by jqm | Jul 17, 2026 | Insurance

If your sports club faced a £10 million liability claim tomorrow, would your committee members be personally liable for the shortfall? It’s a sobering thought for anyone volunteering their time to lead a local team. You shouldn’t have to risk your personal financial security just to support your community’s passion for sport. We know that running a club involves complex risks, and finding the right sports club insurance often feels like an exhausting administrative hurdle rather than a protective benefit.

We understand that the 2026 regulatory landscape can be difficult to navigate, especially with many National Governing Bodies now requiring a minimum of £10 million in public liability cover as standard. You need a solution that balances these strict requirements with affordable premiums that don’t drain your club’s budget. This article explains how to protect your committee, staff, and members with bespoke insurance tailored to your specific activities. We will break down the legal requirements for volunteers, the essentials of clubhouse maintenance cover, and how to ensure your policy satisfies every mandate for the 2026/27 season. You will gain a clear roadmap to securing your club’s future without the stress of complex paperwork or hidden costs.

Key Takeaways

- Understand how the legal “duty of care” makes your organisation responsible for the safety of participants, spectators, and the general public.

- Identify the essential coverage needed to close the “volunteer loophole” and protect non-paid staff under your Employers Liability policy.

- Learn how Trustees and Directors Indemnity acts as a vital shield for committee members, protecting personal assets from claims of mismanagement.

- Follow a practical step-by-step guide to auditing your club’s specific activities and property to secure bespoke sports club insurance.

- Discover why partnering with a specialist broker offers a more reliable, human-centric alternative to automated insurance quote engines.

What is Sports Club Insurance & Why is it Essential in 2026?

Sports club insurance isn’t just a single policy. It’s a strategic package of covers designed to protect your organization from liability, property damage, and financial loss. At its core, What is Insurance? It’s the transfer of risk from your club to a provider, ensuring that an unexpected accident doesn’t lead to total financial ruin. In 2026, this transfer is more critical than ever as legal and medical costs continue to climb.

Every club holds a “Duty of Care” toward anyone interacting with their activities. This means you’re legally responsible for the safety of participants, spectators, and the general public. If a spectator trips over a loose piece of equipment or a player is injured due to poor pitch maintenance, the club is often the first point of blame. Without robust protection, the financial burden of defending these claims falls directly on the club’s shoulders.

The legal environment in 2026 is increasingly litigious. Many National Governing Bodies (NGBs) have responded by tightening their affiliation rules. For example, some regional football associations now mandate a minimum of £10 million in public liability insurance for the 2026-27 season. While some “Association” policies offer basic cover as part of your affiliation, these are often generic. A bespoke policy ensures your specific risks, such as clubhouse bars, specialized equipment, or travel for away matches, are fully addressed.

Legal Requirements vs. Recommended Protection

Legal mandates often surprise committee members. Even if your club is run entirely by volunteers, you still have legal obligations. UK law requires employers liability insurance if you have any staff, which includes part-time workers and often volunteers in a legal context. The minimum legal requirement is £5 million, but the standard offering from most insurers has moved to £10 million to reflect the reality of modern claims. Additionally, most local authorities won’t allow you to hire their pitches or community halls without proof of significant public liability cover.

Who Needs This Cover?

This protection isn’t reserved for professional outfits or large leisure centres. It’s essential for any group that organises physical activity or manages a community space. This includes:

- Amateur football, cricket, and rugby teams playing in local leagues.

- Social clubs and community organisations with a sporting focus.

- Specialised groups like martial arts schools, gymnastics clubs, or dance studios where the risk of injury is naturally higher.

- Leagues and associations that oversee multiple teams or tournaments.

Whether you’re a small grassroots team or a large multi-sport complex, having the right sports club insurance ensures you can focus on the game rather than the paperwork.

Core Coverage: Protecting Your Assets and People

Building on the duty of care mentioned in the previous section, your sports club insurance must address specific operational risks. It’s not enough to have a generic policy. You need coverage that accounts for everyone from the star player to the person serving tea at halftime. Without these core protections, a single accident could lead to a claim that exceeds your club’s total assets.

Public Liability for Sports Clubs Explained

Imagine a spectator is hit by a stray ball during a match, or a visitor slips on a wet floor in your changing rooms. These scenarios lead to third-party injury claims that can reach hundreds of thousands of pounds. Public Liability Insurance provides the legal defence and compensation costs to handle these situations. For the 2026-27 season, many organisations like the East Riding FA now require a minimum indemnity of £10 million. It’s also vital to check if your policy includes product liability. If your club sells merchandise or food, you’re responsible for any illness or injury caused by those products.

Employers Liability: It Is Not Just for “Employees”

A common misconception is that clubs without a payroll don’t need Employers Liability Insurance. In reality, the legal definition of an “employee” often extends to volunteers, students on work placements, and helpers. If a volunteer is injured while performing duties for the club, they have the same right to claim as a paid member of staff. While the legal minimum is £5 million, most insurers provide £10 million as standard to ensure you’re fully protected against rising legal costs.

Personal accident cover provides a different layer of security. It pays out a fixed sum for specific injuries sustained during club activities, such as broken bones or permanent disablement. For instance, some 2026 rugby league policies offer up to £500 for broken bones and £50,000 for accidental death for those aged 16 and over. This isn’t about liability; it’s about supporting your members when they need it most. You should also consider the physical assets your club owns. From expensive maintenance machinery like lawnmowers to team kits and historical trophies, property cover ensures you can replace essential items if they’re stolen or damaged.

Ensuring every angle is covered requires a professional touch. You can explore tailored options to find a policy that fits your club’s unique setup.

Protecting the Committee: Trustees and Directors Indemnity

While previous sections focused on physical injuries and property damage, this layer of protection addresses the “brain” of your organisation. Many volunteers join a committee with a passion for the game, unaware that they could be held personally liable for the club’s administrative failures. In the UK, if your club isn’t incorporated, committee members are often treated as individuals in legal disputes. This means your personal bank account, car, or even your home could be at risk if the club is sued for mismanagement or financial errors. Comprehensive sports club insurance must include Directors and Officers (D&O) cover to prevent this nightmare scenario.

Trustees Indemnity, often referred to as D&O insurance, protects personal assets against claims of “wrongful acts.” These aren’t criminal deeds; they’re usually honest mistakes in club administration. Examples include a breach of trust, negligence in managing club funds, or errors in financial reporting that lead to a loss. If a disgruntled member or a third party alleges that the committee’s decisions caused them financial harm, this policy pays for your legal defence and any resulting settlements. Without it, you’re essentially volunteering your personal financial security along with your time.

Managing Personal Liability for Volunteers

A bespoke policy acts as a vital shield between your private life and your club duties. It ensures that legal challenges regarding how the club is run don’t spill over into your personal finances. If your club provides specific instruction, such as technical coaching or dietary advice, you also need to consider Professional Indemnity Insurance. This covers you if a member suffers a loss or injury because they followed professional advice provided by the club that turned out to be negligent.

Cyber Security for Modern Sports Clubs

In 2026, even the smallest local teams are digital entities. You likely hold sensitive member data, including addresses, medical records, and payment details. GDPR compliance remains a strict requirement, and the risk of a data breach is a reality for any group with an online presence. Small clubs are often seen as soft targets for phishing and payment fraud because they lack the sophisticated IT departments of larger corporations. Integrating Cyber Insurance into your package helps you manage the aftermath of a hack. It covers the costs of notifying members, recovering data, and defending against legal action from affected individuals. Protecting your digital assets is now just as important as maintaining your physical grounds.

A Step-by-Step Guide to Buying Sports Club Insurance

Buying sports club insurance requires a methodical approach to ensure you aren’t paying for cover you don’t need or, worse, leaving gaps in your protection. Start by auditing every activity your club undertakes. This includes match days, but also social events, ground maintenance, and travel to away fixtures. If you only insure for the 90 minutes on the pitch, you’re exposed during the other six days of the week.

