by jqm | May 19, 2026 | Insurance

Did you know that in early 2026, 43% of landlords reported a void period in the past year? It’s a sobering statistic for anyone entering the rental market, especially following the abolition of “no-fault” evictions on May 1st. You likely want to focus on your new venture, but relying on standard home insurance is a common mistake that leaves many properties unprotected. This is why a comprehensive first time landlord insurance checklist is your most valuable tool for protecting your property and your peace of mind from day one.

We’ll show you exactly how to secure your property by clarifying which requirements are legal necessities and which are optional protections. You’ll gain a clear understanding of mandatory safety certificates like the EICR and Gas Safety checks, the differences between buildings and liability cover, and how to safeguard your rental income in a changing market. Simply Just Quote Me to streamline your insurance process and ensure your investment is fully compliant with the latest 2026 regulations.

Key Takeaways

- Identify why standard home insurance leaves your rental property exposed and how to avoid the common trap of voided policies.

- Navigate the mandatory 2026 legal landscape, including the essential requirements for Gas Safety Certificates and five-year EICR reports.

- Utilise our detailed first time landlord insurance checklist to distinguish between buildings, contents, and liability cover for full protection.

- Master the fundamentals of tenancy management, from performing “Right to Rent” checks to vetting tenants effectively in a post-no-fault eviction market.

- Understand the benefits of using an independent broker to access bespoke insurance solutions that offer better value than off-the-shelf alternatives.

Why Standard Home Insurance Won’t Protect Your Rental Property

Many new landlords assume their existing home insurance policy is sufficient to cover their rental property. This is a dangerous misconception. Standard home insurance is built on the assumption that the property owner lives in the building and takes personal care of it. When you introduce a tenant, the risk profile shifts significantly. For anyone building a first time landlord insurance checklist, understanding this distinction is the first step toward securing your investment.

If you continue to use a standard residential policy while renting out the property, you risk your insurer voiding the policy entirely. This means if a fire or flood occurs, you could face total claim rejection. Specialist landlord insurance is designed for the unique challenges of 2026, offering protections that standard policies simply do not provide. These policies account for the fact that you aren’t on-site every day to spot a leak or a maintenance issue before it becomes a catastrophe.

The Legal Distinction of a “Let” Property

The relationship between a landlord and a tenant is a commercial one. It carries different legal weight than living with family members or friends. When a third party pays to reside in your property, your liability risks increase. If a tenant is injured due to a fault in the property, you are legally responsible. Standard policies usually lack the Public Liability limits required for rental scenarios. They also won’t help you recover lost income. By understanding rent insurance, you can see how specialist policies protect your cash flow if the property becomes uninhabitable. This is a feature standard home insurance never includes, yet it’s a vital part of any first time landlord insurance checklist.

Mortgage Lender Requirements

Transitioning from a homeowner to a landlord often involves moving from a residential mortgage to a Buy-to-Let (BTL) mortgage. You must obtain “consent to let” from your lender before any tenant moves in. Failing to inform them of a change in occupancy can be considered mortgage fraud. Most lenders make landlord insurance a mandatory condition of the mortgage agreement. They want to ensure their collateral is protected by a policy that accounts for the specific risks of a let property. Without the right coverage, you are not only exposed to financial loss but also in breach of your mortgage contract. This transition is a critical regulatory step that separates professional landlords from casual homeowners.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

The Regulatory Foundation: Legal Safety Checks and Certificates

Before a tenant ever turns a key, your property must meet strict legal benchmarks. These aren’t mere suggestions; they are the bedrock of your legal standing as a housing provider. Failing to meet these standards doesn’t just invite local authority fines. It can also lead to your insurer rejecting a claim entirely. Any comprehensive first time landlord insurance checklist starts with verifying that your safety certificates are current, valid, and properly documented.

As of 2026, properties must maintain a minimum Energy Performance Certificate (EPC) rating of E to be legally let. While many landlords are proactively upgrading to higher ratings to future-proof their investments, E remains the current legal floor. You should verify your specific landlord safety responsibilities via official government resources to ensure your property remains compliant with the latest energy and safety standards. If you need help understanding how these regulations affect your policy, you can consult an expert broker for tailored advice.

Gas and Electrical Safety Obligations

You must arrange an annual gas safety check conducted by a Gas Safe registered engineer. This results in a Gas Safety Certificate (CP12), which you must provide to your tenants within 28 days of the inspection. For electricity, the Electrical Installation Condition Report (EICR) is required every five years. It’s best practice to keep digital copies of these documents as part of your permanent records. Most insurers view a missing or expired safety certificate as a material breach of policy conditions. If a fire or accident is caused by faulty utilities and you don’t have the proper certification, your insurance policy will likely be invalidated.

Fire and Carbon Monoxide Prevention

Fire safety rules are precise and non-negotiable. You must install a smoke alarm on every habitable storey of the property. Additionally, carbon monoxide alarms are mandatory in any room containing a fuel-burning appliance, such as a gas boiler or a wood-burning stove. For furnished lets, all upholstered furniture must comply with the Furniture and Furnishings (Fire Safety) Regulations. This includes items like sofas, mattresses, and even headboards. Documenting your “start of tenancy” alarm tests provides vital evidence if a dispute or claim arises later. Including these verification steps in your first time landlord insurance checklist ensures you aren’t just paying for a policy, but actually maintaining the protection you need.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

The Essential First-Time Landlord Insurance Checklist

Selecting the right insurance isn’t just about finding the lowest premium. It’s about building a safety net that survives real-world challenges. In a market where 43% of landlords reported a void period in early 2026, your first time landlord insurance checklist must account for both physical damage and financial disruption. A well-structured policy ensures that a single burst pipe or a tenant dispute doesn’t derail your entire investment strategy. By focusing on the specific risks associated with rental properties, you can move forward with the confidence that your assets are professionally protected.

Protecting the Physical Asset

Buildings insurance is the foundation of your coverage. It protects the structure against major perils such as fire, flood, and subsidence. One common mistake for new landlords is insuring the property for its market value. You must calculate the “rebuild cost” instead, which is the actual cost of labour and materials required to reconstruct the property from scratch. Our Residential Letting Insurance options are designed to help you navigate these specific valuations. Don’t overlook contents cover, even for unfurnished lets. You’ll likely still own carpets, curtains, and white goods that need protection. Keep in mind that insurers generally exclude general wear and tear, so regular maintenance remains your responsibility.

Liability and Income Protection

Liability and income protection are where you mitigate the most significant financial risks. Property Owners Liability is a standard inclusion and serves as a specialized form of Public Liability Insurance. It shields you if a tenant or visitor suffers an injury on your property and brings a legal claim against you. Equally vital is Loss of Rent cover. If a fire or flood makes the building uninhabitable, this cover replaces your lost income so you can continue meeting mortgage obligations during repairs. While setting up these protections, ensure you’re compliant with wider regulations, such as using a tenancy deposit protection (TDP) scheme. Compliance with these legal standards is often a prerequisite for your insurance to remain valid during a claim.

You should also consider optional extras to fill potential gaps. Accidental damage cover is useful if a tenant stains a carpet or breaks a window. Malicious damage cover provides a deeper layer of security against intentional harm to the property. Finally, legal expenses cover has become increasingly important in 2026. With the abolition of “no-fault” evictions, legal disputes can be more complex and costly to resolve. Having professional legal support built into your policy ensures you aren’t facing these administrative burdens alone.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Managing Your Tenancy: Vetting, Deposits, and Right to Rent

Managing your tenancy effectively is about more than just being a good host. It is a critical part of your risk management strategy. For those following a first time landlord insurance checklist, the vetting and administrative phase is where you ensure your policy remains enforceable. Insurers often set specific conditions regarding how you select and manage tenants. If you fail to meet these operational standards, you might find your cover compromised exactly when you need it most.

One of your primary legal duties is the “Right to Rent” check. You are required to verify the immigration status of every adult tenant before they move in. This is a statutory obligation that carries significant penalties for non-compliance. Beyond legal requirements, thorough vetting acts as your first line of defence against future claims. This process should include comprehensive credit checks, employment references to confirm income, and history from previous landlords to identify potential red flags. Following these steps helps you build a stable rental business from the start.

The Vetting Process as Risk Mitigation

Thoroughly checking a tenant’s background significantly reduces the likelihood of facing malicious damage or unpaid rent. For tenants with lower credit scores or students, requiring a UK-based guarantor provides an extra layer of financial security. It is important to remember that some Rent Guarantee policies require specific vetting evidence, like a formal reference from a previous landlord, to remain valid in the event of a claim. This vetting process is a core element of your first time landlord insurance checklist because it demonstrates to your insurer that you are acting with professional due diligence.

Deposit Protection and Inventories

Once you accept a deposit, the clock starts ticking. You must protect the funds in one of the three government-approved schemes within 30 days. You are also legally required to provide the tenant with “Prescribed Information” detailing where their money is held. Failing to do this can prevent you from using a Section 8 notice if you ever need to regain possession of the property. Alongside this, a professional inventory and schedule of condition are essential. Detailed notes and high-resolution photos are the only way to prove damage at the end of a tenancy and successfully claim against a deposit.

If your property is part of a mixed-use building, such as a flat above a retail unit, your insurance needs will differ. In these cases, you should look into Commercial Property Insurance to ensure the entire structure is correctly covered. To make sure your specific setup meets all legal and insurance requirements, you can speak with our team today for a professional assessment.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Why Using an Independent Broker Saves New Landlords Time and Money

Completing your first time landlord insurance checklist is a major milestone, but the final hurdle is securing the policy itself. While big banks and automated platforms offer convenience, they often provide rigid, “one-size-fits-all” products. These policies might seem cheaper initially, yet they frequently contain restrictive clauses that don’t account for the specific nuances of your property or tenant type. Working with an independent broker provides a human-centric alternative to these automated systems, ensuring you receive a policy that is actually fit for purpose.

Bespoke Solutions vs. Direct Policies

First-time landlords benefit immensely from a professional risk assessment that looks beyond the basic rebuild cost. An independent broker has access to a wide panel of UK insurers, many of whom don’t sell directly to the public. This allows them to find hidden savings by matching cover exactly to your needs, rather than upselling unnecessary add-ons. With Just Quote Me’s 30 years of experience in the UK market, we understand how to navigate complex risks that automated sites often reject. Whether you’re managing a standard let, a House in Multiple Occupation (HMO), or even a property with specialist features covered under thatched insurance, a broker acts as your expert advisor.

This support becomes most valuable during the claims process. If a tenant causes significant damage or a legal dispute arises, you won’t be left dealing with a generic call centre. Your broker understands your history and the specifics of your policy, providing a steady hand to manage administrative burdens while you focus on your investment. This personalised service ensures that you aren’t just another policy number in a database.

Taking the Next Step with Confidence

Securing the right protection doesn’t have to be a slow or complicated process. By using a broker, you can compare multiple providers at once through a single point of contact. This efficiency is vital when you’re trying to coordinate a tenant move-in date alongside your legal obligations. Before you finalise your first time landlord insurance checklist, ensure you’ve ticked off these essential steps:

- Obtained formal consent to let from your mortgage lender.

- Verified all safety certificates (Gas Safety, EICR, and EPC) are valid.

- Completed thorough tenant vetting and secured the deposit in a government-approved scheme.

- Selected a bespoke insurance policy that includes Property Owners Liability.

By following this structured approach, you transition from a property owner to a professional landlord with your financial interests fully protected. You can Get Your Free Business Insurance Quote now to see how a tailored policy can secure your future rental income.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Secure Your Future as a Professional Landlord

Transitioning into the rental market is a significant step that requires a shift toward a professional risk management mindset. You’ve learned that standard home insurance is insufficient for let properties and that meeting legal safety standards, such as the annual gas check and five-year EICR, is non-negotiable for your policy’s validity. By following this first time landlord insurance checklist, you’ve built a foundation of compliance and protection that guards against the specific risks of the 2026 property market.

Just Quote Me is here to simplify these administrative burdens. As an FCA-authorised independent broker with over 30 years of industry experience, we provide access to top UK insurers and bespoke advice tailored to your unique property needs. Whether you are managing a single flat or a complex mixed-use building, we ensure your investment remains secure and your liability is fully covered. Partner with Just Quote Me today to move forward with the confidence that your new venture is built on the strongest possible footing.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Frequently Asked Questions

Do I legally need landlord insurance in the UK?

Landlord insurance isn’t a legal requirement in the same way as motor insurance, but it’s often a mandatory condition of your mortgage agreement. Most Buy-to-Let lenders require proof of specialist cover before they’ll approve your loan. Without it, you’re personally liable for any structural damage or legal claims, which can be financially devastating for a new investor. It’s the only way to ensure your asset is protected against rental-specific risks.

Can I use standard home insurance if I am only renting out one room?

You shouldn’t rely on standard home insurance even if you only have a single lodger. Most residential policies are voided the moment you take in a paying tenant without notifying the insurer. Specialist cover accounts for the increased liability and property risks associated with third-party occupants, ensuring you stay protected if an accident occurs in the rented space. Always disclose your rental arrangements to keep your coverage valid.

What happens if I don’t have a Gas Safety Certificate as a landlord?

Failing to provide a valid Gas Safety Certificate can lead to unlimited fines or criminal prosecution. Beyond the legal penalties, your insurer will likely reject any claims related to fire, explosions, or carbon monoxide poisoning if you haven’t met your annual inspection duties. Maintaining these records is a vital part of your first time landlord insurance checklist to keep your policy valid and your tenants safe.

Does landlord insurance cover me if my tenant stops paying rent?

Standard landlord policies don’t typically cover unpaid rent unless you’ve added Rent Guarantee Insurance as an optional extra. This specific cover is designed to protect your income if a tenant defaults on their payments. Since the abolition of “no-fault” evictions on May 1, 2026, many landlords now view this as an essential protection during lengthy legal proceedings. It provides a vital safety net for your monthly mortgage obligations.

What is Property Owners Liability and why is it included in my policy?

Property Owners Liability protects you against legal claims if someone is injured on your property. If a tenant trips on a loose floorboard or a visitor is hurt by a falling roof tile, you could be held liable for significant compensation. This cover is a standard inclusion because it manages the high cost of legal fees and court-awarded damages. It’s a critical layer of protection for your personal finances.

How much does landlord insurance cost for a first-time landlord?

The cost of your policy depends on several factors, including the property’s location, the rebuild value, and your tenant’s occupation. While first-time landlords don’t have a specific track record in the sector, insurers look at the safety measures you’ve implemented and the level of cover you choose. Using a broker helps you compare various providers to find a rate that fits your budget while maintaining high standards of protection.

Is accidental damage by a tenant covered by a standard landlord policy?

Accidental damage isn’t usually covered by a basic policy and must be added as an optional extra. Standard insurance focuses on major events like floods or fires rather than smaller mishaps. If you’re worried about tenants damaging worktops or breaking windows, you should check that your first time landlord insurance checklist includes this specific type of protection. It’s an affordable way to avoid paying for frequent, minor repairs yourself.

What is the difference between a residential mortgage and a Buy-to-Let mortgage for insurance?

