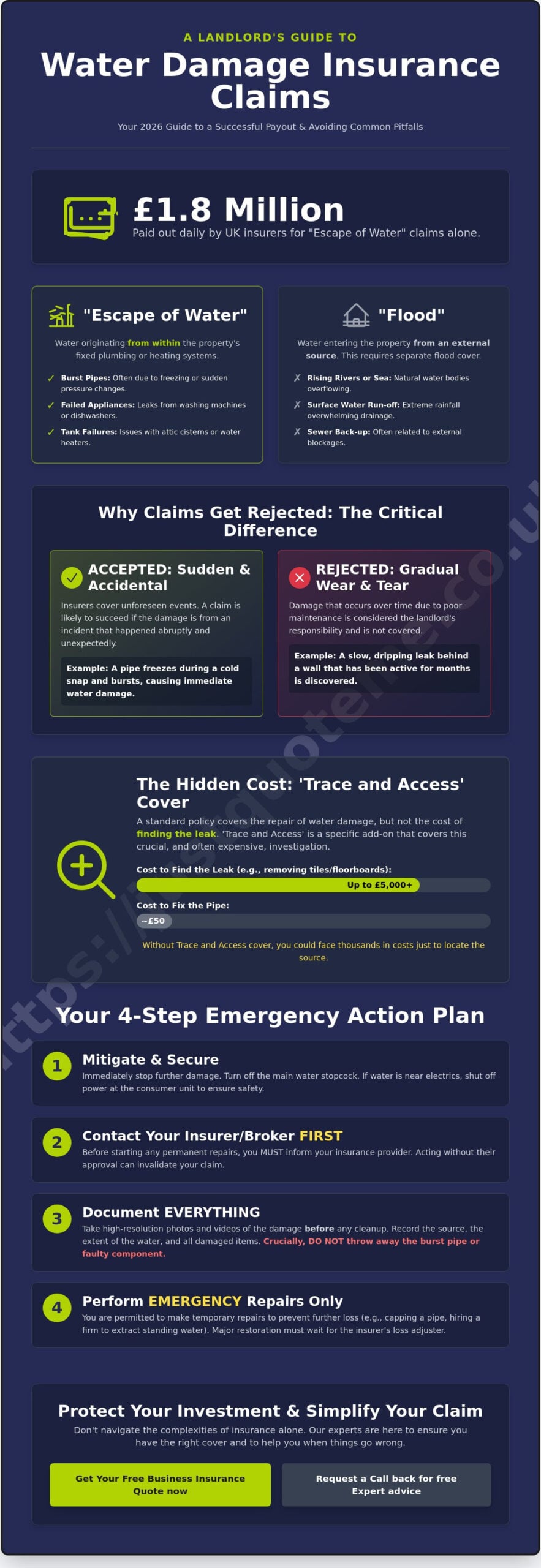

Did you know that UK insurers pay out approximately £1.8 million every single day for “escape of water” claims? Even with such high figures, the process of making a claim on landlord insurance for water damage is often fraught with hurdles that lead to immediate rejection. Most landlords fear the “maintenance issue” label, where a slow leak is dismissed as gradual wear and tear rather than a covered event.

We agree that administrative delays and technical jargon shouldn’t stand between you and a restored property. This 2026 guide simplifies the process, providing the exact steps to secure a successful claim while avoiding common pitfalls. You’ll gain a clear understanding of “Trace and Access” coverage and learn how to navigate the 2026 extension of Awaab’s Law to ensure your property remains compliant and protected.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Key Takeaways

- Learn to distinguish “Escape of Water” from external flooding to ensure your claim falls under the correct policy protection.

- Follow a precise step-by-step checklist to manage immediate damage and coordinate with your tenant without voiding your cover.

- Understand the “sudden and accidental” requirement to prevent your claim from being dismissed as a simple maintenance or wear-and-tear issue.

- Discover the essential documentation techniques, including why you must never throw away a burst pipe before the insurer sees it.

- Streamline the process of making a claim on landlord insurance for water damage by using a broker to manage complex negotiations with loss adjusters.

Understanding ‘Escape of Water’ and What Your Policy Covers

Clarity is your best tool when you are faced with a damp ceiling or a sodden carpet. In the insurance industry, we use specific terminology that dictates whether your payout is approved or declined. The most frequent term you will encounter is “Escape of Water.” This refers specifically to water that has originated from within the property’s fixed plumbing system, such as a leaking pipe, a heating system, or a storage tank. Understanding What is Water Damage? in a legal and insurance context helps you identify exactly which clause applies to your situation.