Next, assess your physical assets. Do you own the clubhouse, or are you just responsible for the equipment stored inside? You also need to confirm specific National Governing Body (NGB) requirements. As we’ve seen with the East Riding FA’s 2026 mandates, these levels can change. Finally, gather your data. You’ll need accurate membership numbers, annual turnover figures, and a clear claims history from the last three to five years. This data allows a broker to find the most competitive rates for your specific risk level.

Specialist Risks: Clubhouses and Maintenance

If your club owns its premises, you need robust Commercial Property Insurance to guard against fire, flood, and vandalism. Maintenance carries its own set of dangers. If your volunteers use heavy equipment or perform floodlight repairs, you must account for these high-risk tasks. Specialized Plant & Machinery Insurance covers the tools that keep your grounds playable, while ensuring your liability cover extends to working at height. Don’t assume a general policy covers these niche activities; always check the fine print for exclusions regarding maintenance work.

Event Insurance for Tournaments and Fundraisers

Standard annual policies might not cover large-scale one-off events like summer tournaments or gala dinners. You may need specific event cover to handle the increased footfall and unique risks of fundraisers. If your club operates a bar or social hub, liquor liability is a non-negotiable addition. This protects the club if an alcohol-related incident occurs on the premises. For clubs with a permanent bar facility, Nightclub & Social Club Insurance provides the specific legal protections required for hospitality environments.

Avoid the trap of rigid, off-the-shelf packages that don’t reflect your club’s actual operations. You can get a tailored insurance quote that matches your specific risk profile and budget. Using an independent broker allows you to compare the entire market and find a policy that satisfies both your NGB and your committee’s peace of mind.

Why Just Quote Me is the Trusted Partner for UK Sports Clubs

Just Quote Me isn’t another faceless corporation or a rigid automated system. Since 1989, we’ve operated as an independent broker with a clear mission: to simplify the insurance process for organisations that serve our communities. We understand that committee members have better things to do than sit on hold with a call centre. When you contact us, you speak with an expert who understands the nuances of sports club insurance and the specific risks your team faces. Our personality is defined by a pragmatic attitude toward the industry, projecting the image of a partner who manages complex administrative burdens so you don’t have to.

Our 30-year heritage provides us with unique leverage in a crowded market. We’ve built long-standing relationships with a broad network of top UK insurers, allowing us to find coverage that fits your specific needs rather than forcing you into a generic box. As an FCA-authorised firm, we provide the authority of an established industry leader with the accessibility of a local provider. We pride ourselves on being a human-centric alternative to automated quote engines, offering a steady hand to help you through the 2026 regulatory changes.

Regional Expertise in Staffordshire and Beyond

We take pride in our deep roots in the local community. With a presence in Stone, Stafford, and Newcastle-under-Lyme, we have a thorough understanding of the West Midlands and Staffordshire sporting landscape. This regional focus is more than just a location; it’s a marker of quality. We know the specific requirements of local authorities when you hire their facilities or pitches. We also understand the regional risks associated with local grounds, from specialized property maintenance to the security of community-owned clubhouses.

This specialized knowledge allows us to secure terms that generalist brokers often overlook. Whether your club deals with complex risks like working at height for floodlight repairs or specialized property maintenance, our experience ensures these niche activities are fully covered. We use our regional expertise to differentiate our service from larger, more impersonal competitors, ensuring you get advice that’s relevant to your local area.

The Just Quote Me Difference

Choosing us means handing over the stress of risk management to professionals. We don’t just provide a policy; we provide a partnership. Our team offers transparent advice on exactly what you need to satisfy NGB mandates for the 2026/27 season, and just as importantly, what you don’t. We help you avoid the rising costs of public liability claims by ensuring your policy is structured correctly from the start. Our communication rhythm is fast-paced and logical, designed to move you from inquiry to protection without unnecessary detail.

We believe in a pragmatic approach to protection that balances cost with essential cover. Whether you’re managing a small grassroots football team or a large multi-sport complex, we find the bespoke solution that offers security without sacrificing value. Our goal is to ensure your committee feels fully informed and secure, allowing you to focus on the game itself. We manage the complex administrative burdens so the client does not have to, providing a personalized and frictionless experience.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Secure Your Club’s Future Today

The safety of your players and the financial security of your committee shouldn’t be left to chance. The 2026 regulatory landscape demands higher indemnity limits and a more thorough understanding of volunteer liability. By auditing your specific activities and closing the “volunteer loophole,” you transform your cover from a basic requirement into a strategic shield for your organisation.

Just Quote Me brings over 30 years of industry experience to the table as an FCA authorised independent broker. We focus on the unique risks of your facility, whether you’re managing a clubhouse in Stone or a league in Newcastle-under-Lyme. We handle the complex administrative tasks so you can get back to the sport you love. Visit our homepage to see how we can protect your team.

Don’t wait for a claim to discover gaps in your protection. Just Quote Me today to ensure your sports club insurance provides the peace of mind your team deserves. Building a safer environment for your members starts with the right partner.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Frequently Asked Questions

Is sports club insurance a legal requirement in the UK?

Employers’ Liability is a legal mandate if your club has any employees, which often includes part-time staff and volunteers. While Public Liability isn’t a universal statutory law, it’s a mandatory requirement for affiliation with most National Governing Bodies and for hiring local authority facilities. Operating without it leaves your committee members exposed to significant personal financial risk from third-party claims.

Do we need insurance if all our members are volunteers?

Yes, because you still hold a legal duty of care toward everyone involved in your activities. Volunteers are entitled to a safe environment; if they’re injured due to club negligence, they have the right to seek compensation. Public liability is also essential to protect the club against claims from spectators or the general public, regardless of whether your staff are paid or unpaid.

How much does public liability insurance for a sports club cost?

Premiums are calculated based on your specific risk profile, including membership numbers, the type of sport played, and your claims history. Because we offer bespoke sports club insurance, we avoid the rigid pricing of off-the-shelf packages. This approach ensures your club pays a fair rate that reflects your actual activities rather than a generic industry average that might include risks you don’t face.

Does sports insurance cover injuries to players during a match?

Standard liability policies often exclude injuries caused by one player to another during play, which is why specialized Personal Accident cover is vital. This provides fixed financial payouts for specific injuries such as broken bones, dental damage, or permanent disablement. It ensures that your members have a financial safety net regardless of who was at fault for the accident on the pitch.

What is Trustees’ Indemnity insurance and why do we need it?

This insurance protects the personal assets of your committee members against claims of mismanagement or “wrongful acts” in club administration. If your club is unincorporated, committee members can be held personally liable for financial errors or legal breaches. This cover acts as a shield, ensuring that a professional mistake at the club level doesn’t lead to personal financial ruin for your volunteers.

Are we covered for social events and fundraisers like BBQs or gala days?

Most annual policies cover standard club social activities, but high-risk events or those with a high footfall may require a specific extension. If you’re planning a gala day with external vendors or a BBQ involving alcohol, you should confirm this with your broker. We can tailor your sports club insurance to include these one-off fundraisers so your protection remains continuous throughout the year.

Can we get insurance if we don’t own our own grounds or clubhouse?

Yes, many clubs operate successfully by hiring local authority pitches or community centres. In these instances, your policy focuses on liability risks and the protection of your portable assets like kits, goals, and training equipment. Even without a building to insure, you still need robust liability cover to satisfy the requirements of the facility owners and to protect your members.

What happens if we have a claim—how does Just Quote Me help?

We act as your dedicated advocate and manage the entire claims process on your behalf. Instead of navigating complex insurer portals alone, you’ll work with an expert who understands your policy and your club’s history. We handle the administrative communication with underwriters to ensure a fair and efficient resolution, allowing your committee to stay focused on running the team.

Article by

Just Quote Me

JustQuoteMe Ltd is an independent UK insurance brokerage specialising in business and personal insurance solutions. With over 35 years of industry experience, the company provides tailored insurance cover for businesses, landlords, tradespeople, hospitality venues, fleets, and individuals across the UK. Known for its personal service, expert advice, and competitive premiums, JustQuoteMe Ltd works with leading insurers to deliver bespoke policies designed around each client’s unique needs. The company is authorised and regulated by the Financial Conduct Authority (FCA No. 586607) and has built a reputation for trusted, straightforward insurance guidance and long-term client relationships.

by jqm | Jul 16, 2026 | Insurance

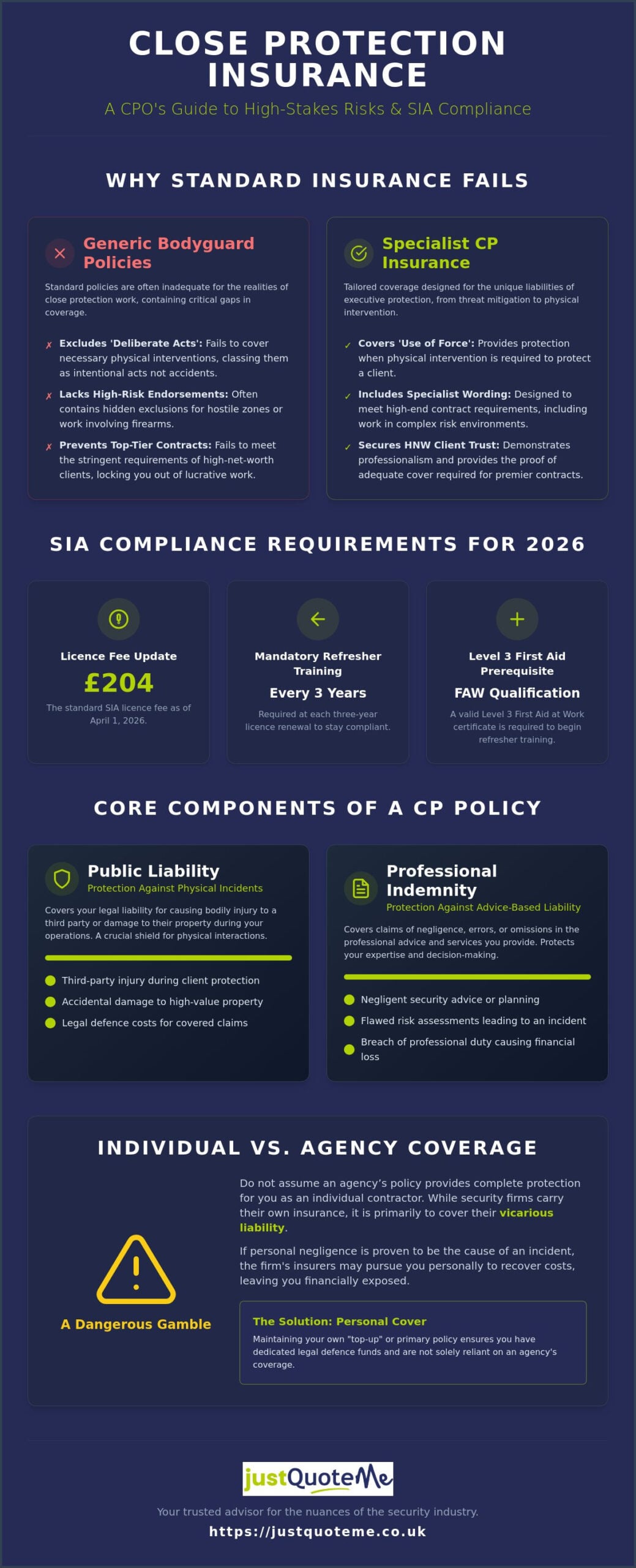

Would your current insurance policy hold up if a routine transit for a high-net-worth client turned into a high-stakes security incident? You understand that close protection work is fundamentally different from standard security roles, yet many generalist brokers fail to grasp the high-risk nature of your environment. It’s frustrating to find that your Close Protection insurance contains hidden exclusions for hostile zones or lacks the necessary cover for the carriage of firearms just when you need it most.

We agree that your professional liability shouldn’t be left to chance or buried under layers of complex corporate jargon. This article will show you how to secure comprehensive, SIA-compliant cover that protects your career, your clients, and your reputation. You’ll discover the essential requirements for 2026, including the mandatory refresher training and Level 3 First Aid qualifications now required for licence renewals. We will also clarify the critical differences between personal and corporate liability to ensure you have total peace of mind on every contract. Just Quote Me simplifies this complex administrative process, acting as your trusted advisor so you can stay focused on the task at hand.

Key Takeaways

- Learn the critical distinction between generic bodyguard policies and specialist professional wording to ensure your cover meets high-end contract requirements.

- Understand how to balance Public Liability and Professional Indemnity to protect against both physical incidents and advice-based liability.

- Discover the specific endorsements needed for high-risk scenarios, including hostile environment work and the legal carriage of firearms.

- Master the process of verifying your ‘Statement of Fact’ to guarantee that your Close Protection insurance remains valid across all operational zones.

- Gain peace of mind by partnering with a trusted advisor who understands the nuances of the security industry and simplifies complex administrative tasks.

What is Close Protection Insurance and Why is it Critical?

Many people use the terms “bodyguard” and “Close Protection Officer” interchangeably, but in the insurance market, the distinction is vital. A bodyguard might imply a generic physical presence, whereas a What is a Close Protection Officer? is a trained professional managing complex, fluid risk environments. Close Protection insurance is a calibrated suite of protections designed specifically for these high-stakes scenarios. It goes beyond basic coverage to address the unique liabilities of executive protection, from threat mitigation to physical intervention.

Standard public liability insurance often fails the modern CPO. Most general policies exclude “deliberate acts” or high-risk security activities, leaving you exposed if a routine task requires physical force. For professionals working with high-net-worth (HNW) individuals or celebrities, specialist insurance is a prerequisite for securing contracts. These clients require proof that your policy understands the nuances of their lifestyle and the specific threats they face. Without it, you aren’t just risking a claim; you’re effectively locked out of the most lucrative sectors of the industry.

SIA Compliance and Legal Requirements for 2026

Staying compliant is a moving target. As of April 1, 2026, the SIA licence fee is £204, and the regulatory requirements have become more stringent. You now must complete mandatory refresher training at every three-year renewal. To even begin this training, you’re required to hold a valid Level 3 First Aid at Work (FAW) qualification. Your Close Protection insurance must align with these standards to remain valid. Operating without adequate professional indemnity insurance can lead to severe legal repercussions, especially if a client alleges that your security advice or risk assessment was negligent. Just Quote Me ensures your policy reflects these current UK standards, keeping your career on solid legal ground.

Individual Operatives vs. Security Firms

If you’re a contractor, don’t assume an agency’s policy provides total protection. While firms often carry security insurance to cover vicarious liability, they may still pursue individual operatives for costs if personal negligence is proven. Many CPOs choose to maintain their own “top-up” or primary policies to ensure they have dedicated legal defence funds. Relying solely on a client’s or agency’s policy is a dangerous gamble that can leave you personally liable for damages. Just Quote Me provides the specialized expertise needed to identify these gaps, offering a human-centric approach to complex risks that automated platforms simply can’t match.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

The Core Components of a Comprehensive CP Policy

A robust Close Protection insurance policy acts as a multi-layered shield. It doesn’t just tick boxes for Official UK Licensing Standards; it provides a financial safety net for the diverse risks encountered in the field. A professional policy isn’t a single product but a combination of several essential covers tailored to your specific role. Understanding how these components interact is the first step toward total career security.