Residential mortgages are for homes you occupy, whereas Buy-to-Let mortgages are for investment properties. Your insurance must reflect this difference because let properties have a higher risk profile for liability and damage. If you have a BTL mortgage but only have residential insurance, your lender may consider you in breach of contract and your insurer could void your policy. Always match your insurance to your specific mortgage type.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Article by

Just Quote Me

JustQuoteMe Ltd is an independent UK insurance brokerage specialising in business and personal insurance solutions. With over 35 years of industry experience, the company provides tailored insurance cover for businesses, landlords, tradespeople, hospitality venues, fleets, and individuals across the UK. Known for its personal service, expert advice, and competitive premiums, JustQuoteMe Ltd works with leading insurers to deliver bespoke policies designed around each client’s unique needs. The company is authorised and regulated by the Financial Conduct Authority (FCA No. 586607) and has built a reputation for trusted, straightforward insurance guidance and long-term client relationships.

by jqm | May 18, 2026 | Insurance

What if a single structural change to your rental property could instantly invalidate your entire insurance policy? Many owners are surprised to find that their standard cover often fails the moment a project exceeds basic cosmetic work. If you are searching for landlord insurance for property undergoing renovation, you likely already feel the pressure of the 30-day unoccupancy limit. It’s a common anxiety, especially since 43% of landlords reported a void period in early 2026. You deserve to know that your capital is safe while the builders are on-site.

This guide will show you how to protect your investment and avoid policy voids while your rental property is being renovated. We’ll explain the vital distinctions between structural and cosmetic definitions and how to maintain liability cover for both workers and the public. You will also learn how to transition smoothly back to standard let property cover once the keys are handed back. Getting the right protection shouldn’t be a complex administrative burden; Just Quote Me for a pragmatic solution that keeps your project moving forward.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Key Takeaways

- Understand why standard policies often fail during building works and how to avoid the “unoccupied” clause trap.

- Discover what specialist renovation insurance covers, including protection for the existing structure and materials stored on-site.

- Learn how to distinguish between cosmetic and structural refurbishments when arranging landlord insurance for property undergoing renovation.

- Get a practical pre-renovation checklist to ensure your contractors are properly insured and your mortgage lender is informed.

- Find out how to access a broad network of UK insurers to secure bespoke protection that standard high-street policies can’t offer.

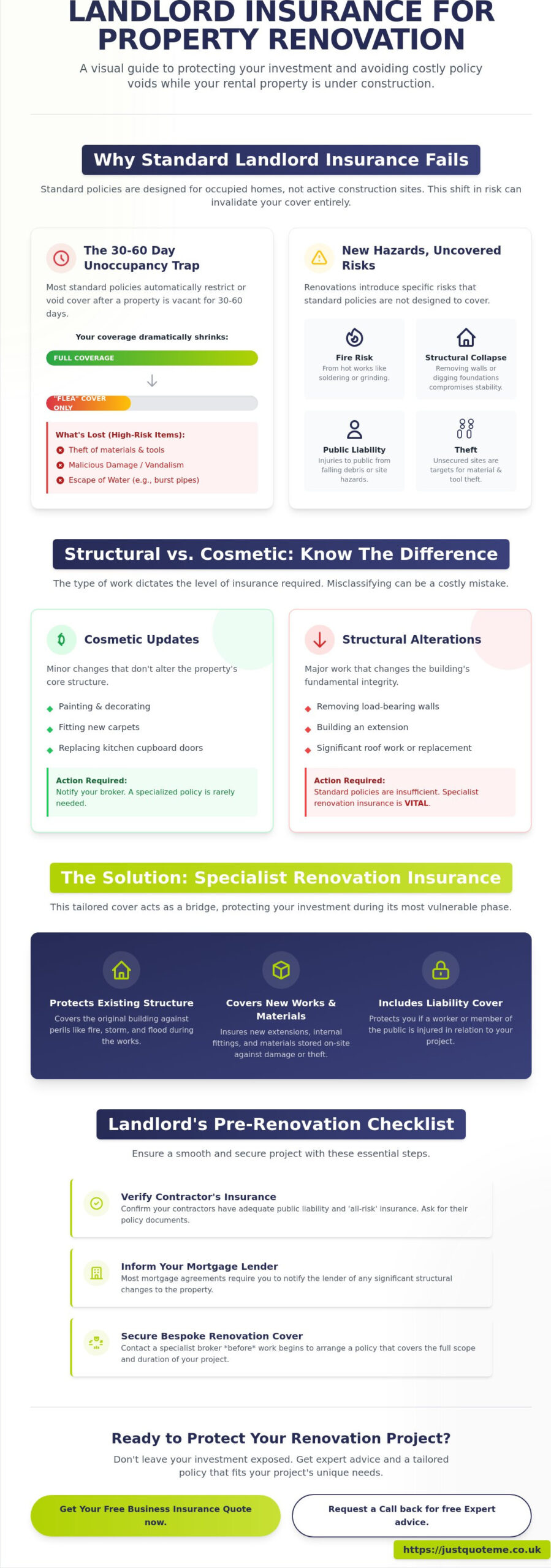

Why Standard Landlord Insurance Fails During Property Renovations

Standard landlord insurance serves a specific purpose: protecting a property that’s occupied and maintained by a tenant. Once you introduce builders, scaffolding, and vacant rooms, the risk profile shifts entirely. Most standard policies aren’t built to handle construction sites. Insurers price their risk based on the property being a home, not a workplace. Failing to update your policy to landlord insurance for property undergoing renovation leaves you exposed to a total policy void if you need to make a claim. Understanding Property Insurance Basics is helpful here; it shows that insurance is a contract based on the disclosure of all material facts. A renovation is a significant material change that your insurer must know about. Specialized landlord insurance for property undergoing renovation ensures that your investment remains protected during these high-risk periods.

The 30-60 Day Unoccupancy Trap

Insurers view a property without a permanent resident as a high-risk asset. Most standard landlord policies include a clause that limits coverage if the property is vacant for more than 30 or 60 consecutive days. Once this threshold is crossed, many insurers strip your protection back to “FLEA” cover only. This covers Fire, Lightning, Explosion, and Aircraft. While these are serious events, this limited cover removes protection for the most common renovation risks. You lose cover for theft, malicious damage, and escape of water from burst pipes. In a renovation setting, these are the very incidents most likely to occur.

Structural Alterations vs. General Maintenance

It’s vital to distinguish between cosmetic updates and structural changes. Cosmetic work like painting, fitting new carpets, or replacing kitchen cupboard doors typically falls under general maintenance. You should still notify your broker, but these rarely require a specialized policy shift. Structural work is different. If you’re removing load-bearing walls, adding an extension, or performing roof work, you’re changing the integrity of the building. Standard residential letting insurance is usually insufficient for these projects. Without the correct disclosure, your insurer can argue that the risk has changed so much that the original policy is no longer valid.

Renovations introduce specific hazards that standard policies often ignore:

- Fire risk: Hot works like soldering or grinding significantly increase the chance of accidental fires.

- Structural collapse: Removing walls or digging foundations can compromise the entire building’s stability.

- Theft: Unsecured sites are prime targets for the theft of expensive building materials and tools.

- Liability: You may be held responsible if a member of the public is injured by falling debris or site hazards.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Specialist Cover: What Renovation Insurance Includes in 2026

Specialist renovation insurance acts as a tactical bridge between standard property protection and a full construction policy. While Standard Insurance Coverage typically focuses on the risks associated with a finished, occupied home, renovation cover accounts for the unique hazards of an active site. It provides a flexible framework that adapts as your project evolves from a stripped-back shell to a completed rental unit. Obtaining landlord insurance for property undergoing renovation ensures that your capital isn’t left exposed during the most vulnerable stage of your investment’s lifecycle.

Protecting the Existing Structure and New Works

One of the most significant gaps in standard policies is the failure to distinguish between the “shell” of the building and the “works in progress.” Specialist cover protects the original structure against traditional perils like fire and storm while simultaneously covering the new extensions, materials, and internal fittings. This is where contractors all risk insurance becomes essential. It covers the cost of repairing or replacing work that’s damaged before completion, such as a newly installed roof destroyed by a gale or copper piping stolen before the property is secured.

Correct valuation is critical in 2026. With high inflation affecting construction materials and labor, you must insure the property for its rebuild cost rather than its market value. Your policy should reflect the total value of the existing building plus the total contract value of the renovations. Securing comprehensive development cover ensures that if a total loss occurs mid-build, you have sufficient funds to clear the site and start again.

Liability Risks During the Renovation Phase

Even if your property is empty, your legal responsibilities don’t disappear. In fact, they often increase. Public liability insurance is a core component of renovation cover, protecting you against claims from third parties. This includes neighbors whose property might be damaged by your contractors or even trespassers who injure themselves on your site. Once a renovation begins, the property effectively becomes a construction site, shifting the liability from standard domestic risks to those associated with active building hazards.

Consider these key inclusions for a 2026 specialist policy:

- Materials on-site: Protection for expensive items like boilers, kitchens, and timber before they’re fitted.

- Unfixed materials off-site: Cover for items stored in a garage or warehouse prior to installation.

- Environmental standards: Support for meeting new 2026 EPC and environmental compliance during the rebuild.

- Alternative accommodation: Liability protection if a structural failure impacts a neighboring property’s habitability.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Navigating Structural vs. Cosmetic Refurbishments

Choosing the right landlord insurance for property undergoing renovation depends heavily on the scope of work you intend to carry out. Insurers generally categorize projects into two brackets: cosmetic and structural. Minor refurbishments, such as installing a new bathroom suite, replacing kitchen cabinets, or refreshing the internal décor, are often seen as low-risk. In many cases, these only require a simple policy note to your existing provider. However, the moment you move a load-bearing wall or alter the roofline, you have crossed a threshold into major works. These projects require a dedicated policy shift to reflect the increased risk of building failure or prolonged exposure to the elements.

The duration of the project also dictates your cover options. A two-week kitchen refit carries a different risk profile than a six-month basement excavation. For longer projects, you may need specialist renovation insurance that accounts for building code compliance and the potential for phased handovers. If your renovation is part of a wider development, you must also ensure that your Planning Permission and Building Regulations approval are in place, as many insurers will void a claim if the work is found to be unauthorized.

When a Minor Refit Becomes a Major Risk

The tipping point between “light” and “heavy” refurbishment often occurs when the property is no longer watertight. If you’re “opening up” the building by removing windows or sections of the roof, standard cover is no longer sufficient. Light refurbishment policies offer a cost-effective middle ground for landlords who are doing more than just painting but aren’t yet into major structural territory. To stay protected, follow this simple assessment checklist:

- Are you altering the external footprint of the building?

- Will the property be unsecured or open to the weather at any point?

- Are you hiring subcontractors who require their own liability oversight?

- Does the project value exceed 20% of the property’s total rebuild cost?

Specialist Protection for Complex Projects

For large-scale works, you must look beyond standard letting policies. Many UK renovations involve Joint Contracts Tribunal (JCT) agreements, which dictate specific insurance requirements for both the employer and the contractor. In these instances, securing professional builders insurance is often a contractual necessity. This ensures that the liability is clearly defined between your own interests and those of the construction firm.

Phased renovations present a unique challenge. If you’re renovating one flat in a block while others remain tenanted, you need a policy that balances contractors all risk insurance with active landlord liability. This prevents gaps in cover that could arise if a renovation accident in an empty unit causes damage to a tenanted one. Managing these complexities is where a specialist broker adds the most value, ensuring your landlord insurance for property undergoing renovation is fit for purpose throughout every phase of the build.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Managing Your Risks: A Landlord’s Pre-Renovation Checklist

Securing the right landlord insurance for property undergoing renovation is only the first step in protecting your capital. You must also implement a rigorous risk management strategy to ensure your cover remains valid throughout the build. Before any demolition begins, notify your mortgage lender. Most UK lenders require formal notification of major works, and failure to inform them can lead to a technical breach of your mortgage deed. You should also document the property’s current state. Take high-resolution photographs of every room, external wall, and the roof. These images serve as vital evidence if a dispute arises regarding whether damage was pre-existing or caused by the renovation process.

Schedule regular site visits, at least once a week, to ensure the property remains safe and secure. Insurers often require these inspections as a condition of your cover. During these visits, check that the site is tidy, waste is being managed, and no flammable materials are left near heat sources. In 2026, insurers are placing greater emphasis on legal compliance; ensure you have up-to-date fire safety protocols and that all gas and electrical certificates are maintained where applicable. This proactive approach not only protects the building but also demonstrates to your provider that you are a responsible risk, which can help when you seek competitive insurance rates for future projects.

Vetting Your Contractors and Their Cover

Never assume your builder’s insurance is sufficient to protect your interests. You must verify their public liability and employers liability certificates before they set foot on-site. Specifically, check the limit of indemnity; a £2 million limit may seem high, but it can be quickly exhausted in a major structural claim. If they are using subcontractors, you must ensure that tradesman insurance is active for every individual firm involved. Relying solely on a contractor’s policy is a dangerous gamble; if their policy lapses or they breach a condition, you could be left with no recourse for damage they cause to your property.

Securing the Site to Reduce Premiums

A secure site is a cheaper site to insure. Implement visible security measures like heavy-duty perimeter fencing and smart, battery-operated site alarms that alert your phone to unauthorized entry. For plumbing works, ensure your policy includes “Trace and Access” cover. This is essential for locating the source of a leak behind walls or under floors without you bearing the full cost of the destructive search. High-quality site management and clear fire safety protocols, such as “hot works” permits for any welding or soldering, significantly reduce the likelihood of a catastrophic claim. By treating the renovation as a professional workplace rather than a DIY project, you maintain the integrity of your landlord insurance for property undergoing renovation. To better understand the technical and compliance standards required for such professional sites, you can visit The Testing Lab PLC.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Securing Bespoke Protection with Just Quote Me

Just Quote Me brings over 30 years of experience to the UK property and construction insurance market. We understand that a renovation project isn’t just a building site; it’s a significant financial commitment that requires a specialized safety net. Finding the right landlord insurance for property undergoing renovation shouldn’t feel like an administrative burden. We provide access to a broad network of top UK insurers, many of whom don’t offer their specialized products through standard high-street brokers or automated platforms. Our role is to bridge the gap between standard landlord insurance and the specific, high-risk requirements of a property under development.

Why a Broker Beats an Online Comparison Site

Algorithms often struggle with the nuances of structural works. Online comparison sites are designed for standard risks; they rarely account for the complexities of a basement conversion or a phased roof replacement. We offer professional risk assessment consultations that look at your unique property and project timeline. Our regional expertise in Staffordshire and the West Midlands allows us to understand the specific nuances of local property stock, from Victorian terraces to modern apartment blocks. Once your project reaches completion and the building inspector provides the final sign-off, we manage the seamless transition back to standard residential letting insurance, ensuring you’re never left with a gap in cover.

Finalizing Your Cover and Starting Your Project

The process of getting a bespoke quote through Just Quote Me is designed to be efficient and straightforward. We don’t just set your policy and walk away. We understand that construction projects rarely go exactly to plan. If your project timeline changes or you decide to increase the scope of the works mid-build, we handle the mid-term adjustments on your behalf. This human-centric approach removes the stress of dealing with call centers and automated systems. We act as your steady hand in a complex market, managing the administrative weight so you can focus on the successful delivery of your build.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Secure Your Property Project Today

Navigating the transition from a rental home to a construction site requires more than just a standard policy. You’ve learned that standard cover often fails during building works due to unoccupancy clauses and structural exclusions. By choosing landlord insurance for property undergoing renovation, you ensure that both the existing structure and the new works remain protected against fire, theft, and liability claims. As an FCA-authorised firm with over 30 years of industry experience, Just Quote Me provides the specialized knowledge needed to bridge this gap. We offer direct access to top UK insurers that high-street brokers often miss; this gives you a steady hand in a complex and evolving market. Don’t let administrative burdens or insurance gaps stall your progress or threaten your capital. Secure your investment with expert landlord cover today so you can focus on completing your build and welcoming new tenants with total confidence.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Frequently Asked Questions

Can I keep my existing landlord insurance during a renovation?

You usually cannot maintain a standard policy without making significant changes. Standard landlord insurance is designed for tenanted properties, and insurers view a construction site as an entirely different risk. You must notify your provider before work begins; they will likely require you to switch to specialized landlord insurance for property undergoing renovation to ensure your building remains protected while it is vacant and under construction.

What happens if a fire occurs while the property is empty for works?

If you haven’t disclosed the renovation to your insurer, they may reject the claim entirely due to a “material change in risk.” If you have the correct cover in place, a fire is typically covered as a core peril. However, if you rely on a standard policy that has lapsed into “unoccupied” status, you might only have basic fire cover while losing protection against theft or water damage.

Do I need different insurance for structural vs. non-structural renovations?

Yes, the type of work dictates the level of cover required. Cosmetic updates like new flooring or painting often only require a simple notification to your broker to keep the policy valid. Structural changes, such as loft conversions or removing load-bearing walls, introduce risks like building collapse. These projects necessitate a dedicated renovation policy that accounts for the increased complexity and liability of major works.

Is renovation insurance more expensive than standard landlord insurance?

Renovation policies generally carry higher premiums because the risks on a building site are much greater than in a tenanted home. Factors such as the presence of “hot works,” unsecured materials, and the lack of a permanent resident increase the likelihood of fire or theft. While the cost is higher, it is a vital investment to prevent your standard policy from being voided during the project.

How long can a property be unoccupied for renovations before cover is restricted?

Most standard policies trigger unoccupancy restrictions after 30 to 60 consecutive days. Once this window passes, your insurer will likely reduce your cover to basic perils only. For any project exceeding this timeframe, you must secure landlord insurance for property undergoing renovation to maintain full protection for the duration of the build.

Does renovation insurance cover my builders’ tools and equipment?

No, your property insurance typically protects the building and the materials that will permanently form part of the structure. It does not cover the tools, plant, or equipment owned by your contractors. You must verify that your builder has their own active tradesman insurance to cover their assets and their own liability while working on your site.

What is the difference between renovation insurance and Contractors All Risk?

Renovation insurance focuses on the existing structure and your liability as the property owner. Contractors all risks insurance is a more comprehensive product that covers the “works in progress” and materials on-site against physical loss or damage. For larger developments, having both ensures that the “shell” of the building and the new construction are equally protected from start to finish.

How do I switch back to normal landlord insurance once the work is done?

You should contact your broker as soon as you receive the final completion certificate from your building inspector. We will then update your policy details to reflect that the property is ready for let. This ensures you have the correct tenant-based liability and rent guarantee protections in place before your first residents move in.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Article by

Just Quote Me

JustQuoteMe Ltd is an independent UK insurance brokerage specialising in business and personal insurance solutions. With over 35 years of industry experience, the company provides tailored insurance cover for businesses, landlords, tradespeople, hospitality venues, fleets, and individuals across the UK. Known for its personal service, expert advice, and competitive premiums, JustQuoteMe Ltd works with leading insurers to deliver bespoke policies designed around each client’s unique needs. The company is authorised and regulated by the Financial Conduct Authority (FCA No. 586607) and has built a reputation for trusted, straightforward insurance guidance and long-term client relationships.

by jqm | May 17, 2026 | Insurance

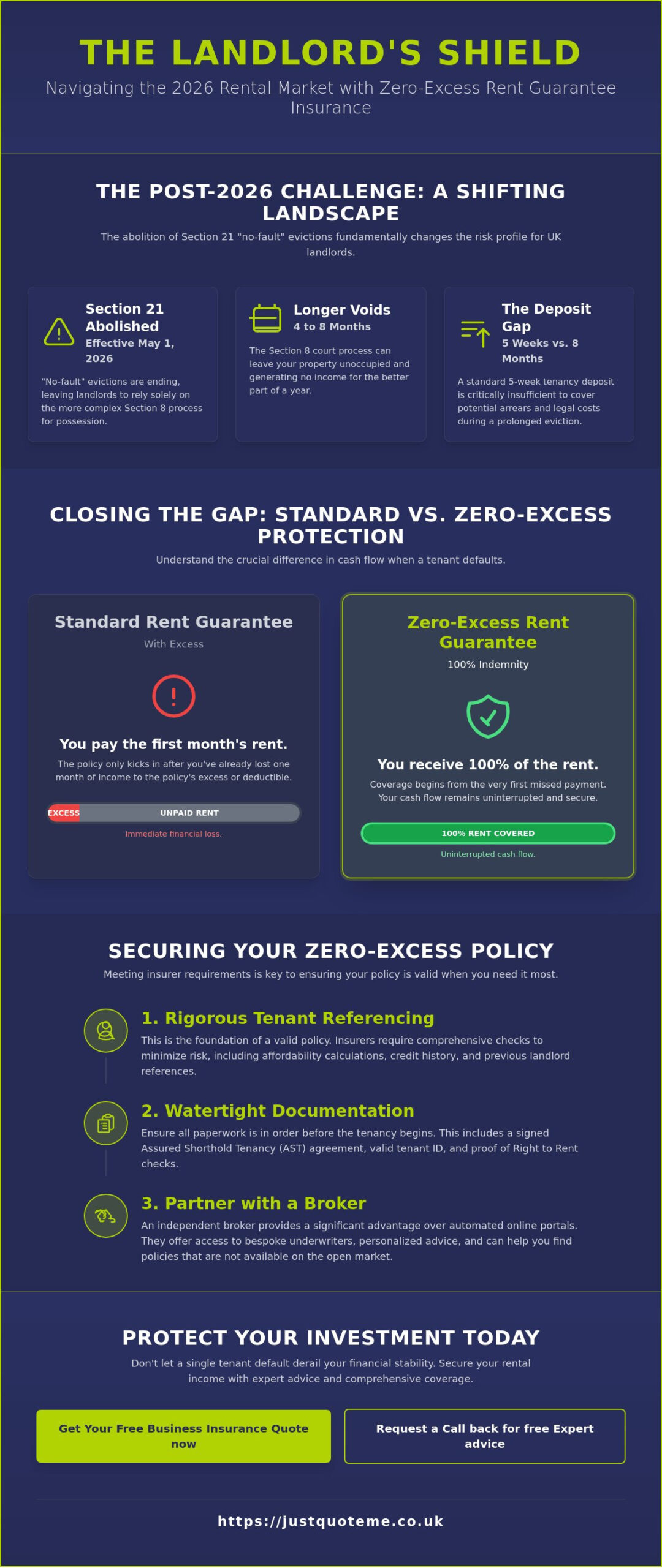

With the abolition of Section 21 “no-fault” evictions as of May 1, 2026, a single tenant default could now leave your mortgage repayments in jeopardy for up to eight months. You likely recognize that the traditional safety nets have shifted, making the financial gap during a Section 8 possession process much harder to manage. Choosing rent guarantee insurance with no excess is the most effective way to close that gap entirely. It ensures that when a tenant stops paying, your coverage kicks in immediately without you having to sacrifice the first month of arrears to a costly deductible.

We understand that unexpected fees and legal complexities are the biggest hurdles to a profitable portfolio. This guide will show you how to eliminate out-of-pocket expenses and maintain a consistent cash flow regardless of tenant behavior. You’ll discover the specific benefits of zero-excess protection under the Renters’ Rights Act 2025 and learn how expert legal handling can take the weight of evictions off your shoulders. Just Quote Me for your landlord protection needs to simplify your administration and secure your professional future.

Key Takeaways

- Understand how the 2026 abolition of Section 21 “no-fault” evictions extends the timeline to regain property and why this makes reliable financial protection essential.

- Learn how rent guarantee insurance with no excess removes the standard one-month deductible, ensuring your cash flow remains uninterrupted from the very first missed payment.

- Identify the rigorous tenant referencing and documentation standards needed to secure a valid policy under the latest 2026 regulations.

- Evaluate the true cost-benefit of zero-excess coverage compared to standard policies, especially when facing a Section 8 court process that can last up to eight months.

- Discover the advantage of using an independent broker to access bespoke underwriters and personalized advice that automated online portals cannot provide.

The Risk of Tenant Default in the 2026 UK Rental Market

The UK rental market in 2026 is fundamentally different from previous years. Legislative shifts and persistent economic volatility have created a landscape where even the most diligent landlords face increased financial exposure. For many, the primary concern is no longer just finding a tenant, but ensuring that the income stream remains uninterrupted. Securing rent guarantee insurance with no excess has become a vital strategy to navigate these uncertainties without losing a month of income to a deductible.

Economic Pressures and Rental Arrears

Tenant stability is under pressure. Rising living costs in 2026 mean that disposable income is tighter than ever, leading to a direct correlation with rental arrears. We’ve seen that even high-earning tenants can suddenly become a liability due to unexpected unemployment or shifting market demands. When a tenant defaults, the financial impact isn’t just the lost rent; it’s the disruption to mortgage schedules and maintenance budgets. Rent insurance serves as a buffer against these systemic risks, providing a layer of security that a standard tenancy deposit simply cannot match. It’s no longer enough to rely on a tenant’s history when the broader economic environment is so unpredictable.

Legislative Hurdles for Modern Landlords

The Renters’ Rights Act 2025 has significantly altered the eviction process. As of May 1, 2026, the abolition of Section 21 “no-fault” evictions means landlords must now rely exclusively on the Section 8 possession process. This change has extended the timeline for regaining property possession to between four and eight months from the first missed payment. Legal expenses have climbed as court hearings become mandatory for most possession orders. Additionally, the 2026 claims process often involves mandatory mediation, adding another administrative layer to an already complex situation. These delays mean that a landlord without protection could be forced to cover mortgage payments out of pocket for the better part of a year.

Traditional deposit protection, usually capped at five weeks’ rent, is insufficient when faced with an eight-month eviction timeline. Without rent guarantee insurance with no excess, a landlord could be looking at thousands of pounds in lost income plus legal fees before the property is back on the market. This financial friction often leads to significant stress, especially for those who rely on rental income to cover mortgage payments. Having a residential letting insurance policy in place provides more than just financial reimbursement. It offers the psychological peace of mind that your investment is protected by experts who handle the legal heavy lifting. You won’t have to navigate the court system alone or worry about how a single tenant’s financial misfortune will impact your own credit standing.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice

What is Rent Guarantee Insurance with No Excess?

Rent guarantee insurance, also known as rent protection, is a specialized policy designed to reimburse landlords if a tenant fails to pay their monthly rent. While standard landlord insurance typically covers physical damage to the property or liability issues, it rarely includes lost income due to tenant default. This is where rent guarantee insurance with no excess steps in to fill the gap. It ensures that your mortgage repayments and maintenance costs don’t fall behind just because a tenant’s circumstances have changed.

Defining the Zero-Excess Advantage

In most insurance sectors, an excess is the amount you agree to pay toward a claim. If you have a £250 or £500 excess on a rent claim, you’re essentially losing a significant portion of your profit margin for that month. For a single-property landlord, this out-of-pocket cost can be the difference between breaking even and falling into debt. Zero-excess rent guarantee insurance is defined as 100% indemnity, meaning the insurer pays the full amount of the arrears from the very first penny. By removing this financial friction, you receive the total rent owed without any deductions. It makes the recovery process much smoother.

Core Policy Features to Look For

When selecting a policy in 2026, you need to look beyond the premium. Most robust plans offer monthly claim limits between £2,000 and £2,500 to reflect the current market rates. You can typically choose from cover durations of 6, 12, or 15 months. This flexibility is critical. Since evictions can now take up to 8 months, shorter policies might leave you exposed. A high-quality policy will also integrate with legal expenses insurance to ensure you aren’t paying for solicitors out of your own pocket.

The official government guide to renting outlines the legal responsibilities landlords must uphold, and a good policy supports these by including mediation services. These services aim to resolve disputes before they reach the court stage, potentially saving months of lost time. If you’re unsure which level of cover fits your portfolio, you can always explore our tailored landlord solutions to find a match. Combining rent guarantee insurance with no excess with expert legal handling creates a comprehensive safety net for your investment.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice

Comparing Standard vs. Zero-Excess Rent Protection

Choosing between a standard policy and rent guarantee insurance with no excess is more than just a matter of premium cost; it’s a strategic decision about your cash flow. Many landlords find that standard policies, while appearing cheaper on the surface, contain hidden financial friction that only becomes apparent during a claim. These policies often include a one-month excess or a fixed deductible that you must cover before the insurer pays a penny. In a market where margins are already squeezed by taxation and rising maintenance costs, losing a full month of rent to an excess can turn a managed risk into a significant financial setback.

The Financial Breakdown

To understand the real-world impact, consider a hypothetical scenario where a tenant defaults on a property with a monthly rent of £1,200. If the tenant stops paying for three months, the total arrears reach £3,600. With a standard policy carrying a £500 excess, your net payout would be £3,100, leaving you with a £500 shortfall. If the policy has a ‘first month’ excess, you might receive nothing for the initial 30 days of the default. This creates an immediate cash flow gap that you must bridge to meet mortgage obligations. In contrast, rent guarantee insurance with no excess provides the full £3,600. You receive 100% of the rent owed from the very first day of arrears, ensuring your financial planning remains uninterrupted.

Who Benefits Most from No-Excess Cover?

Individual landlords with tight mortgage margins are often the most vulnerable to the “first month” gap. If your rental income is your primary means of paying the property’s mortgage, any delay or deduction in payment can impact your credit standing. Professional landlords managing high-turnover HMOs also benefit significantly. Because the risk of default is distributed across multiple rooms, the frequency of claims can be higher; paying an excess on every claim would quickly erode the portfolio’s annual yield. Institutional investors seeking predictable annual returns also prefer zero-excess models because they eliminate the volatility associated with deductible fees and administration costs.

Beyond the immediate payout, standard policies sometimes hide additional costs in the form of administration fees or limited legal cover. We focus on providing a transparent experience where the value is clear from the start. If you want to avoid the administrative burden of calculating deductibles during a crisis, Just Quote Me for a straightforward, zero-friction solution. By removing the excess, you ensure that your residential letting insurance works exactly as intended: as a complete replacement for your lost income.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice

Eligibility and How to Secure a No-Excess Policy

Securing rent guarantee insurance with no excess requires more than just paying a premium. Because the insurer assumes 100% of the financial risk from day one, the eligibility criteria are rigorous. You must prove that your tenant is financially stable and that the tenancy is legally sound. If you’re switching from a standard residential letting insurance policy, understanding these requirements early prevents claim rejections later. Insurers view the quality of the tenant as the primary indicator of risk, so cutting corners during the initial setup isn’t an option.

Tenant Referencing Requirements

Insurance providers mandate a professional reference check for every adult tenant named on the agreement. This involves a formal credit search to identify CCJs or insolvencies, employment verification to confirm a stable income, and references from previous landlords. If a tenant’s income is less than 2.5 times the monthly rent, a guarantor is usually required to bridge the gap. This guarantor must pass the same level of scrutiny. The quality of these references directly dictates whether you qualify for a zero-excess product, as insurers only offer this level of protection to the most reliable tenant profiles.

The Application Process

Securing your policy involves a logical four-step sequence. First, conduct the professional reference check through an approved agency before the tenant moves in. Second, ensure you have a valid written tenancy agreement in place; under the 2026 regulations, these are typically periodic tenancies from day one. Third, obtain your quote for rent guarantee insurance with no excess through a specialist broker who can access exclusive underwriters. Finally, maintain meticulous records of rent statements and all tenant correspondence. It’s important to be aware of the 90-day waiting period. If you apply for cover for an existing tenant who has already moved in without prior insurance, most providers won’t allow a claim for defaults occurring within the first three months. This prevents landlords from seeking cover only after a tenant starts struggling.

You can switch to a zero-excess policy mid-tenancy, provided the tenant has a clear payment history for at least the last six months. Documentation is everything in the 2026 market. If you’re ready to secure your income, get started with a specialist landlord policy today to ensure you’re fully eligible before the next rent due date.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice

The Broker Advantage: Finding Bespoke Rent Protection

While many direct insurers promote a one-size-fits-all product, they often lack the flexibility to offer truly bespoke terms. Independent brokers act as a bridge to “broker-only” underwriters who specialize in high-value, zero-friction products. These specialist providers often reserve their best rent guarantee insurance with no excess deals for brokers because they trust the intermediary’s ability to verify tenant referencing and property standards. This access allows you to secure a policy that isn’t just a generic template; it’s a precise financial tool tailored to the specific risks of your portfolio. By working with a broker, you gain access to a wider market of underwriters who are willing to provide full indemnity without the standard deductibles found on comparison sites.

Personalised Support vs. Automated Systems

In the middle of a stressful tenant dispute, an automated online portal is a poor substitute for a knowledgeable advisor. You need a steady hand to help interpret complex policy wording and ensure your claim documentation is flawless. We provide regional expertise across the West Midlands and Staffordshire, offering a human-centric alternative to impersonal algorithms. A broker understands the local market nuances and can advocate on your behalf if a claim becomes complicated. This level of support simplifies the administrative burden. It allows you to focus on managing your properties while we handle the technicalities with the insurer. We don’t just provide a policy; we manage the complex administrative burdens so you don’t have to.

Customising Cover for Unique Portfolios

Standard portals often struggle with non-standard properties or diverse tenant types. If your portfolio includes HMOs or properties with specific architectural features, a broker can customize your cover to include risks that generic policies might exclude. This is particularly relevant for landlords who also manage commercial assets, such as those requiring thatched pub insurance or shop cover. A broker ensures that your rent guarantee insurance with no excess integrates seamlessly with your broader residential letting insurance, creating a cohesive safety net that leaves no room for unexpected out-of-pocket costs.

Your Next Steps for Secure Income

As we manage the regulatory changes of 2026, the value of predictable cash flow is higher than ever. Choosing a zero-excess policy is a pragmatic decision that eliminates the “first month” financial gap and protects your ROI against the extended timelines of the Section 8 process. Having the right protection in place is the foundation of long-term stability. Just Quote Me is here to ensure that your insurance works for you, providing the security you need in an evolving market. Secure your income today and eliminate the friction of tenant defaults.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice

Secure Your Rental Income for the Long Term

The 2026 rental market demands a proactive approach to income protection. With the Section 21 “no-fault” eviction process now a thing of the past, the financial burden of tenant default falls more heavily on landlords. By opting for rent guarantee insurance with no excess, you ensure that your cash flow remains consistent and your investment stays profitable. You don’t have to navigate these complex legislative changes alone. Our team provides the expert guidance needed to bridge the gap between missed payments and legal resolution.

As an FCA-authorised independent broker with over 30 years of industry experience, we provide more than just a policy. We offer a steady hand and access to a broad network of top UK insurers to find the specific terms that fit your portfolio. Our goal is to simplify your administrative burden and provide the security you need to grow your business with confidence. Protect your professional future and ensure your monthly payments are never in doubt. Just Quote Me for expert landlord protection and experience the reliability of a partner who understands your needs. We’re ready to help you thrive in this new regulatory environment.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice

Frequently Asked Questions

Is rent guarantee insurance the same as landlord insurance?

No, these are two distinct types of protection. Standard landlord insurance focuses on the physical structure of your building and your liability as a property owner. In contrast, rent guarantee insurance with no excess specifically protects your income stream by replacing lost rent if a tenant defaults. Most professional landlords choose to hold both policies to ensure they’re covered for both property damage and the sudden loss of monthly rental payments.

Does “no excess” mean I get every penny of the missing rent back?

Yes, you’ll receive the full amount of the monthly rent owed up to the specific limits stated in your policy. While standard policies often deduct the first month’s rent as an excess, a no-excess policy ensures you don’t lose that initial income. As long as the claim falls within your monthly payout cap, which is often around £2,500, you’ll receive 100% of the arrears without any deductions or out-of-pocket costs.

Can I get rent guarantee insurance for a tenant who is already in arrears?

No, you can’t obtain cover for a tenant who is already failing to pay their rent. Insurers require that the tenancy is “clear” at the point the policy begins. If your tenant has already missed a payment, they’re considered a known risk and will be excluded from new coverage. This is why it’s vital to secure your policy at the start of a tenancy or while the tenant is fully up to date.

What legal expenses are covered under a rent protection policy?

Most policies cover a wide range of costs associated with regaining possession of your property. This typically includes solicitor fees, court filing costs, and the expenses related to professional bailiffs if they’re required. Legal cover often reaches limits between £50,000 and £100,000. These funds are essential for navigating the Section 8 process, especially as court hearings have become a mandatory requirement for most evictions in the 2026 market.

How long does it take for a rent guarantee claim to be paid?

Payouts usually begin once a full month of rent has been missed and the claim has been verified. While the initial administration can take a few weeks, most insurers aim to align their payments with your original rent due dates thereafter. Using a specialist broker can often speed up this process, as they help ensure all your documentation is correct from the first submission, reducing the chance of back and forth delays.

Do I need a new policy every time I get a new tenant?

You don’t necessarily need a brand-new policy, but you must notify your insurer and provide new referencing for the incoming tenant. Each tenant must pass the specific credit and background checks to remain eligible for rent guarantee insurance with no excess. If you fail to update the policy details or reference the new tenant correctly, your cover will be void. It’s best to treat every new tenancy as a fresh application.

Will this insurance cover my legal costs if I have to go to court?

Yes, the legal expenses portion of the policy is specifically designed to cover court-related costs. Since the abolition of Section 21 evictions, landlords must attend court hearings to secure a possession order under Section 8. Your insurance will pay for the legal representation required to present your case. This ensures you aren’t forced to pay thousands of pounds in legal fees just to regain control of your own rental property.

Can I buy rent guarantee insurance as a standalone policy?

Yes, many providers offer rent protection as a standalone product, though it’s frequently purchased as an add-on to buildings insurance. Buying it standalone gives you the flexibility to choose a specialist underwriter who offers better terms, such as a zero-excess clause. We often recommend reviewing standalone options if your current buildings provider doesn’t offer the high-limit rent protection or legal support required for the modern 2026 rental landscape.

Article by

Just Quote Me

JustQuoteMe Ltd is an independent UK insurance brokerage specialising in business and personal insurance solutions. With over 35 years of industry experience, the company provides tailored insurance cover for businesses, landlords, tradespeople, hospitality venues, fleets, and individuals across the UK. Known for its personal service, expert advice, and competitive premiums, JustQuoteMe Ltd works with leading insurers to deliver bespoke policies designed around each client’s unique needs. The company is authorised and regulated by the Financial Conduct Authority (FCA No. 586607) and has built a reputation for trusted, straightforward insurance guidance and long-term client relationships.

by jqm | May 16, 2026 | Insurance

Did you know that underinsurance remains a critical risk for multi-unit buildings, with experts recommending professional rebuild assessments every three to five years to avoid the “average clause” during a claim? As a property manager or freeholder, you already understand that managing these assets is a complex balancing act of legal compliance and financial precision. It’s often a struggle to identify exact responsibilities for different parts of the building while trying to keep service charge accounts manageable for every resident. This 2026 guide simplifies the process of securing insurance for a block of flats uk, ensuring your policy satisfies mortgage lenders and aligns with the transparency requirements of the Leasehold & Freehold Reform Act. We’ll explore specialist protections like Engineering Inspection and explain how to navigate the current 12% Insurance Premium Tax environment. You will learn how to provide the data-led risk management evidence that insurers now demand while securing a competitive premium that never compromises on essential coverage for your leaseholders.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice

Key Takeaways

- Understand why a unified policy is mandatory for multi-unit buildings and how it differs from standard residential buildings insurance.

- Discover how to safeguard the interests of leaseholders and mortgagees using the ‘Joint Insured’ clause within your management structure.

- Learn how to accurately calculate your sum insured by focusing on reinstatement costs rather than market value to avoid the risks of underinsurance.