It is vital to distinguish this from “Flood” cover. While both involve unwanted water, a flood is generally defined as water entering the property from an external source, such as a rising river, sea surge, or extreme surface water run-off. Standard buildings insurance and specialized landlord insurance handle these risks differently. A landlord-specific policy is designed for the unique risks of rental properties, including higher unoccupancy limits and protection against tenant-related issues that a standard homeowner policy might exclude.

Success in making a claim on landlord insurance for water damage often depends on how the event occurred. Insurers look for “sudden and accidental” incidents. If water has been dripping behind a wall for six months due to poor maintenance, you may find your claim rejected. However, if a pipe freezes and bursts during a cold snap, you are on much firmer ground for a successful settlement.

Common Sources of Covered Water Damage

- Burst Internal Pipes: These are often caused by sudden pressure changes or freezing temperatures during winter months.

- Failed Appliance Seals: Water escaping from the internal plumbing of a washing machine or dishwasher often causes significant floor damage.

- Header Tank Failures: A failed ball valve in an attic cistern can lead to hundreds of litres of water cascading through the property in a matter of hours.

The Crucial Role of ‘Trace and Access’ Coverage

One of the most expensive aspects of a water claim isn’t the repair itself, but finding the leak. Many landlords assume their policy covers the cost of a plumber tearing up expensive floorboards or removing kitchen tiling to locate a pinhole leak. This is not always the case. “Trace and Access” is a specific clause that covers the costs of locating the source of the escape of water and making good the damage caused during that search.

Without this cover, you could be left with a bill for thousands of pounds just to find a pipe that costs fifty pence to fix. When making a claim on landlord insurance for water damage, always check your “Trace and Access” limits. Some policies cap this at £5,000, which can disappear quickly if you have to remove high-end finishes or navigate complex modern plumbing systems.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

The Landlord Checklist: Making Your Claim Step-by-Step

A water leak is a race against time. The actions you take in the first few hours determine whether your insurer pays out or finds a reason to decline. When making a claim on landlord insurance for water damage, your priority is to stop the flow without destroying the evidence. Turn off the stopcock immediately and instruct your tenant to avoid using any affected plumbing or appliances. If the water is near any electrical sockets or light fittings, shut off the power at the consumer unit to ensure the property is safe for inspection.

Before you hire a contractor for a permanent fix, you must contact your insurance provider. Many landlords make the mistake of repairing the damage first and asking for reimbursement later. This often leads to disputes over costs and the necessity of the work. You are legally allowed to perform emergency repairs to prevent further loss, such as capping a burst pipe or hiring a professional to extract standing water. However, major restoration must wait for the insurer’s green light. If you are unsure about what constitutes an emergency repair, speaking with an experienced broker can clarify the insurer’s specific expectations.

In the 2026 claims environment, loss adjusters rely heavily on digital evidence. They need high-resolution photos and videos of the damage before any cleanup begins. Capture the source of the leak, the extent of the water spread, and any damaged fixtures or landlord-owned furniture. This documentation is the backbone of a successful settlement. Keep a log of all communications with your tenant and any contractors who visit the site, as this timeline is vital for proving you acted swiftly to mitigate the damage.

The First 24 Hours: Critical Actions

- Step 1: Stop the flow and ensure the property is safe. Switch off the electricity if there’s any risk of contact with water.

- Step 2: Document the “as-is” state. Do not mop up or move furniture until you have clear photos of the water level and the immediate impact.

- Step 3: Call Just Quote Me to initiate the professional claims process. We handle the complex administrative burdens so you don’t have to.

Working with Your Tenants During a Claim

Under the Renters’ Rights Act 2025, which saw its first phase commence on May 1, 2026, your relationship with your tenant is more regulated than ever. If the water damage makes the property uninhabitable, you have a legal obligation to provide alternative accommodation or a rent abatement. Be transparent about drying-out timelines. Industrial dehumidifiers are loud and intrusive, so clear communication is essential to maintain a good tenant relationship. Ensure your tenants understand that they must allow access for loss adjusters and contractors to avoid delays in making a claim on landlord insurance for water damage.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Maintenance vs. Sudden Damage: Why Claims Get Rejected

One common reason for rejection when making a claim on landlord insurance for water damage is the distinction between a sudden accident and a maintenance failure. Insurance policies are not maintenance contracts; they are designed to cover “sudden and accidental” events. If a pipe bursts due to a sudden cold snap, it’s usually covered. However, if a joint has been weeping for months, insurers label it “gradual seepage.” This is a standard exclusion because the damage was preventable through regular upkeep.

“Wear and tear” is another frequent hurdle. If your property has ancient copper work or lead piping that has reached the end of its natural life, the insurer may argue that the failure was inevitable rather than accidental. Maintaining the property in a good state of repair is a fundamental condition of your cover. When a loss adjuster identifies rusted fittings or perished seals that should have been replaced years ago, they have a clear path to deny the claim. You must be able to show that the incident was an unforeseen event that occurred despite your best efforts to maintain the building.