Public Liability: Beyond the Basics

Standard Public Liability Insurance usually covers accidental slips and trips. In the world of close protection, however, you need cover that accounts for ‘use of force’. If you’re required to physically intervene to protect a client and a third party is injured, a generic policy might deny the claim. Specialist CP wording ensures you’re protected during these high-pressure moments. This cover also extends to property damage. Imagine you’re securing a perimeter at an HNW estate and a piece of expensive equipment or bespoke furniture is damaged. The repair bills for high-end assets can easily exceed an operative’s annual earnings, making this protection indispensable.

Professional Indemnity for Security Consultants

While liability covers the physical, Professional Indemnity Insurance covers your intellectual output. Senior operatives often provide detailed threat assessments or security planning. If a client believes your advice was negligent and led to a security breach, they may seek damages for financial or reputational loss. For high-profile individuals, a breach isn’t just a safety issue; it’s a massive PR crisis. PI is the most overlooked cover for senior CPOs, yet it’s vital for anyone moving into a consultancy or management capacity where risk assessments are the primary deliverable.

Beyond these, you must consider Employers’ Liability Insurance if you hire staff or use sub-contractors on a detail. It’s a legal necessity in the UK. Finally, Personal Accident and Medical Expenses cover provides a vital safety net for you. In a role where physical risk is a daily reality, ensuring you have financial support for medical costs or loss of income is essential. Building a policy with these components ensures your Close Protection insurance is fit for purpose. You can explore our specialized security options to see how these covers fit your specific operational profile.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Navigating High-Risk and Specialized CP Scenarios

Operational environments for Close Protection Officers (CPOs) aren’t limited to the safe streets of London. As you move into Hostile Environment Close Protection (HECP) or maritime security, the risk profile changes drastically. Standard Close Protection insurance often includes strict territorial limits that stop at the UK border or exclude specific “red-listed” conflict zones. If you’re operating in high-risk regions, your policy must be explicitly extended to include repatriation and emergency evacuation clauses. This ensures you aren’t left stranded or facing ruinous medical bills if a situation deteriorates rapidly. Under the Private Security Industry Act 2001, the legal burden of care and liability is significant, making it essential that your cover follows you wherever the contract leads.

International and Hostile Zone Coverage

Working overseas requires a deep dive into your policy’s fine print. Many operatives discover too late that their cover doesn’t extend to “local labour,” such as drivers or fixers hired on the ground. If a local contractor’s action leads to a claim, your policy needs to clearly define who is covered and to what extent. You should also verify that your evacuation cover includes political risk as well as medical emergencies. Just Quote Me acts as your steady hand in these complex markets, ensuring every operational nuance is disclosed in your Statement of Fact to prevent claim denials based on geographic exclusions.

Specialist Risks: Firearms and K9 Units

Carriage of firearms is perhaps the most sensitive area of specialist cover. Most insurers won’t touch armed details without a specific “Carriage of Firearms” endorsement. This requires a rigorous disclosure of your training, the legal framework of the host country, and the specific rules of engagement. Similarly, if your detail utilizes K9 units for explosive detection or patrol, your liability extends to the actions of the animal. A handler is only as protected as their policy’s wording allows. You can find more detail on these specific endorsements through our Security Insurance page, where we break down the requirements for specialized teams.

Asset protection often goes hand-in-hand with person protection. When you’re tasked with securing high-value goods, jewelry, or sensitive data alongside a client, your insurance must reflect this dual responsibility. This is where a human-centric approach to insurance pays off. By discussing your specific contract requirements with a broker who understands the industry, you can avoid the hidden exclusions that automated systems often miss. We help you navigate these high-stakes scenarios with clarity and professional restraint, ensuring your reputation remains as protected as your clients.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

How to Choose the Right Close Protection Insurance

Selecting the right Close Protection insurance requires a tactical mindset similar to planning a security detail. You wouldn’t enter a high-risk zone without a reconnaissance report; you shouldn’t sign an insurance contract without a thorough audit of the terms. The process should be systematic, moving from a broad assessment of your needs to the fine print of your policy wording.

- Step 1: Conduct a thorough personal and operational risk assessment. This goes beyond your current contract. Consider the maximum potential loss you could face, including legal fees and compensation.

- Step 2: Verify the ‘Statement of Fact’. Ensure every risk is disclosed with absolute precision. Any undisclosed activity, such as a planned trip to a high-risk region, can void your cover entirely.

- Step 3: Compare policy exclusions as carefully as the premiums. A lower price often indicates broader exclusions, particularly regarding ‘use of force’ or specific territorial limits.

- Step 4: Check the insurer’s reputation for handling security-sector claims. A general insurer may lack the expertise to handle a complex claim involving professional negligence in a security context.

- Step 5: Review your limits of indemnity against your largest contract. High-net-worth clients often mandate specific minimum levels of cover, sometimes exceeding £5 million or £10 million.

Common Mistakes to Avoid When Quoting

Many operatives underestimate the ‘use of force’ risk in their declarations. They assume standard public liability insurance covers physical intervention, but this is rarely the case without specialist wording. Choosing ‘cheap’ over ‘comprehensive’ is another frequent error. The true cost of a rejected claim is far higher than any annual premium saving. You must also update your broker whenever your operational environment changes. A policy that covers you in London may not provide the same protection if your contract moves to a developing nation or involves higher-risk assets.

The Role of a Specialist Broker

Generic comparison sites fail the security industry because they rely on automated algorithms that don’t understand the nuances of close protection. A specialist broker provides access to exclusive Lloyds of London syndicates that specifically appetite security risks. This human-centric approach ensures your Close Protection insurance is bespoke rather than a generic template. You can secure specialist security cover that reflects your actual daily risks rather than a best-guess estimate. If you’re unsure how to align your policy with the new 2026 SIA standards, you should Request a Call back for free Expert advice to tailor your policy to your specific needs.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Secure Your Career with Just Quote Me

Securing the right Close Protection insurance shouldn’t feel like a second job. At Just Quote Me, we’ve spent over 30 years refining our approach to bespoke UK business insurance. We know that in the security sector, your reputation is your most valuable asset. That’s why we don’t rely on automated, one-size-fits-all systems. Instead, we provide a human-centric service that addresses the specific, high-risk nature of your work. Our team acts as a steady hand, navigating the complex administrative burdens so you can stay focused on protecting your clients.

The 2026 security landscape is more regulated than ever. With the SIA’s updated requirements for refresher training and first aid now in full effect, your insurance must be as current as your licence. As an FCA-authorised broker, we provide guidance that’s tailored to these shifts. We ensure your policy isn’t just a piece of paper but a tactical asset that stands up to scrutiny during contract negotiations with HNW individuals or corporate entities. We’re here to make sure your cover is as professional as the service you provide.

Why CPOs Trust Our Expertise

While we have deep roots in the West Midlands and Staffordshire, our reach is national. We understand the nuances of the regional security market but have the leverage to access a panel of top UK security underwriters. This means we can find cover for risks that other brokers often find difficult to place, such as hostile environment work or the specialized needs of maritime security. We support you through the entire lifecycle of your policy. From the initial quote to the event of a claim, we’re there to advocate for you and simplify the process, ensuring you’re never left to manage a crisis alone.

