Could one piece of misunderstood advice or a minor oversight in a high-value contract result in a claim that ends your career? As a consultant, your expertise is your product, but it’s also your greatest liability. We know that navigating the fine print of policy documents often feels like a distraction from your actual work. However, securing the right insurance for business consultants uk isn’t just about ticking a box. It’s about building a fortress around your professional reputation and your financial stability.

You’ve worked hard to establish yourself as a reliable expert, and you shouldn’t have to worry about the financial impact of a legal challenge or a strict contract clause. This guide clears away the jargon to show you exactly which covers are essential for your specific niche. We’ll explore the critical “Big Three” policies and look at the 2026 regulatory updates, including the latest Statutory Sick Pay rules and the increased legal duty to prevent workplace harassment. By the end of this article, you’ll have a clear roadmap to total compliance and the peace of mind to focus entirely on delivering results for your clients.

Key Takeaways

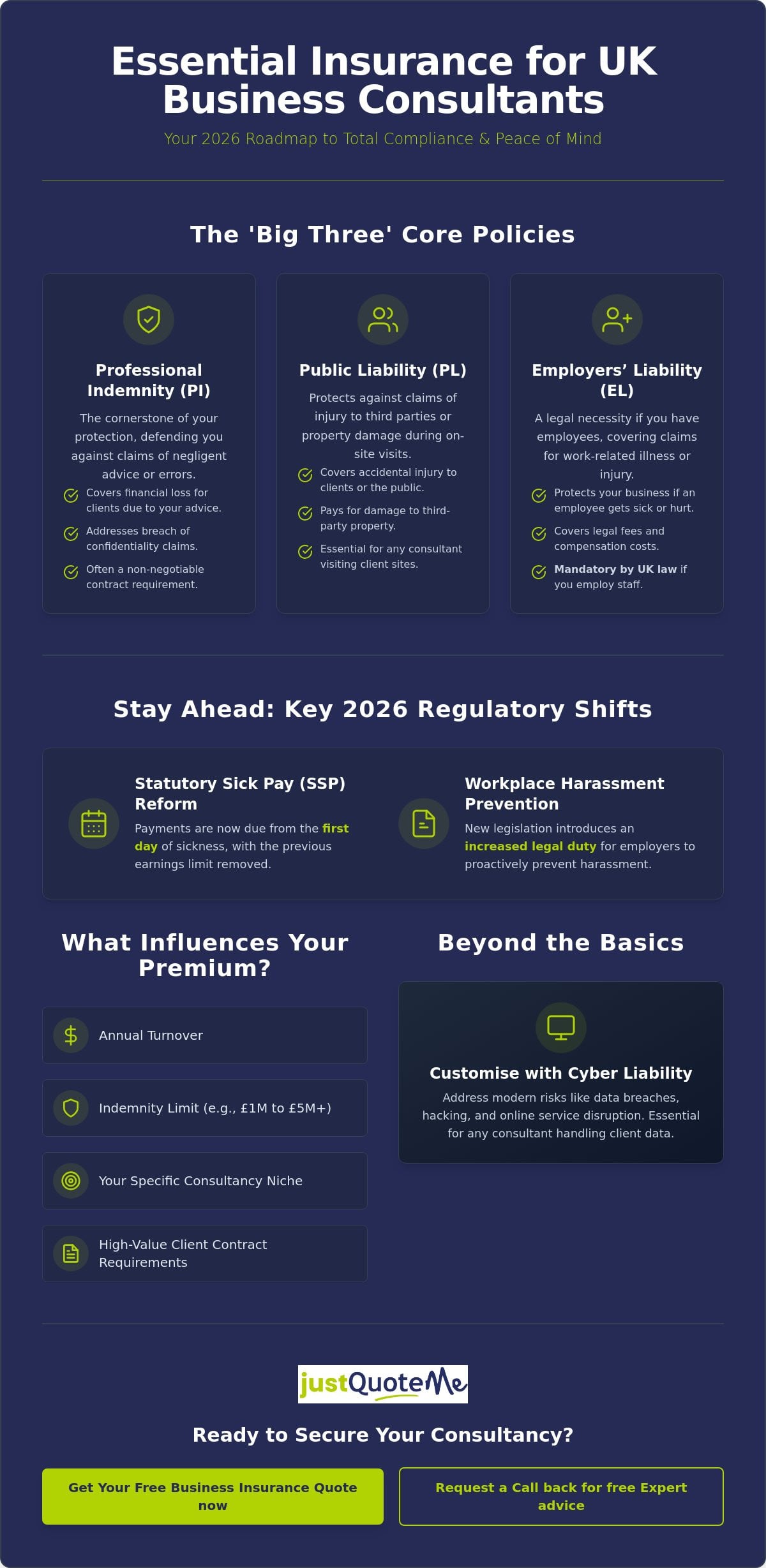

- Identify the essential “Big Three” policies—Professional Indemnity, Public Liability, and Employers’ Liability—that form the foundation of comprehensive insurance for business consultants uk.

- Learn how to customise your coverage based on your specific consultancy niche, ensuring you address modern risks like Cyber Liability without paying for unnecessary extras.

- Stay ahead of 2026 regulatory shifts, including new Statutory Sick Pay requirements and updated legal duties regarding workplace harassment prevention.

- Understand the specific factors that influence your premium costs, from your annual turnover to the indemnity limits required by high-value client contracts.

- Discover the benefits of working with an independent broker to secure a human-centric, flexible policy that adapts as your business grows.

Essential Insurance for Business Consultants in the UK: Why It Matters

Insurance for business consultants uk is more than just a defensive measure; it’s a strategic asset that safeguards your professional standing. While a traditional retailer might worry about physical stock or property damage, your primary risk lies in the intangible. You sell expertise, strategy, and advice. If a client follows your recommendation and suffers a financial loss, you are the one held accountable. This makes a tailored insurance package the foundation of a stable consultancy business.

