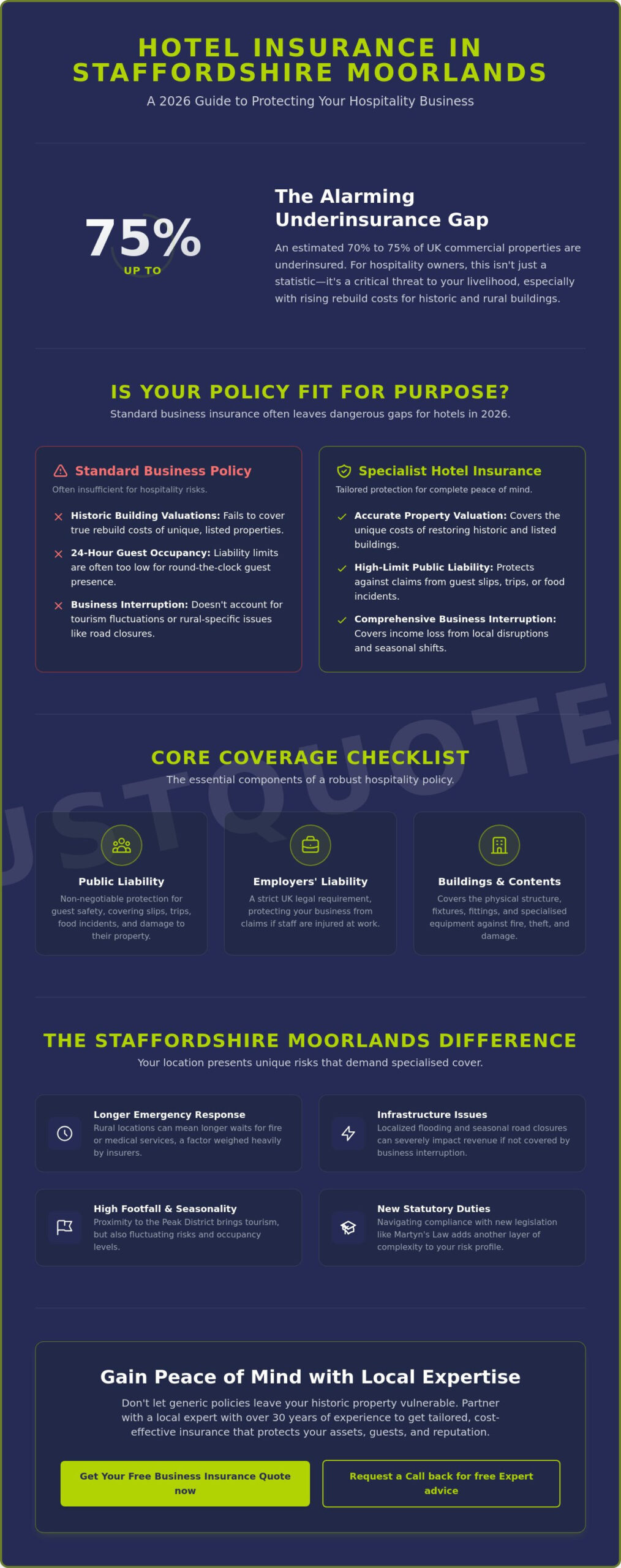

Did you know that an estimated 70% to 75% of UK commercial properties are underinsured in 2026? For hospitality owners in the Peak District, this statistic isn’t just a number; it’s a significant threat to your livelihood. Securing the right hotel insurance staffordshire moorlands is no longer a simple administrative task, especially when generic national providers fail to account for the unique heritage of our local buildings.

We know that running a guest house or hotel right now is demanding. You’re likely balancing new statutory duties under Martyn’s Law with rising operational costs, such as the 15% employer National Insurance rate. It’s frustrating when high premiums for historic assets or complex claims processes through automated systems add to your burden. You deserve a partner who understands the local tourism fluctuations and the specific risks of rural Staffordshire.

This article provides a clear roadmap to securing comprehensive, locally-tailored insurance that protects your assets and your guests. We’ll explore how to avoid underinsurance despite rising rebuild costs and explain how local expertise ensures your claims are handled with speed and efficiency. Discover how to gain peace of mind while protecting your historic property for the long term.

Key Takeaways

- Understand why standard business policies often fall short and how to build a package specifically for the 2026 hospitality landscape.

- Identify your essential legal obligations, from mandatory Employers Liability to robust Public Liability protections for guest safety.

- Discover the secrets to insuring historic or listed buildings while effectively managing seasonal occupancy shifts in the Peak District.

- Learn a two-step process to evaluate your unique risks and secure the most accurate hotel insurance staffordshire moorlands for your venue.

- Explore how partnering with a local expert with over 30 years of experience can streamline your claims and reduce administrative burdens.

What is Hotel Insurance and Why is it Essential in the Staffordshire Moorlands?

In 2026, hotel insurance staffordshire moorlands is much more than a simple set of certificates. It’s a comprehensive, combined policy designed to protect the unique operational risks of hospitality businesses in our region. While standard business insurance might cover basic contents and general risks, it often leaves dangerous gaps for hotel owners. A generic policy rarely accounts for 24-hour guest occupancy, specialized kitchen equipment, or the high-value assets found in many of our local historic buildings. Without a tailored approach, you might find yourself underinsured when you need support the most.

Reputation is the lifeblood of any guest house or hotel in a tight-knit community. In places like Leek or Cheadle, news of a poorly handled accident or a failed claim travels fast. Protecting your business means protecting your local standing. An independent broker plays a vital role here, acting as a human-centric advisor rather than an automated system. They help you navigate the 2026 insurance market, where insurers are applying increased scrutiny to individual applications despite a general softening of rates. Having a professional who understands the specific nuances of the Staffordshire hospitality sector ensures your policy is both cost-effective and robust.

The Core Components of a Hospitality Policy

A hospitality policy typically bundles property cover, business interruption, and Public Liability into one manageable package. It’s important to realize that hotels require much higher liability limits than a standard retail shop. You’re responsible for your guests’ safety while they sleep, dine, and relax on your premises. As we move through 2026, we’re also seeing a significant shift toward digital risk management. Even smaller B&Bs now rely on sophisticated online booking systems, making cyber protection a standard part of a modern insurance renewal to prevent operational downtime.

Staffordshire Moorlands: A Unique Hospitality Landscape

Your risk profile is deeply connected to your location. Proximity to the Peak District brings high footfall, but it also presents rural challenges. Destination hotels in the Moorlands often face longer emergency response times than those in urban centers, a factor that insurers carefully weigh when setting premiums. Whether you’re managing a boutique hotel in Leek or a country inn near Cheadle, your policy must reflect these geographical realities. Rural infrastructure issues, such as localized flooding or seasonal road closures, can impact your revenue, making specialized business interruption cover essential for maintaining your cash flow during unexpected disruptions.

Core Coverage: Protecting Your Guests, Staff, and Assets

Building a robust policy starts with identifying the specific risks that could halt your operations overnight. For owners seeking hotel insurance staffordshire moorlands, coverage must extend beyond the front door to protect every interaction within your venue. A comprehensive approach ensures that whether you are dealing with a guest injury or a sudden equipment failure, your business remains financially resilient.

Guest Safety and Public Liability

Public liability insurance is the non-negotiable foundation of your hospitality policy. It covers claims arising from slips, trips, or food-related incidents that can occur in busy dining rooms or guest suites. In 2026, guest expectations are higher than ever, and a single accidental injury claim could be financially devastating without the right indemnity limits. This protection also extends to guest belongings, ensuring that if accidental damage occurs to a visitor’s property while under your roof, your business isn’t left footing the bill. You might also want to consult with a specialist to ensure your liability limits match the scale of your events and guest capacity.

Protecting Your Human Capital

Your staff are the heart of your service. In the UK, there is a strict legal requirement for employers’ liability insurance that applies even if you only hire seasonal cleaners or part-time bar staff. With the employer National Insurance rate at 15% for the 2026/27 tax year and new statutory rights like sick pay from day one, managing your team has become more complex. Accurate employers liability insurance protects you against claims related to workplace injuries or illnesses. Modern policies in 2026 also frequently include clauses for employee mental health and wellbeing, reflecting the high-pressure nature of the modern hospitality industry.

Property and Asset Protection

The physical heart of your business requires specialized care. With UK commercial rebuild costs rising by approximately 30% to 35% between 2020 and 2025, an estimated 70% to 75% of commercial properties are now underinsured. Using specialist commercial property insurance is essential to cover high-value kitchen equipment and bespoke hotel furnishings. It’s vital to have an accurate rebuild cost assessment to ensure your hotel insurance staffordshire moorlands actually covers the current market price of materials and labor. These costs were 2% higher in January 2026 than the previous year, making regular valuation reviews a necessity rather than an option.

Don’t overlook revenue protection. Business interruption insurance keeps your cash flow steady if you’re forced to close due to a fire, flood, or major equipment failure. Similarly, loss of license cover is vital for hotels where bar or restaurant revenue is a significant portion of the turnover. These layers of protection ensure that an unexpected event doesn’t lead to a permanent closure.

Specialised Risks for Moorlands Hotels and B&Bs

The Staffordshire Moorlands isn’t just a scenic backdrop; it’s a specific risk environment that requires more than a generic insurance policy. While previous sections highlighted core liabilities, local hotel owners must also navigate the complexities of the Peak District fringe. From the unique preservation requirements of historic stone buildings to the sudden weather shifts in the valleys, your hotel insurance staffordshire moorlands needs to be as specialized as the landscape itself. Standard national providers often overlook these regional nuances, leaving you vulnerable to significant financial shortfalls.

Heritage and Listed Property Challenges

Many guest houses in Leek and the surrounding villages are Grade II listed, which brings specific legal obligations for repairs. If a fire or flood damages a heritage building, you can’t simply use modern, off-the-shelf materials. Heritage officers often insist on Staffordshire blue bricks, specific lime mortars, or hand-carved stonework. These materials and the specialist craftsmen required to install them are expensive. Standard policies fail here because they don’t account for the massive gap between modern rebuild costs and heritage restoration. Your policy must also cover the cost of bringing a damaged building up to 2026 building regulation standards, which is a common requirement during major repairs.

Tourism Peaks and Seasonal Staffing

Tourism in the Moorlands is highly seasonal, peaking during the summer months and the Christmas period. This fluctuation impacts your risk profile in two ways. First, your liability exposure increases when guest numbers swell. It’s essential to follow the Health and Safety Executive guidance for hospitality to manage risks like slips in gardens or kitchen incidents during peak service. Second, the low season brings its own dangers. If a property sits partially unoccupied during the quiet months of January or February, the risk of undetected pipe bursts or rural theft increases. A tailored policy allows you to scale your cover, ensuring you aren’t paying for excess capacity in winter while remaining fully protected during the summer rush.

Digital Risks in Rural Locations

Rural connectivity issues don’t just affect your Netflix stream; they impact your business security. Most Moorlands hotels now rely on a Property Management System (PMS) to handle bookings and guest data. Even a small B&B is a target for data breaches, making cyber insurance a critical requirement in 2026. Furthermore, the rural infrastructure in our valleys is prone to power failures or broadband outages. If a local network failure prevents you from taking bookings or processing payments, you need business interruption cover that specifically includes “failure of utilities.” This ensures that a fallen tree or a local exchange fault doesn’t result in a total loss of revenue for the week.

How to Evaluate Your Hotel Insurance Requirements

Evaluating your hotel insurance staffordshire moorlands requirements requires a methodical approach to ensure no operational gaps remain. A generic policy might seem sufficient on paper, but the reality of 2026 regulations and local environmental factors demands a closer look. Follow these five steps to build a more resilient business model.

- Step 1: Conduct a physical risk assessment. Walk your premises to identify hazards, paying close attention to guest safety in communal areas and kitchen fire suppression systems.

- Step 2: Review financial projections. Your 2026 revenue and occupancy levels dictate your business interruption limits; ensure these reflect your actual growth.

- Step 3: Monitor regulatory changes. Ensure compliance with Martyn’s Law and the Employment Rights Act updates effective April 2026.

- Step 4: Secure a professional audit. A local expert can identify risks unique to the Moorlands that national call centers miss.

- Step 5: Prioritize value. The cheapest premium often hides restrictive exclusions that cost more in the long run.

For a clear perspective on your current coverage, speak with a local insurance expert today to identify any hidden vulnerabilities in your current policy.

The Independent Broker Advantage

Algorithms use generic data. They don’t understand the specific access issues of a rural Peak District guest house or the heritage value of a stone-built hotel in Leek. A local broker provides access to niche underwriters who specialize in heritage properties and high-risk hospitality venues. These specialists don’t always appear on automated comparison sites. Perhaps most importantly, having a human advocate during the claims process ensures you receive personal support when you’re under pressure. You aren’t just a policy number in an automated system; you’re a local business owner with a dedicated partner.

Avoiding the Underinsurance Trap

Many owners fall victim to “Average Clauses” in their property insurance. If you insure your building for only 80% of its actual value, the insurer may reduce any claim payout by 20%, even for a minor incident. Underinsurance in 2026 occurs when a property’s declared value fails to match the current, inflated costs of labor and materials, potentially resulting in a claim payout that is reduced by the same percentage as the shortfall. To stay protected, update your asset register annually to reflect the rising material costs seen in early 2026. A tailored hotel and guest house insurance policy should always be based on a professional reinstatement cost assessment rather than a simple market valuation.

Just Quote Me: Your Local Staffordshire Moorlands Insurance Partner

Just Quote Me acts as your steady hand in a complex market. We’ve spent over 30 years refining our knowledge of the Staffordshire and West Midlands hospitality sectors. This experience means we can quickly identify the specific risks associated with your venue, whether it’s a historic coaching inn or a modern guest house. We provide hotel and guest house insurance that is highly customized, ensuring you don’t pay for unnecessary extras while remaining fully protected against regional risks. Our approach is intentionally straightforward and jargon-free. We believe you should feel confident in your policy wording without needing to decipher complex legal terminology.

Securing the right hotel insurance staffordshire moorlands is about more than just finding a policy; it’s about building a partnership. By leveraging our extensive insurer network, we find competitive pricing that balances value with security. We manage the administrative burdens and complex negotiations with underwriters so you don’t have to. This commitment to efficiency allows you to focus on what matters most: delivering an exceptional experience for your guests.

Why Local Expertise Matters

National call centers often fail to grasp the nuances of our region. They don’t understand the specific access issues of the Peak District fringe or the heritage value of stone buildings in Leek, Cheadle, and Biddulph. We do. Our deep roots in the local business community allow us to provide a personalized service that larger national brokers cannot replicate. Supporting the Staffordshire Moorlands economy through local partnership is a core part of our identity. When you work with us, you’re partnering with a team that understands your environment because we live and work in it too.

Ready to Secure Your Business?

Our efficient process is designed to save you time and reduce your administrative workload. We provide a human-centric alternative to automated systems, ensuring you have a dedicated advocate who understands your specific professional sector. Whether you need to cover seasonal staff or protect a listed property asset, we provide the expertise needed to navigate the 2026 insurance landscape with confidence. Take the first step toward comprehensive protection today.

