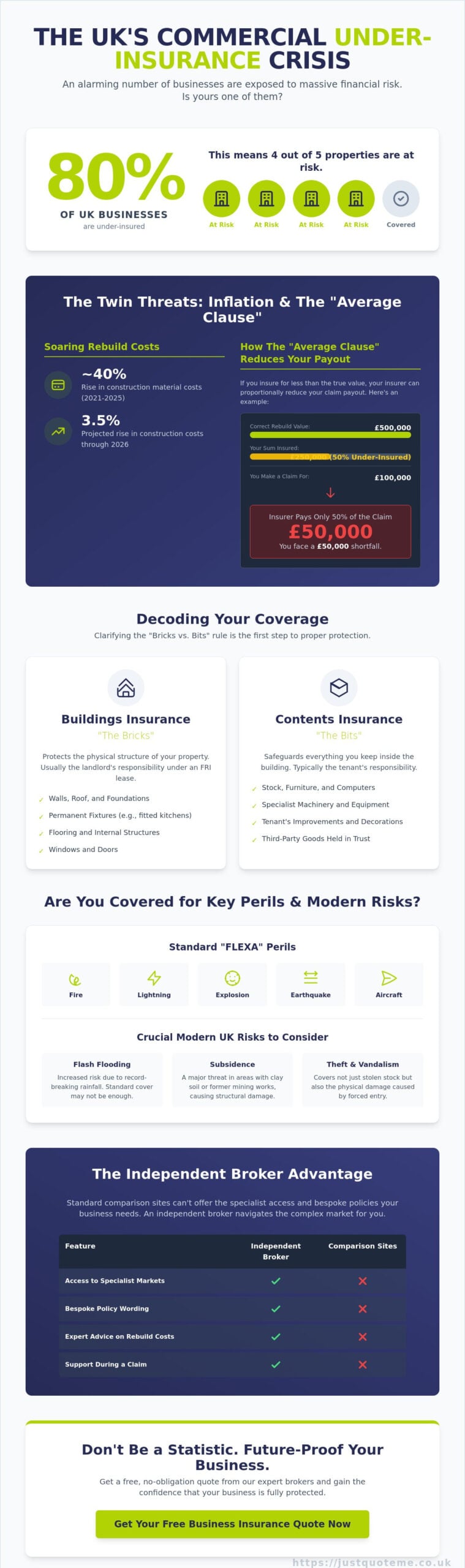

Recent data from the Building Cost Information Service (BCIS) reveals that 80% of UK commercial properties are currently under-insured. This means four out of five business owners risk a pro-rata claim rejection during a commercial property insurance dispute if disaster strikes. It’s a stressful reality, especially as construction costs are projected to rise by 3.5% through 2026. You likely feel the pressure of rising premiums and the confusion of where your responsibility ends and your landlord’s begins. We agree that securing your livelihood shouldn’t be this complicated.

This guide empowers you to master your coverage with expert insights from a leading UK independent broker. We promise to clear the fog around buildings versus contents cover and provide a reliable framework to calculate your correct sum insured. You’ll gain the confidence that your specific trade, whether it’s hospitality or retail, is fully protected against modern risks. We will explore the essential steps to future-proof your assets and avoid the pitfalls of under-insurance in an inflationary market.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Key Takeaways

- Understand how rising material costs and new building regulations have shifted the landscape for commercial property insurance in 2026.

- Learn to identify core “FLEXA” perils and ensure your assets are protected against increasing UK environmental risks like flash flooding and subsidence.

- Clarify the “Bricks vs. Bits” rule to determine whether you or your landlord are legally responsible for insuring the building structure under an FRI lease.

- Discover why insuring for market value instead of rebuild cost is a critical mistake that could trigger the “Average Clause” and reduce your claim payout.

- Find out how using an independent broker provides access to specialist markets and bespoke policy wording that standard comparison sites cannot offer.

What is Commercial Property Insurance and Why is it Essential in 2026?

Commercial property insurance is a specialized policy designed to protect your business’s physical assets. It covers the bricks and mortar of your building along with everything you keep inside it. This insurance provides a vital financial safety net against unpredictable risks like fire, flood, and theft. To understand the foundational concepts of how these policies categorize risks, you can read more about What is Property Insurance? and how it differs from other types of coverage.

In 2026, the landscape for UK business owners has changed. Construction material costs rose by roughly 40% between 2021 and 2025, meaning many older policies no longer cover the actual cost of a full rebuild. New regulations like the Building Safety Act have also introduced stricter requirements for premises maintenance and safety. If your commercial property insurance hasn’t been updated to reflect these 2026 realities, you could find yourself facing a massive shortfall during a claim.

The cost of staying uninsured is often terminal for a small business. A single burst pipe in a retail unit can cause over £15,000 in stock damage and structural repairs. An electrical fire in a workshop can easily exceed £50,000 in equipment loss alone. Without a robust policy, these incidents often lead to immediate bankruptcy. It is also a mistake to rely on a standard home insurance policy if you run a business from your residence. Most residential insurers will void a claim instantly if they discover the property was used for commercial activities without their knowledge.

The Two Pillars: Buildings vs. Contents Cover

Buildings insurance protects the physical structure of your property. This includes the roof, walls, and permanent installations like fitted kitchens or flooring. It is designed to cover the cost of repair or a total rebuild after a catastrophic event. Contents insurance safeguards your stock, furniture, and specialist machinery. It even covers third-party goods that you might be holding in trust for customers. In every policy, the Sum Insured is the maximum amount an insurer will pay for a total loss, so it must be calculated accurately based on current market rates.

Is it a Legal Requirement?

While commercial property insurance isn’t a statutory law like Employers Liability Insurance, it’s rarely optional in practice. If you have a mortgage on your premises, your lender will insist on buildings cover as a contractual requirement to protect their investment. The Financial Conduct Authority (FCA) regulates how these products are sold, ensuring that brokers provide clear and honest advice. To ensure your business has a complete protection overview, you should also look into our Public Liability Insurance options to cover your interactions with clients and the general public.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

What Does a Comprehensive Commercial Policy Cover?

A standard commercial property insurance policy provides a safety net for your physical assets, but the level of protection depends on the specific perils included. Most basic policies cover “FLEXA” events: Fire, Lightning, Explosion, Earthquake, and Aircraft. While these represent catastrophic risks, they’re only the starting point for a robust insurance strategy. To ensure your business isn’t left vulnerable, you should Calculate Your Rebuild Value using professional standards to avoid the trap of underinsurance during a total loss claim.

Environmental risks are a growing concern for UK business owners. With the Environment Agency noting that record-breaking rainfall in 2024 has increased the risk of flash flooding, standard cover must be scrutinised. Subsidence is another critical factor, particularly in areas with clay-heavy soil or old mining works. A comprehensive policy accounts for these shifts in the landscape, providing the funds needed for structural repairs or site stabilisation.

Theft and vandalism coverage is designed to handle more than just missing stock. It addresses the physical damage caused by forced entry, such as smashed doors or damaged security shutters. For high-traffic businesses, adding “Accidental Damage” is often a smart move. This “all-risks” extension covers mishaps that don’t fall under standard perils, such as a vehicle hitting your building or a burst pipe damaging internal fixtures.

Critical Add-ons for Business Continuity

Property damage is often followed by a period where you cannot trade. Business Interruption cover is essential here; it replaces lost income and covers fixed costs like payroll while your premises are being repaired. For those in the retail sector, Shop Insurance packages often include specific protections for glass frontages and external signage. These assets are frequently targeted by vandals or damaged by weather, and replacing bespoke branding can be surprisingly expensive.

The Intersection with Liability and Cyber

It’s helpful to remember that property insurance covers the “where,” while liability covers the “who.” If a storm damages your roof and a falling tile injures a passerby, you will likely face a Public Liability claim alongside your property repairs. Modern businesses also face digital risks that physical cover can’t solve. If a fire destroys your on-site servers, you’ll need Cyber Insurance to help recover lost data and manage the resulting breach notifications. Pairing these covers ensures that a single physical event doesn’t lead to a total business collapse.

If you’re unsure which extensions your specific trade requires, it’s often best to speak with a specialist broker who understands the local risks in your area.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Who is Responsible? Landlord vs. Tenant Obligations

Understanding who pays for what in a commercial lease can be a headache. The general rule follows a “Bricks vs. Bits” logic. Landlords typically insure the bricks (the structure) while tenants look after the bits (contents and improvements). For a broader look at standard coverage types, this Association of British Insurers overview explains the basics of fire, flood, and theft protection.

Most UK commercial agreements are Full Repairing and Insuring (FRI) leases. In these cases, the tenant takes on the financial burden of repairs and building insurance premiums. Even though the landlord selects the commercial property insurance policy to protect their asset, they’ll usually recharge the cost to you via a service charge or insurance rent. You should always check your lease to confirm exactly which costs you’re expected to cover.

