Did you know that the average plumbing insurance claim reached £4,912 over the last year? In 2026, insurance isn’t just a safety net; it’s a ‘licence to trade’ that determines which lucrative contracts you can actually win. Understanding the specific plumbers insurance requirements uk is no longer a simple box-ticking exercise. It’s now the primary way to protect your livelihood against rising operational costs and increasingly strict regulatory scrutiny.

You’ve probably noticed that clients are asking for higher indemnity limits while the gap between legal mandates and commercial expectations grows wider. It’s natural to feel concerned about whether your current policy would actually pay out or if a simple oversight could lead to a £2,500 daily fine. We understand that you want to focus on the tools, not the paperwork, but staying informed is the only way to ensure your business remains resilient in a shifting market.

This guide provides a straightforward roadmap to help you stay compliant and competitive. We will examine the mandatory Employers’ Liability standards, the commercial necessity of Public Liability, and the critical 2026 updates regarding Gas Safe registration and the June 30 deadline for RPZ valve testing. By the end, you’ll have the clarity needed to Just Quote Me with confidence, knowing your cover is robust and your business is fully protected.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Key Takeaways

- Identify the single legal mandate of Employers’ Liability and how to avoid the heavy daily fines associated with non-compliance.

- Understand why Public Liability is a commercial essential for winning larger contracts and which coverage limits are now expected by UK clients.

- Navigate the complex plumbers insurance requirements uk to ensure your professional indemnity and Gas Safe certifications are perfectly aligned.

- Protect your high-value assets with specific cover for tools and plant machinery that standard van insurance typically excludes.

- Learn how a bespoke approach to your policy can simplify administrative burdens while providing a steady hand in a changing market.

What Insurance is Legally Required for Plumbers in the UK?