Proving the Damage was Accidental

To secure your payout, you need evidence that the property was in good condition before the incident. Detailed property inspection reports are invaluable here. They prove you have been proactive in checking the plumbing and fixtures. A professional plumber’s report can also support your case by confirming the nature of the failure was sudden. In newer developments, you might encounter “latent defects” where poor construction causes a sudden failure. In these specific cases, your insurer might pay the claim and then seek to recover the costs from the builder’s warranty provider.

The Unoccupied Property Pitfall

Empty properties represent a significantly higher risk for water damage because a leak can go undetected for weeks. Most standard landlord policies trigger an unoccupancy clause after a property has been vacant for 30 consecutive days. Once this 30-day limit is reached, cover for risks like escape of water is often automatically removed or severely restricted. To keep your cover active during a void period, you must follow strict conditions. These often include draining the water system entirely or maintaining a minimum temperature, usually 12-15°C, to prevent pipes from freezing. If you anticipate long periods between tenants, choosing specialized residential letting insurance can provide the specific terms needed to protect your investment while it is empty.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Maximising Your Settlement: Evidence and Documentation

The success of your payout depends entirely on the quality of the evidence you provide. When making a claim on landlord insurance for water damage, you must act as a meticulous record-keeper from the moment the leak is discovered. Start by creating a comprehensive inventory of every affected item. This list should include floor coverings, kitchen units, and any furniture you provide as part of the tenancy. If you have receipts or original invoices for these items, attach them to your inventory to justify the replacement value.

One of the most frequent mistakes landlords make is disposing of the evidence too quickly. You must keep the “damaged part” that caused the escape of water. Whether it is a hairline crack in a copper pipe or a failed plastic valve, the loss adjuster may need to inspect it to verify the cause of the claim. If the faulty component is thrown away before inspection, the insurer might argue that the cause of loss is unproven. Once you have the evidence secured, obtain at least two like-for-like quotes for the restoration work. This ensures that the settlement offered by the insurer reflects the actual costs of labour and materials in the current market.

If the documentation process feels overwhelming while you are managing a property crisis, our specialists can help you organise your claim file to meet insurer expectations.

The Digital Evidence Pack

In 2026, a digital-first approach is essential for a fast settlement. Use your smartphone to take wide-angle shots of each affected room to show the full context of the damage. Follow these with macro (close-up) shots of the specific leak source and any secondary damage, such as peeling paint or warped skirting boards. If you can access a moisture meter, document the readings in different areas of the property to prove how far the water has travelled behind the surface. Maintain a chronological log of all communications with your tenants and contractors. This timeline is vital if the insurer questions the speed of your mitigation efforts.

Claiming for Loss of Rent

A major leak often forces tenants to vacate, resulting in a total loss of rental income. You can trigger the loss of rent clause in your landlord insurance if the property is deemed “uninhabitable.” Standards for habitability in Staffordshire and across the UK generally involve the loss of essential services like heating, water, or safe cooking facilities. To secure this part of your settlement, provide your insurer with a copy of the current tenancy agreement. They will use this to calculate the monthly loss and incorporate it into your total claim value, ensuring your cash flow remains stable while the property is being dried out and repaired.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Why an Independent Broker is Your Best Asset in a Water Claim

The moment you discover a leak, the pressure to act is immense. While many landlords default to calling their insurer’s automated claims line, there is a significant difference between speaking to a call centre operative and working with a personal broker. A call centre follows a rigid script and often lacks the authority to make nuanced decisions. In contrast, Just Quote Me acts as your dedicated advocate. We understand the technicalities involved in making a claim on landlord insurance for water damage and represent your interests when dealing with loss adjusters who may try to undervalue your settlement.

Our role is to simplify the administrative burden that often overwhelms property owners. By leveraging our established relationships with a panel of leading UK insurers, we ensure you have access to policies with superior wording. This includes higher limits for “Trace and Access” and more flexible unoccupancy terms. We don’t just help you file a claim; we guide you through the entire restoration process, ensuring that the “sudden and accidental” nature of the damage is clearly communicated to prevent unnecessary rejections.

Expert Advice Over Automated Systems

Experience matters when navigating the local property market. With 30 years of expertise serving landlords across Staffordshire and the West Midlands, we understand the specific risks associated with regional property types. This knowledge is particularly useful when dealing with commercial property insurance, where water damage can impact not just the building but also business continuity for your tenants.

We also work proactively to prevent the “average clause” from being applied to your claim. In 2025, rebuild costs rose significantly due to inflation in materials and labour. If your property is underinsured by even 20%, your insurer could proportionally reduce your payout. We help you calculate accurate rebuild values before an incident occurs, ensuring that when you are making a claim on landlord insurance for water damage, you receive the full amount required for repairs.

