The cheapest pub and bar insurance policy on the market might actually be your most expensive mistake if the fine print leaves you exposed during a crisis. For UK landlords, the hospitality landscape in 2026 is defined by volatility, from shifting consumer habits to the implementation of new safety legislation. You’re likely feeling the squeeze of rising premiums and the constant worry that your current cover isn’t quite enough to satisfy complex licensing requirements. It’s a frustrating position to be in when you’re trying to focus on your trade.

We believe that your coverage should be a bespoke safety net, not a generic box-ticking exercise. This guide simplifies the process of protecting your livelihood by breaking down the essential components of a robust policy. We will preview the core legal mandates, specialist add-ons like loss of license cover, and practical ways to reduce your premium through better risk management. At Just Quote Me, we offer the personal touch of a local broker combined with thirty years of industry expertise to do the heavy lifting for you.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Key Takeaways

Understand why standard business policies often exclude late-night risks and how specialized pub and bar insurance provides the specific protection your licensed premises needs.

Learn the essential legal requirements for Employers’ Liability to ensure your business remains compliant and avoids severe penalties.

Explore specialist add-ons like Loss of License and Business Interruption cover that protect your income and the long-term value of your venue.

Gain insight into the variables that dictate your premium, including your venue’s location, opening hours, and the type of entertainment you provide.

Discover the advantage of working with a specialist broker to access bespoke rates and personalized support tailored to the UK hospitality trade.

What is Pub and Bar Insurance and Why is it Essential in 2026?

Pub and bar insurance is a specialized collection of covers designed to protect the specific operational risks of the hospitality trade. While a general business policy might cover basic fire and theft, it often lacks the depth required for licensed premises. In 2026, the complexity of running a bar has evolved. You aren’t just selling drinks; you’re managing a high-traffic environment where alcohol consumption and late-night hours create unique liabilities. A standard policy might fail to cover incidents involving glass-related injuries or noise-related disputes with local authorities, leaving your livelihood exposed to significant financial risk. Investing in dedicated pub and bar insurance ensures that these industry-specific challenges are fully managed.

The 2026 economic climate has made specific coverage even more critical. Inflation has driven up the cost of replacement furniture and professional kitchen equipment by over 12% in the last year alone. If your sums insured haven’t been updated to reflect these 2026 valuations, you could face the “average clause” during a claim, where your payout is reduced because you were underinsured. This is why a tailored approach is necessary. An independent broker helps you navigate these rising costs by finding underwriters who specialize in hospitality, ensuring your protection keeps pace with current market values.

Legal Requirements vs. Recommended Protection

It is vital to distinguish between what the law demands and what your business actually needs to survive. The Licensing Act 2003 remains the cornerstone of your operational obligations, requiring you to maintain a safe environment for both staff and patrons. While employers liability insurance is a strict legal mandate for any pub with employees, other covers like public liability insurance are often contractual requirements set by your landlord or mortgage provider. Understanding the history of pubs shows how these establishments have transitioned from simple alehouses to complex community assets, each with its own set of modern liabilities that “basic” cover simply cannot address.

The Human Element: Why Brokers Beat Algorithms

The rise of automated quote generators has led many landlords toward one-size-fits-all policies that ignore the nuances of their specific venue. A chatbot won’t notice that your beer garden has an unfenced water feature or that your basement cellar has a particularly steep staircase. At Just Quote Me, we rely on 30 years of experience to spot these hidden risks before they become claims. We take a straightforward, no-nonsense approach to securing your cover, acting as a human-centric alternative to faceless algorithms. We do the heavy lifting to ensure your bar’s layout and unique services are fully accounted for in your premium.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

The Core Components of a Robust Pub Insurance Policy

Building a solid foundation for your pub and bar insurance requires a look at four specific pillars of protection. It’s not just about meeting the bare minimum; it’s about anticipating the unique chaos that comes with the hospitality trade. A robust policy ensures that if a pipe bursts behind the bar or a customer suffers an injury, your business doesn’t have to foot the bill alone. While every venue is different, the following components form the essential core of any professional insurance package in 2026.

Deep Dive into Public Liability for Pubs

Dealing with the public means dealing with the unpredictable. Public liability insurance is your primary defense against claims of injury or property damage made by third parties. Think of a customer slipping on a spilled drink in a crowded beer garden or a patron being injured by broken glass during a busy Friday night set. These aren’t just hypothetical risks. In 2026, high-traffic city centre bars are increasingly moving toward £10 million limits to account for rising legal costs and high-value settlements. You can find more specific details on our Public Liability Insurance page to see how we tailor these limits to your footfall.

Employers’ Liability: Protecting Your Team

If you employ anyone, you’re legally bound by UK law to have at least £5 million in cover. This isn’t optional. It applies whether you have a full-time kitchen crew, seasonal glass collectors, or contracted door security. The penalty for failing to have this cover is a fine of £2,500 for every day you’re uninsured. A comprehensive policy covers your entire team under one roof, providing peace of mind that you’re protected if a staff member is injured while handling heavy kegs or working in a high-pressure kitchen. Our Employers’ Liability Insurance options are designed to scale with your staff numbers throughout the year.

Beyond these liabilities, you must safeguard your physical assets. Buildings and contents insurance protects the structure of your pub and the expensive equipment inside, from high-end sound systems to industrial glass washers. If you’re a gastropub or serve any food, product liability is also essential. This protects you if a customer falls ill from a meal or drink served on your premises. If you’re unsure which limits are right for your specific venue, you can speak to our team for a tailored review of your current risks.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Specialist Add-ons: Tailoring Cover to Your Venue’s Needs

While core coverages protect the basics, your pub and bar insurance needs to reflect the reality of operating in 2026. This means looking beyond the building and the staff to the very things that make your business profitable. For example, stock insurance isn’t just about bottles on a shelf. It covers the thousands of pounds worth of draught beer in your cellar and perishable food in your kitchen. If a refrigeration unit fails overnight, you could lose your entire weekend’s inventory. We ensure these specific trigger points are clearly defined in your policy so that a equipment failure doesn’t become a financial disaster.

A critical update for 2026 is the full implementation of Martyn’s Law, also known as the Protect Duty. This legislation requires venues to have robust public safety and counter-terrorism plans in place. Your insurance must align with these new responsibilities. We help you ensure that your liability coverage accounts for these 2026 requirements, protecting you from potential negligence claims related to security protocols. It is a specialized area that many generic providers have not yet addressed, leaving landlords exposed to significant legal risks.

Loss of License and Revenue Protection

If your premises license is revoked or suspended, the value of your business could plummet overnight. Loss of license insurance provides a financial cushion, covering the depreciation in your property’s value or lost profits during the appeal process. This works alongside business interruption cover, which keeps your cash flow steady if a fire or flood forces you to close for repairs. While commercial property insurance covers the physical structure, business interruption covers the lifeblood of your trade. It ensures you can still meet your financial obligations even when your doors are closed.

Covering Specific Risks: From Thatched Roofs to Nightclubs

Certain venues carry a high risk label that scares off standard insurers. If you run a historic building, you will need specialized thatched pub insurance to account for the unique fire risks and specialist repair costs associated with traditional materials. Similarly, nightclub insurance requires a different approach to security and late-night liability than a quiet village inn. We also ensure you meet mandatory requirements like Employers’ Liability (EL) insurance, which is a legal must-have for any venue with a team. Whether you host live DJ sets or operate a thatched gastropub, we find the right underwriters for your specific niche.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Calculating the Real Cost: What Influences Your Premium?