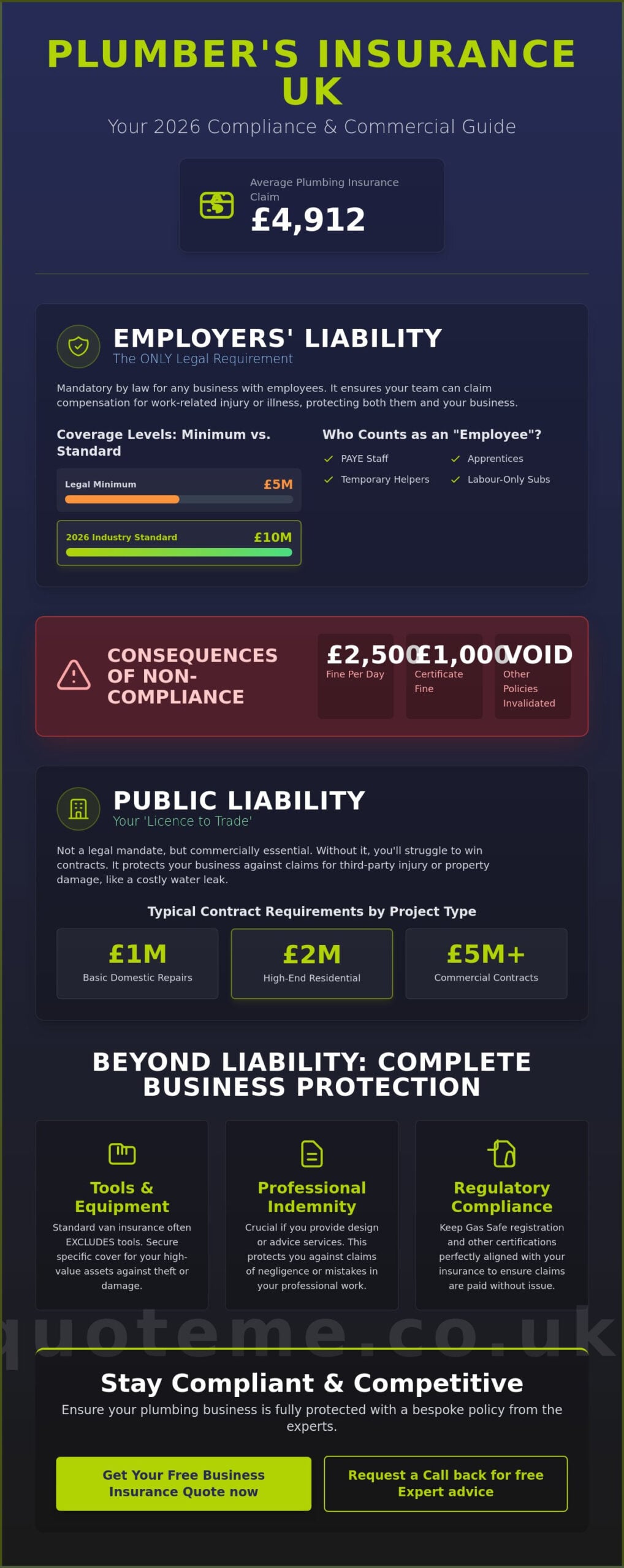

While you might need various types of cover to trade safely and win contracts, only one specific policy is mandated by UK law. The Employers’ Liability (Compulsory Insurance) Act 1969 dictates that any business with employees must have cover in place. This legislation ensures that if a member of your team is injured or falls ill as a direct result of their work, they can claim compensation. This requirement is a cornerstone of Liability insurance, providing a financial safety net that protects both the worker and the business owner. Getting this right is the first and most critical step in meeting the plumbers insurance requirements uk.

The law requires a minimum of £5 million in cover, though most standard policies in 2026 provide £10 million to account for rising legal costs. You don’t have a choice in this matter if you have even one person working for you. The only common exemption is for sole traders who work entirely alone, or limited companies where the sole director owns more than 50% of the share capital and has no other employees.

Employers’ Liability: Who Counts as an Employee?

The legal definition of an “employee” is often broader than many plumbing contractors realise. It isn’t limited to those on a permanent PAYE contract. If you use apprentices, part-time helpers, or temporary staff to help with a heavy workload, you are legally an employer. Labour-only subcontractors also trigger this requirement. These are individuals who work under your direct supervision, use your tools, and do not provide their own materials. Because they don’t operate with the independence of a bona fide subcontractor, the law views them as your responsibility. For any growing firm, securing employers liability insurance is a non-negotiable administrative task that prevents catastrophic legal exposure.

Legal Consequences of Non-Compliance

The Health and Safety Executive (HSE) enforces these regulations with significant rigour. If you’re found to be trading without valid EL cover while employing staff, the financial penalties are steep. You can be fined up to £2,500 for every single day you operate without the correct insurance. There is also a £1,000 fine for failing to display your ‘Certificate of Insurance’ or refusing to make it available to HSE inspectors when asked. Beyond the fines, a lack of legal cover can have a domino effect on your business. Many insurers will invalidate your other protections, such as public liability or tools cover, if they discover you’ve breached your statutory duties. It’s a risk that can end a plumbing career overnight.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Commercial Requirements: Public Liability and Contract Limits

Public Liability (PL) insurance often creates confusion for new tradespeople. Unlike the legal requirement for employers’ liability insurance, PL isn’t strictly mandated by UK law for sole traders. However, for any working plumber, it functions as a ‘licence to trade’. Without it, you’ll struggle to find a reputable main contractor or trade association willing to work with you. It protects your business against claims for third-party injury or property damage. For a plumber, this usually involves the classic nightmare scenario: a major water leak causing thousands of pounds of damage to a client’s home or a commercial building’s infrastructure.

Industry standard limits typically start at £1 million, but these are increasingly seen as insufficient for anything beyond basic domestic repairs. Many commercial contracts and even some high-end residential projects now demand £2 million or £5 million as a baseline. Meeting these plumbers insurance requirements uk is essential if you want to move beyond small call-out jobs and into more profitable contract work. If you’re working on projects where a mistake could lead to significant structural damage, a higher limit provides the security you need to operate without fear of personal financial ruin.

Choosing the Right Limit for Your Contracts

The limit you choose should reflect your highest-risk environment. While £1 million might cover a minor domestic flood, it won’t touch the sides of a claim involving structural damage to a block of flats or a public facility. Trade associations frequently require members to hold public liability insurance with specific minimums to maintain accreditation. Cutting corners on indemnity limits might save a few pounds on monthly premiums, but it can cost you thousands in lost revenue when you’re disqualified from a lucrative project during the vetting stage. If you’re unsure which level fits your current workload, speaking with a specialist broker can help clarify your needs.

Winning Tenders in the West Midlands

Local context matters when applying for council work. In areas like Newcastle-under-Lyme and Stafford, local authority tenders often set a strict £5 million Public Liability baseline. This is standard for any work involving schools, council housing, or public buildings in Staffordshire. To win these bids, you must provide a valid certificate of insurance during the pre-qualification questionnaire (PQQ) phase. Main contractors in the West Midlands are equally rigorous; they need to know that your policy covers the specific risks of the site. As your business scales, you can easily increase your indemnity limits to match the requirements of larger, more complex projects without disrupting your existing coverage.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Protecting Your Assets: Tools, Plant, and Equipment

Tool theft remains a significant threat to the UK plumbing trade, with thieves often targeting vans for high-value items like press tools and expensive power drills. Relying solely on your vehicle’s motor policy is a common mistake. Standard van insurance covers the vehicle’s bodywork and engine, but it rarely extends to the specialist equipment inside. Given that the average insurance claim for a plumber reached £4,912 between April 2025 and March 2026, failing to secure specific asset protection can leave you with a massive bill to pay before you can return to work. Understanding these plumbers insurance requirements uk is vital for maintaining your daily operations.

