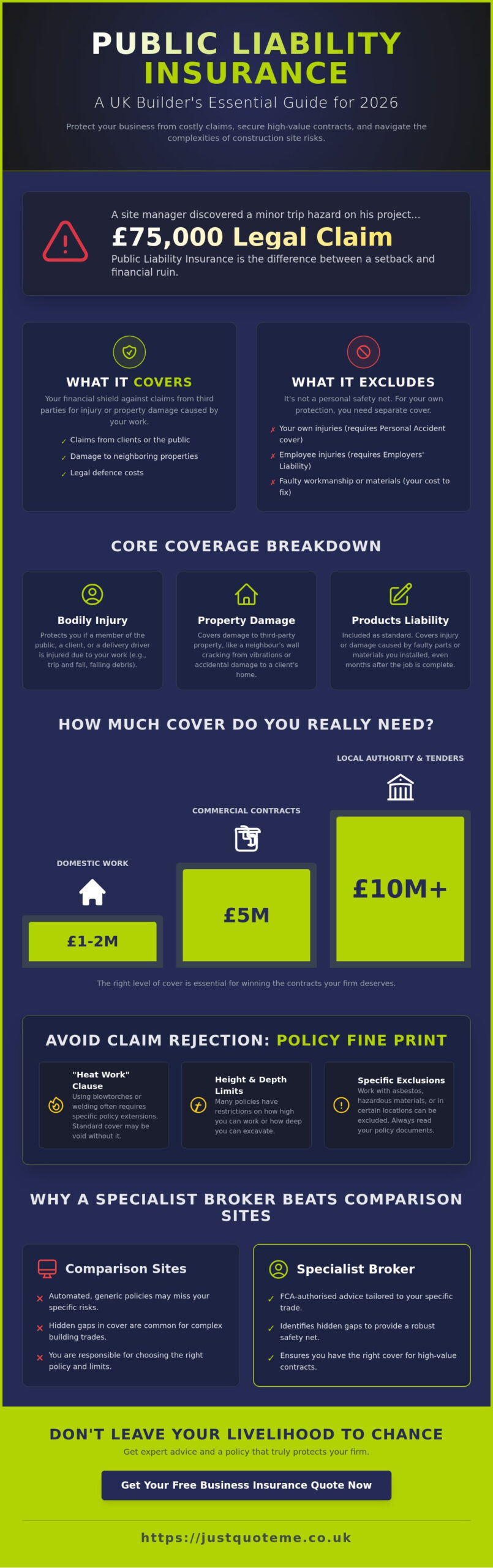

Last Tuesday, a site manager named Dave discovered that a minor trip hazard on his project had escalated into a £75,000 legal claim against his firm. You likely already feel the pressure of rising premiums and the constant worry that your public liability insurance for builders uk might fail you due to complex fine print. It’s a common frustration for tradespeople who just want to get the job done without being bogged down by industry jargon. We understand that your focus should be on the build, not on deciphering fifty pages of technical terms.

This guide ensures you master the essentials to protect your livelihood and secure the high-value contracts your firm deserves. You’ll learn how to satisfy strict local authority tenders while ensuring your tools, plant, and reputation are fully covered. We’ve simplified the process, moving from FCA-authorised advice to practical steps for managing your 2026 costs. By the end of this article, you’ll have a clear roadmap to a policy that actually works when you need it most.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Key Takeaways

- Discover why public liability insurance for builders uk is the essential foundation for protecting your business against accidental injury and third-party property damage claims.

- Learn how to calculate the right level of cover—from £1 million up to £10 million—to ensure you remain eligible for lucrative local authority and commercial contracts.

- Identify critical policy exclusions, such as “Heat Work” and height restrictions, to ensure your coverage remains valid during high-risk construction tasks.

- Understand why a specialist broker offers a more robust safety net than automated comparison sites by identifying hidden gaps in complex building trade risks.

- Master the essentials of 2026 policy requirements to secure your firm’s professional reputation and avoid the rising costs of legal pitfalls.

Understanding Public Liability Insurance for UK Builders in 2026

For any construction professional, public liability insurance for builders uk represents the most critical component of a risk management strategy. This specific type of cover protects your business if a third party, such as a client, a delivery driver, or a member of the public, suffers an injury or property damage due to your work. In the high-risk environment of a UK building site, the potential for accidents is constant. Understanding Public Liability involves recognising your duty of care to ensure that your activities don’t cause harm to others.

This policy serves as the foundation of a comprehensive builders insurance portfolio. While you might be focused on the quality of your brickwork or the precision of your joinery, the Health and Safety Executive (HSE) focuses on site safety standards. According to HSE statistics for 2023/24, there were 51 fatal injuries to workers in the UK construction sector. The HSE sets rigorous benchmarks through the Construction (Design and Management) Regulations 2015, which remain the gold standard for site safety in 2026. Failing to meet these standards doesn’t just invite fines; it increases the likelihood of a liability claim that could end your career.

Is Public Liability Insurance a Legal Requirement for Builders?

The UK government doesn’t legally mandate public liability insurance in the same way it requires Employers Liability insurance under the 1969 Act. However, it’s a commercial necessity. Most local authorities, main contractors, and private homeowners won’t allow you to set foot on a site without proof of valid cover. If you’re a sole trader, you’re personally responsible for any damages awarded against you. Without a liability safety net, a single court case could result in the loss of your home or personal savings. For most tradesmen, public liability insurance for builders uk is the difference between a minor setback and total financial ruin. If you operate as a self-employed professional, understanding your full range of obligations is essential — our guide to sole trader insurance covers everything you need to know about protecting your business in 2026.

How Public Liability Differs from Personal Accident Cover

It’s easy to confuse different types of protection, but the distinction is clear. Public liability insurance acts as a shield against third-party property damage and bodily injury claims arising from your work. It doesn’t pay out if you fall off a ladder and break your own leg. For that, you need personal accident cover. You likely need both to ensure full business continuity. Public liability looks outward to protect your reputation and assets from external claims, while personal accident cover looks inward to support your income if you’re unable to work.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

What Does Builders Public Liability Insurance Actually Cover?

At its heart, public liability insurance for builders uk acts as a financial safety net. It protects your business if a third party suffers an injury or property damage because of your work. While you focus on the build, this policy handles the potential for six-figure claims that could otherwise bankrupt a small firm. Most policies also include “Products Liability” as standard. This is vital because it covers you if a defect in the materials you’ve installed, such as a faulty pipe fitting that bursts months after the job is finished, causes damage to a client’s home.

Bodily Injury and Public Safety on Site

Construction sites are inherently risky environments. A stray piece of timber or a tool left on a walkway can lead to a serious trip and fall. If a delivery driver or a member of the public is injured by falling debris, your policy covers their medical costs and loss of earnings. This cover applies to anyone who isn’t an employee, including pedestrians walking past your scaffolding or a client visiting for a progress update. You’ll need to follow safety protocols, as many insurers include specific clauses regarding “Signage and Hoarding” to ensure you’ve taken reasonable steps to prevent unauthorized access to the site.

Property Damage: Beyond the Building Site

Damage isn’t always confined to the area you’re currently working on. Vibrations from heavy machinery can cause cracks in a neighbor’s wall, or a sudden storm could cause water ingress through an unfinished roof. When Calculating Your Risk, remember that standard policies usually exclude “Care, Custody, and Control.” This means the insurance covers the neighbor’s house or the customer’s existing furniture, but it won’t pay for damage to the specific part of the property you are actually working on at that moment. Accidental damage to underground services is another common headache. Striking a water main or a fiber optic cable can lead to repair bills in the thousands, which your policy provides the necessary cover for, provided you’ve followed standard site survey procedures.

Legal fees are a major part of any claim. Even if a claim against you is groundless, hiring a solicitor to defend your business is expensive. A robust policy for public liability insurance for builders uk covers these legal defense costs, which often exceed the actual compensation amount. This ensures you have professional representation without draining your cash flow. If you’re unsure about the specifics of your project, it’s worth looking at specialist liability options to ensure you aren’t leaving gaps in your protection.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Calculating Your Risk: How Much Public Liability Cover Do You Really Need?

Choosing the right indemnity limit isn’t just a tick-box exercise; it’s a strategic business decision that protects your future. Most insurers offer standard tiers starting at £1 million, moving up to £2 million, £5 million, and £10 million. While a £1 million policy might satisfy the basic legal requirements for a small domestic handyman, it’s often insufficient for established firms in 2026. High inflation has driven up the costs of materials and legal fees significantly over the last few years. A claim that cost £800,000 in 2021 could easily exceed £1.3 million today. Opting for a “cheap” policy with a low limit might save you a few pounds on your monthly premium, but it can leave you personally liable for any shortfall in a claim.

Several factors dictate your premium costs. Your annual turnover is a primary indicator of risk, as higher revenue usually correlates with more active sites and increased exposure. Your trade type also plays a massive role. If you use sub-contractors, insurers will look closely at whether they carry their own public liability insurance for builders uk. If they don’t, your policy must cover their actions, which significantly increases your premium. Being transparent about your business structure ensures you don’t face rejected claims later. Self-employed builders should also review their broader coverage needs — a comprehensive sole trader insurance guide can help you identify the full range of policies required to keep your business protected as it grows.

Contractual Requirements for Tenders

If you’re aiming for government or local council projects, you’ll find that a £5 million limit is the standard entry requirement. These entities won’t even look at your bid if your cover falls short. You should also look for an “Indemnity to Principal” clause. This ensures that if a claim is made against the client due to your negligence, your policy covers them too. As your business moves from small domestic extensions to larger commercial builds, you must scale your public liability insurance for builders uk to match the contract values and client expectations.

Assessing High-Risk Trade Factors

Risk profiles vary wildly across the construction sector. Roofers and demolition specialists naturally pay higher premiums than painters or decorators because the potential for catastrophic damage is greater. A major factor is the risk associated with working at height, where even a dropped tool can cause life-changing injuries or severe property damage. It’s vital to be honest about your activities to ensure your policy remains valid. You should review your indemnity limit annually to ensure it matches the value of your largest current contract. For a broader view of the covers every tradesperson should consider, our tradesman insurance buying guide walks you through the essential protections required to stay legally compliant and financially secure in 2026.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Avoiding Claim Rejection: Common Exclusions and Policy Fine Print

Buying public liability insurance for builders uk is only half the battle. You also need to understand the conditions that could lead an insurer to reject your claim. Many builders assume they’re covered for every mishap on-site, but the fine print often contains specific “conditions precedent” that you must follow. If you ignore these, you’re essentially paying for a policy that won’t pay out when you need it most.

The “Heat Work” exclusion is one of the most frequent causes of rejected claims. If you’re using blowtorches, welding equipment, or angle grinders, your policy likely requires specific safety measures. This often includes having a dedicated fire extinguisher within reach and conducting a “fire watch” for at least 30 minutes after the work finishes. Failing to document this process can void your cover if a fire breaks out later that evening.

Height and depth restrictions are equally critical. A standard policy might limit you to working at heights of 10 metres or depths of 2 metres. If you take on a project involving a four-storey scaffolding rig or deep trenching without a specific rider, you aren’t covered. Always check your schedule before starting a new contract that pushes these boundaries.

You must also distinguish between physical damage and professional errors. Public liability covers you if you drop a brick on a car or a visitor trips over your cabling. It doesn’t usually cover financial losses caused by poor advice or design errors. For that, you need professional indemnity insurance to protect against claims of negligence in your professional services.

- Unvetted Sub-contractors: If you hire “Bona-Fide” sub-contractors, you must ensure they have their own insurance with the same indemnity limits as yours. If they don’t, and an accident occurs, your insurer might refuse to step in.

- Reasonable Precautions: Most policies require you to take “all reasonable steps” to prevent injury or damage. This means following HSE guidelines and keeping a clean site isn’t just good practice; it’s a policy requirement.

Specific Construction Exclusions to Watch For

Standard policies typically exclude hazardous materials like asbestos or silica unless you’ve paid for a specialist extension. You should also look closely at the “Defective Workmanship” clause. While your insurance covers the damage your mistake caused, it won’t pay to fix the mistake itself. For example, if a faulty pipe leaks, the policy pays for the water damage to the floor, but it won’t pay the plumber to reinstall the pipe correctly. To protect work-in-progress against fire, theft, or storm damage, you should consider contractors all risk insurance as a vital secondary layer.

The Role of Employers Liability in Your Policy

If you employ anyone, employers liability insurance is a legal requirement under the 1969 Act. Even if you only hire casual labour for a week or take on an apprentice, you must have this cover in place. The law requires a minimum of £5 million in cover, though most policies provide £10 million as standard. This integrates with your public liability to form a complete tradesman package, ensuring that both the public and your workforce are protected. Managing this liability starts with keeping an accurate register of everyone on your site, regardless of their employment status.

Don’t leave your livelihood to chance by guessing which exclusions apply to your trade. Speak to a specialist broker to ensure your policy matches the reality of your daily work.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Why Independent Brokerage Beats Comparison Sites for Construction Insurance

Comparison websites are designed for high-volume, low-complexity products like car or home insurance. They rely on rigid algorithms that often fail to grasp the nuances of the building trade. When you buy public liability insurance for builders uk through an automated platform, you risk purchasing a generic policy that contains hidden exclusions. These platforms don’t ask about the specific nature of your structural work or the unique risks of your next site.

A specialist broker identifies critical gaps that software misses. Many standard policies include a 10-metre height limit or a 2-metre depth restriction as default. If your project exceeds these limits, your cover is effectively void. At Just Quote Me, we use our 30 years of UK construction insurance expertise to spot these pitfalls before you sign. We move beyond the “one-size-fits-all” model, transitioning you from a mere policyholder to a partner who receives ongoing professional support.

- Expert Oversight: We review the fine print to ensure height and depth limits match your actual workload.

- Human Advocacy: If you need to make a claim, you speak to a person who understands your business, not a call centre script.

- Tailored Risk Assessment: We account for specific trade activities that algorithms often categorise incorrectly.

Bespoke Coverage vs. Generic Policies

Generic policies often leave out essential protections that keep a business solvent during a crisis. We focus on building a comprehensive shield by tailoring your policy to include plant and machinery insurance or specialized tool cover. This ensures that whether you own your equipment or hire it in, you aren’t left with a massive bill following a site theft.

Our local knowledge in Staffordshire and the West Midlands provides a distinct advantage. We understand the regional site-specific risks and the local supply chains, allowing us to offer advice that is grounded in reality. Having a human advocate during the claims process means we fight your corner, ensuring insurers settle valid claims quickly so you can get back to the job site.

Getting Your Bespoke Quote Today

Securing public liability insurance for builders uk shouldn’t be a bureaucratic headache. Our process is simple and no-nonsense. We start with a conversation to understand your turnover, employee count, and typical contract size. From there, we access our broad network of top-tier UK insurers to find competitive pricing that doesn’t sacrifice the quality of your protection.

We do the heavy lifting by comparing specialist markets that aren’t available on standard comparison sites. This gives you access to better rates and more robust policy wording. Reliability is our hallmark; we aim to provide the certainty you need to step onto any site with confidence.

Protect Your Trade With Expert Construction Cover

Navigating the complexities of public liability insurance for builders uk doesn’t have to be a burden on your business. You’ve seen how critical it is to look beyond the initial premium and understand your specific policy exclusions. Relying on generic comparison sites often leaves gaps that lead to rejected claims when you need support the most. By choosing a bespoke approach, you ensure your cover matches the actual risks you face on-site every day. JustQuoteMe brings over 30 years of industry experience to the table as an FCA-authorised independent broker. We don’t rely on faceless algorithms; we provide tailored solutions that fit the unique scale of your building firm. Securing the right protection means you can focus on your projects with total confidence. Our team understands the nuances of the UK construction sector, ensuring your policy remains compliant with the latest 2026 regulations. We’re here to handle the technical details so you can get back to work.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Take the stress out of your insurance today and build your future on a solid foundation.

Frequently Asked Questions

Is public liability insurance for builders a legal requirement in the UK?

Public liability insurance isn’t a legal requirement under UK law, unlike employers’ liability insurance which is mandatory if you have staff. However, most trade bodies like the Federation of Master Builders require it for membership. You’ll also find that 95% of local authorities and commercial clients won’t let you start work without seeing a valid certificate. It’s a commercial necessity that protects your business from devastating compensation claims.

How much does public liability insurance for builders cost in 2026?

Premiums for public liability insurance for builders uk typically start from around £120 per year for sole traders, but your specific price depends on several risk factors. In 2026, insurers calculate costs based on your annual turnover, the number of staff you employ, and your previous claims history. A builder handling £500,000 extensions will pay more than a handyman doing minor repairs. Getting a tailored quote is the only way to see an accurate figure.

Does builders public liability insurance cover my own tools and equipment?

Standard public liability insurance doesn’t cover your own tools or plant equipment; it only protects you against third-party injury or property damage. If a brick falls and smashes a neighbour’s conservatory, you’re covered, but if your van is broken into, you aren’t. You need to add specific “tools and equipment” cover to your policy to protect your gear. Most UK insurers offer this as a straightforward add-on during the quote process.

Am I covered if a sub-contractor causes damage on my site?

You’re generally covered for labour-only sub-contractors because they’re treated as employees under your direction. However, bona-fide sub-contractors who provide their own materials and tools must carry their own insurance. You should always check their insurance certificates before they start work on your site. If a bona-fide sub-contractor causes a major fire and their insurance has lapsed, the legal claim could still land on your desk, so proper vetting is essential.

What is the difference between public liability and professional indemnity for builders?

Public liability covers physical accidents like trips, falls, or property damage, while professional indemnity covers financial losses caused by your professional advice or designs. If you accidentally burst a water pipe, that’s a public liability claim. If you provide a structural design that’s flawed and causes a building to subside six months later, that’s a professional indemnity issue. Many modern builders now take both to ensure they’re protected from every angle.

What happens if I work without public liability insurance?

Working without insurance means you’re personally liable for all legal costs and compensation awards, which can easily exceed £50,000 for a single injury. You also risk losing out on 80% of potential contracts, as most savvy homeowners and all main contractors demand proof of cover. One small mistake could lead to bankruptcy or the loss of your home if you’re a sole trader. It’s a risk that simply isn’t worth taking for any professional.

Can I get public liability insurance for a single building project?

You can purchase short-term public liability insurance for a single project, but it’s often more expensive than an annual policy in the long run. These policies are designed for one-off builds or renovations that might last three to six months. If you’re planning to work on multiple jobs throughout the year, a standard annual policy offers better value and ensures you don’t have gaps in your protection between different contracts.

Does my insurance cover work on high-rise buildings or deep excavations?

Standard policies usually have height limits of 10 metres and depth limits of 2 metres, so you must declare any work exceeding these boundaries. If you’re working on high-rise blocks or deep basement excavations, you’ll need a bespoke policy with those specific limits increased. Failing to disclose these details to your broker can void your policy entirely. We’ll help you find specialist cover that matches the exact scale and risk of your specific construction projects.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.