Pricing for pub and bar insurance isn’t a “one-size-fits-all” calculation. Underwriters look at a wide range of variables to determine your risk profile, meaning two venues on the same street could pay vastly different amounts. Location is perhaps the most significant factor. A quiet village pub might see annual premiums between £600 and £900, while a busy urban bar in a city centre could pay £1,200 to £2,000 or more. If you require a full package including commercial buildings insurance, the average starting cost in the UK is now over £4,400 per year. Insurers aren’t just looking at your postcode; they’re looking at local crime rates and how quickly emergency services can reach your door.

Your operating model also dictates the price. A venue with a 24-hour license or one that hosts regular live DJ sets and “experiential socializing” activities will naturally face higher costs than a traditional alehouse. These features increase the statistical likelihood of a public liability claim. Security measures like industry-approved fire suppression systems and high-definition CCTV can help mitigate these hikes, as they provide concrete evidence of your commitment to risk management.

Risk Management Strategies to Lower Premiums

You can actively make your bar more “insurable” by documenting your safety protocols. Underwriters value proof over promises. Keeping detailed staff training records and incident logs shows that you have a professional handle on your operations. This documentation is vital for defending against liability claims, which we previously noted can average £13,500 per settlement. Another practical tip is to review your voluntary excess. While a “cheap” policy with a high excess might look attractive on a monthly statement, it can leave you dangerously out of pocket when a freak accident occurs. Striking the right balance between a manageable premium and a realistic excess is key to long-term financial health.

The 2026 Hospitality Squeeze

In 2026, the hospitality sector is facing a unique squeeze. Asset values for kitchen equipment and building materials have risen sharply, meaning policies from even two years ago might now leave you underinsured. If your sum insured doesn’t reflect 2026 replacement costs, you won’t receive the full value of a claim. We recommend a specialist broker review to ensure your limits are accurate and to strip out any policy “fluff” you don’t actually need. For landlords managing mixed-use venues, our 2026 Restaurant and Takeaway Insurance Checklist offers a great benchmark for protecting diverse hospitality assets. If you operate accommodation alongside your bar, our guide to hotel and guest house insurance is equally valuable for understanding how shifting property markets and rising liquor liability costs affect your overall coverage needs.

If you want to ensure your coverage is accurate for today’s market, you should get a bespoke premium review from our hospitality specialists today.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Securing Your Future with Just Quote Me

Just Quote Me isn’t just another name in an insurance directory. We bring over 30 years of experience in the UK insurance brokerage market to every conversation. This longevity gives us a deep understanding of the hospitality sector’s volatility, especially as we move through 2026. Unlike automated platforms that treat every pub like a series of data points, we recognize that your business is a unique operation. We access a broad network of underwriters to find bespoke hospitality rates that reflect your actual risk, not just a generic postcode average. We don’t rely on faceless algorithms; we rely on established relationships and industry expertise.

Dealing with a claim is often the most stressful part of being a landlord. When things go wrong, you don’t want to talk to a chatbot or navigate a complex phone menu. Our approach is built on the personal touch. You deal with a human expert who understands the nuances of the trade. We offer simplified claims support, doing the heavy lifting so you can focus on getting your doors back open. This steady hand is what differentiates a specialist broker from a generalist aggregator. We’re here to ensure that your pub and bar insurance actually delivers when you need it most.

A Bespoke Approach to Pub Insurance

We don’t just provide a number. We consult with you to ensure your specific risks are fully covered, from your historic building’s quirks to your modern security protocols. While some providers might offer generic Shop Insurance, a pub requires a much more intricate level of protection. Our commitment to the Staffordshire and West Midlands hospitality community means we’re local enough to care but established enough to provide the authority you need. We understand the local landscape and the specific challenges facing venues in this region.

Next Steps for Your Pub or Bar

Our quoting process is designed to be efficient and no-nonsense. We know your time is spent managing stock and serving customers, not filling out endless forms. By choosing a partner who understands the 2026 hospitality landscape, you’re securing the future of your livelihood against the unpredictable. Whether you’re a small village local or a high-volume city centre bar, the right advice is just a conversation away. Protecting your staff, your customers, and your reputation starts with a policy that fits.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Future-Proof Your Licensed Premises Today

Running a pub in 2026 means balancing community tradition with increasingly complex legal and financial risks. We’ve explored how a robust policy protects you from expensive liability claims and ensures you meet the latest safety legislation like Martyn’s Law. Securing the right pub and bar insurance means your livelihood is protected against both everyday accidents and major business interruptions that could otherwise end your trade. It’s about having a safety net that reflects the true value of your assets and staff in today’s economy.

As an FCA-authorised independent broker with 30+ years of industry experience, Just Quote Me provides bespoke cover from top UK insurers. We strip away the policy fluff so you can focus on your patrons and your team. You don’t have to navigate these shifting regulations alone. Our specialists are ready to provide the human expertise that automated algorithms simply can’t replicate. It’s time to protect your hospitality business with a partner who understands the UK trade. We look forward to helping you stay open and successful for years to come.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Frequently Asked Questions

Is pub insurance a legal requirement in the UK?

Employers’ Liability insurance is a strict legal requirement in the UK if you employ anyone, including part-time or seasonal staff. Failing to have at least £5 million in cover can result in daily fines of £2,500. While other forms of pub and bar insurance like public liability or buildings cover aren’t mandated by law, they are almost always required by your mortgage provider or commercial landlord to protect their financial interests.

Does bar insurance cover me for live music and DJs?

Most standard policies can include cover for live music and DJs, but you must disclose these specific activities to your broker. Entertainment increases your risk profile because of higher noise levels and potential crowd incidents. We ensure your policy specifically accounts for these events, protecting you against claims related to equipment failure or accidents that basic policies might exclude. This clarity prevents claim rejection during busy weekend sets.

What happens if a customer gets food poisoning at my gastropub?

If a customer falls ill after eating at your venue, your product liability insurance handles the legal costs and any resulting compensation. This protection is essential for any gastropub or bar serving food. It shields your business from the financial fallout of accidental contamination or allergic reactions, provided you have maintained accurate health and safety records. It is a vital safety net for your reputation and cash flow.

Can I get insurance for a pub with a thatched roof?

You can certainly get insurance for a thatched property, but it requires a specialist underwriter who understands the unique fire risks. Standard insurers often avoid these historic buildings because of the specialized rebuilding costs. We use our network to find providers who offer dedicated thatched pub insurance, ensuring you have the right protection for traditional materials and specialist repairs that modern policies won’t cover.

Does my policy cover cash stolen from the premises?

Yes, “money cover” is a common add-on that protects your cash while it is on the premises, in a safe, or in transit to the bank. Most policies have specific limits for cash kept overnight, and insurers often require an approved safe for higher amounts. We help you set these limits based on your typical weekend takings so you aren’t left out of pocket if a theft occurs during your operations.

What is the difference between public and product liability for bars?

Public liability covers injuries or property damage caused by your business operations, such as a customer slipping on a wet floor. Product liability specifically covers illness or injury caused by the items you sell, like a contaminated drink or a faulty glass. Both are critical components of pub and bar insurance, as they address different types of third-party claims that can arise during a normal shift.

How much does pub insurance cost on average in 2026?

In 2026, basic quotes start from £53.26 per month for policies including employers’ and public liability. However, the average cost for a full package including buildings insurance is over £4,400 per year. Your specific premium depends on your venue’s location, turnover, and claims history. We recommend a personalized review to find a rate that fits your unique risk profile while ensuring you aren’t paying for unnecessary policy fluff.

Will Martyn’s Law affect my bar insurance requirements?

Martyn’s Law, also known as the Protect Duty, impacts your insurance by requiring more robust public safety and counter-terrorism measures. Insurers in 2026 now look for evidence of these security protocols when assessing your liability risk. We work with you to ensure your policy aligns with these new legislative requirements, preventing potential gaps in cover that could arise from non-compliance with these important 2026 safety standards.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Article by

Just Quote Me

JustQuoteMe Ltd is an independent UK insurance brokerage specialising in business and personal insurance solutions. With over 35 years of industry experience, the company provides tailored insurance cover for businesses, landlords, tradespeople, hospitality venues, fleets, and individuals across the UK. Known for its personal service, expert advice, and competitive premiums, JustQuoteMe Ltd works with leading insurers to deliver bespoke policies designed around each client’s unique needs. The company is authorised and regulated by the Financial Conduct Authority (FCA No. 586607) and has built a reputation for trusted, straightforward insurance guidance and long-term client relationships.

The lowest quote on a comparison site feels like a win until a £5 million claim arrives and you discover a hidden exclusion. It’s a common worry for UK business owners in 2026, especially as you try to balance rising operational costs with the need for robust protection. You want cheap public liability insurance, but you don’t want to gamble with your livelihood. We understand that the average small business premium now sits between £115 and £155 per year. While the market is currently softening, securing a deal that satisfies both your budget and your clients requires a tactical approach.

This article explains how to drive down your insurance costs without stripping away essential cover. We will explore how to leverage current market trends and avoid the jargon that leads to rejected claims. You will learn how to secure a policy that offers genuine peace of mind at a price that makes sense for your bottom line.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Key Takeaways

Learn why public liability is a vital commercial requirement for securing contracts, even when it isn’t legally mandated.

Understand how your specific trade and annual turnover levels directly dictate the premium you pay.

Discover how to secure cheap public liability insurance by bundling policies and demonstrating proactive risk management to insurers.

Identify the hidden traps in budget policies, such as high excesses, that can leave your business financially exposed during a claim.

Find out why using an independent broker provides access to exclusive markets and tailored cover that comparison sites often miss.

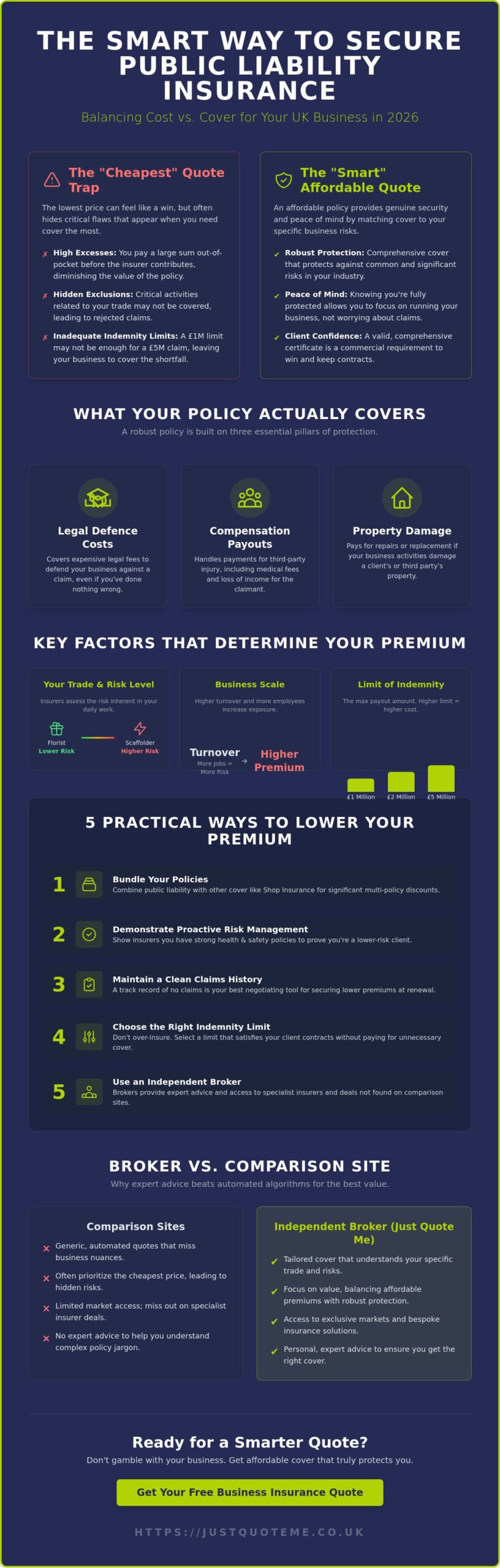

What is Public Liability Insurance and Why is Cost Rising?

Public liability insurance serves as a financial safety net for your business. It steps in if a client, delivery driver, or passerby suffers an injury or property damage due to your business activities. While it’s not a legal requirement in the UK, most clients will refuse to let you on-site without a valid certificate. To get a better grasp of the legalities, you can read about what is public liability and how it relates to civil law. In 2026, the search for cheap public liability insurance has intensified as businesses face a complex economic environment.

The cost of cover is shifting. While some sectors saw premium reductions of 11% to 20% at the end of 2025, other areas are under pressure. Rising costs for building materials and specialist labour mean that property damage claims are more expensive to settle than they were two years ago. When repair costs go up, insurers eventually pass those expenses on to the policyholder. This makes it crucial to distinguish between a “cheap” policy that cuts corners and an “affordable” policy that provides genuine security.

The Core Components of a Public Liability Policy

A robust policy is built on three pillars. First, it covers legal defence costs. Even if you’ve done nothing wrong, defending a claim in court is expensive. Second, it handles compensation payouts, which include medical fees and loss of income for the claimant. Finally, it covers property damage. Whether you’re a cleaner who accidentally ruins a carpet or a builder involved in a major structural mishap, these costs can easily reach six figures without insurance.

Why Businesses are Desperate for Lower Premiums in 2026

Small business overheads are under more scrutiny than ever. With the UK insurance market projected to reach $836.5 billion by 2033, the industry is growing, but so are the risks. AI integration and cyber threats are adding new layers of complexity to standard business operations. Many owners look for cheap public liability insurance to keep their margins healthy. Just Quote Me helps by cutting through the noise of automated algorithms. We find bespoke solutions that fit your specific trade, ensuring you don’t pay for cover you don’t need. You can find more details on our public liability insurance service page.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Factors That Determine the Price of Your Insurance Quote

Insurers don’t pick numbers out of a hat. They use complex actuarial data to decide your premium, and your trade is often the most significant factor. A florist working in a controlled environment faces far lower risks than a scaffolder working at height. If your work involves dangerous equipment, heat, or high altitudes, the insurer expects a higher likelihood of a significant claim. This is where finding cheap public liability insurance becomes a balancing act between the lowest price and the specialist expertise required for your specific industry.

Your business scale also dictates the cost. A firm with a £50,000 turnover has fewer interactions with the public than one turning over £5 million. More jobs mean more opportunities for an accident to occur. Similarly, your employee count changes the risk profile. While you might be looking for a basic policy, having more staff often correlates with a higher volume of work and increased public liability exposure. A clean claims history is your best tool for negotiation. If you’ve operated for five years without a single incident, you’re in a much stronger position to secure a discount. This track record highlights the role of liability insurance in your broader asset protection strategy. It isn’t just an overhead; it’s a shield for your business capital.

Location and Territorial Limits

Where you work changes what you pay. Rates in London are often higher due to increased legal costs and higher settlement values. However, if you’re based in the West Midlands or Staffordshire, you might find more competitive local rates. Working on-site at various locations is generally riskier than working from a fixed base. For those with a permanent physical presence, dedicated Shop Insurance often provides a more cost-effective way to bundle public liability with other essential covers. You should speak with a broker to ensure your territorial limits actually cover where you work.

The Limit of Indemnity: £1m, £2m, or £5m?

The limit of indemnity is the maximum amount the insurer will pay for a single claim. While a £1 million limit might seem like enough, it’s often the bare minimum. Most public sector contracts and local authority projects require a minimum of £5 million in cover. Choosing a lower limit might help you find cheap public liability insurance today, but it could cost you a lucrative contract tomorrow. We often find that the price difference between £2 million and £5 million of cover is surprisingly small, making the higher limit a better long-term value.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

The Hidden Risks of Choosing the Cheapest Policy

“I just need the certificate to get on-site.” It’s a phrase we hear often from contractors looking for cheap public liability insurance. While getting the paperwork sorted is necessary for access, viewing insurance as a mere box-ticking exercise is a dangerous gamble. If a policy is priced significantly below the market average of £115 to £155, the insurer has likely stripped away essential protections or inflated the excess to an unmanageable level. You might save a few pounds today, but the long term cost of an inadequate policy can be devastating.

A high policy excess is one of the most common traps. You might save £20 on your annual premium, but if the policy carries a £500 or £1,000 excess, you’ll be paying out of pocket for minor accidents that a better policy would have covered in full. When you consider the factors that determine insurance price, remember that the lowest upfront cost often hides the highest eventual liability. There’s also the risk of “unrated” insurers. These companies aren’t backed by the same financial guarantees as established UK providers, meaning they could potentially fold before your claim is settled, leaving you to face the legal costs alone.

Common Exclusions in Budget Public Liability Policies

Budget policies are often riddled with narrow definitions that leave builders or tradesmen vulnerable. For example, many low-cost options include strict height and depth restrictions. If your policy limits work to 2 metres and you’re working on a 3-metre scaffold, your cover is effectively void. Similarly, the use of heat is a major sticking point. “Cheap” policies frequently exclude welding, soldering, or blowtorch work unless you pay an additional premium. For comprehensive protection that covers the full scope of a project, a Contractors All Risk Insurance policy might be a more appropriate investment than a basic liability certificate.

Cheap vs. Comprehensive: A Comparison

Imagine a “bare bones” policy costing £10 per month versus a bespoke policy at £15 per month. That extra £5 usually buys you lower excesses, higher indemnity limits, and fewer exclusions. For consultants or service-based firms, it also provides the opportunity to bundle essential add-ons. Combining your liability with Professional Indemnity Insurance ensures that both physical accidents and professional errors are covered. If your business sells or distributes physical goods, it’s equally important to understand where your public liability ends and your product liability insurance begins, as budget policies rarely make this distinction clear. Investing in cheap public liability insurance is only a success if the policy actually pays out when you need it most.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

5 Practical Ways to Secure Cheap Public Liability Insurance

Securing a competitive rate doesn’t mean you have to settle for inferior cover. By taking a proactive approach to how you present your business to underwriters, you can unlock discounts that automated systems often overlook. There’s power in being a well-prepared applicant. Here are five practical methods to reduce your premiums while maintaining the high level of protection your business deserves.

Optimise your trade description: Be specific about what you do. If you’re listed as a general contractor but only perform domestic decorating, you’re likely paying a premium for risks you don’t actually face.

Bundle your insurance: Combining different types of cover is one of the most effective ways to find cheap public liability insurance. For instance, if you have any staff, you’re legally required to have employers liability insurance. Purchasing these together usually results in a lower total cost than buying them separately.

Pay the full amount annually: Monthly direct debits often come with interest rates that can add 10% to 15% to your total bill. Paying upfront eliminates these finance charges and simplifies your accounting.

Demonstrate risk management: Show the insurer you’re a safe bet through documented procedures and safety accreditations.

Adjust your voluntary excess: Taking on a slightly higher portion of the initial claim cost can significantly lower your ongoing premium.

Risk Assessments and Safety Accreditations

Insurers look for evidence that you take safety seriously. Memberships in trade bodies or holding safety accreditations signal to an underwriter that you’re a low-risk prospect. A risk assessment is a proactive tool that proves business competence to an insurer. By keeping these documents updated and available, you’re in a much better position to negotiate. If you haven’t reviewed your safety protocols lately, you should get a specialist quote to see how your improved standards affect your rate.

Adjusting Your Voluntary Excess

The relationship between your excess and your premium is a simple mathematical trade-off. By increasing your voluntary excess from £250 to £500, you reduce the insurer’s potential payout on small claims, which they reward with a lower premium. However, you must find a “sweet spot” where the savings are meaningful but the excess remains affordable if you need to claim. This is particularly relevant in high-risk sectors; for example, firms seeking Security Insurance often use higher excesses to manage the costs of specialized liability cover. Always ensure you have the funds set aside to cover the excess at a moment’s notice.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Why an Independent Broker Beats a Comparison Site for Price

Comparison sites offer speed, but they often sacrifice the depth required for complex business risks. While they might show a low price, they rarely provide the context needed to ensure your cover is actually valid. Just Quote Me has spent over 30 years building a reputation with a panel of top-tier UK insurers. This longevity gives us access to “Broker-Only” markets. These are specialist insurers who avoid comparison platforms to focus on businesses that require a more considered approach. By tapping into these exclusive markets, we often secure cheap public liability insurance that isn’t available to the general public.

Bespoke policy tailoring is where a human advisor truly adds value. Instead of a generic package that might include irrelevant add-ons, we strip away the excess. You only pay for the specific protection your business requires. Whether you’re a tradesman or a professional consultant, we ensure your policy reflects your actual turnover and activities. Having a broker on your side during a claim also provides a level of advocacy that a faceless call centre cannot match. We act as your voice, dealing with the insurer so you don’t have to navigate the stress of a claim alone.

Faceless Algorithms vs. Expert Advice

Automated systems are binary; they often flag businesses as “high risk” based on a single keyword or postcode. This can lead to inflated premiums or outright rejections for perfectly safe operations. As a local specialist in Staffordshire and the West Midlands, we understand the local business landscape. We can speak directly to underwriters to explain your safety protocols and specific risk profile. This human intervention often results in a fairer price and more robust cover than any algorithm can provide.

Ready to Lower Your Business Insurance Costs?

The transition from searching for “cheap” insurance to finding “smart” insurance is about value. It’s about knowing your business is safe without overpaying for the privilege. We’ve helped thousands of UK businesses navigate the complexities of the 2026 market with honesty and efficiency. By choosing a partner who understands your trade, you gain both competitive rates and the peace of mind that your policy will perform when you need it most.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Secure Your Business Future Today

Securing cheap public liability insurance doesn’t have to be a race to the bottom that leaves your assets exposed. By focusing on proactive risk management and choosing the right indemnity limits for your specific trade, you can protect your livelihood without overspending. We’ve explored how avoiding the hidden traps of budget policies and opting for bespoke tailoring ensures that your cover remains valid when it matters most. As an FCA-authorised independent broker with over 30 years of UK industry experience, Just Quote Me provides the specialist knowledge that automated algorithms lack. We leverage our access to a top-tier panel of UK insurers to find competitive rates that generic sites often miss.

Don’t leave your business protection to chance. Whether you need to meet a £5 million contract requirement or simply want a more efficient way to manage your overheads, we’re here to help. You can start your journey to better cover by speaking with our team today. We look forward to helping your business thrive with the right protection in place.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Frequently Asked Questions

Is the cheapest public liability insurance always the best option?

No, the lowest price rarely guarantees the best protection. While you might save money on your monthly premium, budget policies often feature high excesses of £500 or more and narrow exclusions that could leave you footing the bill for a claim. It’s vital to ensure the policy actually covers your specific trade activities before committing to the cost.

How can I get cheap public liability insurance as a sole trader?

The most effective way for a sole trader to secure cheap public liability insurance is to pay your premium annually and provide a precise trade description. Avoiding monthly interest charges and ensuring you aren’t rated for high-risk activities you don’t perform can lead to significant savings. Bundling your liability with other covers, such as tools or professional indemnity, also typically reduces the total cost.

Will my premium go down if I have a health and safety policy?

Yes, insurers often view businesses with documented health and safety policies as lower-risk prospects. By proving you have proactive risk management in place, you give underwriters the confidence to offer more competitive rates. Documented risk assessments and safety accreditations serve as tangible proof of your business competence and can lead to lower annual premiums.

Can I change my public liability cover mid-year to save money?

You can switch providers at any time, but you should check for cancellation fees in your current contract first. If you find a significantly better rate elsewhere, the savings might outweigh the exit costs. However, it’s usually most efficient to review your options 30 days before your renewal date to avoid administrative penalties and gaps in cover.

What is the average cost of public liability insurance in the UK for 2026?

As of March 23, 2026, the average annual cost for small businesses in the UK typically falls between £115 and £155. While some low-risk businesses can find cover from around £50 per year, high-risk trades or those with large turnovers may pay £500 or more. Your specific premium depends on your claims history and the level of indemnity you choose.

Does “cheap” insurance cover me for working on larger construction sites?

Budget policies often include restrictive clauses that prevent work on major construction sites or at specific heights. Many low-cost certificates are designed for domestic work and exclude high-risk environments. You must verify that your policy meets the specific contractual requirements of the site manager, which often include a minimum of £5 million in cover.

Why is my public liability quote so high compared to last year?

Rising labour and material costs have increased the average value of property damage claims throughout 2025 and into 2026. If your business turnover has increased or you’ve moved into a higher-risk postcode, insurers will adjust your premium accordingly. Even without a claim, industry-wide inflation means insurers must increase rates to remain solvent and meet FCA requirements.

How does an independent broker find cheaper rates than a comparison site?

Brokers have access to specialist “broker-only” markets that are not available on public comparison tools. Instead of relying on a generic algorithm, a broker manually negotiates with underwriters to find cheap public liability insurance that is tailored to your specific risks. This personal touch ensures you don’t pay for unnecessary add-ons that automated systems often include by default.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Article by

Just Quote Me

JustQuoteMe Ltd is an independent UK insurance brokerage specialising in business and personal insurance solutions. With over 35 years of industry experience, the company provides tailored insurance cover for businesses, landlords, tradespeople, hospitality venues, fleets, and individuals across the UK. Known for its personal service, expert advice, and competitive premiums, JustQuoteMe Ltd works with leading insurers to deliver bespoke policies designed around each client’s unique needs. The company is authorised and regulated by the Financial Conduct Authority (FCA No. 586607) and has built a reputation for trusted, straightforward insurance guidance and long-term client relationships.

Did you know that motor trade insurance premiums rose by as much as 15% during 2025? It’s a frustrating reality for many in the industry, especially while adapting to the ZEV mandate that requires 52% of new car sales to be zero-emission by the end of 2026. You probably feel that finding affordable motor trade insurance has become a moving target, particularly with the fuel duty freeze finally ending in September 2026.

We agree that the paperwork and rising costs can feel overwhelming. This guide from Just Quote Me promises to help you master the complexities of modern coverage, ensuring you stay legal without overpaying for protection you don’t need. We’ll preview the essential policy types for 2026, clarify your Motor Insurance Database (MID) obligations, and show you how a specialist broker can secure a bespoke deal that covers everything from your premises to your customers’ vehicles. Whether you’re a full-time dealer or a part-time trader, we’ll help you find the right balance of value and protection.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Key Takeaways

Learn why standard insurance falls short and how to correctly identify the legal cover required for handling customer vehicles.

Understand the critical differences between Road Risks and Combined policies to protect your premises, tools, and stock-in-trade.

Discover how to reduce your motor trade insurance costs through proven security enhancements and specialist risk assessments.

Master the nuances of trade-specific coverage, ensuring your MOT centre or dealership has the right internal risks and demonstration cover.

Realise the value of human-centric brokerage in securing a bespoke policy that automated algorithms often overlook.

What is Motor Trade Insurance and Who Requires it in 2026?

Motor trade insurance is the essential legal and financial framework for any UK business handling third-party vehicles. This specialist policy is designed for businesses that handle, repair, or sell vehicles as their primary source of income. While a standard car insurance policy protects a specific vehicle owned by an individual, motor trade insurance covers the trader while they are in control of various vehicles that they don’t necessarily own. Without this specific protection, you’re not just risking your livelihood; you’re operating outside the law.

The necessity for this cover extends across the entire automotive sector. Whether you’re running a high-volume dealership in Birmingham or operating as a mobile valeter in a rural village, you need a policy that reflects your daily risks. Standard business car insurance is insufficient because it typically excludes the “carriage of goods for hire and reward” or the professional handling of customer property. If a vehicle is damaged while under your care for a service, or if you’re involved in an accident during a diagnostic road test, only a dedicated trade policy provides the necessary safety net.

The Legal Requirement: Road Risks vs. Private Use

Under the Road Traffic Act, every driver on UK roads must have a minimum of third-party insurance. For motor traders, this is achieved through Road Risks cover. This allows you and your named employees to drive any vehicle for business purposes. It’s a common misconception that these policies allow for unlimited private use. In 2026, insurers are increasingly strict; “any driver” clauses are almost always restricted to business activities unless you’ve specifically paid for a social, domestic, and pleasure extension.

Accuracy on the Motor Insurance Database (MID) is more critical than ever. With the 5.9% increase in new car registrations seen in early 2026, the volume of vehicles moving through the trade is high. You must update the MID immediately when stock arrives or leaves your possession. Failure to do so can lead to vehicle seizures and heavy fines, as police ANPR systems now sync with the MID in real-time.

Full-Time vs. Part-Time Motor Traders

The UK insurance market doesn’t just cater to large showrooms. Many individuals operate on a part-time basis, perhaps flipping two or three cars a month or offering weekend mechanical repairs. Insurers typically define “trading” based on your intent to make a profit. If you’re buying and selling for gain, you’re a trader in the eyes of the law.

Hobbyists often fall into the trap of thinking they don’t need professional protection. However, a single mistake during a repair can lead to a massive claim. This is where Liability insurance becomes a non-negotiable asset. For mobile operators, combining road risks with public liability insurance ensures that you’re protected if you accidentally damage a customer’s driveway or if a third party is injured due to your work. Don’t leave your personal assets exposed by assuming you’re too small to need professional cover.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Deconstructing Coverage: Road Risks, Liability, and Combined Policies

Understanding the different layers of motor trade insurance is the only way to ensure your business isn’t left exposed. Most traders start with Road Risks, but as your operation grows to include a workshop or showroom, your insurance needs to evolve. A Combined Policy acts as a comprehensive shield for businesses with a physical footprint, merging your road activities with the protection of your premises and assets.

Understanding Road Risks Levels

Road Risks cover is the foundation of any policy. It allows you to drive vehicles for business purposes, ensuring you meet the legal requirement for vehicle insurance on UK roads. There are three primary levels to consider:

Third-Party Only: This is the bare minimum. It covers damage or injury to others but offers zero protection for the vehicle you’re driving.

Third-Party, Fire and Theft: This adds a layer of safety for your business assets, covering vehicles in your care against fire damage or theft.

Comprehensive: This is the gold standard. It covers damage to the vehicle you are driving, regardless of fault, which is vital when handling high-value customer cars.

The Role of Liability Insurance in the Motor Trade

While Road Risks protect you on the move, liability cover protects you when the vehicle is stationary. Public Liability is essential if customers visit your site, as it covers claims for slips, trips, or accidental damage to their property. However, many traders overlook Service Indemnity. This specific cover protects your business against claims of faulty workmanship or the failure of parts you’ve fitted. If a brake repair fails a week later, Service Indemnity is what stands between you and a massive legal bill.

If you employ anyone, even on a casual or part-time basis, employers liability insurance is a strict legal requirement. Failing to have this in place can result in fines of up to £2,500 for every day you’re uninsured. It’s often easier to speak with an independent broker to bundle these covers into a single, manageable policy.

Combined Motor Trade Insurance: The Premises Shield

For those with a garage, MOT centre, or dealership, a Road Risks policy isn’t enough. A Combined Policy brings everything under one roof. It protects your building, your expensive diagnostic tools, and your stock-in-trade. In 2026, with the cost of parts and specialist EV tools rising, the “Combined” approach ensures that a fire or break-in at your premises doesn’t end your business. It bridges the gap between the road and the workshop, providing a seamless safety net that separate modules often miss.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Tailoring Cover to Your Specific Automotive Trade

A one-size-fits-all approach doesn’t work for motor trade insurance because no two businesses operate the same way. A mobile valeter working on a private driveway faces entirely different hazards than a dealer with a multi-million pound showroom. Tailoring your policy ensures you aren’t paying for “demonstration cover” if you only do repairs, or “internal risks” if you don’t have a physical workshop. Getting the details right prevents expensive gaps in your protection that only become apparent when you try to make a claim.

Insurance for Car Dealers and Showrooms

Dealerships manage high-value assets that fluctuate constantly throughout the year. With 614,854 new cars registered in the UK during the first three months of 2026, keeping track of stock-in-trade values is a full-time job. Your policy needs to reflect these changes, especially with the “Luxury Car Tax” threshold for zero-emission vehicles increasing to £50,000 on April 1, 2026. Most dealers also require “unaccompanied demonstration” cover. This allows potential buyers to test drive vehicles alone, which is now a standard expectation in the sales process. For those with high-street premises, integrating commercial property insurance protects your building and glass against accidental damage or vandalism.

Specialist Cover for Mechanics and Bodyshops

Workshop owners deal with unique hazards every day. Beyond the customer vehicles, your diagnostic equipment and hand tools represent a massive financial investment. If your workshop handles large-scale refurbishments or structural work, contractors all risk insurance provides essential protection for ongoing projects. The backbone of your garage insurance remains service and repair indemnity. It covers you if a vehicle is returned because a repair was handled incorrectly. As the industry shifts toward complex electric vehicle systems in 2026, the risk of a technical error increases, making this indemnity more vital than ever.

Mobile Mechanics, Valeters, and Recovery Operators

Mobile operators have a different set of priorities. You’re often working at the roadside or on customer property where you can’t control the environment. Your policy must include robust tool cover, as mobile vans are frequent targets for theft in the West Midlands and beyond. For those in vehicle recovery, the requirements are even more specific. You need specialist indemnity for winching and towing. Standard road risks won’t cover damage caused to a vehicle while it is being lifted or transported on a spec-lift. Whether you’re towing a broken-down EV or valeting a high-end sports car, your cover must match the specific “hire and reward” nature of your work.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

How to Calculate and Reduce Your Motor Trade Insurance Costs

With motor trade insurance premiums rising by an estimated 10-15% in 2025, finding ways to manage your overheads is no longer optional. Insurers calculate your risk based on several core variables, including your business location, the age of your drivers, and your claims history over the last five years. Proactive risk management is the most effective way to secure long-term premium discounts. By demonstrating that you’ve taken steps to reduce the likelihood of a claim, you position your business as a lower risk in a tightening market.

Physical security is your strongest tool for lowering costs. Insurers look favourably on businesses that invest in 24-hour monitored CCTV, gated perimeters, and Thatcham-approved immobilisers for all stock vehicles. Even simple measures, like storing keys in a signal-blocking “Faraday” box, can prevent high-tech thefts that have become more common in the West Midlands. When you show a commitment to security, you give your broker the leverage they need to negotiate better rates with underwriters. It’s often worth the effort to get a specialist motor trade quote that takes these specific improvements into account.

Managing the Motor Insurance Database (MID)

Accuracy on the MID is about more than just avoiding a fine; it’s about premium stability. In 2026, the FCA is prioritising consumer outcomes and clarity, which means insurers are looking for traders who maintain meticulous records. If your MID records are messy or outdated, insurers may view your business as poorly managed, which can lead to higher “administration” loadings on your policy. For larger traders, using the MID to efficiently manage fleet car insurance ensures that every vehicle is accounted for, reducing the risk of vehicle impoundment and the subsequent spike in premium costs that follows an uncovered loss.

Smart Ways to Lower Your Annual Premium

There are several practical steps you can take to trim your costs without sacrificing essential cover. First, review your driver list. Limiting cover to essential personnel only, and avoiding drivers under the age of 25, can significantly drop your quote. Younger drivers statistically represent a higher risk, and removing them from the policy is a quick win for your budget.

Second, consider your voluntary excess. Choosing a higher voluntary excess can lead to immediate reductions in your annual premium. You should also look at consolidating your various covers. Instead of having separate policies for your tools, your building, and your road risks, a bespoke motor trade package brings everything into one manageable payment, often at a discounted rate compared to individual modules. This streamlined approach saves time and money while ensuring there are no overlapping covers.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Why a Specialist Broker is Essential for West Midlands Motor Traders

Securing the right motor trade insurance isn’t just about finding the lowest number on a comparison site. In an industry where 796,000 people are employed across the UK automotive sector, the risks are too varied for a generic algorithm to handle. Bypassing faceless automated systems for a human-centric risk assessment ensures that your specific business model is actually understood. At Just Quote Me, we bring 30 years of independent brokerage experience in Staffordshire to the table, providing a steady hand in a complex market.

We believe in a no-nonsense approach to coverage. Instead of forcing you through a rigid digital form, we offer a personal touch that identifies the nuances of your trade. Whether you’re a dealer in Stone or a mechanic in Newcastle-under-Lyme, we simplify the jargon and do the heavy lifting for you. We access a broad network of top UK insurers, many of whom don’t deal directly with the public, to find bespoke solutions that fit your business like a glove.

Local Expertise for Staffordshire Businesses

Local knowledge matters when it comes to assessing risk. We understand the regional dynamics of the West Midlands, from the busy industrial estates in Stafford to the mobile traders serving rural villages. This local expertise allows us to provide more accurate advice on everything from premises security to the specific liabilities faced by local workshops. Many businesses in our region prefer the reliability of a commercial insurance broker in Staffordshire over the frustration of a generic call centre. We’re part of the same community, and we’re committed to helping Staffordshire’s automotive trade thrive through 2026 and beyond.

The Just Quote Me Process: Stress-Free Coverage

Our process is designed to be efficient and reassuringly straightforward. It starts with an initial consultation where we listen to your needs, followed by a thorough search of the market to build your bespoke policy. We don’t just disappear once the policy is signed; we provide ongoing support for mid-term adjustments and renewals. As your business grows or your fleet changes, we’re here to ensure your cover evolves with you. This personal service is why so many traders trust us to manage their professional risks year after year.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Secure Your Automotive Business for 2026

Your business deserves more than a generic policy that leaves you exposed to unexpected risks. We’ve explored how a modular approach ensures your road risks and premises are fully protected, while proactive security measures help keep your overheads manageable. By focusing on accurate MID updates and trade-specific indemnity, you build a resilient foundation that can handle the shifting regulations of the UK automotive market. It’s about more than just staying legal; it’s about ensuring your hard work is backed by a policy that actually performs when you need it most.