Protection should also extend to your materials. Stock in transit cover is essential when you’re transporting high-value boilers or large quantities of copper piping to a job site. If these items are stolen or damaged in a collision before they are installed, a standard liability policy won’t provide a penny toward their replacement. By ensuring your materials are covered from the moment they leave the merchant, you protect your profit margins from unexpected losses.

Tool Insurance and Security Requirements

In 2026, insurers are increasingly strict about how you store your equipment. Many policies include an “overnight storage” clause, which may invalidate your claim if tools are stolen from your van while it’s parked on the street after a certain hour. To ensure your van tools insurance remains valid, you must check if your policy requires a specific level of van security or if tools must be removed from the vehicle at night. Keeping a digital, up-to-date inventory with serial numbers and photos is the best way to speed up a claim. When choosing cover, decide between “replacement as new,” which buys you a brand-new tool, or “indemnity value,” which only pays the current second-hand value of the item.

Plant and Machinery Coverage

Your responsibility doesn’t end with the tools you own. If you hire an excavator for groundworks or a specialized drain camera for a complex diagnostic job, you are often contractually liable for that equipment while it’s in your possession. If a hired-in machine is damaged or stolen, the hire company will expect you to cover the full replacement cost and their lost hire revenue. Dedicated plant machinery insurance manages this risk, ensuring you aren’t personally liable for expensive equipment that doesn’t belong to you. For those working on major projects, Contractors All Risk insurance provides the ultimate shield by combining cover for the permanent works, your own tools, and hired-in plant under one comprehensive policy.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Professional Requirements: Design Advice and Gas Safety

Beyond the physical risks of leaks and injuries, modern plumbers often take on the role of a consultant. When you recommend a specific heating system or design the layout of a plant room, you’re providing professional advice. If that advice leads to a financial loss for the client, even without physical damage, standard public liability might not cover you. This is a nuanced area of the plumbers insurance requirements uk that many tradespeople overlook until a dispute arises. It’s about ensuring your intellectual input is as protected as your manual labour.

Another critical element is the ‘efficacy’ clause. This is a common condition in trade policies stating that the work you perform must actually achieve its intended purpose. For example, if you install a backflow prevention system that fails to prevent contamination because it was the wrong specification for the job, an efficacy clause helps define the insurer’s liability. Ensuring your policy includes this protection is vital for anyone working on complex commercial systems or high-specification domestic projects where performance is guaranteed.

Do Plumbers Need Professional Indemnity?

The line between ‘doing’ and ‘designing’ is thinner than you think. If you simply install a boiler the client bought, you’re a contractor. If you specify the boiler based on your own heat loss calculations, you’re a designer. For those providing specifications, professional indemnity insurance is essential. Consider a scenario where an incorrectly specified boiler fails to heat a large property sufficiently. The client may sue for the cost of replacing the unit and the associated disruption; a claim for professional negligence that falls outside the scope of property damage. Protecting your advice ensures a single calculation error doesn’t derail your business.

Gas Safe and Specialist Risks

Your insurance must align perfectly with your trade certifications. If you are on the Gas Safe Register, your policy must explicitly cover ‘hot work’, such as the use of blowtorches. Many standard policies have strict conditions regarding fire safety, including having a fire extinguisher at hand and performing a fire watch after the work is complete. For those involved in new-build plumbing, contractors all risk insurance provides a broader umbrella that covers the works in progress against fire, flood, or theft. For new registrants in 2026, remember that the mandatory three-month probationary period requires you to notify the Gas Safe Register of all jobs. Your insurer needs to know you’re operating within these regulatory boundaries to maintain valid cover.

Ready to ensure your professional advice is fully protected? Talk to our experts today to align your cover with your certifications.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Bespoke Brokerage: Why ‘Just Quote Me’ is the Plumber’s Choice

Managing the administrative burden of a trade business shouldn’t take you away from your clients. With over 30 years of experience in the UK market, we’ve seen how the plumbers insurance requirements uk have evolved into a complex set of rules. We act as your trusted advisor, navigating these changes so you don’t have to. Our team provides a human-centric alternative to the faceless, automated bots found on many comparison sites. Based in Staffordshire, our advisors offer local expertise and a pragmatic approach to securing your livelihood.

By using a broad panel of insurers, we find competitive pricing that matches your specific risk profile. We handle the heavy lifting of policy comparison and jargon-busting. This allows you to focus on your trade while we ensure your business remains compliant and contract-ready. Our commitment to efficiency means you get the cover you need without unnecessary delays or hidden gaps in protection. We understand the nuances of the 2026 market, providing a steady hand when you need it most.

The Value of an Independent Broker

Standard ‘off-the-shelf’ policies often fail to account for the nuances of your daily work. They might overlook the specific hot work requirements or the professional indemnity needs discussed in previous sections. We tailor tradesman insurance to fit your exact business size, whether you’re a sole trader in Stone or a large firm in Stafford. This bespoke approach ensures you aren’t paying for redundant cover while filling the gaps that leave you vulnerable. We know the West Midlands market and the specific expectations of local contractors, giving you a competitive edge when tendering for work.

Ready to Secure Your Business?

You need straightforward advice that cuts through the noise. We simplify the process of staying insured and compliant, providing the security you need to grow your business with confidence. Don’t leave your protection to chance or a generic algorithm. Choose a partner who understands the tools of your trade and the risks you face every day. Our goal is to provide a personalized and frictionless experience that lets you get back to the job at hand.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Future-Proof Your Plumbing Business Today

Meeting the plumbers insurance requirements uk is about more than just avoiding the HSE’s £2,500 daily fines for missing Employers’ Liability. It’s about building a reputation for reliability that helps you win high-value tenders in Staffordshire and beyond. By aligning your cover with your Gas Safe certifications and securing professional indemnity for your design work, you protect your business from every angle.

Whether you’re a sole trader or managing a growing team, the right protection provides the confidence to take on larger projects. As an FCA Authorised and Regulated broker with over 30 years of industry experience, we specialize in providing bespoke cover from top UK insurers. We handle the complex administrative burdens so you can focus on the tools. Take the next step in securing your professional future. Just Quote Me today and ensure your business is fully compliant for the year ahead.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Frequently Asked Questions

Is Public Liability insurance a legal requirement for plumbers in the UK?

Public Liability insurance isn’t a legal requirement under UK law, but it’s a commercial necessity for any professional plumber. Most main contractors, local authorities, and trade associations will refuse to hire you without it. It protects your livelihood from the financial fallout of third-party injuries or property damage, which is essential given the high risks associated with water leaks and gas work.

How much cover do I need for local council plumbing contracts?

You typically need a minimum of £5 million in Public Liability cover for council work. Local authorities across the West Midlands often set this as the baseline for any projects involving public buildings, schools, or social housing. You should always check the specific tender documents, as some larger infrastructure projects may occasionally require limits as high as £10 million to manage the increased risk.

Does my plumbers’ insurance cover me for hot work like soldering?

It only covers you if ‘hot work’ is explicitly included in your policy schedule. Many insurers have strict fire safety conditions you must follow, such as having a fire extinguisher on-site and performing a mandatory ‘fire watch’ for 30 minutes after you finish soldering. Failing to meet these specific plumbers insurance requirements uk could lead to a rejected claim if a fire occurs.

What is the minimum Employers’ Liability limit required by law?

The legal minimum for Employers’ Liability insurance is £5 million. Most reputable UK insurers provide £10 million as a standard offering to ensure you are fully protected against rising legal fees and compensation costs. This cover is mandatory the moment you hire an apprentice, part-time helper, or labour-only subcontractor, even if they’re only helping you for a single day.

Can I get insurance that covers my tools overnight in my van?

Yes, you can, but it usually requires a specific ‘overnight storage’ clause. This often mandates that the van is fitted with an alarm, parked in a secure location, or that high-value items are removed. Since tool theft claims averaged nearly £5,000 recently, checking the fine print of your van tools policy is vital to ensure your equipment is actually protected while you sleep.

Do I need Professional Indemnity if I only do domestic repairs?

You generally don’t need it for simple ‘like-for-like’ repairs, but you do if you provide design advice or specifications. If you recommend a specific system layout or specify a boiler size for a customer, you’re acting as a consultant. Professional Indemnity protects you if your advice leads to a client’s financial loss, even if no physical damage occurs during the installation.

How do I prove to a client that my insurance is valid?

You provide a ‘Certificate of Insurance’ or a ‘To Whom It May Concern’ letter from your broker. This document lists your policy numbers, expiry dates, and indemnity limits. It’s standard practice to carry digital copies on your phone or tablet so you can immediately reassure clients or main contractors that your plumbers insurance requirements uk are fully met before you start work.

What happens if I don’t have the legal minimum insurance?

You face severe financial and legal penalties from the Health and Safety Executive (H&SE). Operating without mandatory Employers’ Liability can result in fines of up to £2,500 for every single day you are uncovered. You can also be fined £1,000 for failing to display your insurance certificate, and a lack of legal cover may void your other business protections.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice