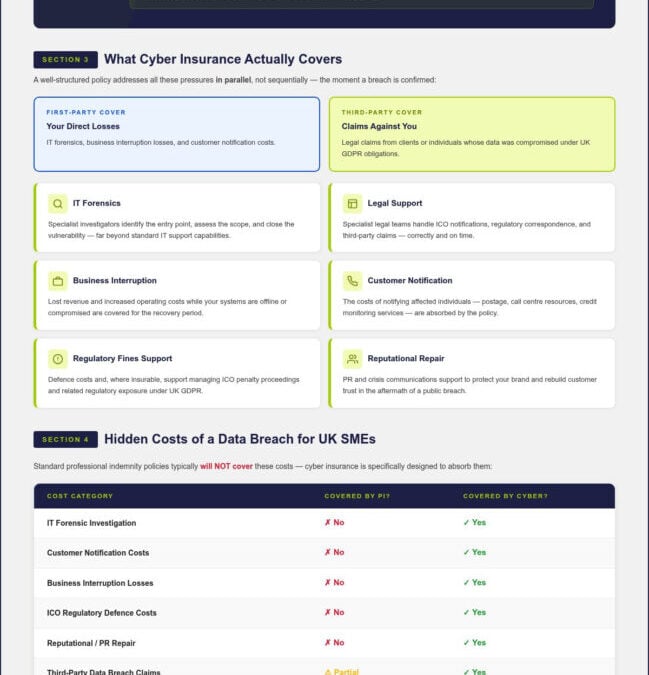

What Does Cyber Insurance Cover in a Data Breach?

When a breach occurs, the clock starts immediately. You’re facing a forensic puzzle, a regulatory deadline, potential legal claims, and a business that may have ground to a halt — all at once. A well-structured cyber insurance for small business data breach policy addresses each of these pressures in parallel, not sequentially. Here’s what that actually looks like in practice.

IT Forensics. Before you can fix anything, you need to understand what happened. Cyber policies fund specialist forensic investigators who identify the entry point, assess the scope of the compromise, and close the vulnerability. This isn’t something your general IT support is equipped to handle. Forensic work is highly specialised, and without it, you risk patching the surface while the underlying weakness remains exploitable.

Legal Support and GDPR Notifications. UK GDPR requires you to notify the ICO within 72 hours of becoming aware of a reportable breach. Miss that window and the regulatory consequences compound. Cyber cover funds specialist data protection solicitors who manage that notification process on your behalf, assess whether affected individuals also need to be contacted, and handle any subsequent ICO correspondence. This alone removes an enormous burden from a business owner who has no prior experience dealing with regulators under pressure.

Data Restoration. Recovering corrupted or encrypted data isn’t simply a matter of restoring a backup. Ransomware attacks, in particular, can compromise backup systems simultaneously. Cyber policies cover the cost of specialist data recovery services, rebuilding databases, and restoring systems to operational condition. The financial exposure here can be substantial, particularly for businesses whose entire operation depends on client records or proprietary files.

Business Interruption. If your systems are offline, your revenue stops. Business interruption cover within a cyber policy compensates for lost income during the period your operations are disrupted, helping you meet fixed costs — payroll, rent, supplier payments — while recovery work is underway.

The Emergency Response Team

One of the most underappreciated features of cyber cover is access to a coordinated incident response from the moment a breach is confirmed. Policies typically provide a dedicated helpline connecting you to IT specialists, legal advisors, and crisis communications professionals simultaneously. Rather than spending critical hours sourcing individual experts, you have a structured response team activated on your behalf. For reputation management, this matters enormously: a well-handled public statement in the first 24 hours can meaningfully reduce the long-term reputational damage that a poorly managed breach inflicts.

Third-Party Claims and Legal Defence

A data breach doesn’t just cost you internally. Clients or individuals whose data was compromised may pursue damages against your business. Cyber liability cover funds your legal defence and, where liability is established, covers the cost of any awarded damages. This is a distinct area of exposure that sits outside the scope of professional indemnity insurance, which responds to claims of professional negligence rather than data security failures. Understanding where one policy ends and another begins is essential to ensuring you’re not left with an uncovered gap.

If you want to understand precisely how these coverage layers map to your specific business, speaking with an independent broker is the most efficient route. Just Quote Me can assess your exposure and match you to a policy that covers the scenarios most relevant to how your business actually operates.

The Hidden Costs of a Data Breach for UK SMEs

Most small business owners, when they think about breach costs, think about the ransom demand or the IT repair bill. Those are real. But they’re often the smallest items on the final invoice. The costs that genuinely threaten business survival tend to arrive weeks and months later, quietly accumulating while you think the crisis is over.

Customer notification alone can be surprisingly expensive. If your business holds personal data for several hundred clients, you’re legally required to contact every individual whose data was compromised. That means drafting legally compliant communications, managing responses, and in some cases, offering credit monitoring services as a goodwill gesture. For a business without dedicated legal or communications support, this process can consume significant staff time and external resource costs simultaneously.

Then there’s the supply chain dimension. Contracts with larger clients, particularly in professional services or public sector supply chains, increasingly include data security clauses. A confirmed breach can trigger a clause review, a temporary suspension, or outright contract termination. Losing a single major client relationship as a direct consequence of a security failure can represent a revenue impact that dwarfs every other breach-related cost combined. This is precisely why cyber insurance for small business data breach scenarios needs to be understood as business continuity protection, not simply a technical expense policy.

GDPR Fines and Penalties

The ICO operates a two-tier fine structure under UK GDPR. The lower tier covers fines of up to £8.7 million or 2% of global annual turnover, whichever is higher. The upper tier, reserved for the most serious infringements, reaches up to £17.5 million or 4% of global annual turnover. For a small business, even a lower-tier fine calibrated to turnover can be existential.

One important legal nuance deserves clarity here: regulatory fines imposed by the ICO are generally not insurable under UK law, as public policy prevents insurance from indemnifying deliberate or reckless regulatory penalties. However, a well-structured cyber policy can cover the legal costs of responding to an ICO investigation, preparing your defence, and managing the notification process that determines whether a fine is issued at all. That distinction matters enormously in practice.

Reputational Damage and Loss of Trade

Reputational damage doesn’t appear on an invoice. It shows up in your pipeline three months later when a prospect quietly chooses a competitor, or a long-standing client doesn’t renew. For businesses operating in tight-knit regional communities across Staffordshire and the West Midlands, where professional reputation travels fast through local networks, this effect is amplified.

One practical step that works in tandem with cyber insurance for small business data breach cover is achieving Cyber Essentials certification, the UK government-backed scheme that demonstrates your business meets a defined baseline of cyber hygiene. Displaying that certification signals to clients and procurement teams that your security posture has been independently verified. Insurance funds your recovery; certification helps rebuild the trust that makes recovery commercially viable.

Understanding the full financial picture of a breach is the first step toward choosing cover that’s genuinely adequate. Just Quote Me’s cyber liability insurance service is built around exactly that assessment, matching your specific exposure to the right level of protection rather than defaulting to a generic policy limit.

Ready to protect your business from the full cost of a data breach?

Get Your Free Business Insurance Quote Now or Request a Callback for Free Expert Advice from one of our specialist brokers.

How to Choose the Right Cyber Policy for Your Business

Picking a cyber policy isn’t a box-ticking exercise. The right cover depends entirely on the specific data your business holds, how your operations are structured, and where your genuine exposure sits. A generic off-the-shelf policy might look adequate on paper and leave you critically underinsured when it actually matters.

Start with an honest data audit. Ask yourself what sensitive information your business actually processes. Customer payment details, employee records, medical information, and commercially confidential data all carry different risk profiles and different regulatory obligations. A business holding financial records for several hundred clients faces a materially different exposure than a sole trader whose only digital asset is a contact list. Your indemnity limit needs to reflect that reality, not a default figure chosen for its low premium.

Turnover is a useful but imperfect proxy for the right level of cover. A business generating £500,000 annually but holding data for thousands of individuals may need a higher indemnity limit than a £2 million turnover firm with minimal client data. The calculation should be driven by your notification obligations, your legal defence exposure, and your realistic business interruption costs, not just a percentage of revenue.

Exclusions deserve particular scrutiny. Social engineering attacks, where a criminal impersonates a supplier or executive to trick an employee into transferring funds or sharing credentials, are among the most common and costly breach scenarios facing small businesses. Some policies exclude them entirely or apply a sub-limit that bears no relation to actual losses. Read the exclusions before the headline figures.