The regulatory environment for 2026 has introduced several new pressures for UK firms that make robust cover even more critical. From April 2026, changes to Statutory Sick Pay (SSP) mean payments are now due from the first day of sickness, removing the previous earnings limit. Furthermore, new legislation regarding umbrella company liability and increased duties to prevent workplace harassment mean your administrative and legal risks have grown. Having the right protection in place ensures these shifting rules don’t derail your operations.

Beyond legal safety, insurance acts as a powerful trust signal. In a competitive market, being able to provide an insurance certificate immediately can be the difference between winning a contract or losing it to a rival. It demonstrates that you are a professional who understands risk management and has the financial backing to stand by your work.

The Risk of Professional Advice

Consultants occupy a unique position because their product is intellectual property. There’s a significant difference between “doing” work and “advising” on it. When you provide a report or a strategy, you’re essentially guaranteeing its validity. A single calculation error or a misinterpreted data point can lead to massive financial damages for your client. This is why Professional Indemnity Insurance is so vital for the industry. It covers your legal costs and any compensation payments if a client alleges your advice was flawed. Consider a management consultant whose cost-saving strategy inadvertently causes a client to breach a high-value contract. Without Professional Indemnity Insurance, the legal fees alone could be enough to bankrupt a small consultancy.

Meeting Contractual Obligations

Most UK corporate clients and local authorities won’t even consider signing a contract without seeing proof of cover. In 2026, it’s standard to see requirements for indemnity limits of at least £1 million, while larger firms often demand £5 million or more. High-value contracts frequently include strict clauses regarding Public Liability Insurance to cover any accidental damage or injury during on-site visits. Having these policies ready to go speeds up your onboarding process. It shows you’re prepared and reliable, allowing you to move from the proposal stage to delivery without administrative delays.

The ‘Big Three’ Covers: Professional Indemnity, Public Liability, and Employers’ Liability

While every firm has unique needs, most insurance for business consultants uk packages focus on three primary areas of risk. One is mandated by law, one is almost always required by clients, and the third protects your physical interactions with the world. Understanding the difference between a commercial necessity and a legal obligation is vital for your financial health. If you’re unsure which applies to your current project, you can speak with a specialist to clarify your needs.

Professional Indemnity (PI) Insurance

Professional Indemnity Insurance is the cornerstone of your protection. It’s the primary defense for consultants because it addresses the core of what you do: providing advice. If a client claims your strategy led to a breach of confidentiality or caused them a significant financial loss due to negligence, PI covers the legal fees and any resulting compensation. It’s often a non-negotiable requirement in UK management consultancy contracts. Even if you haven’t made a mistake, the cost of defending a meritless claim can be devastating without this cover in place.

Public Liability (PL) Insurance

While PI covers your advice, Public Liability Insurance covers your physical presence. This policy protects you against claims of third-party injury or property damage. You might think it’s unnecessary if you work from home, but even occasional site visits or hosting a client for coffee carries risk. A spilled drink over a client’s laptop or a trip over a loose cable in your office could lead to a claim. Most corporate sites and local authorities will require proof of PL before allowing you through the doors for a project.

Employers’ Liability (EL) Insurance

Unlike other covers, Employers’ Liability Insurance is a strict legal requirement for Employers’ Liability insurance if you employ at least one person. This includes part-time staff and temporary contractors. The law requires a minimum of £5 million in cover, though most policies provide £10 million as standard. Fines for non-compliance are severe; the Health and Safety Executive (HSE) can charge up to £2,500 for each day you operate without a certificate. Only sole traders and some family-run businesses are exempt from this requirement.

Finally, don’t overlook “Run-off cover” when setting up your insurance for business consultants uk. Professional Indemnity claims can arise years after a project ends. If you plan to retire or change careers, this extension ensures you remain protected against claims relating to past work, providing long-term security for your personal assets and professional reputation.

Beyond the Basics: Tailoring Your Policy to Your Consultancy Niche

A general policy might cover the basics, but it often leaves gaps or charges you for protection you’ll never use. Effective insurance for business consultants uk requires a granular look at your specific daily activities. For example, a marketing consultant needs protection against copyright infringement, while a management consultant focusing on strategy needs robust coverage for financial loss advice. By building a bespoke policy, you ensure every pound of your premium is working to protect a real-world risk rather than subsidising covers irrelevant to your niche.

The rise of digital threats in 2026 has made Cyber Insurance a critical addition for any consultant handling client data. If you manage digital assets or store sensitive information on your local devices, standard professional indemnity might not cover the full cost of a data breach. A dedicated cyber policy helps manage the fallout of a cyber attack, covering notification costs, system restoration, and even legal defense if you’re sued for losing third-party data. It’s a proactive way to maintain client trust even in a crisis.

IT and Tech Consultants

Tech-focused roles carry a heavy burden of responsibility regarding system integrity. If you’re implementing software or managing a cloud migration, a failure can cause immediate operational paralysis for your client. Because of this, professional indemnity limits for tech consultants are typically higher than in other sectors to account for these massive potential losses. You should also consider protecting your physical assets. If you’re frequently travelling to client sites with high-spec laptops or specialised testing equipment, ensuring your physical tools are protected against theft or accidental damage is a pragmatic step that prevents out-of-pocket replacement costs.

HR, Recruitment, and Management Consultants

If your work involves personnel advice or strategic restructuring, your risks are more human-centric. You deal with sensitive employment law and confidential corporate data daily. Claims in this sector often revolve around defamation, breach of confidentiality, or alleged errors in recruitment processes that lead to “wrongful hire” lawsuits. Additionally, the legal landscape for 2026 includes stricter IR35 enforcement and complex tax investigations. Adding “Legal Expenses” cover to your policy provides the financial backing to defend yourself during HMRC disputes or employment tribunals. This is especially vital given the new six-month time limit for tribunal claims introduced in October 2026, which gives disgruntled parties more time to initiate legal action against your business. Securing the right insurance for business consultants uk means accounting for these specific legal timelines.