Next Steps for Your Property Protection

Securing your investment requires more than just reactive claiming. Now is the time to review your current policy limits, specifically focusing on your Trace and Access coverage and how your public liability insurance integrates with your water damage protection. If a tenant is injured due to a damp-related slip or a collapsed ceiling, you need to be certain your legal protections are robust and up to date.

- Review your policy for the 30-day unoccupancy trigger to avoid cover gaps during voids.

- Check that your Trace and Access limit is sufficient for modern, complex plumbing systems.

- Ensure your loss of rent cover matches your current tenancy agreements.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Protect Your Property Investment

A successful settlement relies on your ability to prove that damage was sudden and that you acted quickly to mitigate the loss. By prioritising thorough digital evidence and understanding the technical nuances of “Trace and Access” cover, you move from a position of uncertainty to one of control. Proactive maintenance remains your best defence against claim rejections, ensuring that when you are making a claim on landlord insurance for water damage, the facts and the policy wording are on your side.

Just Quote Me provides bespoke solutions for Staffordshire landlords, backed by 30+ years of industry experience and FCA-authorised expert advice. We manage the complex administrative burdens so you don’t have to, acting as your steady hand in a shifting market. Our team ensures your coverage is robust enough to handle the rising rebuild costs and legal requirements seen in 2026. Don’t wait for a leak to discover the gaps in your policy. You can protect your portfolio today with a partner who understands the local landscape and prioritises your recovery.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Frequently Asked Questions

Does landlord insurance cover water damage from a leaking roof?

Landlord insurance typically covers water damage from a leaking roof if the leak was caused by a sudden, insured event like a storm or a fallen tree. It won’t cover damage resulting from gradual wear and tear or a lack of maintenance. Insurers expect you to keep the roof in a good state of repair. If the felt or tiles have perished over time, any resulting water ingress is usually considered your financial responsibility.

How much is the average excess for an escape of water claim in the UK?

Excess amounts vary between providers, but many policies apply a specific “escape of water” excess that is higher than your standard buildings excess. While a standard excess might be £250, the escape of water portion often ranges from £350 to £500. You should check your policy schedule for these specific figures. Choosing a higher voluntary excess can lower your premium, but it increases your out-of-pocket costs when making a claim on landlord insurance for water damage.

Will my landlord insurance pay for a plumber to fix a burst pipe?

Most policies cover the damage caused by the water and the cost of “Trace and Access” to find the leak, but they don’t pay for the actual repair of the pipe itself. You are responsible for the cost of the new section of pipe or the plumber’s labour to fix the specific break. However, the insurer covers the more expensive aspects, such as drying out the property and replacing damaged floorboards or plasterwork affected by the burst.

What is the difference between flood damage and escape of water?

The primary difference lies in the source of the water. Escape of water refers to leaks originating from within the property’s fixed plumbing, such as a burst pipe or a leaking tank. Flood damage is caused by water entering the building from an external source, like a rising river or extreme surface water runoff. Insurers treat these as separate risks with different policy conditions and excess amounts.

Can I claim for water damage if my property was empty?

You can claim for water damage in an empty property if you have adhered to the specific unoccupancy conditions in your policy. Most standard policies trigger these rules after 30 consecutive days of vacancy. Common requirements include turning off the water at the stopcock or maintaining a minimum temperature of 12-15°C. If these conditions aren’t met, the insurer may reduce the payout or reject the claim entirely due to increased risk.

How long does a landlord insurance water damage claim usually take?

A straightforward claim can be settled in a few weeks, but complex water damage often takes several months to resolve fully. This is largely due to the “drying out” phase, which cannot be rushed without risking future mould issues. A loss adjuster must verify the property is completely dry before restoration work begins. Using a broker can help speed up the process by ensuring all documentation is submitted correctly the first time.

Does landlord insurance cover damage to the tenant’s belongings?

Your policy does not cover the tenant’s personal belongings, such as their clothes, electronics, or furniture. Landlord insurance only protects the building’s structure and any contents that you own as the property owner. It’s best practice to advise your tenants to take out their own contents insurance. This ensures they are protected if an escape of water destroys their personal property, as your insurance won’t compensate them for these losses.

What should I do if my water damage claim is rejected?

If your claim is rejected, your first step is to request a formal written explanation from the insurer citing the specific policy exclusion used. Review this against your policy wording to ensure the interpretation is correct. If you believe the rejection is unfair, you can follow the insurer’s internal complaints procedure. If the dispute remains unresolved, you have the right to escalate the matter to the Financial Ombudsman Service for an independent review.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice