by jqm | Jun 23, 2026 | Insurance

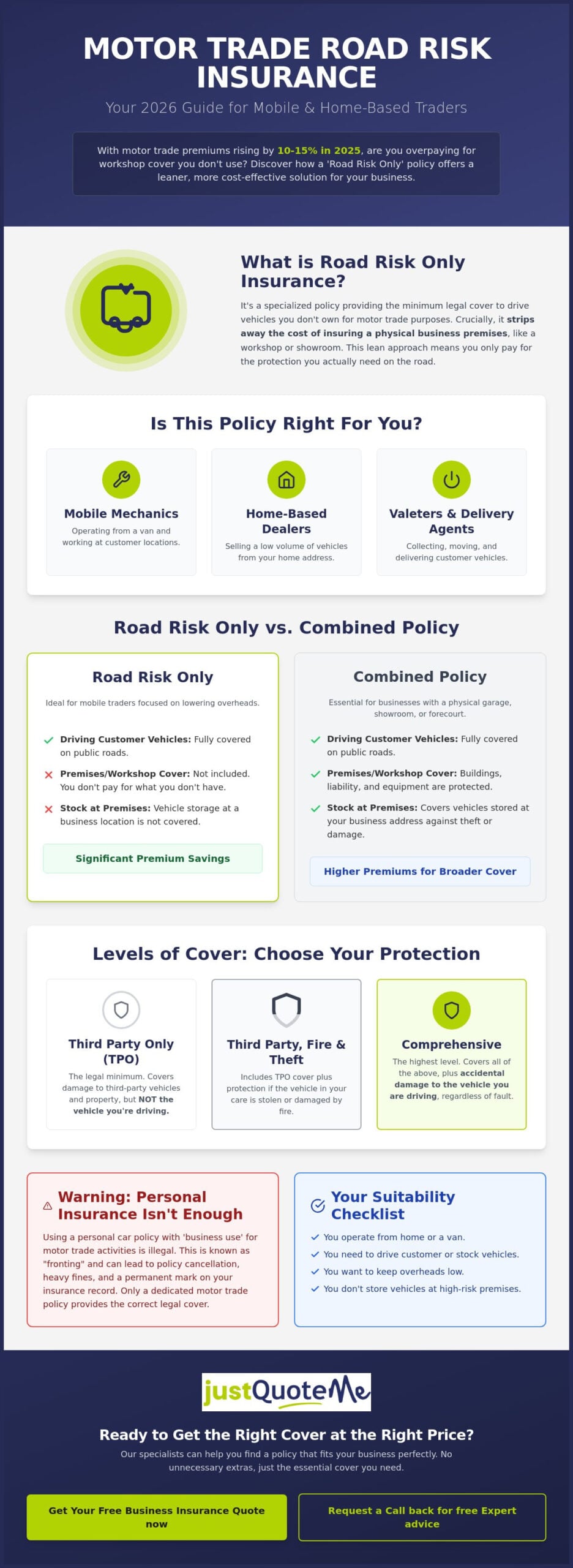

Why are you paying for a brick-and-mortar workshop policy when your entire business operates from a driveway or a mobile van? It’s a common frustration for mobile mechanics and home-based car dealers who find themselves subsidizing the costs of large garages they don’t own. If you’re looking to cut costs, focusing on motor trade road risk insurance only is the most efficient way to stay legal on UK roads while protecting customer vehicles in transit. You shouldn’t have to struggle through a complex market just to find a policy that fits your actual working day.

We understand that the 10-15% premium increases seen in 2025 have made budgeting a challenge for independent traders in 2026. This guide promises to simplify the process, helping you secure the essential protection you need at a price that reflects your specific trade. We will preview the latest MID update grace periods, explain how to manage the removal of the fuel duty freeze in September 2026, and show you how to maintain compliance without the burden of unnecessary premises cover. It’s time to get your business moving with a policy that works as hard as you do.

Key Takeaways

- Learn how to eliminate the overhead of physical premises insurance by choosing a policy tailored specifically for mobile and home-based operations.

- Identify the differences between Third Party Only and Comprehensive protection to ensure customer vehicles are fully covered during transit.

- Discover why motor trade road risk insurance only offers significant premium savings compared to combined policies while meeting all legal requirements.

- Master the essential requirements for the Motor Insurance Database (MID) to avoid penalties and ensure your business remains compliant on UK roads.

- Find out how working with a specialist broker provides access to a wider network of industry underwriters than standard comparison sites.

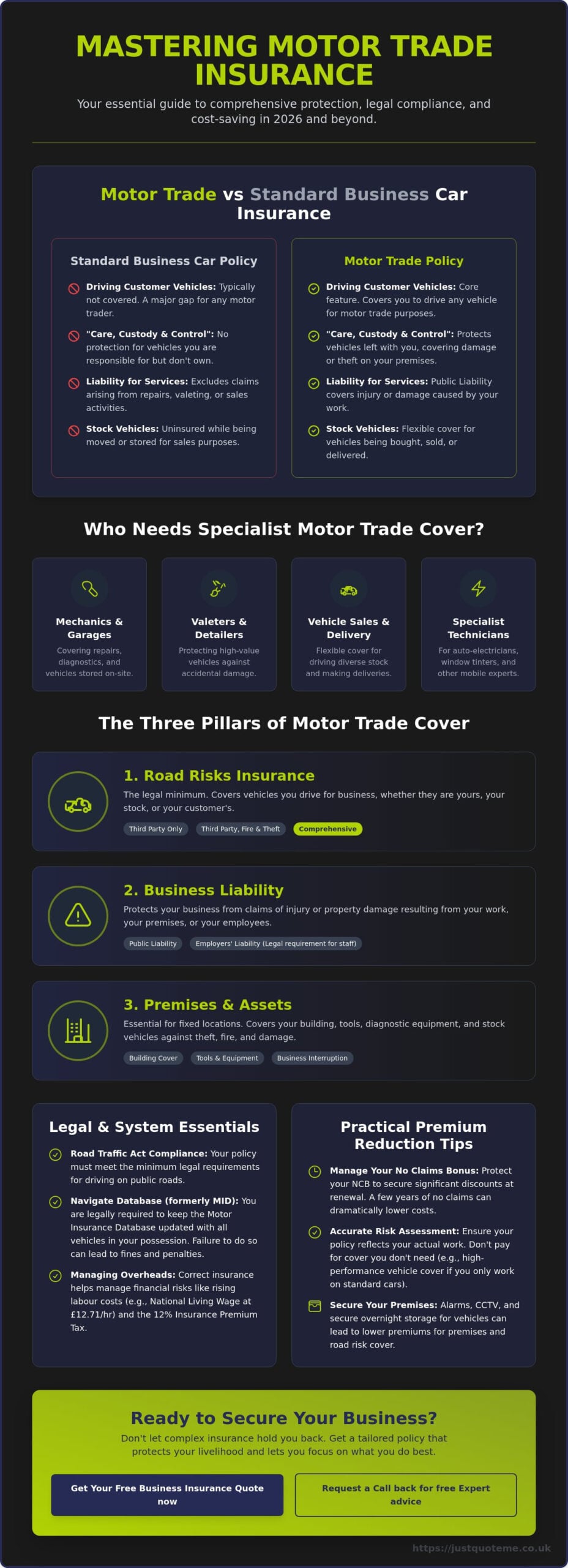

What is Motor Trade Road Risk Insurance Only?

Motor trade road risk insurance only is a specialized policy designed for professionals who move vehicles as part of their daily business activities but lack a dedicated commercial premises. It provides the legal framework required to drive cars, vans, or motorcycles that you don’t personally own. Unlike a combined policy, which includes cover for a physical workshop or showroom, this option focuses purely on the risks associated with being on the road. It’s a pragmatic solution for those who prioritize efficiency and lower overheads.

The “only” part of the name is critical. It signifies a lean approach to business protection. It’s built for the mobile mechanic working from a van or the part-time dealer selling vehicles from a home driveway. By stripping away the costs of building insurance and stock-in-trade cover for a fixed location, you ensure that your business expenses remain manageable. Following the 10-15% increase in motor trade premiums during 2025, many traders are switching to motor trade road risk insurance only to maintain their margins in 2026.

This type of cover is the backbone for various sectors. Mobile valeters, delivery drivers, and vehicle collection agents all rely on it to operate legally. Understanding vehicle insurance basics is helpful, but trade policies operate on a different level of liability. They allow you to handle customer assets with the confidence that you’re meeting UK road requirements without paying for a garage you don’t use.