Calculating the Real Cost of Consultant Insurance in 2026

Finding the right balance between cost and protection starts with understanding how insurers price your specific risk. When you search for insurance for business consultants uk, you’ll notice that premiums aren’t a flat rate. Instead, they reflect your business’s unique profile. Insurers look at the probability of a claim and the potential cost of settling it based on your sector and contract values. It’s a logical process that rewards transparency and a solid professional history.

Don’t fall for the trap of choosing the lowest headline price without checking the fine print. Very cheap policies often lack “any one claim” protection. This means your total indemnity limit might be an aggregate for the whole year, rather than applying to each separate claim. If you face more than one legal challenge in a single policy period, you could find your cover exhausted before the second claim is even heard. A robust policy ensures your limit resets for every new incident.

Factors Influencing Your Premium

Your annual turnover and the size of the contracts you advise on are the biggest influences on your premium. Advising a multinational on a strategy worth millions carries more risk than helping a local small business—such as those featured on Anglia Market—with their social media presence. Your level of experience also matters; insurers view a consultant with a decade of claims-free history as a lower risk than someone just starting out. The sector you consult for changes the math too. High-risk industries like Oil and Gas generally command higher premiums than lower-stakes sectors like Retail due to the potential scale of financial loss if something goes wrong.

Ways to Manage Insurance Costs

One of the best ways to keep costs down is to bundle your Professional Indemnity Insurance and other core covers into a single policy. This is often more efficient than managing multiple separate renewals. You might also consider increasing your voluntary excess. By agreeing to pay a slightly higher amount toward any claim, you can often secure a lower annual premium. However, always make sure you have the funds available to cover that excess at short notice. To see how these factors apply to your specific consultancy, you can get a personalised assessment of your insurance needs today.

Working with an independent broker can also find better value than direct “price-beat” algorithms. Algorithms are rigid and often struggle with the nuances of specialized consulting. A broker understands which insurers have an appetite for your specific niche, often accessing rates that aren’t available on standard comparison sites. This human-centric approach ensures you aren’t paying for cover you don’t need while maintaining the protection your contracts require.

Why an Independent Broker is the Right Choice for Consultants

Many consultants start their search for insurance for business consultants uk on automated comparison sites. While these digital tools are fast, they are often too rigid to understand the nuances of a specialist consultancy. Just Quote Me for a more personalised approach to your protection. We don’t rely on algorithms to decide your level of security. Instead, we rely on 30 years of experience in the UK market to find the right fit for your firm.

Our bespoke process is intentionally straightforward and efficient. We listen to your specific business needs before we even begin searching the market. This personalized approach allows us to identify gaps that a standard online form might miss, such as specific regional risks or unique contract requirements. Our team brings deep local expertise to the table, particularly for businesses across Staffordshire and the West Midlands. We position ourselves as a steady partner who manages the complex administrative burdens so you can focus entirely on client delivery. This local focus ensures you are never just a policy number in a database.

Access to a Wider Panel of Insurers

Independent brokers have access to a panel of specialist insurers that aren’t available to the general public. These insurers often provide more flexible terms for “non-standard” consultancy roles that automated platforms might reject or overcharge. This access is critical for finding comprehensive cover at a fair price if you’re working in a niche sector. In addition, having a broker advocate for you during a complex claim process is a significant advantage. We manage the technical dialogue with the insurer, ensuring your interests are protected and the process moves quickly toward a resolution.

Personalised Risk Assessment

A truly effective policy for insurance for business consultants uk must move beyond the “7-minute quote” template. We conduct a thorough risk assessment to ensure you are covered for the specific professional activities you perform every day. It’s about ensuring your policy stands up to the scrutiny of a high-value contract clause or a legal challenge from a difficult client. As a dedicated Commercial Insurance Broker Staffordshire, we handle the technical fine print and renewal dates on your behalf. This human-centric service ensures you have a reliable expert to call whenever your business circumstances change or you take on a new, high-stakes project. We provide the pragmatic advice you need to sign contracts with total confidence.