Landlord Responsibilities

Landlords must protect their investment and their income. If a fire makes the building unusable, Loss of Rent cover keeps cash flowing while repairs happen. Property Owners Liability is equally vital. If a roof tile falls and hits a passerby, the landlord is usually the one facing the claim. For those with mixed portfolios, such as flats above shops, Residential Letting Insurance provides the specific cover needed for the domestic quarters. Owners of hospitality venues face unique risks, so checking specialized hotel and guest house insurance is a smart move to manage complex guest liabilities.

Tenant Responsibilities

Tenants often wrongly assume the landlord’s policy covers everything inside the four walls. It doesn’t. Your stock, machinery, and office tech are your responsibility. If you’ve spent £50,000 on a high-end mezzanine or shop fit-out, you must declare these tenant improvements to your insurer. Standard building policies won’t cover your bespoke lighting or custom flooring. For mobile professionals, Van and Tools insurance protects assets when they leave the premises. Don’t forget the glass. Many UK leases state the tenant is responsible for the shopfront windows, even if they don’t own the building structure itself.

Getting the right commercial property insurance depends on the specific wording of your lease. Whether you’re the one owning the building or the one running the business inside it, clarity on these obligations prevents expensive gaps in cover.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

How to Calculate Your Rebuild Value and Avoid Under-Insurance

Your property’s market value has almost nothing to do with your commercial property insurance requirements. While a retail unit in a prime London location might sell for millions, the cost to rebuild it if it burns down could be significantly lower. Conversely, an old warehouse in a less expensive area might have a low market value but cost a fortune to reconstruct using modern safety standards. You must insure for the full reinstatement cost. This includes the price of materials, labour, and specific site requirements. If you base your cover on what you paid for the building, you’re likely making a costly mistake.

Most policies include an “Average Clause.” This is a penalty for under-insurance that many owners overlook. If you insure your building for £750,000 but the true rebuild cost is £1 million, you’re 25% under-insured. If you suffer a fire causing £100,000 of damage, the insurer will only pay £75,000. You’re left to find the remaining £25,000 yourself. This applies to every claim, no matter how small. It’s a standard industry practice designed to ensure premiums reflect the actual risk held by the insurer.

Don’t just look at bricks and mortar. You need to account for architects, surveyors, and legal fees. Debris removal alone can cost thousands, especially if hazardous materials like asbestos are present. A RICS-certified surveyor provides the most accurate figure. Relying on a “best guess” in 2026 is a high-risk strategy that often leads to financial gaps. Professional valuations give you a robust defense if an insurer ever questions your sum insured during a claim. It’s always better to compare commercial property insurance rates with an accurate valuation in hand.

The Impact of Inflation on Sums Insured

Construction costs in 2026 are vastly different from 2020 prices. Labour shortages and material price hikes mean building a project now costs roughly 30% more than it did five years ago. We recommend index linking your policy. This ensures your cover increases in line with inflation automatically. Owners of specialist properties, such as those needing Thatched Pubs insurance, face even higher specialist labour costs that must be reviewed every twelve months.

Risk Assessment for Premium Reduction

Proactive risk management lowers your commercial property insurance costs. Installing Grade 3 alarm systems or CCTV can lead to immediate premium discounts. Your fire risk assessment is also vital. If you haven’t updated your fire protocols according to current UK regulations, your insurer might dispute a claim. Premises with high-value stock should also consider specific Security Insurance to bridge any gaps in their standard building cover.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Why Use an Independent Broker Like Just Quote Me?

Finding the right commercial property insurance shouldn’t feel like a gamble. While comparison sites offer speed, they often lack the depth needed for complex UK business assets. Most “off-the-shelf” policies use rigid algorithms that struggle with anything outside of a standard office block. This is where an independent broker adds real value. We have access to specialist, broker-only markets that don’t list on public sites. These insurers often provide more competitive rates because they trust a broker’s professional risk assessment over a generic online form.

Bespoke policy wording is another critical advantage. A one-size-fits-all approach is dangerous for high-risk sectors. For instance, the requirements for Nightclubs involve specific public liability and property damage nuances that a standard policy might miss. Similarly, our tailored cover for Restaurants accounts for specialized kitchen equipment and specific fire safety protocols. We ensure your policy actually covers what you own, rather than leaving you with expensive gaps in your protection. Hospitality venue owners should also explore our dedicated pub and bar insurance guide, which covers the unique licensing requirements and specialist risks facing UK landlords in 2026.

If the worst happens and you need to claim, we act as your personal advocate. Dealing with loss adjusters is a technical and often stressful process. We handle those difficult conversations for you, ensuring your claim is processed fairly and quickly. Our Staffordshire-based team provides a personal touch that automated call centres cannot match. You get a dedicated human advisor who understands your local market and your specific business goals.

Navigating Complex Risks with Expert Advice

We specialize in “difficult to place” risks that other providers turn away. This includes unoccupied buildings or properties used for high-hazard trades. If your premises have been empty for more than 30 consecutive days, standard cover usually lapses. We find specialist solutions to keep you protected. You can also streamline your overheads by bundling your property cover with Professional Indemnity, which often triggers a multi-policy discount. This approach simplifies your renewals and ensures all your liabilities are managed under one roof.

Get Your Free Quote Today

The process of securing a bespoke quote is designed to be efficient. To get started, you’ll need a few key details ready. This includes an accurate rebuild value (often based on BCIS data), details of your physical security such as BS3621 compliant locks, and a minimum of three years of claims history. Having this information helps us negotiate the best possible terms with our panel of insurers. We don’t believe in long, drawn-out applications; we focus on getting you the right cover at the right price as quickly as possible.

Secure Your Business Assets for the Years Ahead

Protecting your physical premises in 2026 requires a proactive approach to risk management. You’ve now seen how accurate rebuild valuations prevent the common trap of under-insurance and why clear boundaries between landlord and tenant duties are vital for legal clarity. Securing commercial property insurance shouldn’t be a source of stress for UK business owners. Just Quote Me brings over 30 years of industry experience to the table. As an FCA-authorised independent broker, we provide access to a broad network of top UK insurers to find the right fit for your specific trade. We believe in a straightforward, no-nonsense service that puts your protection first. Our specialists are ready to help you navigate the complexities of the current market with ease and confidence. We handle the heavy lifting so you can focus on running your business.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Take the first step toward comprehensive protection today; we’re here to make the process as simple as possible.

Frequently Asked Questions

Is commercial property insurance a legal requirement in the UK?

Commercial property insurance isn’t a legal requirement under UK law, unlike the mandatory Employers Liability cover required by the 1969 Act. However, you’ll find it’s almost always a contractual necessity. Lenders and landlords typically mandate buildings insurance within their agreements to protect their financial interests. If you have a mortgage or a lease, you’re likely obligated to keep the property insured to its full reinstatement value.

Does commercial property insurance cover my stock?

Yes, but your policy only covers stock if you specifically include Contents and Stock protection. Standard buildings cover excludes inventory, so you must declare the total value of your goods to ensure protection against theft, fire, or water damage. For instance, a wholesaler holding £100,000 in inventory needs this specific addition to avoid a total loss during a flood or break-in. It’s vital to update these values regularly.

What is the Average Clause in commercial insurance?

The Average Clause is a rule where insurers reduce a claim payout by the same percentage that a property is under-insured. If a surveyor values your building at £1 million but you’ve only insured it for £500,000, you’re 50% under-insured. Consequently, the insurer will only pay 50% of any claim, even for minor damage. This means a £20,000 repair bill would only result in a £10,000 payout from your provider.

Are tenants responsible for commercial property insurance?

Responsibility for insurance costs depends entirely on your specific lease agreement. Under a Full Repairing and Insuring (FRI) lease, which is common in many UK commercial tenancies, the tenant is responsible for the insurance costs. While the landlord usually arranges the policy to ensure their asset is protected, they’ll recharge the premium to you. Always check your contract to see if you’re paying this “insurance rent” directly to the landlord.

Does it cover damage from floods?

Most standard commercial property insurance policies include flood damage, but terms vary based on your location’s risk profile. If the Environment Agency identifies your business area as a high-risk zone, you might face a higher excess or require a specialist policy. You should always check your policy wording with a broker to confirm you’re protected. Some businesses may need bespoke terms if they’ve had previous flood claims within the last five years.

Can I get insurance for a home-based business property?

Standard home insurance usually excludes business activities, meaning your professional equipment and stock aren’t covered. If you run a business from home, you’ll need a specific “working from home” extension or a dedicated small business policy. This provides the necessary cover for your kit and any liability for clients visiting your premises. Without this specialist cover, a business-related incident could potentially invalidate your entire domestic insurance policy.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.