As an FCA-authorised independent broker with over 30 years of industry experience, Just Quote Me is here to do the heavy lifting. We provide access to a broad network of top UK insurers, ensuring you get a policy that reflects the true nature of your trade rather than an automated guess. It’s time to trade with confidence and leave the complexities of motor trade insurance to the specialists. Partner with Just Quote Me today to secure your future.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Frequently Asked Questions

Can I drive any car with motor trade insurance?

You can drive vehicles in your professional custody for business purposes, such as customer cars or stock vehicles. This doesn’t grant permission to drive any vehicle for personal use. Most policies restrict cover to specific vehicle types or engine sizes related to your trade. You should always verify these limits on your policy schedule to avoid being uninsured during a road test.

Is motor trade insurance the same as business car insurance?

No, motor trade insurance is a specialist product for those who handle multiple third-party vehicles, whereas business car insurance covers a specific owned vehicle for work travel. A trade policy is essential if you’re repairing, selling, or valeting cars you don’t own. It provides the legal flexibility required to operate an automotive business without insuring every vehicle individually.

Do I need motor trade insurance for a part-time valeting business?

Yes, you require professional cover if you handle customer vehicles, even for a few hours a week. If you move a vehicle on a public road or a customer’s driveway, you’re legally liable for any incidents. Combining this with public liability ensures you’re protected against claims of damage to the car’s finish or the customer’s property while you work.

What happens if I forget to update the Motor Insurance Database (MID)?

Failure to update the MID can result in immediate vehicle seizure by the police and a fixed penalty fine. Since ANPR systems check the database in real-time, an unlisted vehicle will show as having no insurance. This can lead to your business being flagged as high-risk, which often results in higher premiums or difficulty securing cover in the future.

Does motor trade insurance cover my own personal vehicles?

Your personal vehicles can be covered if they are added to the policy schedule and the MID with the correct use class. Most trade policies focus on business activities, so you must ensure social, domestic, and pleasure use is explicitly included. Just Quote Me can help you determine if adding a personal vehicle is the most cost-effective option for your specific situation.

Can I get motor trade insurance if I work from home?

Yes, many mobile mechanics and small-scale traders operate from a home address with full legal cover. You must disclose your home-based status to your broker to ensure the policy remains valid. It’s also vital to check that your home insurance doesn’t have restrictive clauses that conflict with your professional automotive activities.

What is the minimum age for a motor trade insurance policy?

Most insurers set the minimum age at 25 years due to the statistically higher risk associated with younger drivers. While some specialist schemes exist for those aged 21 to 24, they often carry higher excesses and restrictions on high-performance vehicles. If you’re under 25, working with an expert commercial insurance broker in Staffordshire is the best way to find an underwriter willing to accept the risk.

Does my policy cover tools and equipment kept in my van?

Standard road risks policies don’t automatically cover tools; you must include “Tools in Transit” cover as an optional extra. Given the high cost of diagnostic gear in 2026, ensuring your policy limit matches the replacement value of your equipment is essential. Just Quote Me recommends verifying that your security measures meet the insurer’s specific requirements for tool protection.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Article by

Just Quote Me

JustQuoteMe Ltd is an independent UK insurance brokerage specialising in business and personal insurance solutions. With over 35 years of industry experience, the company provides tailored insurance cover for businesses, landlords, tradespeople, hospitality venues, fleets, and individuals across the UK. Known for its personal service, expert advice, and competitive premiums, JustQuoteMe Ltd works with leading insurers to deliver bespoke policies designed around each client’s unique needs. The company is authorised and regulated by the Financial Conduct Authority (FCA No. 586607) and has built a reputation for trusted, straightforward insurance guidance and long-term client relationships.

Why should a rigid computer script decide the value of your passion based on a single BHP figure? If you drive a high-performance vehicle in 2026, you’ve likely encountered the “algorithm penalty” where standard insurers overcharge for engine size or reject you for minor modifications. We agree that it’s frustrating to be treated like a generic risk, especially when vehicle thefts surged by 21% in the year ending March 2025 and the average value of a single theft claim has risen to over £12,000. Securing performance car insurance shouldn’t feel like a battle against a faceless machine that doesn’t understand your car’s true worth.

This guide promises to show you how to bypass these rigid systems to find specialist schemes that offer agreed value protection and cover for occasional track use. We’ll preview the essential 2026 updates, including the shift in the Expensive Car Supplement threshold to £50,000 for zero-emission vehicles and the impact of Euro 7 standards arriving on November 29, 2026. With group 50 supercar premiums often exceeding £5,145 in central London, it’s time to move beyond the automated “no” of the big insurers and find a policy that fits your specific needs.

Key Takeaways

Understand how 2026 performance classifications for BHP and torque can push high-end family saloons into expensive insurance groups.

Learn why standard automated systems often overcharge for performance car insurance and how specialist brokers avoid these algorithm penalties.

Discover the benefits of specialist cover, such as the ability to choose your own marque-certified repairer and securing agreed value protection.

Identify practical security upgrades, like Faraday pouches and Thatcham-approved trackers, that can significantly lower your annual premiums.

Access exclusive, non-standard insurance schemes that aren’t available on comparison sites to ensure your vehicle is fully protected.

What is Classed as a Performance Car in 2026?

The definition of a performance vehicle has shifted significantly. In 2026, it’s no longer enough to look at engine displacement alone. While a 2.0-litre engine once suggested a standard saloon, modern turbocharging and hybrid assistance mean that same capacity can now produce upwards of 400 BHP. To understand what is a performance car in the eyes of a modern underwriter, we must look at a combination of power-to-weight ratios, insurance group ratings between 30 and 50, and the specific technology under the bonnet. Standard insurers often struggle to categorise a vehicle that looks like a family car but possesses the acceleration of a mid-90s supercar. This creates the “Super-Saloon” trap, where owners of cars like the BMW M5 or Audi RS6 are hit with massive premiums because an algorithm sees a four-door car with 600 BHP and defaults to the highest possible risk category.

The Performance Metrics That Matter to Insurers

Insurers prioritising performance car insurance risk profiles focus on three core numbers. First is the 0-62 mph acceleration time. Any car hitting that mark in under 6 seconds is automatically flagged as high performance. Second is the top speed. While many German cars are electronically limited to 155 mph, insurers view the removal of this limiter as a major modification that changes the risk entirely. Finally, Thatcham security ratings are more critical than ever. With vehicle thefts in England and Wales having surged by 21% in the year ending March 2025, a car with a high BHP but a low Thatcham rating for keyless entry protection will be almost impossible to cover through standard channels.

High-Performance EVs and Hybrids

2026 marks a turning point for performance electric vehicles (EVs). With the Expensive Car Supplement threshold for zero-emission vehicles rising to £50,000 on April 1, 2026, many high-end EVs now sit in a complex tax and insurance bracket. Insurers are particularly wary of the instant torque provided by cars like the Porsche Taycan or Tesla Model S. The inclusion of “Ludicrous” or “Plaid” modes isn’t just a marketing feature; it’s a specific risk factor that specialists must underwrite manually. Furthermore, the high cost of battery replacement in a total-loss claim means that even a minor accident in a performance EV can lead to a write-off. This is why specialist performance car insurance is essential for EV owners who want to ensure their battery and specialist aerodynamic components are covered at their true replacement value.