Get Started Today

You don’t have time for endless paperwork or confusing jargon. Our goal is to get you on-site quicker with a policy that actually works. We handle the heavy lifting, from verifying your operational risks to ensuring your limits of indemnity match your largest contracts. We take pride in being a knowledgeable and approachable partner in a complex market. You can explore our broader range of Business Insurance options to see how we protect various professional sectors. When you’re ready to secure your career with Close Protection insurance that offers genuine peace of mind, we make it easy to take the next step.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Secure Your Professional Reputation Today

Your role as a security professional requires constant vigilance and a proactive approach to evolving risks. We have covered how a tailored policy ensures SIA compliance for the 2026 landscape and why specialized endorsements for firearms or hostile zones are non-negotiable for high-end contracts. Don’t leave your career to the limitations of generic comparison sites that don’t understand the tactical nature of your work. Relying on standard wording can leave you exposed when your client needs you most.

Just Quote Me brings over 30 years of UK insurance expertise to your side. As an FCA-authorised and regulated broker, we provide access to a specialist security underwriting panel that understands the nuances of HNW and celebrity protection. We manage the administrative complexity so you can focus on your operational duties. It’s time to trade uncertainty for the confidence of a bespoke policy that reflects your daily reality. We are a human-centric partner in a complex market, ready to help you operate with total peace of mind.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Frequently Asked Questions

Is Close Protection insurance a legal requirement for individual CPOs?

No, it isn’t a legal requirement for individual operatives in the same way car insurance is, but it’s a professional necessity. Almost all high-net-worth clients and security agencies mandate that you carry your own liability cover before awarding a contract. Without it, you are personally liable for legal costs and damages, which can be financially ruinous even if you’re eventually found not at fault.

Does my policy cover me for work outside of the United Kingdom?

Your policy can cover international work, but it isn’t always automatic. Standard policies often limit cover to the UK or EU, so you must notify your broker if you’re heading to higher-risk regions. Operating in a hostile environment without a specific territorial extension will void your cover. We help you disclose these operational areas correctly to ensure your protection follows you across borders.

What is the difference between Public Liability and Professional Indemnity for a bodyguard?

Public Liability protects you against claims of physical injury or property damage caused during your work. Professional Indemnity, however, covers you if a client suffers a loss because of your security advice or threat assessments. While PL is essential for the physical side of being a bodyguard, PI is vital for the consultancy and planning aspects that senior operatives provide to high-profile clients.

Am I covered if I have to use physical force to protect a client?

You are covered for physical intervention only if your Close Protection insurance includes a specific “use of force” endorsement. Most general liability policies exclude deliberate acts, which can leave a security professional exposed during a crisis. Specialist policies are designed to account for necessary physical contact, provided it is lawful and falls within the scope of your professional duties and training.

How much does Close Protection insurance typically cost in 2026?

The cost of your policy depends on your specific risk profile, contract types, and required indemnity limits. Because close protection involves higher risks than standard guarding, premiums are calculated based on factors like international travel and the profile of your clients. We recommend getting a bespoke quote to ensure you’re paying for the exact level of protection your specific security detail requires.

Does insurance cover the carriage of firearms in hostile environments?

Insurance for the carriage of firearms is a highly specialized endorsement that requires full disclosure of your training and the host nation’s laws. It is not a standard feature and must be negotiated with specialist underwriters who understand armed protection details. You’ll need to demonstrate that your use of firearms is legal and follows strict rules of engagement within the specific hostile environment.

What happens if my SIA licence expires while I have an active policy?

An expired SIA licence will likely invalidate your insurance for any activities that legally require a licence to perform. Most policies include a condition that you must remain fully compliant with official licensing standards. With the 2026 mandatory refresher training rules now in place, it’s essential to stay ahead of your renewal dates to avoid any gaps in your professional protection.

Can I get short-term cover for a specific one-off contract?

Short-term Close Protection insurance is available for operatives who only work on specific, one-off contracts throughout the year. This allows you to buy cover for a set duration, such as a single month, rather than committing to an annual policy. It’s a cost-effective solution for contractors who need to meet the insurance requirements of a high-value detail without the overhead of a full year’s premium.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Article by

Just Quote Me

JustQuoteMe Ltd is an independent UK insurance brokerage specialising in business and personal insurance solutions. With over 35 years of industry experience, the company provides tailored insurance cover for businesses, landlords, tradespeople, hospitality venues, fleets, and individuals across the UK. Known for its personal service, expert advice, and competitive premiums, JustQuoteMe Ltd works with leading insurers to deliver bespoke policies designed around each client’s unique needs. The company is authorised and regulated by the Financial Conduct Authority (FCA No. 586607) and has built a reputation for trusted, straightforward insurance guidance and long-term client relationships.

by jqm | Jul 15, 2026 | Insurance

Could your standard home insurance policy be the biggest hidden risk to your business? Many hosts assume their existing cover extends to paying guests, but residential policies rarely account for the unique liabilities of the hospitality industry. Operating without specific bed and breakfast insurance leaves you exposed to expensive public liability claims and potential legal breaches that could shutter your doors. It’s a common point of confusion, but one that carries significant financial weight.

We know that running a guest house involves enough daily pressure without the added anxiety of deciphering complex policy wording. You want to focus on your guests while knowing your livelihood is secure. This guide explains how to protect your property and income with tailored cover that handles everything from guest injuries to business interruption. We also provide a clear overview of the 2026 mandatory national registration scheme and explain how a specialist broker can find the best market rates. You’ll learn how to secure full legal compliance and the peace of mind that comes with professional, expert-led protection.

Key Takeaways

- Learn why residential policies are insufficient for commercial hosting and how to avoid accidental coverage gaps that could invalidate your protection.

- Navigate your legal obligations regarding Employers’ Liability and the critical role of Public Liability in protecting your business from guest claims.

- Explore how tailored cover for buildings, contents, and business interruption secures both your physical assets and your future revenue.

- Understand the specific variables that determine the cost of your bed and breakfast insurance, from room capacity to regional risk factors.

- Discover the benefits of using an independent broker to access a broad network of top UK insurers for the most competitive and comprehensive rates.

Why Standard Home Insurance Isn’t Enough for Your B&B

Many owners treat their guest house as an extension of their private life, but your insurer sees things differently. The moment you accept payment for a room, your property transitions from a private residence to a commercial enterprise. Standard residential policies are built on the assumption of low-risk, private occupancy. They don’t account for the increased footfall, fire safety requirements, or legal liabilities that come with running a business. With the mandatory national registration scheme for short-term lets in England launching in Spring 2026, maintaining correct cover is no longer optional; it’s a requirement for your unique registration number.

If you don’t disclose your business activity, you risk a total claim rejection. Insurers call this “non-disclosure of material facts.” Whether a guest slips in the bath or a storm damages your roof, the discovery of an undeclared B&B operation gives the provider grounds to void your cover entirely. Securing bed and breakfast insurance solves this by creating a comprehensive hybrid. It protects the structural integrity of your home while providing the commercial-grade protection required for guest safety and business continuity.

The “Paying Guest” Clause Explained

In the insurance world, a “paying guest” is anyone who provides financial consideration for their stay. It doesn’t matter if you only host during the peak summer months or rent out a single spare room. Most standard policies explicitly exclude any loss or damage that occurs while the property is used for business. To stay protected, you must issue a “Change of Use” notification. Upgrading to a dedicated Hotel and Guest House insurance policy ensures your provider understands the exact nature of your risks.

Home vs. Business: Where the Lines Blur

Managing a B&B means your personal life and your professional life share the same four walls. This creates unique insurance challenges. You need to ensure your personal belongings are covered against theft or damage, while also protecting the high-value furniture and linens used by guests. Shared spaces like stairwells and dining rooms represent the highest liability risks. A robust bed and breakfast insurance policy includes Commercial General Liability (CGL) insurance to handle these overlaps. It ensures your family remains secure under the same roof while providing a professional safety net for your guests and your reputation. Just Quote Me to find a policy that effectively bridges the gap between your home and your business.

Essential Liability Covers: Protecting Guests, Staff, and Reputation

Liability is the most significant financial risk any hospitality business faces. While your property is your asset, your guests are your responsibility. In a high-traffic environment where visitors are unfamiliar with the layout, accidents happen easily. A comprehensive bed and breakfast insurance policy acts as a shield against the legal and financial fallout from these incidents.

Public Liability for B&B Owners

Public Liability is your primary defense against claims from the general public. In the context of a guest house, Public Liability provides financial protection if a visitor suffers an injury or property damage for which your business is held legally responsible. Common risks include slips on polished floorboards, trips on loose stair carpets, or accidental hot drink spills during breakfast service. We recommend a minimum limit of £2 million, though many owners opt for £5 million to ensure they are fully protected against high-value personal injury claims. Even a minor incident can lead to substantial legal fees and compensation costs that could bankrupt an uninsured business.

Employers’ Liability: Staying Legal

If you employ anyone to help run your B&B, you must have Employers Liability Insurance. This is a legal mandate in the UK, requiring a minimum cover of £5 million. This applies to full-time staff, part-time cleaners, and even seasonal help. The only common exception is for family-run businesses that aren’t incorporated as limited companies. However, if you’ve structured your guest house as a limited company, even family members count as employees in the eyes of the law. Failing to hold this cover can result in daily fines of up to £2,500. It’s often helpful to speak with a specialist broker to clarify your specific obligations under current 2026 regulations.

Beyond these core protections, you should consider Product Liability and Legal Expenses. Product Liability is vital if you serve food or provide amenities like toiletries. It covers you if a guest falls ill from a meal or suffers an allergic reaction to a provided product. Legal Expenses cover provides the funds needed to defend your business against various disputes, including contract disagreements or employment tribunals. Together, these layers of protection ensure that a single mistake or stroke of bad luck doesn’t end your hosting career. Bed and breakfast insurance isn’t just about ticking boxes; it’s about securing your reputation and your future.

Buildings, Contents, and Business Interruption: Safeguarding Your Assets

While liability covers the people, your property and its contents represent your most significant capital investment. Standard residential policies often fall short here, especially if your guest house is a listed building or features traditional construction. Specialist bed and breakfast insurance provides the specific cover needed for these unique structures, ensuring that a physical disaster doesn’t lead to a total financial collapse.

Protecting Your Property and Stock

When calculating your buildings cover, you must focus on the rebuild cost rather than the market value. Market prices fluctuate based on location and demand; the cost of labor and materials to reconstruct a stone or brick property is what matters to an insurer. This is particularly critical for those operating in specialized environments like Thatched Pub insurance contexts, where specialized craft skills and materials significantly drive up repair costs. You also need to protect your business contents, including high-value furniture, professional linens, and food stock. Be aware that many policies only cover theft if there is evidence of “forcible and violent entry.” If a guest leaves with a television or designer towels, a standard theft claim might be rejected unless you’ve secured specific extensions for guest-related losses.

The Importance of Business Interruption

Physical damage is only half the battle. If a fire or flood forces you to close for several months, the loss of bookings can be more damaging than the repair bill itself. This is where Business Interruption cover becomes essential. It replaces your lost income, ensuring you can still meet ongoing expenses like mortgages and staff wages while your doors are shut. For seasonal hospitality businesses, calculating the “Indemnity Period” is vital. You need to ensure the cover lasts long enough to see you through to the next peak booking window. Many owners underestimate how long repairs to specialist properties can take. A 12-month period might seem sufficient, but 24 or 36 months provides a much safer buffer for businesses that rely on specific peak seasons to remain profitable.

Finally, consider including cover for Guest Effects. While most visitors should carry their own travel insurance, providing a limited amount of cover for their lost or damaged items is a mark of a professional host. It helps preserve your reputation if a guest’s suitcase is damaged by a leak or accidental fire. Integrating these protections into your bed and breakfast insurance package ensures that both your physical assets and your future revenue remain secure. It’s about building a safety net that catches everything from a broken window to a season of lost revenue.

Calculating the Cost: What Influences Your B&B Insurance Premium?

Understanding the variables behind your premium helps you manage your overheads effectively. Insurers don’t just look at the size of your property; they analyze the level of exposure your business creates. A larger guest house with ten rooms naturally carries more risk than a two-room establishment, as the probability of an incident occurring increases with higher occupancy levels. Your bed and breakfast insurance rate is essentially a reflection of these combined risk factors.

Location remains a primary driver of cost. Properties situated in high-flood-risk areas or regions with higher than average crime rates will see this reflected in their quotes. However, your personal track record is equally important. A clean claims history over several years can secure a substantial No Claims Discount, significantly lowering your annual outlay. Insurers view a lack of previous claims as a primary indicator of a well-managed, low-risk business.

How to Lower Your Premium

You have direct control over several factors that influence your rate. Installing industry-standard security, such as five-lever mortice deadlocks on external doors and an approved alarm system, signals to insurers that you take asset protection seriously. Maintaining detailed health and safety records, including regular fire risk assessments and PAT testing for guest appliances, further demonstrates a proactive approach to risk management. You might also consider choosing a higher voluntary excess. By agreeing to pay a larger portion of a claim yourself, you reduce the insurer’s liability and can often secure a lower monthly or annual premium.

Factors Unique to Hospitality

The specific services you offer also shift the risk landscape. If you serve alcohol, your policy will need to reflect this, often incorporating elements similar to restaurant insurance to manage the increased liability associated with licensing. Additional activities like bike hire, boat rentals, or guided tours introduce new layers of risk that must be declared to ensure your cover remains valid.

In the modern market, even your digital reputation plays a role. Robust online reviews and a professional website suggest a well-managed operation, which some niche insurers view as a sign of lower operational risk. Because these factors vary so widely between properties, it’s vital to compare tailored insurance options that reflect your specific business model rather than relying on a generic policy. This ensures you aren’t paying for cover you don’t need while remaining fully protected for the services you do provide.

Choosing a Broker: Bespoke B&B Insurance with Just Quote Me

Selecting the right bed and breakfast insurance shouldn’t be another administrative burden on your already busy schedule. While automated comparison sites promise speed, they often lack the professional depth required to handle complex hospitality risks. Just Quote Me offers a human-led alternative. We leverage 30 years of industry experience to navigate the UK insurance market for you. Based in Stone, Staffordshire, we combine local accessibility with the authority of an established independent broker. We don’t just provide a quote; we provide a partnership that manages the complex paperwork so you can stay focused on your guests.

The Advantage of Independent Advice

A “one size fits all” approach is dangerous in the hospitality sector. Direct insurers only offer their own products, which might leave you with dangerous coverage gaps. As an independent broker, we have access to a panel of top UK insurers. This allows us to perform a competitive comparison that aggregators simply can’t match. We specialize in building bespoke Hotel and Guest House insurance packages that reflect your specific occupancy levels and service offerings. Whether you operate a traditional stone cottage or a modern boutique establishment, we ensure your policy is as unique as your business. If the worst happens and you need to make a claim, we act as your advocate, handling the negotiations to ensure a fair and efficient resolution.

Get Started with Just Quote Me

Our process is straightforward and designed for efficiency. We’ve stripped away the jargon to provide a frictionless experience from your first inquiry to the final policy documents. Every B&B has a different risk profile, and we take the time to understand yours through expert call backs and tailored assessments. This personalized service ensures you only pay for the specific cover your business requires, avoiding the wasted costs of irrelevant “bundle” products. We pride ourselves on being a steady hand in a complex market, offering the reliability you need to host with confidence.

Secure Your Hospitality Future Today

Running a successful guest house requires more than just excellent hospitality; it demands a solid foundation of legal and financial security. You’ve seen how standard residential policies fail to cover the unique risks of paying guests and how specialist liability and business interruption covers keep your doors open during unforeseen events. Maintaining the right bed and breakfast insurance is the most effective way to protect your livelihood and reputation in an increasingly regulated market.

As an FCA Authorised Broker with 30+ years of industry experience, Just Quote Me provides the expertise you need to navigate this complex landscape. We offer access to top UK insurers to ensure you receive a bespoke policy at a competitive rate. We manage the administrative details so you can focus on providing an exceptional guest experience. Take the first step toward comprehensive protection and long-term peace of mind by partnering with a specialist broker who understands your industry.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Frequently Asked Questions

Do I need specific insurance for a B&B if I only have one guest room?

Yes, you require specialist cover even if you only rent out a single room on an occasional basis. Most residential home policies explicitly exclude business activities and paying guests, which means any claim could be rejected if your insurer discovers you are operating a hospitality business. Securing dedicated bed and breakfast insurance ensures you are protected against the unique liabilities that arise the moment you accept payment for a stay.

Is public liability insurance a legal requirement for B&Bs in the UK?

Public liability insurance is not a statutory legal requirement in the UK, but it is considered essential for any hospitality business. Most mortgage lenders and local authorities will insist on a minimum level of cover before you can legally operate or be included in local tourism directories. Without it, you are personally liable for legal fees and compensation if a guest is injured or their property is damaged while staying at your premises.

Does B&B insurance cover my own personal contents?

Yes, a tailored policy acts as a hybrid to cover both your professional equipment and your personal belongings. While standard commercial policies focus solely on business assets, a guest house policy is designed for live-in owners. It ensures that your private furniture, clothes, and electronics are protected alongside the linens and furniture used by your guests, providing comprehensive cover for your entire home under one single policy.

Can I get insurance for a guest house with a thatched roof?

You can certainly get insurance for a thatched guest house, though it requires a specialist approach due to the higher fire risk associated with the construction material. Standard insurers often avoid thatched properties, so using a broker with experience in non-standard buildings is vital. We can help you find a provider that understands the maintenance requirements and safety protocols necessary to secure robust cover for your heritage building.

What happens if a guest sues me for food poisoning?

Your policy’s Product Liability section will handle the legal defense and any resulting compensation if a guest sues for food poisoning. This protection is critical for any host serving breakfast or providing snacks. The insurer will investigate the claim and manage the costs of defending your business, ensuring that a single hygiene dispute or allergic reaction doesn’t lead to a devastating financial loss for your establishment.

How much does B&B insurance typically cost in 2026?

The cost of your premium depends on several variables including your location, the number of guest rooms, and your claims history. In 2026, factors such as updated fire safety regulations and the new national registration scheme also influence how insurers calculate risk. Because every establishment is unique, the most accurate way to determine your cost is to request a tailored quote that reflects your specific operational risks and occupancy levels.

Does my policy cover damage caused by guests?

Most bed and breakfast insurance policies include cover for accidental damage caused by guests, such as spills on carpets or broken fixtures. However, malicious damage or theft by guests often requires a specific extension and may only be covered if there is evidence of a police report. It’s important to check your policy wording to understand the exact level of protection provided for guest-related incidents and any applicable excesses.

What is the difference between guest house and hotel insurance?

The primary difference lies in the scale of the operation and the level of service provided. Guest house insurance is typically designed for smaller, owner-managed properties where the host often lives on-site. Hotel insurance accounts for larger staff numbers, complex facilities like spas or gyms, and higher guest turnover. Both provide similar core protections, but the specific limits and additional covers are scaled to match the complexity and size of the business.

Article by

Just Quote Me

JustQuoteMe Ltd is an independent UK insurance brokerage specialising in business and personal insurance solutions. With over 35 years of industry experience, the company provides tailored insurance cover for businesses, landlords, tradespeople, hospitality venues, fleets, and individuals across the UK. Known for its personal service, expert advice, and competitive premiums, JustQuoteMe Ltd works with leading insurers to deliver bespoke policies designed around each client’s unique needs. The company is authorised and regulated by the Financial Conduct Authority (FCA No. 586607) and has built a reputation for trusted, straightforward insurance guidance and long-term client relationships.

by jqm | Jul 14, 2026 | Insurance

Did you know that one major UK insurer paid out £57 million in claims across the hospitality sector in 2025? As a hotelier in 2026, you’re likely feeling the weight of new regulatory demands, from the impending requirements of Martyn’s Law to the expanded scope of the Package Travel Regulations. Securing reliable hotel insurance shouldn’t feel like a gamble against the fine print, yet rising premiums and complex hospitality risks make it harder than ever to find a policy that actually fits.

We understand that you’d rather focus on guest experience than deciphering insurance jargon or navigating the 2026 business rate revaluations. You deserve a partner who simplifies these administrative burdens while ensuring your coverage is airtight. This article will show you how to secure bespoke hotel and guest house insurance that protects your business, guests, and reputation in 2026. We’ll break down the essential covers you need to meet new legal duties, explain how to manage modern liability risks, and show you how a human-centric approach to risk management can deliver competitive pricing through specialized broker panels.

Key Takeaways

- Learn how upcoming 2026 legislation, including Martyn’s Law and updated employment rights, directly impacts your hotel’s legal obligations and risk profile.

- Identify the core components of a robust Hotel insurance policy, focusing on Public Liability and the legal requirement for Employers’ Liability cover.

- Discover how to safeguard your revenue through specialist extensions like Business Interruption and Loss of Licence cover to protect against unforeseen closures.

- Understand the critical dangers of underinsurance in a high-inflation environment and how regular building valuations keep your assets fully protected.

- Explore the advantage of working with an independent broker to access a broad panel of UK underwriters for bespoke, competitive hospitality solutions.

Understanding Hotel and Guest House Insurance in 2026

Modern hotel insurance is far more than a simple building and contents policy. It’s a sophisticated, multi-class risk management strategy designed specifically for the unique pressures of the hospitality sector. In 2026, the industry faces a perfect storm of regulatory changes and rising operational costs. A generic business policy simply won’t cut it. Your coverage needs to account for everything from guest safety and employee welfare to the physical security of your premises.

Legislation like the Terrorism (Protection of Premises) Act 2025, often called Martyn’s Law, is now a critical factor in risk assessment. This requires venues to take active steps to mitigate attack risks, with standard tier requirements already affecting hotels with a capacity over 200. Additionally, Public liability remains the bedrock of any hospitality policy, protecting you against claims for injury or property damage. Just Quote Me leverages 30 years of experience to simplify these administrative burdens. We act as a steady hand, ensuring your policy reflects the specific nuances of your operation without the headache of automated call centres.

Who Needs Specialist Hospitality Cover?

The hospitality world is diverse. A 50-room city centre hotel has vastly different needs than a family-run bed and breakfast in Stone or Stafford. We provide bespoke hotel and guest house insurance for a wide range of providers, including:

- Boutique Accommodations: High-value interiors and curated experiences require specialized asset protection, especially for venues catering to elite guests who rely on Private Jet Charter for their travel needs.

- Pubs with Rooms: These businesses face double the risk, combining liquor liability with guest accommodation needs.

- Traditional Guest Houses: Family-run businesses need simple, efficient cover that protects their home and their livelihood simultaneously.

The Role of an Independent Broker

Buying direct might seem faster, but it often leaves gaps in your protection. Direct insurers use standardized models that can’t account for the complexity of 2026’s hospitality risks. For example, new employment laws making Statutory Sick Pay a day-one right from April 2026 require a review of your financial resilience. We offer a human-centric alternative to automated systems. As an independent, FCA-authorised broker, we navigate the market for you. We provide regional expertise across Staffordshire and the UK, ensuring you get expert advice that a generic website simply cannot offer.

Essential Coverage: Protecting Your Guests, Staff, and Assets

Protecting your business requires a multi-layered approach that addresses three distinct areas: the people who visit, the people who work there, and the physical structure itself. A comprehensive Hotel insurance policy acts as the glue holding these protections together, ensuring that a single incident doesn’t lead to financial ruin. In an era of rising operational costs and increased guest expectations, having the right levels of cover is a pragmatic necessity rather than a luxury.