The Road Risk Only Suitability Checklist

Determining if this policy fits your business model is straightforward. If you answer yes to these points, a road risk policy is likely your best option:

- Do you operate your business from a home address or a mobile van?

- Do you need to drive customer vehicles or stock on public highways?

- Are you looking to keep overheads low by excluding buildings and stock-in-trade cover?

- Do you handle a low volume of vehicles that don’t require high-security premises storage?

Why Personal Insurance Isn’t Enough

It’s a common mistake to assume a personal car policy with “business use” is sufficient. Standard domestic policies are designed for social, domestic, and commuting purposes. They specifically exclude any activity related to the motor trade. This means you aren’t covered the moment you pick up a customer’s car for a service or transport a vehicle you intend to sell. Attempting to use a personal policy for these tasks is often viewed as “fronting,” which can lead to cancelled insurance, heavy fines, and a permanent mark on your record. A dedicated trade policy allows you to drive any vehicle for business purposes, ensuring you stay on the right side of the law.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Levels of Cover: Choosing the Right Protection for 2026

Selecting the right level of protection is a balancing act between cost management and risk mitigation. While the primary goal of motor trade road risk insurance only is to keep your business lean, choosing the wrong tier can leave you financially exposed. In 2026, with the cost of parts and labor continuing to rise, the level of cover you select determines how much of a loss your business can absorb. There are three standard tiers available to traders.

Third Party Only (TPO) is the legal floor. It covers damage or injury to others but offers zero protection for the vehicle you are driving. This is often the starting point for those looking to meet official trade licence requirements without spending more than necessary. Third Party, Fire and Theft (TPFT) adds a layer of security, protecting you if a vehicle in your care is stolen or damaged by fire. However, for most active traders, Comprehensive cover is the standard. It protects the vehicles you drive against accidental damage, which is vital when handling expensive customer assets.

You must also pay close attention to indemnity limits. This is the maximum amount an insurer will pay for any single vehicle. If you routinely move high-end electric vehicles, which often exceed the £50,000 Luxury Car Tax threshold, a standard £20,000 limit won’t be enough. You can explore these options further when you compare motor trade insurance with an expert who understands these nuances.

Third Party Only (TPO) vs. Comprehensive

TPO might seem sufficient for low-value vehicle delivery or scrap collectors, but it’s rarely enough for service-based trades. If a mobile mechanic or valeter clips a wall while moving a customer’s car, a TPO policy leaves them footing the entire repair bill. Comprehensive motor trade road risk insurance only ensures that accidental damage is covered. While the premium is higher, the cost-to-benefit ratio usually favors Comprehensive cover because it prevents a single mistake from bankrupting a small business.

Optional Extensions for Road Risk Policies

A basic road risk policy covers the driving, but your business likely involves more than just being behind the wheel. Mobile workers should consider adding public liability insurance to protect against claims of injury or property damage at a customer’s site. You can also include tool and equipment cover to protect the specialized gear kept in your van. For home-based dealers, demonstration cover is a vital addition, allowing potential buyers to test drive vehicles under your insurance framework.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Road Risk Only vs. Combined Insurance: Which Saves You More?

Choosing between a road risk only policy and a combined motor trade policy is primarily a question of overhead management. For many small businesses, the cost of premises insurance is the single largest administrative burden. By opting for motor trade road risk insurance only, you’re essentially stripping your policy back to its functional core: the ability to drive vehicles legally. This lean approach is particularly effective in 2026, as traders look for ways to offset the 10-15% premium increases seen over the last year. It allows you to pay for the protection you use on the road without subsidizing the high fire and theft risks associated with a physical garage or showroom.

The risk profile for a mobile trader is fundamentally different from that of a fixed-site business. Insurers often view mobile professionals as a lower risk for large-scale theft because they don’t have a single location where dozens of high-value vehicles are gathered. Reading through a commercial vehicle insurance guide can help you understand these liability differences, but the practical result is a lower premium for those who don’t need a combined policy. Consider a mobile valeter compared to a fixed-site car wash. The valeter only needs to cover the vehicle while it’s being moved or worked on at a customer’s home. The car wash owner, however, must insure the building, the specialized machinery, and the high volume of cars parked on-site at any one time.

When “Road Risk Only” is the Correct Choice

This policy is the tactical choice for traders whose business doesn’t rely on a commercial lot. If you’re a home-based trader using your own driveway for a small amount of stock, a road risk policy provides the legal cover you need for test drives and collection. Mobile mechanics who carry out repairs at a customer’s location also benefit, as their primary risk is the transit of the vehicle rather than the storage of it. It’s also the ideal solution for part-time traders who balance car sales with a 9-5 job, providing a professional safety net without the corporate price tag.

Transitioning to a Combined Policy

There comes a point where a business might outgrow a road risk policy. If you start holding more than five or six high-value vehicles at a single location, the risk of a single fire or theft event could be devastating. Road risk policies generally don’t cover vehicles when they’re parked at your business premises; they’re designed for transit. If you’ve recently moved into a dedicated unit or workshop, it’s time to talk to us about a combined policy. We help you bridge this gap during your expansion, ensuring your growing stock is protected while keeping your transition costs as low as possible.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Eligibility and Managing Your Policy via the MID

Securing motor trade road risk insurance only requires meeting specific criteria that underwriters use to assess risk. Most providers look for drivers aged 25 or over, though some specialist schemes exist for younger traders with significant experience. You’ll typically need to have held a full UK driving license for at least one year. It’s also vital to understand that certain risks are often excluded from standard motor trade road risk insurance only policies. This includes the handling of hazardous goods or operating in postcodes with exceptionally high theft rates. If your business involves high-performance sports cars, you must ensure your indemnity limits reflect their value, especially with the Luxury Car Tax threshold for zero-emission vehicles rising to £50,000 as of April 1, 2026.

The Motor Insurance Database (MID) is the most critical administrative tool for any motor trader. It is a central record used by the police and the DVLA to identify uninsured vehicles. As a trader, it’s your legal responsibility to keep this database updated with every vehicle in your possession, including stock and customer cars you’re driving under your policy. Failing to manage this effectively can lead to immediate police interest and avoidable fines.

The MID: Your Legal Obligation

While there is technically a grace period of up to 14 days to add a newly acquired vehicle to the MID, as confirmed in May 2026, we strongly recommend doing it immediately. If you’re stopped by the police and the vehicle isn’t on the database, you face the risk of vehicle seizure. In 2026, the integration between the MID and roadside cameras is faster than ever. Updating your list takes only a few minutes through your insurer’s portal, providing instant peace of mind and keeping your business compliant.

Factors That Affect Your Road Risk Premium

Your premium isn’t just based on your trade; it’s influenced by your personal and professional profile. Your location plays a major role, specifically where vehicles are kept overnight. Even without premises insurance, insurers want to know if stock is on a secure driveway or parked on a public road. Your driver history, including any penalty points or previous claims, will also shift the cost. Finally, your estimated annual turnover and the number of vehicles you handle help insurers gauge the level of activity. If you’re unsure how these factors apply to you, talk to our specialist team for a clear breakdown.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Securing Your Motor Trade Quote with Just Quote Me

Just Quote Me brings 30 years of experience to the UK insurance market, providing a steady hand for traders in an increasingly complex sector. We understand that finding motor trade road risk insurance only isn’t always straightforward on generic comparison sites. Those platforms often use rigid algorithms that struggle with the nuances of part-time trading or mobile services. This often leads to inflated premiums or, worse, inadequate protection that leaves you vulnerable. As an independent broker, we have direct access to a broad network of specialist UK motor trade underwriters. This allows us to negotiate on your behalf, ensuring your policy reflects the actual risks of your business without forcing you to pay for unnecessary extras.

Our approach is grounded in bespoke advice. We don’t believe in one-size-fits-all solutions. Instead, we look at your specific vehicle throughput and trade type to find the most efficient path to coverage. By stripping away the administrative burdens, we help you maintain your margins in a year where external costs like fuel duty and parts inflation are putting pressure on the bottom line. You get the authority of an industry expert with the accessibility of a partner who genuinely cares about your business success.

Why Staffordshire Traders Trust Just Quote Me

While we serve professionals across the country, our local expertise in Stone, Stafford, and the wider West Midlands gives us a unique perspective. We pride ourselves on a personalized service that prioritizes human interaction over automated chatbots. When you contact us, you’ll speak directly to an expert who understands the local trade environment and the specific challenges you face. Our commitment to efficiency means we work quickly to get you covered and on the road. We know that in the motor trade, time is money, and we aim to make your insurance experience as frictionless as possible.