Secure Your Venue’s Future in the Staffordshire Moorlands

Protecting your hospitality business in 2026 requires more than a standard policy. It demands a strategy that accounts for the unique heritage of the Peak District and the evolving regulatory landscape. By prioritizing accurate rebuild valuations and addressing modern digital risks, you ensure your hotel remains resilient against the unexpected. Choosing a partner with specialized hospitality sector knowledge means you won’t be left navigating complex claims alone.

Just Quote Me brings over 30 years of industry experience to every policy we audit. As an FCA-authorised independent broker, we provide human-centric advice that automated algorithms simply can’t offer. We manage the administrative weight of your hotel insurance staffordshire moorlands so you can focus on welcoming guests to our beautiful corner of the country. We look forward to helping you protect your business for years to come.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Frequently Asked Questions

Do I need specific insurance for a small B&B in the Staffordshire Moorlands?

Yes, you require a specialized policy that bridges the gap between residential and commercial risks. Standard home insurance usually excludes business activities like hosting paying guests. A tailored policy for a B&B covers your personal belongings alongside business liabilities, ensuring you aren’t left vulnerable if a guest is injured or your property is damaged during their stay. It’s a vital safeguard for your home and livelihood.

Is public liability insurance a legal requirement for UK hotels?

Public liability insurance isn’t a legal requirement in the UK, but it’s considered essential for any hospitality provider. Without it, your business would be responsible for legal fees and compensation if a guest claims for an injury or property damage. Given the high volume of guest interactions in a hotel, the financial risk of operating without this protection is far too high for most owners to manage safely.

How does listed building status affect my hotel insurance premiums?

Listed building status generally increases premiums due to the higher costs of specialist materials and traditional craftsmanship required for repairs. Insurers must account for strict planning requirements and the potential for extended repair timelines. When seeking hotel insurance staffordshire moorlands, it’s vital to declare your building’s grade accurately to ensure your sum insured reflects the true cost of heritage restoration rather than modern rebuild rates.

Does hotel insurance cover guest cancellations or no-shows?

Standard hotel policies don’t typically cover individual guest cancellations or no-shows. However, you can often add specific extensions for loss of revenue caused by larger external events that prevent guests from reaching you. It’s best to check the specific exclusions in your policy regarding “cancellation of bookings” to see if you have protection for major disruptions beyond your control, such as local road closures or utility failures.

What is business interruption insurance and do I really need it?

Business interruption insurance covers the loss of income you suffer following a physical claim, such as a fire or flood. It ensures you can still pay your fixed costs and staff while your hotel is closed for repairs. For many venues, this is the difference between a temporary setback and permanent closure, as it maintains your cash flow during the months you cannot trade.

Can I get insurance for a hotel that is only open seasonally?

Yes, you can secure coverage that reflects your seasonal trading patterns. Many insurers offer policies that adjust liability limits and property protection based on your peak and low seasons. This ensures you aren’t paying for full guest capacity during months when you’re closed, though you must still maintain essential property and liability cover to protect the building and any remaining staff during the off-season.

Why should I use a broker instead of a comparison website for my hotel?

Using a broker provides access to niche insurers that don’t appear on generic comparison sites. A broker understands the specific risks of the hospitality sector and can negotiate better terms based on your individual risk profile. This human-centric approach ensures you get a policy tailored to your actual needs rather than a “one size fits all” solution that might leave you underinsured in a crisis.

What happens if my hotel is flooded or suffers storm damage?

If your hotel suffers flood or storm damage, your buildings and contents insurance covers the physical repair costs. Additionally, your business interruption cover kicks in to replace the revenue lost while the property is uninhabitable. When arranging your hotel insurance staffordshire moorlands, it’s important to verify that your policy includes “flood cover” as a standard peril, especially if your venue is located in a valley or near a watercourse.