Secure Your Professional Future Today

Your expertise is your most valuable asset, but it also creates your biggest professional risks. We’ve explored how the “Big Three” covers protect your advice, your physical presence, and your team. In a shifting 2026 regulatory environment, staying compliant with updated employment laws and contract requirements is no longer optional. It’s a fundamental part of running a successful consultancy. Securing the right insurance for business consultants uk ensures that one administrative error or a single piece of misunderstood advice doesn’t compromise years of hard work.

At Just Quote Me, we provide the human-centric expertise that automated systems simply can’t match. With over 30 years of industry experience and a broad network of top UK insurers, we build policies that fit your specific niche. Our FCA-authorised expert advice gives you the confidence to sign high-value contracts and focus entirely on client delivery. Don’t leave your reputation to chance when you can have a steady hand managing your risks. Partner with us to protect your business today and move forward with total peace of mind.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Frequently Asked Questions

Is professional indemnity insurance mandatory for consultants in the UK?

Professional Indemnity insurance isn’t a legal requirement under UK law, but it is almost always a commercial necessity. Most corporate clients and government bodies will refuse to sign a contract unless you provide proof of cover. It protects you against claims of negligence or errors in your advice. Without it, you are personally liable for legal fees and compensation costs that could easily exceed your business’s total assets.

Can I get insurance as a self-employed freelance consultant?

You can absolutely secure tailored insurance as a self-employed freelancer. In fact, insurance for business consultants uk is specifically designed to scale with your business, whether you’re a limited company or a sole trader. We focus on your specific turnover and the nature of your advice rather than your business structure. This ensures you only pay for the protection you need while meeting the strict insurance clauses found in modern consultancy contracts.

What is the difference between Public Liability and Professional Indemnity?

Public Liability covers physical mishaps, such as a client tripping over your laptop cable or you accidentally damaging property during a site visit. In contrast, Professional Indemnity covers the intellectual side of your work. It protects you if a client suffers a financial loss because of your professional recommendations or a mistake in a report. Both are essential because they cover entirely different types of legal and financial risk.

How much Professional Indemnity cover do I need for a standard contract?

Most UK consultancy contracts require a minimum of £1 million in Professional Indemnity cover, though larger firms often demand £5 million. The specific amount depends on the potential financial impact of your advice. If a mistake in your strategy could cost a client £2 million, a £1 million policy won’t be sufficient. You should always check the insurance clause in your contract before starting work to ensure your limits are compliant.

Does my insurance cover me if I work with international clients?

Standard policies often cover work for international clients, but you must confirm the territorial limits and jurisdiction in your policy. Many UK insurers exclude claims brought in the USA or Canada due to their complex legal systems unless you specifically request an extension. If you’re advising overseas firms, we can help you adjust your policy to ensure your protection follows you across borders, regardless of where the client is based.

What happens if I retire? Do I still need insurance for past advice?

You should maintain run-off cover after you retire or close your consultancy to stay protected. Professional Indemnity insurance for business consultants uk is written on a claims-made basis, meaning the policy must be active when the claim is filed, not just when the work was done. Since a client could sue you years after a project ends, run-off cover ensures you remain protected against legacy claims. This prevents a surprise legal challenge from draining your retirement savings.

Is Employers’ Liability insurance required if I only use subcontractors?

You generally need Employers’ Liability insurance if you use labour-only subcontractors who work under your direct supervision. However, if you hire bona-fide subcontractors who provide their own tools and insurance, it might not be a legal requirement. Because the distinction is often subtle, many consultants maintain EL cover to avoid the Health and Safety Executive’s fine of £2,500 per day. It’s a pragmatic way to ensure total legal compliance as your team fluctuates.

How quickly can I get my insurance certificate after paying?

You will typically receive your insurance certificate via email immediately after your payment is processed. We understand that consultants often need proof of cover to finalise a contract or gain site access at short notice. Our efficient system is designed to provide documentation within minutes, allowing you to move from an inquiry to a fully insured status without any unnecessary administrative delays. This speed ensures you never miss a project deadline.