Next Steps for Your Trade Protection

Securing your trade protection is a simple process when you have the right details ready. You’ll need to provide your driving licence, evidence of your trade activities, and the maximum value of the vehicles you expect to handle. We use this information to find the most competitive motor trade road risk insurance only rates available. Our team ensures your indemnity limits are accurate, protecting you against the rising costs of vehicle repairs seen throughout 2026. Taking action now ensures your business remains legal, professional, and protected against the unexpected.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Protect Your Trade and Drive Your Business Forward

Choosing motor trade road risk insurance only is a tactical decision that aligns your overheads with your actual business model. By focusing on essential road protection and diligent MID management, you ensure your mobile or home-based operation remains both legal and lean throughout 2026. You’ve seen how stripping away premises cover can safeguard your margins while still providing the comprehensive protection required for customer vehicles in transit. It’s about paying for the cover you use, not the buildings you don’t own.

With 30+ years of industry experience, Just Quote Me stands as an FCA-authorised independent broker dedicated to simplifying your administrative burdens. We provide direct access to top-tier UK underwriters, ensuring you receive a policy that fits your professional needs without the corporate bloat. You don’t have to manage these complexities alone; we’re here to provide the steady hand and expert advice your business deserves. Partner with an expert today and stay focused on what you do best. Your business has the potential to thrive, and the right insurance partner makes that journey much smoother.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Frequently Asked Questions

Is road risk insurance a legal requirement for motor traders?

Yes, road risk insurance is the minimum legal requirement for any individual or business driving vehicles they don’t personally own on public roads. If you move customer cars or drive stock for your trade, you must have this cover to comply with the Road Traffic Act. Operating without it can lead to heavy fines, the seizure of vehicles, and a permanent mark on your commercial insurance record.

Can I get motor trade road risk insurance for a part-time business?

You can certainly secure a policy for a part-time venture as long as you can prove you are running a legitimate business for profit. Many insurers offer specialist schemes for those who sell cars or offer mobile repairs alongside another job. It is an excellent way to maintain professional standards and legal compliance without the high overheads associated with a full-time commercial garage or showroom.

Does road risk only insurance cover my own personal vehicles?

Most policies allow you to include your own personal vehicles, provided they are declared to your insurer and added to the Motor Insurance Database. This allows you to manage all your driving under one professional policy, often simplifying your administration. You must ensure that the policy includes “Social, Domestic and Pleasure” use for these specific vehicles, as trade-only cover may restrict your personal use during evenings and weekends.

What is the average cost of motor trade road risk insurance only in 2026?

The cost of your policy depends on several factors, including your location, driving history, and the types of vehicles you handle. While we don’t provide fixed pricing, the industry has seen premium increases of 10-15% recently due to the rising costs of parts and labor. Opting for motor trade road risk insurance only remains the most cost-effective choice for mobile traders because it excludes the expensive premiums required for physical business premises.

Can I add public liability to a road risk only policy?

Yes, adding public liability is a standard and highly recommended extension for most road risk policies. It protects your business if you accidentally cause injury to a member of the public or damage their property while you are working. For mobile mechanics or valeters working on a customer’s driveway, this extra layer of protection is vital for covering risks that occur when you aren’t actually behind the wheel.

Does comprehensive road risk insurance cover the tools in my van?

A standard comprehensive policy covers damage to the vehicle you are driving but does not usually include the tools or equipment kept inside. If you are a mobile professional, you will need to add a specific tools and equipment extension to protect your gear against theft or damage. This ensures that your specialized diagnostic tools or valeting equipment are financially protected while you are traveling between different jobs.

What happens if I forget to update a vehicle on the MID?

Failing to update the Motor Insurance Database can result in your vehicle being flagged by police roadside cameras, leading to immediate stops and potential seizure. While a 14-day grace period exists for some acquisitions, it’s safer to update the database the moment you take possession of a vehicle. Keeping your motor trade road risk insurance only records current is the most effective way to avoid unnecessary fines and police interest during your working day.

Can I get road risk insurance if I am under 25?

Securing cover for traders under 25 is possible, though it often requires a specialist underwriter and may carry stricter terms or higher excesses. Most standard insurers prefer drivers with at least one year of experience and a clean license. If you are a younger trader, working with an independent broker is the best way to find a provider that understands your specific trade and is willing to offer a competitive quote.

Article by

Just Quote Me

JustQuoteMe Ltd is an independent UK insurance brokerage specialising in business and personal insurance solutions. With over 35 years of industry experience, the company provides tailored insurance cover for businesses, landlords, tradespeople, hospitality venues, fleets, and individuals across the UK. Known for its personal service, expert advice, and competitive premiums, JustQuoteMe Ltd works with leading insurers to deliver bespoke policies designed around each client’s unique needs. The company is authorised and regulated by the Financial Conduct Authority (FCA No. 586607) and has built a reputation for trusted, straightforward insurance guidance and long-term client relationships.

by jqm | Jun 22, 2026 | Insurance

The UK commercial motor insurance market is estimated to reach a value of USD 32.29 billion in 2026, yet many operators still struggle to find a single insurer willing to cover a fleet of fewer than five vehicles. If you manage a handful of trucks, securing hgv fleet insurance for small business often feels like a constant battle against complex jargon and rising premiums driven by Ogden Rate changes. You need a solution that recognizes your specific operational needs rather than forcing your business into a corporate sized box that doesn’t fit.

It’s frustrating when administrative burdens pile up alongside rising repair costs, which have increased by more than 20% since 2021. We understand that your priority is keeping your drivers on the road safely and legally, especially with new mandates like the Smart Tachograph Version 2 taking effect for international transport in July 2026. This guide promises to simplify the process of protecting your heavy vehicle fleet with expert broker advice and tailored cost saving strategies. We’ll explore how to consolidate your policies into a single renewal date, manage driver age restrictions, and navigate the latest safety regulations to keep your premiums manageable and your business moving.

Key Takeaways

- Learn how to consolidate 2 to 5 vehicles into a single renewal date to significantly reduce your administrative burden.

- Understand the tactical differences between Any Driver and Named Driver policies to balance operational flexibility with premium costs.

- Discover how an independent broker secures hgv fleet insurance for small business by accessing specialist markets that automated portals often miss.

- Identify high-impact strategies to lower premiums, including the use of telematics and task-specific driver training programmes.

- Navigate the latest 2026 regulatory updates with expert guidance to ensure your small fleet remains fully compliant and cost-effective.

What is HGV Fleet Insurance for Small Businesses?

HGV fleet insurance for small business is a unified policy designed to cover multiple heavy goods vehicles under a single agreement. In the UK, any vehicle with a gross weight exceeding 3.5 tonnes is classified as an HGV. While large haulage firms might manage hundreds of units, small businesses often operate in the “sweet spot” of 2 to 5 vehicles. Consolidating these into one policy eliminates the stress of managing separate renewal dates and multiple sets of paperwork. It’s an efficient way to gain oversight of your entire transport operation without the administrative headache of individual contracts.

This type of cover is fundamentally different from standard commercial van or motor trade policies. Motor trade insurance typically focuses on businesses that handle customer vehicles, whereas an HGV fleet policy protects your own assets used for your specific trade. It provides the essential legal protection required to operate on public roads, meeting the UK’s minimum requirements for third-party liability. Understanding the basics of Vehicle insurance is a good starting point for any operator, but HGV policies require more specialized oversight due to the weight of the vehicles and the potential risk associated with their cargo.

Who Needs a Small HGV Fleet Policy?

Many sectors rely on heavy vehicles to function effectively. Construction firms often require Motor Fleet Insurance to move heavy plant and machinery between sites. Similarly, local distribution and “last-mile” delivery businesses operating 7.5t trucks find that a fleet policy offers the flexibility they need to swap drivers between vehicles as demand shifts. Specialized trades, such as those in waste management or heavy engineering, also benefit from the streamlined administration of a consolidated policy. If you’re managing more than one heavy vehicle, the transition to hgv fleet insurance for small business is usually the most cost-effective move.

Gross Vehicle Weight (GVW) and Your Policy

Weight classes define your insurance requirements and premium levels. Light Goods Vehicles (LGVs) usually stay under the 3.5-tonne mark, while anything above that enters HGV territory. The distinction becomes even more critical when vehicles exceed 7.5 tonnes. At this level, insurers look for specific driver qualifications and apply higher risk tiers because of the increased damage potential in the event of an accident. If your business uses a mix of transit vans and larger lorries, you don’t need separate policies. We can integrate mixed fleets into a single, cohesive plan that covers everything from your smallest van to your heaviest articulated truck, ensuring consistent protection across your entire operation.

Core Components of Comprehensive Small Fleet Cover

Choosing the right level of cover for high-value assets is the first step in protecting your bottom line. While Third Party, Fire and Theft is an option, most operators opting for hgv fleet insurance for small business choose Comprehensive. This level covers accidental damage to your own vehicles, which is vital when a single unit represents a significant financial investment. Commercial vehicle insurance is about more than just staying legal; it’s about protecting your balance sheet from total loss in the event of an at-fault accident.

Flexibility is a major factor for SMEs. An Any Driver policy allows any qualified employee to jump in the cab, which is perfect for busy periods or sudden shifts in scheduling. However, this often comes with age restrictions, typically requiring drivers to be over 25 or 30. If you have a stable team of experienced drivers, a Named Driver policy might lower your premiums, but it limits your ability to react to sudden staff absences. To ensure you aren’t overpaying for features you don’t need, it helps to speak with a specialist broker who can trim the fat from your policy.

Your vehicles are just tools; the cargo is your revenue. Goods in Transit cover protects the items you carry against theft, loss, or damage while they are out for delivery. Without it, a single incident could wipe out your profit for the quarter. Securing the right hgv fleet insurance for small business ensures that your vehicles and your cargo are protected under one cohesive agreement.

Liability Protections for Fleet Operators

HGV operations carry risks that extend far beyond the tarmac. Public Liability Insurance is essential for covering incidents during loading or unloading on a client’s site. You also need to consider environmental liability. A fuel leak or a chemical spill can lead to massive cleanup costs and legal fines. Finally, Employers Liability Insurance remains a strict legal requirement for any fleet owner with employees, providing protection against claims for workplace injuries or illnesses.

Specialist Add-ons for HGVs

Small fleets often benefit from specialist add-ons that handle the “what ifs.” HGV breakdown and recovery is a prime example. Towing a 44-tonne truck requires specialized equipment that can cost thousands without a policy in place. Legal expenses cover is another wise addition, helping you manage the fallout from post-accident litigation. If your business delivers across the Channel, ensure you have a foreign use extension. This is particularly important for 2026 as Smart Tachograph Version 2 mandates take effect for all goods vehicles over 2.5 tonnes used for international transport.

Why an Independent Broker is Essential for Small Fleets

Automated comparison portals are efficient for standard car insurance, but they often struggle with the nuances of hgv fleet insurance for small business. An independent broker provides a vital link to specialized markets, including Lloyd’s of London. These insurers don’t typically offer quotes on public price comparison sites. They prefer working with brokers who can present a detailed, professional risk profile. This access ensures you receive a policy tailored to your specific trade rather than a generic product that might leave you underinsured or overcharged.

Impartiality is a core benefit of the broker model. We don’t work for the insurance companies; we work for you. This means we scan the entire market to find the best value without any bias toward a specific provider. Our team also brings deep local expertise to the table. We understand the economic landscape of the West Midlands and Staffordshire. We know the regional routes and the specific risks facing local trades, which helps us build a more accurate and persuasive case for underwriters when negotiating your premiums.

The Human-Centric Alternative to Algorithms

Algorithms can’t understand why your 7.5t truck has specialized equipment or why your business only operates within a specific radius. When a “computer says no” because your operation doesn’t fit a standard template, a human broker steps in to explain the context to an underwriter. This human-to-human negotiation is often the only way to secure cover for niche HGV uses. Having a local contact is also invaluable during the claims process. If an accident occurs, you won’t be stuck in an endless automated phone queue. You’ll have a dedicated advisor to manage the paperwork and advocate for a fair, fast settlement. For more information on regional support, you can read our guide on choosing a Commercial Insurance Broker Staffordshire.

Streamlining Your Renewals

Managing multiple insurance policies with different start dates is a significant drain on your time. We can consolidate all your vehicles into one “common renewal date.” This means you only have to deal with your insurance once a year, significantly reducing your administrative overhead. Brokers also handle mid-term adjustments seamlessly. If you buy a new vehicle or sell an old one, we update the policy and ensure your cover remains continuous and compliant. It’s a pragmatic approach to fleet management that allows you to focus on your daily operations while we handle the complex administrative burdens.

Strategies to Reduce HGV Fleet Premiums in 2026

Managing the costs of hgv fleet insurance for small business in 2026 requires more than just shopping around; it demands a commitment to tactical risk management. Implementing telematics and multi-camera dashcam systems is a proven way to demonstrate driver safety to underwriters. These tools provide objective data that can override generic risk profiles, often leading to significant premium reductions. When you combine technology with updated driver training programmes, specifically those aligned with the January 2026 ABA categories, you present your hgv fleet insurance for small business as a lower-risk entity.

Another effective lever is the voluntary excess. Increasing your excess can lower your annual premium, but you must calculate the right balance to ensure your business can comfortably cover out-of-pocket costs after an incident. Security also plays a major role. Parking your fleet in a secure, monitored facility overnight significantly reduces the risk of theft and vandalism compared to street parking, which insurers reward with more favorable terms. When you need to simplify this process, Just Quote Me to see how these factors impact your specific costs today.

Managing Your Claims History

The Ogden Rate remains a significant factor in premium calculations, as it dictates how much insurers set aside for personal injury claims. With CPI inflation predicted to reach 3.5% by the end of 2026, repair and medical costs continue to rise. Since 2021, average claim values have already increased by more than 20% due to inflationary pressures on parts and labor. To protect your low-claim bonuses, you should adopt a proactive incident reporting policy. Reporting minor bumps within 24 hours prevents claim inflation and allows your insurer to manage third-party costs effectively before they spiral.

Driver Management and Age Restrictions

Driver age is a sensitive variable in HGV insurance pricing. While an “Any Driver Over 21” policy offers recruitment flexibility, premiums are substantially higher than “Any Driver Over 25” agreements. Insurers view younger drivers as a higher risk due to a lack of experience with heavy loads. Vetting new hires remains essential; you should conduct thorough licence checks and verify previous experience to maintain fleet integrity. To put it simply, every year of age and experience added to your driver roster typically correlates with a measurable reduction in your annual insurance expenditure.

Securing Your Bespoke HGV Fleet Quote with Just Quote Me

With 30 years of experience in the UK insurance brokerage market, Just Quote Me understands the unique pressures facing small fleet operators. We specialize in providing Motor Fleet Insurance for SMEs, moving beyond the rigid templates used by larger, impersonal corporations. Our approach is built on regional trust. Businesses in Stone, Stafford, and Newcastle-under-Lyme rely on our expertise because we combine the authority of an industry veteran with the accessibility of a local partner. We manage the complex administrative burdens so you can focus on your core business goals.

The process of securing hgv fleet insurance for small business with us is efficient and transparent. It starts with an initial consultation where we identify the specific risks associated with your trade. We then take that information directly to our network of specialist underwriters to negotiate the best possible terms on your behalf. This human-to-human interaction often results in more tailored cover and better pricing than any automated portal could provide. We pride ourselves on being a steady hand in a complex market, ensuring your fleet remains protected and compliant as regulations evolve through 2026.

What Information You Need for an HGV Quote

To provide an accurate and competitive quote, we need a clear picture of your transport operation. Gathering these details in advance will speed up the process significantly:

- Vehicle details: We require the make, model, and Gross Vehicle Weight (GVW) for every unit in the fleet, including any specialized equipment or modifications.

- Driver details: You will need to provide the age, licence types, and at least three to five years of claims history for all named drivers or those covered under “any driver” restrictions.

- Business details: Be prepared to discuss the nature of the goods you carry, your typical annual mileage, and your primary operating radius.

Take the Next Step for Your Small Business

Partnering with an independent broker like Just Quote Me provides your business with tactical advantages that go beyond simple price savings. You gain access to specialist markets and benefit from our proactive approach to risk management. As an FCA-authorised firm, we provide expert advice that you can rely on for long-term security. We are here to simplify your administration, consolidate your renewal dates, and advocate for you during the claims process. Protecting your heavy vehicle fleet shouldn’t be a source of stress; it should be a foundation for your business growth.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Future-Proof Your Transport Operation

Managing a small fleet in 2026 requires a balance of regulatory compliance and smart financial planning. By consolidating your vehicles into a single policy and implementing proactive risk management, you can stabilize your overheads despite rising industry costs. Choosing hgv fleet insurance for small business through an independent broker ensures you aren’t just another number in an automated system. You benefit from over 30 years of industry experience and direct access to top UK insurers, including the specialized Lloyd’s market.

As an FCA-authorised broker, Just Quote Me provides the human oversight necessary to navigate complex jargon and secure bespoke cover that fits your specific trade. Whether you’re moving plant machinery or handling last-mile deliveries, we manage the administrative weight so you can focus on the road ahead. Let us help you find a pragmatic solution that keeps your business moving forward safely and cost-effectively.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Frequently Asked Questions

What is the minimum number of vehicles for an HGV fleet policy?

Most insurers require a minimum of two vehicles to qualify for a fleet policy. While some providers focus on massive haulage operations, we specialize in helping businesses in the two to five vehicle bracket. This entry point allows you to consolidate your paperwork and renewal dates immediately. It’s an efficient way to manage hgv fleet insurance for small business without needing a large fleet to see the administrative benefits.

Can I include vans and HGVs on the same fleet insurance policy?

You can absolutely include both vans and HGVs on a single multi-vehicle policy. This is known as a mixed fleet and is a pragmatic choice for businesses that use smaller transit vans for local errands alongside larger trucks for heavy haulage. Consolidating different vehicle types into one agreement simplifies your management tasks. It also ensures that every asset, regardless of its weight class, is protected under a consistent level of cover.

How does Gross Vehicle Weight (GVW) affect my insurance premiums?

Gross Vehicle Weight is a primary factor in determining your premium because heavier vehicles have a higher potential for damage in an accident. A 44-tonne articulated lorry carries more risk than a 7.5-tonne rigid truck. Insurers also consider the specific driver qualifications required for higher weight classes. As you move up the GVW scale, underwriters look for more robust safety records and specialized experience to mitigate the increased liability risks.

Is Goods in Transit insurance included in an HGV fleet policy?

Goods in Transit insurance is typically an optional add-on rather than an automatic feature of a standard HGV policy. While your fleet insurance covers the vehicle itself, Goods in Transit protects the cargo you are carrying against theft or damage. It is essential for distribution businesses to ensure their revenue is protected while on the move. We recommend reviewing your cargo values to ensure your limits match the actual worth of your loads.

Are there age restrictions for drivers on a small business HGV fleet?

Most HGV insurers apply a minimum age restriction of 25 for drivers due to the high risk associated with heavy vehicles. While it is possible to find cover for drivers over 21, you will likely face significantly higher premiums and increased excesses. We often advise small businesses to aim for a driver roster aged 30 and over to secure the most competitive rates. This demographic is viewed by underwriters as the most stable and experienced.

What happens if my HGV breaks down without specialist recovery cover?

Without specialist recovery cover, you are responsible for the full cost of towing and roadside assistance for your heavy vehicles. Standard breakdown services often lack the equipment needed to recover a fully laden HGV, leading to private recovery fees that can reach thousands of pounds. Including this as an add-on to your hgv fleet insurance for small business prevents these sudden, high expenses. It ensures your drivers aren’t stranded and your delivery schedules remain intact.

How can telematics help lower my small business fleet insurance costs?

Telematics systems lower costs by providing insurers with objective evidence of safe driving behaviors. By monitoring braking, cornering, and speed, you can prove to an underwriter that your fleet is lower risk than the industry average. This data-driven approach is particularly effective for small businesses looking to differentiate themselves from larger fleets. Many insurers now offer premium discounts or more favorable terms to operators who commit to using active telematics and on-board cameras.

Why should I use an insurance broker instead of going direct to an insurer?

Using an independent broker gives you access to a wider range of insurers, including specialist markets like Lloyd’s of London that don’t sell directly to the public. Unlike a direct insurer who only offers their own product, a broker works for you. We compare multiple quotes to find the best value and provide human advocacy during the claims process. This personalized service is a human-centric alternative to the automated systems used by many direct providers.

Article by

Just Quote Me

JustQuoteMe Ltd is an independent UK insurance brokerage specialising in business and personal insurance solutions. With over 35 years of industry experience, the company provides tailored insurance cover for businesses, landlords, tradespeople, hospitality venues, fleets, and individuals across the UK. Known for its personal service, expert advice, and competitive premiums, JustQuoteMe Ltd works with leading insurers to deliver bespoke policies designed around each client’s unique needs. The company is authorised and regulated by the Financial Conduct Authority (FCA No. 586607) and has built a reputation for trusted, straightforward insurance guidance and long-term client relationships.

by jqm | Jun 21, 2026 | Insurance

Why are you still managing three different renewal dates, three separate sets of paperwork, and three climbing premiums every year? For many small businesses, reaching a trio of vehicles is the exact moment where individual policies stop making sense and administrative overhead starts to bite. Choosing mini fleet insurance for 3 vans is often the most efficient way to regain control over your schedule and your budget. With van insurance premiums seeing a 2.3 percent climb in early 2026, sticking with the status quo could be costing you more than just your time.

It’s frustrating to watch your overheads rise while you’re busy trying to grow your business. We understand that you need a solution that is both reliable and straightforward. This guide will show you exactly how a single policy can reduce your annual costs and eliminate the headache of managing new drivers. We will explore the latest 2026/2027 tax updates, including the £4,170 van benefit charge, and provide a clear roadmap to help you secure the best coverage for your fleet.

Key Takeaways

- Consolidate your administrative burden by moving three separate renewal dates into a single, manageable policy.

- Learn how switching to mini fleet insurance for 3 vans unlocks commercial rates that are often lower than individual premiums.

- Discover the flexibility of “Any Driver” coverage which simplifies the paperwork involved when hiring new staff or swapping vehicles.

- Understand why accurate declarations for “Carriage of Own Goods” are essential to protecting your assets and maintaining policy validity in 2026.

- Find out how working with an independent broker provides a human-centric alternative to automated systems for more personalized coverage.

What is Mini Fleet Insurance for 3 Vans?

Mini fleet insurance is a specialized commercial product designed to consolidate the coverage of a small number of vehicles, typically ranging from 3 to 12. For many UK businesses, the transition to mini fleet insurance for 3 vans marks the point where manual administration becomes a genuine burden. Instead of juggling three separate policies with different providers and varying renewal dates, a mini fleet policy brings everything under one roof. This single-renewal structure is a game changer for builders, couriers, and service providers who need to focus on their clients rather than their filing cabinets.

An independent broker plays a vital role in this process. Unlike automated comparison sites that often struggle with the nuances of commercial use, a broker can tailor a policy to your specific trade. They act as a steady hand, ensuring that your fleet is protected by a policy that reflects how you actually work. This human-centric approach avoids the “computer says no” mentality, providing a pragmatic solution for businesses that don’t fit into a standard box.

How a Mini Fleet Policy Differs from Multi-Van Cover

While they might sound similar, fleet insurance is a distinct commercial category. Multi-van cover is frequently a consumer-grade extension of a personal policy, which can be restrictive for a growing business. Fleet terms are built for professional flexibility. One of the most significant advantages is the “Any Driver” option. While individual policies often require you to name every driver, motor fleet insurance often allows any authorized employee to get behind the wheel. This is particularly useful in 2026, as recruitment needs can change quickly. Most specialist underwriters view three vehicles as the baseline for these professional terms, making it the ideal entry point for small businesses.

Key Components of a 3-Van Policy

Every policy starts with the legal requirement for Vehicle insurance, as defined by the Road Traffic Act 1988. You can choose between Comprehensive, Third Party Fire and Theft (TPFT), or Third Party Only (TPO). A major benefit of mini fleet insurance for 3 vans is the ability to mix vehicle types. You don’t need a fleet of identical vans; you can cover a mix of large Transits and smaller Caddies under the same agreement. This flexibility is essential for service-based businesses that use different vehicles for different tasks.

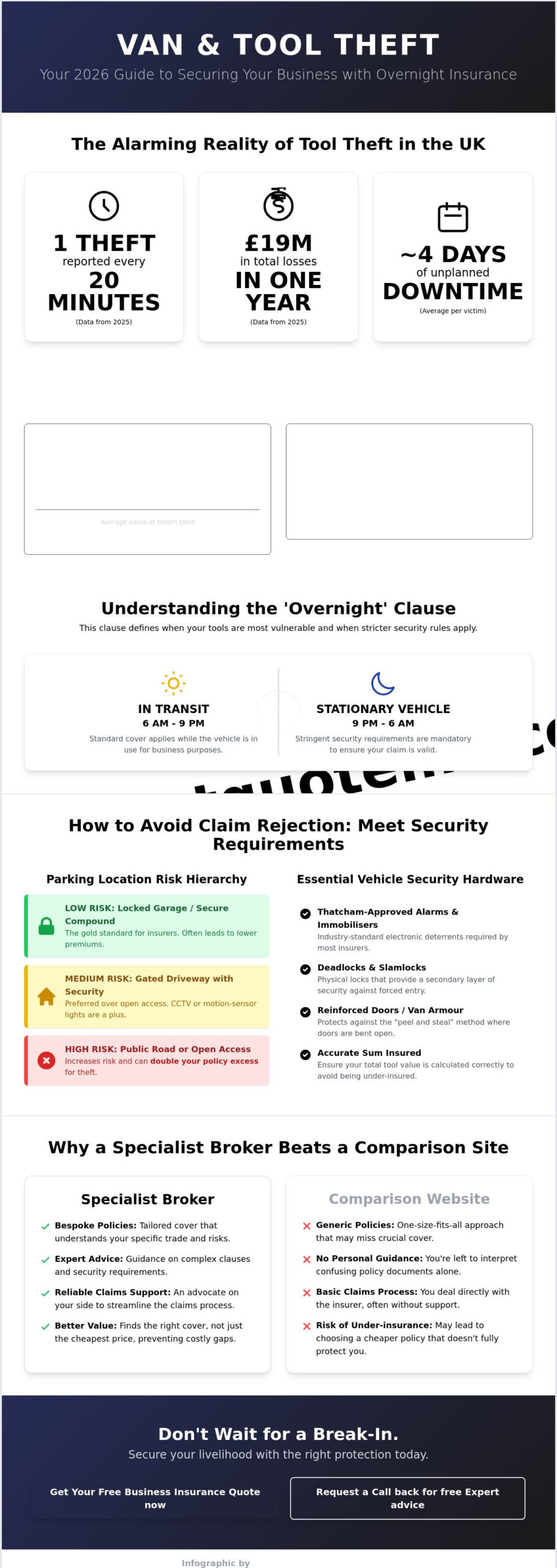

Centralised claims management is another cornerstone of these policies. If an accident occurs, you deal with one point of contact for the entire business. This efficiency is critical when you consider that the average claim for tool theft from vans now exceeds £3,200. Having a single, robust policy ensures that the claim process is as frictionless as possible, allowing you to get back to work without unnecessary delays.

The Benefits of Switching at the 3-Van Milestone

Reaching three vehicles is a significant milestone for any small business. It’s the point where you stop being a collection of individual drivers and start operating as a professional fleet. This is why mini fleet insurance for 3 vans is so effective; it rewards your growth by offering access to bulk rates that are simply unavailable to individual policyholders. By moving to a commercial auto insurance policy, you’re no longer just three separate risks in the eyes of an insurer. You’re a single, manageable entity, which often results in a lower cost per vehicle.

The “Any Driver” advantage is particularly potent at this stage. As your team grows, you don’t want to be stuck on the phone with an insurer every time you hire a new technician or a temporary courier. Fleet policies typically allow any authorized employee over a specific age to operate any vehicle in the fleet. This removes the administrative friction of “Named Driver” policies and ensures your vans are never sitting idle because of a paperwork delay. It’s a pragmatic shift that supports the fast-paced nature of modern trade and delivery services.

Future-proofing is another key benefit. Adding a fourth or fifth van to an existing motor fleet insurance policy is significantly faster than starting a fresh individual application. If you win a new contract and need another vehicle on the road by Monday, your fleet policy can usually accommodate it with a simple notification. This agility is vital for businesses looking to scale without being held back by their administrative setup.

Managing Your No Claims Discount (NCD)

One common concern when switching to mini fleet insurance for 3 vans is what happens to your hard-earned NCD. Most insurers will convert your individual years of no-claims into a “Fleet Rated” bonus. This doesn’t mean your history is lost; instead, it’s pooled to benefit the entire business. If one van has a minor scrape, it won’t necessarily wipe out the discount for the entire fleet in the same way an individual claim would. This structure protects your business from the financial impact of a single isolated incident, helping you maintain a stable premium over time.

Simplifying Business Administration

Managing your finances becomes much easier with a consolidated policy. You move from three different monthly or annual payments to one single premium, which improves your cash flow management. Bookkeeping is also simplified with just one VAT receipt to process and one renewal date to remember. You can even add temporary vehicles or hired vans to the same policy during busy periods. If you’re ready to cut down on your paperwork, you can explore tailored fleet options that fit your specific business model and trade requirements.

- One single renewal date replaces multiple administrative cycles.

- Easier accounting with a single premium and VAT receipt.

- Flexible “Any Driver” terms that simplify recruitment.

- The ability to add or remove vehicles quickly as your business scales.

Individual vs. Fleet Insurance: Which is Right for Your 3 Vans?

Deciding between three separate policies and a single fleet agreement is a pivotal moment for a growing business. While a fleet policy isn’t always cheaper on day one, the long-term savings in administrative time and operational flexibility are significant. For many, mini fleet insurance for 3 vans represents the threshold where the math shifts in favor of consolidation. Industry data from early 2026 suggests that switching to business fleet cover can offer savings of 10 to 25 percent compared to insuring vehicles individually. This makes it a pragmatic choice for those looking to scale without increasing their paperwork.

There are instances where sticking with individual policies might still make sense. If your three vehicles have vastly different uses, such as one dedicated to heavy site work and another used primarily for personal errands, the risk profiles might be too disparate for a single fleet underwriter to price competitively. However, for most trades where all three vans are performing similar commercial duties, the benefits of a single renewal date and unified claims process usually outweigh any minor price differences found on generic comparison sites.

The Cost Comparison: 3 Policies vs. 1 Fleet

Individual policies are often priced for the mass market, which means they don’t account for the unique needs of a professional team. Brokers like Just Quote Me specialize in finding “mini-fleet” underwriters that major aggregators frequently overlook. These specialists understand that three vans are a distinct risk profile and offer terms that reflect your professional status. By combining your vehicles, you reduce the insurer’s administrative cost per unit. You can review more motor fleet insurance details to see how these technical specifications apply to your specific vehicle mix. This approach ensures you aren’t paying a premium for three separate sets of overhead costs.

Evaluating Your Driver Risk

Driver experience is the biggest variable in your premium calculation. In 2026, insuring drivers under the age of 25 can increase a premium by 25 to 40 percent. An “Any Driver over 25” policy is the gold standard for small fleets. It simplifies your hiring process immediately because you don’t need to wait for an insurer’s approval before a new team member starts their first shift. This is the point where driver flexibility becomes a major operational win. Instead of managing three separate “Named Driver” lists, you have a blanket of protection that covers your entire workforce. It’s a straightforward solution for businesses that value speed and efficiency over micro-managing every policy detail.

How to Secure the Best Rates for 3-Van Mini Fleet Insurance

Securing the most competitive rates for mini fleet insurance for 3 vans requires a shift from generic searching to precise data presentation. Insurers in 2026 are increasingly analytical, rewarding businesses that provide granular details about their operations. You need to gather comprehensive driver histories, exact vehicle specifications, and realistic annual mileage estimates before starting the process. Being honest about mileage is particularly important; underwriters are now more skeptical of ultra-low claims, and accurate declarations prevent policy invalidation during a claim.

One of the most critical elements is the “Carriage of Own Goods” declaration. This term is often misunderstood, but it’s essential for businesses that transport their own equipment or stock. Whether you’re a plumber with a van full of copper piping or a landscaper with heavy machinery, declaring this use correctly ensures your protection is valid. To complement this, many small fleets are now adopting telematics and dashcams. These “black box” technologies monitor driving habits like braking and speed, providing tangible evidence of a low-risk profile that can lead to lower premiums over time.

While automation works for simple car insurance, it often fails when handling the nuances of a small business. An independent broker can access non-standard markets and specialist underwriters that don’t appear on price comparison sites. This human-centric approach allows for a pragmatic evaluation of your risk rather than a “computer says no” result. If you want to see how this personalized service can benefit your bottom line, you can get a tailored quote from our expert team today.

Risk Management for Small Fleets

Implementing a basic driver safety policy is a straightforward way to demonstrate reliability to an insurer. Even with a small three-man team, having clear guidelines on vehicle maintenance and usage can lower your risk profile. Location also plays a significant role in your quote. For businesses operating in Staffordshire or the West Midlands, secure overnight parking in a locked compound or garage can positively impact your premium. Given that the average claim for stolen tools now exceeds £3,200, many tradespeople also choose to integrate van tools insurance as a vital bolt-on to their main fleet policy.