- Identify the essential components of insurance for a block of flats uk, including property owners’ liability and coverage for communal areas.

- Gain the confidence to evaluate excess levels and compare quotes effectively to find a balance between competitive premiums and robust protection.

What is Insurance for a Block of Flats in the UK?

A block of flats isn’t just a collection of individual homes; it’s a single structural entity with shared liabilities. Therefore, insurance for a block of flats uk is designed as a master policy that covers the entire building fabric from the foundations to the roof. Standard buildings insurance fails here because it doesn’t account for the complex Legal Responsibilities: Freeholders, RTMs, and Management Companies established in the property’s lease. Without a unified policy, you risk gaps in coverage where a claim in a communal hallway might not be covered by any individual flat owner’s insurance. This type of protection ensures that the structural integrity of the entire building is maintained under one umbrella.

Most leasehold agreements legally mandate that the building is insured under one comprehensive policy. This ensures that every mortgagee’s interest is protected and that the building can be fully reinstated after a major event like a fire or flood. It eliminates the chaos of trying to coordinate multiple insurers when a single incident affects several units at once.

Specialist vs. Standard Property Insurance

Standard residential policies often exclude communal areas like lift shafts, shared gardens, and stairwells. A specialist block policy treats these as integral parts of the risk. It’s much more efficient to have one insurer handling the entire structure. If a leak starts in flat A and damages flat B, having a single insurer prevents the long, expensive legal disputes that occur when multiple companies try to shift blame. We usually recommend ‘All Risks’ cover rather than simple ‘Perils-based’ insurance. While perils-based cover only protects against specific named events like fire or theft, ‘All Risks’ provides a broader safety net for any accidental damage unless specifically excluded. This level of detail is a vital component of commercial property insurance for landlords managing multi-unit sites where the unexpected is common.

Who is Responsible for Arranging the Policy?

The duty to arrange insurance usually falls on the freeholder. They own the land and the building’s shell, so they have a vested interest in protecting the structural integrity. However, many blocks are managed by a Residents’ Management Company (RMC) or a Management Company (ManCo) appointed by the freeholder. In these cases, the agent handles the administration while recharging the premium to leaseholders via service charges.

Right to Manage (RTM) groups also hold significant responsibility. When leaseholders exercise their legal right to take over management, they also inherit the obligation to maintain adequate insurance for a block of flats uk. Failing to do so is a breach of the lease and can lead to severe legal consequences. It’s a heavy administrative burden, but it ensures that the residents maintain control over their protection and costs. Just Quote Me to simplify your search for the right policy and ensure every legal box is ticked.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice

Essential Coverage Components for Multi-Unit Buildings

Securing insurance for a block of flats uk requires a granular understanding of both physical and financial risks. The foundation of any policy is buildings insurance, which covers the cost of repairing or rebuilding the structure following damage from fire, flood, or subsidence. Because building costs remain volatile in 2026, it’s vital to base your sum insured on a professional rebuild assessment conducted within the last three to five years. This prevents the “average clause” from reducing your claim payout if the property is found to be underinsured.

Property owners’ liability is equally critical. This protects the freeholder or management company against claims for injury or property damage occurring in communal areas like stairwells, car parks, and gardens. If a visitor trips on a loose carpet in a hallway, the legal costs and compensation can be astronomical. A robust policy also includes alternative accommodation for residents if a major incident makes the building uninhabitable. For those managing mixed-use blocks, loss of rent cover ensures that the income stream from commercial ground-floor units remains stable while repairs are carried out. You can find more detail on protecting your rental income via our landlord insurance solutions.

Engineering Inspection and Lift Insurance

If your block includes a lift, you have a statutory legal obligation under LOLER (Lifting Operations and Lifting Equipment Regulations) to have it inspected by a competent person every six months. Standard buildings insurance doesn’t typically cover these inspections or sudden mechanical breakdowns. An engineering policy provides the necessary certification and covers the repair of communal machinery, including boiler systems and pressurized tanks. Integrating this into your primary policy simplifies your administration and ensures you remain compliant with UK safety laws. Expert advice is often the quickest route to securing a tailored policy that includes these specific technical requirements.

Directors & Officers (D&O) Liability

Many property managers overlook the personal risks faced by directors of Residents’ Management Companies (RMC) or Right to Manage (RTM) groups. These individuals are often volunteers, yet they are personally liable for “wrongful acts,” including allegations of mismanagement, breach of duty, or failure to comply with the Leasehold & Freehold Reform Act 2026. D&O insurance covers the legal defense costs and awards for such claims, ensuring that a director’s personal assets aren’t at risk. While this protects the individuals, management professionals may also want to consider Professional Indemnity Insurance to cover errors in professional advice or service delivery. Protecting your leadership team is just as important as protecting the bricks and mortar when arranging insurance for a block of flats uk.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice

Legal Responsibilities: Freeholders, RTMs, and Management Companies

The legal architecture of a multi-unit building requires a policy that recognizes multiple stakeholders simultaneously. Central to this is the ‘Joint Insured’ clause. Unlike a standard homeowner policy, insurance for a block of flats uk must name the freeholder, the management company, and the collective interests of the leaseholders. This structure ensures that if one party inadvertently invalidates the policy through an act of negligence, the interests of the other parties remain protected. It’s a vital safety net that prevents a single individual’s mistake from leaving the entire building without cover.

When a Right to Manage (RTM) company takes over, maintaining insurance continuity is a primary legal duty. You must ensure there’s no gap during the transfer of responsibilities, as any lapse could breach the terms of every individual lease in the building. Compliance with the Landlord and Tenant Act is also non-negotiable. This legislation dictates that insurance costs recovered from residents must be “reasonably incurred.” In the 2026 regulatory environment, you’re expected to demonstrate that you’ve tested the market to find the best value, rather than simply renewing the first quote you receive. A broker acts as an essential mediator here, balancing the demands of the freeholder with the cost-sensitivity of the leaseholders.

Satisfying Mortgage Lenders

High street and commercial lenders have strict requirements before they’ll release funds for a flat purchase. They typically demand ‘Non-Invalidation’ and ‘Vesting’ clauses. These clauses guarantee that the lender’s interest in the property stays secure even if a leaseholder breaches a policy condition. Because every lender has slightly different criteria, a broker is far better equipped to navigate these demands than a direct insurer. We ensure the policy wording matches the specific requirements of the UK’s major lending institutions, preventing delays in property sales or refinancings.

Managing Service Charges and Premiums

Under the Leasehold & Freehold Reform Act 2026, transparency is the new standard for service charges. Property managers must provide clear breakdowns of how premiums are calculated and justify any administrative fees. Most leases allow for the full recovery of insurance costs through the service charge account, but this doesn’t give managers a blank check. You need to show that you’ve balanced the premium cost against the quality of protection. For mixed-use developments where shops sit beneath residential units, the complexity increases. In these scenarios, aligning your block policy with specialized Commercial Property Insurance ensures that the business and residential risks don’t conflict, keeping the service charge fair and transparent for all parties.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice

How to Compare Block Insurance Quotes Effectively

Comparing insurance for a block of flats uk requires looking past the annual premium to ensure the policy actually performs when needed. The most common mistake is confusing market value with the reinstatement value. Market value includes the land’s price and location desirability, whereas the reinstatement value is purely the cost of materials, labor, and professional fees required to rebuild the structure from scratch. If your sum insured is based on market value, you’re likely paying for cover you can’t claim or, worse, leaving yourself dangerously underinsured.

You must also evaluate “Trace and Access” limits carefully. In multi-storey buildings, finding the source of a leak often involves tearing into walls or floors across multiple units. Without adequate Trace and Access cover, the cost of simply locating the problem can exceed the cost of the actual repair. This leaves the service charge account to bridge the gap, which can lead to disputes with leaseholders. A policy that seems cheap on the surface often hides low sub-limits for these essential “hidden” costs.

The Danger of Underinsurance