Public Liability is your first line of defence. Specifically, Public Liability is the protection against claims of negligence or injury by guests. Whether it’s a slip on a wet floor or a more complex accident in a hotel gym, the financial repercussions of a claim can be immense. Integrating robust public liability insurance into your wider business strategy ensures you can handle these challenges professionally without draining your cash reserves.

Next, you must consider your team. It’s a legal requirement for employers’ liability insurance to be in place for any UK business with staff. With the 2026 changes to employment laws, including Statutory Sick Pay becoming a day-one right, the relationship between employers and insurers is more important than ever. You need a policy that reflects these new legal realities, protecting you from claims related to workplace injuries or illnesses while you manage a shifting regulatory landscape.

Finally, we address property damage. Your building, contents, and stock represent a significant capital investment. Whether you’re managing a modern complex or a listed building in Stone, your commercial property insurance must be precise. This includes safeguarding high-value items like professional kitchen equipment and wine stock against fire, flood, or theft. If you’re unsure about your current levels of protection, you can explore our bespoke hospitality solutions to see how we tailor these covers to your specific premises.

Liability Protection for Guest Interactions

Hospitality thrives on interaction, but every touchpoint carries a potential risk. Bars and restaurants are high-traffic areas where slips and trips are common. Even with rigorous hygiene standards, claims of food poisoning can occur and escalate quickly. A specialist Hotel insurance policy provides the legal support and financial backing to manage these claims efficiently. This allows you to focus on maintaining your reputation and guest service rather than getting bogged down in legal paperwork.

To further enhance guest confidence and support your security protocols, you can visit Imagin Products Ltd for professional staff name badges and identification solutions.

Safeguarding Your Physical Hotel Assets

Fire and flood remain the most significant threats to your physical assets. In 2026, the cost of materials and labour for repairs has risen, making accurate valuations more critical than ever. Your cover should extend beyond the bricks and mortar to include specialized equipment and high-value stock. For many hoteliers in Newcastle-under-Lyme and across the UK, the wine cellar or the professional kitchen represents a huge portion of their capital. Generic business policies often have restrictive limits on these items, leaving you vulnerable to significant losses.

Specialist Extensions for Modern Hospitality Risks

Core protections like property and liability cover provide the foundation for your business. However, modern hospitality operations in 2026 face nuanced threats that standard policies often overlook. These gaps are filled by specialist extensions, which transform a basic Hotel insurance policy into a comprehensive safety net. Whether it’s a digital breach or a sudden loss of trading rights, these additions ensure your business remains resilient against the unexpected.

For hotels with on-site catering or fine dining, Deterioration of Stock is a pragmatic necessity. A simple freezer failure or a prolonged power cut can result in thousands of pounds of wasted premium produce. This cover ensures that mechanical breakdowns don’t eat into your profit margins, providing a straightforward solution for businesses that pride themselves on their culinary offerings. We focus on these practical details so you can manage your kitchen with confidence.

Business Continuity and Revenue Protection

If a fire or flood forces you to close your doors, property cover pays for the repairs. It doesn’t, however, replace the lost income needed to pay your staff or cover your mortgage. Business Interruption (BI) cover is essential for maintaining cash flow during these periods. You must carefully calculate your indemnity period. In 2026, supply chain delays mean that rebuilding or refitting a hotel can take significantly longer than expected. Many hoteliers now opt for 24 or 36-month periods to ensure they aren’t left without support before they’re ready to trade again.

For properties with a strong focus on pub and bar insurance interests, Loss of Licence cover is equally vital. If your alcohol permit is revoked through no fault of your own, the resulting drop in revenue can be catastrophic. This extension provides financial protection to offset the loss in business value or income while you work to resolve the issue.

Digital Risks and Cyber Security

The hospitality industry’s reliance on digital booking systems makes it a prime target for cybercriminals. Every hotel, regardless of size, needs cyber insurance in 2026 to manage the fallout of a data breach. If guest lists or payment details are compromised, you face more than just a PR disaster. You face significant costs related to forensic investigations, legal fees, and potential GDPR fines. Ransomware attacks can also freeze your booking systems, making it impossible to check guests in or out. Having a specialist digital extension ensures you have expert support to recover your data and resume operations quickly.

How to Avoid Common Pitfalls: Underinsurance and Risk

In the current economic climate, underinsurance is one of the most significant threats to UK hoteliers. With the 2026 revaluation of business rates and the continued rise in construction costs, many businesses are operating with outdated valuations. If your Hotel insurance policy is based on figures from even two years ago, you’re likely exposed. Ensuring your coverage reflects today’s reality is a pragmatic step that protects your business from devastating financial shortfalls during a claim.

Risk management is the other side of the coin. It isn’t just about ticking boxes for compliance; it’s a strategic tool to lower your premiums and improve your operational resilience. By identifying hazards before they result in an incident, you position your hotel as a preferred risk for top UK underwriters. This proactive approach is essential for navigating the rising insurance costs seen across the hospitality sector in 2026.

The Reality of Underinsurance

A common mistake is confusing market value with reinstatement cost. Market value is what your property would sell for on the open market. Reinstatement cost is what it would actually cost to rebuild the structure from scratch, including debris removal, architect fees, and modern planning requirements. If your building is insured for less than its true rebuild value, insurers may apply the “Average Clause.” This means that if you’ve only covered 80% of the value, the insurer may only pay 80% of any claim, regardless of its size. You should Request a Call back for free Expert advice to review your current limits and ensure your business is fully protected.

Proactive Risk Management

Lowering your overheads starts with a robust health and safety strategy. Regular audits of guest-facing areas, especially high-risk zones like kitchens or leisure facilities, demonstrate a commitment to safety that insurers value. Fire safety compliance is particularly critical in 2026. With stricter enforcement and higher penalties, an outdated fire risk assessment doesn’t just put lives at risk; it could potentially invalidate your policy. We recommend conducting annual reviews of all safety protocols to ensure they meet the latest standards.

For businesses in Stone, Stafford, or Newcastle-under-Lyme, local factors play a significant role in your risk profile. Historic properties, which are common in our region, often feature non-standard construction materials that carry unique risks. Working with a Staffordshire broker allows you to identify these hidden regional risks before they lead to a rejected claim. You can explore our tailored hospitality packages to see how we combine regional expertise with access to a broad panel of insurers to keep your business secure.

The Broker Advantage: Why Choose Just Quote Me?

Independence is a significant asset in the hospitality sector. Many hoteliers find themselves restricted by a single insurer’s appetite when buying direct, which often leads to standardized policies that don’t account for unique operational risks. We provide a human-centric alternative. As an independent, FCA-authorised broker, we work for you rather than the insurance company. This allows us to compare multiple options from a broad panel of top UK underwriters to secure the most competitive Hotel insurance for your specific requirements.

Experience matters when managing hospitality risks. We’ve spent over 30 years refining our approach, acting as a steady hand for businesses navigating the complexities of the 2026 insurance market. By managing the heavy administrative burden of renewals and compliance, we allow you to focus on your guests. We don’t just provide a policy; we offer a partnership grounded in reliability and straightforward advice.

Bespoke Solutions for Every Hospitality Niche

Independent guest houses face vastly different pressures than large commercial hotels. We specialize in tailoring hotel and guest house insurance to fit your specific niche. This includes ensuring your employers liability insurance is aligned with the latest legal standards, protecting your team and your business simultaneously. Our expertise also covers specialized sectors, such as nightclub insurance or properties with non-standard features like thatched roofs. This level of customization ensures you don’t pay for generic cover that fails to address your actual vulnerabilities.