Preparing for Your Broker Consultation

Preparation is the key to a frictionless experience. You should have your V5C logbooks and proof of your current No Claims Discount (NCD) ready for review. Explaining your business use accurately is the best way to avoid claim rejection later. For example, if your vans are primarily used for construction projects, you should discuss how your fleet policy integrates with your wider builders insurance. This ensures there are no gaps in your coverage between your transit risks and your site-based liabilities. Having this documentation organized allows your broker to present your business in the best possible light to specialist underwriters.

Why Just Quote Me is Your Ideal Mini Fleet Partner

Finding the right mini fleet insurance for 3 vans isn’t just about finding the lowest number on a screen. It’s about finding a partner who understands the local landscape and the specific pressures of running a small business in 2026. Just Quote Me brings over 30 years of experience as an independent UK insurance broker to your side. We don’t rely on the rigid, automated algorithms that larger aggregators use. Instead, we use our long-standing relationships with a wide panel of specialist UK underwriters to find coverage that actually fits your trade.

Our expertise extends deep into the local markets of Stafford, Stone, and Newcastle-under-Lyme. We know the regional risks and the local business community, which allows us to provide advice that’s both relevant and practical. By working with us, you gain access to insurance markets that are often closed to the general public. This ensures your three-van fleet is rated fairly and accurately based on your actual performance rather than a generic postcode average. We position ourselves as a steady hand in a complex market, managing the administrative heavy lifting so you don’t have to.

The Human Touch in Commercial Insurance

We prioritize expert advice over automated systems because we know that no two businesses are identical. Whether you’re transitioning from individual policies or looking to move away from a standard multi-van setup, we’re here to manage the paperwork for you. Our goal is to simplify your administrative cycles, replacing three separate renewal dates with one clear, manageable point in the year. As your business scales, we scale with you. We’ve helped many clients grow their operations from a modest 3-van setup to a 30-vehicle fleet, providing steady guidance through every stage of their expansion.

Ready to Simplify Your Van Insurance?

Switching to a consolidated policy is the most effective way to reclaim your time and potentially reduce your annual premiums. You’ve seen how the 2026 market is shifting; don’t let rising costs or administrative burdens slow your momentum. Getting a tailored quote is the first step toward a more efficient business model. Our team is ready to provide the pragmatic, straightforward solutions your business deserves.

Take Control of Your Small Business Fleet

Consolidating your vehicles into a single policy is more than just a convenience; it’s a strategic move to protect your bottom line. By switching to mini fleet insurance for 3 vans, you replace the friction of multiple renewal dates with a unified system that grows alongside your team. You’ve seen how this transition unlocks commercial rates and provides the essential flexibility to hire new drivers without the usual administrative delays.

As an FCA-authorised independent broker with over 30 years of industry experience, Just Quote Me specializes in delivering these bespoke solutions for UK trades and businesses. We know that your time is better spent on-site than managing a filing cabinet full of individual policies. Our pragmatic approach ensures that your coverage is as reliable as the vans you drive.

If you’re ready to slash your admin time and secure a deal that reflects your professional status, Get Your Free Business Insurance Quote now. Streamlining your operations is a straightforward process when you have a steady hand to guide you through the market. Focus on your growth and let us handle the complexities of your commercial protection.

Frequently Asked Questions

Is mini fleet insurance cheaper for exactly 3 vans?

It is often more cost-effective because insurers offer bulk-buying discounts once you reach this specific threshold. While individual premiums for a single van averaged £432 in early 2026, combining three vehicles under one agreement reduces the insurer’s administrative overhead. This efficiency is passed on to you as a lower rate per vehicle. You also save on the hidden costs of managing three separate sets of paperwork and renewal dates.

Can I include different types of vehicles on a 3-van fleet policy?

Yes, you can mix and match various vehicle types within a single policy. You don’t need a uniform fleet of identical models to qualify for these terms. It’s common to cover two large Transit vans alongside a smaller Caddy or even a commercial 4×4. This flexibility allows your insurance to reflect the actual diversity of your business operations without forcing you into multiple individual policies for different vehicle classes.

What happens to my No Claims Discount when I move to a fleet policy?

Your individual No Claims Discount (NCD) is typically converted into a “fleet-rated” discount during the transition. This means your previous driving history isn’t lost; instead, it’s used to calculate a collective bonus for the entire policy. If one vehicle is involved in an incident, it won’t necessarily reset the discount for the other two vans. This structure helps stabilize your premiums even if one driver has a minor scrape.

Does fleet insurance cover “Any Driver” for my business?

Most mini fleet insurance for 3 vans policies offer an “Any Driver over 25” option as a standard feature. This is a significant upgrade from individual policies where you must name every specific person on the document. It allows any authorized employee meeting the age criteria to drive any vehicle in your fleet. This streamlines your recruitment process because you don’t need to contact your broker every time you hire a new technician.

Is public liability insurance included in a mini fleet policy?

Public liability is not automatically included in a standard road risk policy, but it can be added as a bolt-on. While your fleet policy covers vehicle-related incidents, it doesn’t protect you if a member of the public is injured by your business activities outside the van. Most tradespeople choose to bundle these protections together for administrative ease and to ensure there are no gaps in their commercial liability.

What is the minimum number of vehicles for a fleet policy in the UK?

The standard minimum for a fleet policy in the UK is usually two or three vehicles. While some niche products exist for two vehicles, most specialist fleet underwriters consider mini fleet insurance for 3 vans to be the ideal entry point for professional terms. Reaching this milestone allows you to move away from consumer-grade multi-car extensions and into the more flexible world of commercial fleet rating and management.

Can I add a fourth van to my policy mid-term?

You can easily add a fourth vehicle to your existing policy at any point during the term. This is one of the primary benefits of fleet management; you don’t need to start a fresh application or wait for a new renewal date. Your broker simply updates the schedule and adjusts the premium proportionally for the remaining months. This agility is vital for businesses responding to new contracts or seasonal demand.

Do I need employers liability insurance if I have 3 vans and 3 drivers?

Employers liability is a legal requirement if you employ anyone, even on a temporary or casual basis. If those three drivers are employees rather than just the business owners, you must have this cover in place by law. While it’s a separate legal protection from your vehicle insurance, it’s often more efficient to manage both through the same broker to ensure your business remains fully compliant and legally protected.

Article by

Just Quote Me

JustQuoteMe Ltd is an independent UK insurance brokerage specialising in business and personal insurance solutions. With over 35 years of industry experience, the company provides tailored insurance cover for businesses, landlords, tradespeople, hospitality venues, fleets, and individuals across the UK. Known for its personal service, expert advice, and competitive premiums, JustQuoteMe Ltd works with leading insurers to deliver bespoke policies designed around each client’s unique needs. The company is authorised and regulated by the Financial Conduct Authority (FCA No. 586607) and has built a reputation for trusted, straightforward insurance guidance and long-term client relationships.

by jqm | Jun 20, 2026 | Insurance

Did you know that as of 2026, failing to meet the latest SIA training requirements could leave your firm’s liability coverage completely void? Running a professional security firm involves managing high-stakes risks every single day, yet finding Security company insurance that actually understands the specific nuances of the regulatory environment often feels like an uphill battle. You are likely frustrated by soaring premiums and the ongoing headache of deciphering complex ‘efficacy’ or ‘wrongful arrest’ clauses that seem designed to confuse rather than protect. It is a common challenge to find a partner who sees beyond the high-risk label to the professional, disciplined operation you actually run.

We believe that protecting your business shouldn’t be more stressful than the job itself. This guide simplifies these complexities by offering a clear, pragmatic path to bespoke insurance solutions tailored for 2026. We will explore how to manage modern cyber-physical threats, ensure your contracts remain fully compliant, and gain the peace of mind that comes from knowing your guards are truly protected against liability claims. This overview provides the expert advice you need to turn your insurance from a complex administrative burden into a strategic shield for your firm’s future.

Key Takeaways

- Understand why standard policies often fail and how specialist Security company insurance protects against ‘failure to perform’ risks specific to 2026.

- Identify the essential covers required for contract compliance, including mandatory Employers’ Liability and robust Public Liability protections for your workforce.

- Learn why ‘Efficacy’ and ‘Wrongful Arrest’ clauses are critical for protecting your firm if security measures fail or legal disputes arise.

- Navigate emerging 2026 threats, such as liability for AI surveillance errors and cyber breaches affecting digital access control systems.

- Discover how working with an expert broker provides access to a specialist panel of UK underwriters who truly understand the security sector.

What is Security Company Insurance and Why is it Essential in 2026?