If you’re finding that automated sites don’t understand your car’s true specification, it’s time to speak to a human expert. We don’t rely on rigid scripts to decide your premium.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Why Standard Car Insurance Fails Performance Owners

Most mainstream insurers use broad-brush logic when calculating performance car insurance premiums. If your vehicle has a high-BHP engine, the automated systems often apply a significant penalty without considering the context of your ownership. They don’t account for whether you store the car in a climate-controlled garage or if you only drive it 2,000 miles a year. This rigid, binary approach is Why insuring performance cars is different; it requires a level of human nuance that a computer script simply cannot provide.

The financial risk for standard insurers is also driven by rising repair costs. Performance vehicles often feature specialist carbon-fibre bodywork or active aerodynamic components that require specific technicians and expensive parts. Because these models are highly desirable to organised criminal groups, generic companies often default to a flat refusal or an astronomical quote. At Just Quote Me, we bypass these scripts to negotiate bespoke terms directly with underwriters who understand the enthusiast market.

The Problem with Market Value Settlements

Standard policies usually pay out based on “Market Value” at the time of a claim. For a rare or pristine performance car, this figure is often insufficient to replace the vehicle. If your car is a future classic or has undergone significant restoration, you need an “Agreed Value” policy. This ensures that in the event of a total loss, you receive a pre-determined sum that reflects the car’s true worth, rather than a depreciated figure pulled from a generic trade guide. We work with you to verify the condition of your vehicle to secure these higher settlement figures.

Modification Rejection: The Mainstream Dealbreaker

Mainstream sites often cancel policies or refuse cover if they discover a simple ECU remap or an upgraded exhaust system. They view any change from factory specification as an unacceptable increase in risk. However, a specialist broker knows the difference between a performance upgrade and a dangerous modification. We ensure your changes are “accepted” rather than just “declared,” providing you with total peace of mind. If you are an enthusiast who spends time working on your own vehicles, you might also find value in our guide to Specialist Motor Trade Insurance. For those operating a business that buys, sells, or repairs performance vehicles, our comprehensive motor trade insurance guide for 2026 covers everything from MID obligations to protecting customers’ vehicles on your premises.

You can explore our range of tailored insurance products to see how we help drivers protect their high-value investments with a personal touch.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Comparing Specialist Performance Cover vs. Standard Policies

Standard insurers usually promote “Comprehensive” cover as the ultimate protection. However, for a high-performance vehicle, this label often hides significant gaps. Standard policies default to market value settlements, whereas specialist performance car insurance prioritises “Agreed Value.” This distinction is vital because a market value calculation doesn’t reflect the true cost of replacing a pristine Porsche or a limited-edition Ferrari. If your car is damaged, a standard insurer might insist on using their “approved” repair network. These garages are often high-volume centres that lack the specialist jigs or diagnostic software required for high-performance marques. We ensure your policy includes a “Choice of Repairer” clause, allowing you to send your vehicle to a technician you trust.

Usage patterns also dictate your premium. If your car is a “weekend” vehicle, we can secure limited mileage discounts that reflect its reduced time on the road. Unlike standard policies that exclude any form of circuit use, specialist schemes can include occasional track day cover. This provides protection while you explore the car’s limits in a controlled environment. Understanding these ways to potentially lower your insurance costs is essential for managing the total cost of ownership in 2026. With the daily Congestion Charge in London rising to £18 as of January 2, 2026, and fuel duty set to rise on September 1, 2026, every saving on your premium counts.

Specialist Benefits You Won’t Find on Comparison Sites

One of the biggest advantages of a specialist policy is like-for-like replacement of modified parts. If your aftermarket carbon-fibre splitter is damaged, a specialist insurer replaces it with the same component, rather than a factory-standard plastic version. Additionally, many of our clients enjoy European road trips. Our policies often include full continental cover as standard, which is important for rallies or alpine tours. For those with a collection of high-performance vehicles, a bespoke Fleet Car Insurance policy often provides better value and less paperwork than individual covers.

The Multi-Car and Business Use Factor

It’s a common myth that performance cars can’t be used for business. If you use your vehicle for client visits or travelling between sites, we can arrange “Class 1” business use. This is a common requirement for consultants who also hold Professional Indemnity Insurance and want their vehicle to reflect their professional status. We can often bundle your daily driver and your performance car into a single multi-car policy, simplifying your admin while maintaining the high level of protection your performance vehicle requires.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Practical Ways to Reduce Your Performance Car Insurance Premium

Reducing your performance car insurance premium requires a proactive approach to risk management. It isn’t just about finding the cheapest quote; it’s about proving to underwriters that you’re a lower-than-average risk. With vehicle thefts in England and Wales having surged by 21% in the year ending March 2025, security is the most significant lever you can pull. Modern 2026 security goes beyond a simple alarm. Insurers now look for AI-monitored trackers that can detect unauthorised movement in real-time. Since keyless theft accounted for 98% of stolen vehicles located by recovery companies in July 2023, simple steps like using Faraday pouches can have a direct impact on your quote.

Thatcham-approved S5 or S7 trackers with 24/7 monitoring

Ghost immobilisers or physical steering locks to deter relay attacks

Professional-grade Faraday boxes for overnight key storage

Beyond hardware, your driving credentials matter. Completing an advanced driving qualification with the Institute of Advanced Motorists (IAM) or RoSPA demonstrates a level of competence that automated algorithms often ignore. Similarly, joining a marque-specific owner’s club can unlock specialist schemes. These clubs often have pre-negotiated rates with brokers because their members are statistically more likely to maintain their vehicles to a high standard. This human-centric approach to risk is why we prefer manual underwriting over rigid computer scripts.

The Impact of Storage and Location

Where you keep your car overnight is a critical factor. A locked, brick-built garage is the gold standard, but even a secure driveway with retractable bollards can lower your rate. We understand the specific risks in the West Midlands and Staffordshire. If you’re based in Stafford or Newcastle-under-Lyme, our local knowledge allows us to present your risk to underwriters more effectively than a national call centre could. We know which postcodes have higher recovery rates and which areas require extra physical security to satisfy specialist insurers.

Policy Structuring for Lower Costs

You can also lower costs by adjusting your policy structure. Increasing your voluntary excess is a direct way to reduce the annual premium for your performance car insurance, provided you can afford the upfront cost in the event of a claim. If you only drive your car during the summer months, a “laid-up” policy provides fire and theft cover while the vehicle is SORN, which is significantly cheaper than a full road policy. While telematics or “black box” insurance is often associated with young drivers, some performance specialists now offer “pay-per-mile” schemes for weekend cars. This allows you to maintain comprehensive cover while only paying for the exact distance you travel.

To find a policy that rewards your security efforts, you can get a tailored quote from our expert team today.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Why Choose Just Quote Me for Your Performance Insurance?

Choosing the right partner for your performance car insurance is about more than just finding a policy; it’s about finding an advocate who understands the machine in your garage. With 30 years of expertise in the UK specialist motor market, Just Quote Me has built relationships with underwriters that the general public simply cannot access. While the average cost of comprehensive car insurance in the UK stands at approximately £726 as of January 2026, owners of high-performance vehicles face a much more volatile market. We specialise in placing risks that automated systems often reject, whether that’s due to a high-BHP engine or a specific modification list.

Our roots in Staffordshire and the West Midlands give us a unique perspective on local risk factors. We don’t just see a postcode; we see the secure garaging and proactive security measures you’ve taken to protect your investment. This local knowledge is vital as we move through 2026, especially with the temporary 5p reduction in fuel duty beginning to phase out from September 1, 2026. We help you manage the total cost of ownership by ensuring your premium reflects your actual risk, not a generic regional average calculated by a computer script.

The Personal Touch of an Independent Broker