A modern Private security company operates in an increasingly litigious and regulated environment. Security company insurance is not a single policy but a strategic bundle of specialist covers designed to protect manned guarding firms, door supervisors, and electronic security installers. By 2026, the gap between standard business insurance and specialist security cover has widened significantly. General policies often exclude “failure to perform” risks, leaving firms vulnerable if a security measure fails to prevent a loss. Without bespoke protection, your firm faces catastrophic financial exposure from claims that a standard public liability policy won’t touch.

Your insurance status directly affects your standing with the Security Industry Authority (SIA). Following the April 1, 2025, introduction of mandatory refresher qualifications, insurers now scrutinize training records more closely before offering terms. Maintaining the right Security company insurance is essential for your Approved Contractor Scheme (ACS) standing. If your insurance lapses or provides inadequate protection, you risk losing your accreditation and the high-value contracts that come with it. Firms handling close protection or high-value assets require even more granular policies to address specific risks like international transit liabilities or specialized equipment failure.

The Core Components of a Security Policy

A robust policy starts with public liability insurance, which covers third-party injuries or property damage occurring during patrols. Next is employers’ liability insurance. This is a legal requirement for any firm employing guards, bouncers, or office staff. Finally, professional indemnity insurance protects your firm when providing consultancy or risk assessments. These three pillars form the foundation of a contract-compliant business. They ensure you can meet the stringent demands of commercial clients who require proof of cover before work begins.

Manned Guarding vs. Electronic Security Needs

Physical guarding and electronic security face very different threat profiles. For firms providing physical personnel, risks often center on wrongful arrest or claims regarding the use of force. Conversely, electronic security firms deal with alarm failures and system monitoring liabilities. If a CCTV system fails during a break-in, the installer could be held liable for the resulting theft. A “one size fits all” approach creates dangerous gaps in cover. You need a policy that reflects the specific tasks your team performs every day. Generic business cover doesn’t account for these professional nuances.

Navigating the ‘Must-Have’ Covers for Security Professionals

Building a robust insurance portfolio is about more than ticking boxes. It is about ensuring your business survives a worst-case scenario. Securing the right Security company insurance requires a granular understanding of your daily operations. While many providers offer a generic package, a professional firm needs a policy built on specific, high-limit protections that satisfy both the law and demanding client contracts.

Public Liability: More Than Just ‘Slips and Trips’

In the security sector, public liability insurance serves as the primary shield against claims of third-party injury or property damage. Unlike a standard retail shop, your guards operate in high-friction environments where the risk of accidental damage is significantly higher. A critical aspect often overlooked is the ‘care, custody, or control’ extension. Standard policies frequently exclude damage to property you’re actively guarding. If your team is responsible for a site and a fire occurs due to a missed patrol, you need specific wording to ensure the claim is paid. Most commercial contracts now demand a minimum of £5 million in cover, though £10 million is becoming the standard for public-facing roles. The legal necessity for such protection is mirrored internationally, as seen in Washington state law for security firms, which mandates liability insurance to maintain a professional license.

Employers’ Liability: Protecting Your Frontline

For any firm utilizing personnel, employers liability insurance is a non-negotiable legal requirement. In the UK, you must have at least £5 million in cover, though we typically recommend £10 million to account for severe incidents. This protection is vital if you use subcontractors or temporary staff, as the law often views them as employees for insurance purposes. It provides a safety net if a guard is assaulted, injured on-site, or develops a long-term illness related to their duties. Failing to hold valid EL cover can result in fines of up to £2,500 per day from the Health and Safety Executive. It’s about protecting the people who protect your clients.

Your hardware also needs protection. Commercial property and equipment cover ensures that expensive radios, body cams, and monitoring station hardware are replaced quickly if stolen or damaged. Additionally, if your firm provides consultancy, professional indemnity insurance covers you if your advice leads to a client’s financial loss. You can find more details on these specific protections by viewing our business insurance services designed for the security industry.

Specialist Clauses: Why ‘Efficacy’ and ‘Wrongful Arrest’ Matter

Standard business insurance is designed for offices and shops where the primary risks are simple slips and trips. For a security firm, the biggest risk is often what doesn’t happen. If your security measures fail to prevent a loss, a standard policy will likely leave you exposed. This is why specialist Security company insurance includes specific clauses that address the unique operational failures of the industry. Without these technical extensions, your firm is essentially self-insuring against the most common claims in the sector.

Understanding Efficacy and Contractual Liability

The ‘Efficacy’ clause is perhaps the most critical component of a professional security policy. Most standard liability policies exclude what they call ‘failure to perform’. If a guard misses a scheduled patrol or an alarm system fails to trigger during a break-in, the insurer might argue that you simply failed to fulfill your contract. They won’t pay for the resulting theft or damage. A specialist security insurance policy adds this protection back in, ensuring your liability is covered even when a service failure occurs.

Imagine a high-value warehouse breach where thieves bypass a perimeter fence. If the investigation reveals a guard was distracted or a sensor was improperly maintained, the client will likely sue your firm for the total value of the stolen goods. Efficacy cover ensures that your insurer handles the claim, protecting your firm from a potentially bankrupting settlement. This level of technical protection is what separates a generalist broker from a specialist partner who understands the high stakes of your work.

Legal Protection and Wrongful Arrest

Retail security and door supervisors face a constant risk of allegations regarding wrongful arrest or false imprisonment. Even if your staff followed every protocol, a disgruntled individual can still file a claim for illegal detention or assault. The legal costs to defend these cases are substantial. This protection often works alongside your professional indemnity insurance to provide a complete legal defence. It’s about protecting your firm’s reputation as much as its finances during a dispute.

Two other essential clauses to look for are Fidelity Bonding and Lost Key Cover. Fidelity Bonding protects your business if one of your own employees commits a dishonest act, such as theft from a client site. Lost Key Cover is equally practical. If a guard loses a master set of keys for a large commercial complex, the cost to replace all locks and re-secure the premises can run into thousands of pounds. Having these specific protections in place ensures that a single human error doesn’t derail your entire operation.

Managing Modern Risks: Cyber Security and AI in 2026

The security industry is changing rapidly. By 2026, the line between a physical guard and a digital firewall has almost disappeared. If your firm uses automated surveillance or facial recognition, you face liability risks that didn’t exist a decade ago. AI errors can lead to misidentification or privacy breaches, which could result in costly legal actions. Standard Security company insurance must now evolve to cover these digital-first threats. It’s no longer enough to protect against physical entry; you must also protect the systems that monitor those entry points.

The Rise of Cyber-Physical Threats

Cyber-physical threats occur when a digital breach leads to a physical security failure. If a hacker gains access to your client’s digital access control system and unlocks a door, the responsibility often falls on the security provider. This convergence makes cyber insurance a vital addition to your portfolio. It isn’t just about stolen passwords; it’s about the physical consequences of a digital attack. With 43% of UK businesses reporting a cybersecurity breach in the last 12 months, the risk is real and measurable. You also need to manage GDPR compliance for CCTV footage and biometric data stored by your firm. If this sensitive data is leaked, the financial penalties and reputational damage can be devastating. Remote monitoring stations must also have contingency plans for downtime to avoid “failure to perform” claims during a system outage.

How to Reduce Your Security Insurance Premiums

Insurers reward proactive risk management. Maintaining your SIA Approved Contractor status is one of the most effective ways to lower your risk profile. It signals to underwriters that you follow industry best practices and maintain high training standards. Using body-worn cameras is another strategic move. These devices provide undeniable evidence during a claim, often preventing expensive legal battles over disputed events. Robust incident reporting protocols also help. When you can demonstrate a consistent history of detailed, accurate reporting, insurers see a lower risk of unexpected lawsuits. Proactive guard training, especially in counter-terrorism and vulnerability awareness as required by 2025 SIA updates, further demonstrates your commitment to safety. If you want to ensure your firm is protected against these emerging threats, you can compare security insurance options that match your specific risk profile today.

Why Choose Just Quote Me as Your Security Insurance Partner?

Choosing the right partner to manage your firm’s protection is a strategic decision that shouldn’t be left to chance. Just Quote Me brings over 30 years of experience as an independent insurance broker. This longevity in the market has allowed us to build strong relationships with a specialist panel of UK underwriters who truly understand the technicalities of the security sector. We don’t just find you a policy; we find the right Security company insurance that addresses the precise risks your team faces every day.

We’ve built our reputation on being a human-centric alternative to the impersonal, automated systems that often dominate the insurance landscape. We believe in providing expert advice through direct, honest communication. Our team acts as a steady hand, managing the complex administrative burdens and paperwork so you don’t have to. This pragmatic approach ensures that whether you’re a sole trader or a national firm with a large fleet, your cover remains bespoke and scalable as your business grows.

Expert Advice from a Local Staffordshire Broker