by jqm | Jun 8, 2026 | Insurance

Did you know that an estimated 70% to 75% of UK commercial properties are underinsured in 2026, with many covered for only 67% of their true rebuild cost? For a local entrepreneur, the fear of being caught short during a claim is a valid concern. Finding reliable office insurance for small business lichfield often feels like a choice between generic online algorithms or policies that ignore local realities like the city’s specific crime rates or regional flood risks.

You deserve a policy that fits your exact sector and office size without the headache of complex jargon. This 2026 broker guide simplifies the process of protecting your workspace. We’ll explain how to avoid the £2,500 daily fines associated with Employers’ Liability non-compliance, address the latest cyber security standards, and secure a tailored plan that gives you total peace of mind. By the end of this guide, you’ll know exactly how to safeguard your Lichfield office against the unexpected while keeping your focus on growth.

Key Takeaways

- Learn how to identify and mitigate specific Lichfield risks, from city centre security concerns to flood assessments near local waterways.

- Understand the critical legal obligations of your business, ensuring you have robust Employers’ Liability and Public Liability cover in place.

- Discover the benefits of securing tailored office insurance for small business lichfield that accounts for your unique sector and headcount.

- Gain a clear roadmap for choosing a Staffordshire broker who offers expert advice and access to a broad range of leading UK insurers.

- Explore how to streamline your administrative processes by partnering with a trusted advisor who manages complex insurance requirements on your behalf.

Why Small Businesses in Lichfield Need Bespoke Office Insurance

Lichfield isn’t a one-size-fits-all business environment. From the historic timber-framed offices in the city centre to the sprawling industrial units at Fradley Park, the risks your company faces vary wildly based on your specific location. Securing office insurance for small business lichfield requires more than a generic online form. While a standard Business Owner’s Policy provides a useful baseline for property and liability, it often misses the nuances of Staffordshire’s unique geography and local economic shifts. Relying on a rigid, automated policy can leave you overpaying for cover you don’t need or, worse, underinsured when a claim arises.

Lichfield’s Office Diversity: From Historic Buildings to Modern Hubs

The age and architecture of your workspace play a significant role in your insurance profile. A firm operating out of a Grade II listed building near Lichfield Cathedral faces different challenges than a tech startup at Wall Island. Historic properties often have higher rebuild costs and specific maintenance requirements that influence premiums. In contrast, modern hubs in Fradley or near the A38 require robust protection for high-value digital assets and complex logistics. We see many businesses struggle because their generic policy doesn’t account for the specialized restoration costs required for historic Staffordshire masonry or the advanced security needs of modern business parks.

The Value of Local Brokerage in Staffordshire

Automated call centres don’t understand why a business in the WS13 postcode might have different security needs than one in WS14. A local broker understands the footfall patterns near Three Spires and the specific flood risks associated with local waterways like the Minster Pool. This regional insight ensures your risk assessment is accurate from day one. Bespoke office insurance for small business lichfield allows you to navigate these regional nuances without paying for irrelevant extras. For claims, having a partner who can visit your site in person makes the process significantly more efficient than dealing with a remote chatbot.

Small businesses must balance tight budgets with the legal necessity of Employers Liability Insurance and the protection offered by Public Liability Insurance. Whether you’re a fresh startup or an established firm, precision in your policy is the key to sustainable protection. By auditing your specific risks rather than accepting a generic package, you ensure that every pound of your premium is working to safeguard your livelihood. This pragmatic approach removes the administrative burden, letting you focus on running your business while we manage the complexities of your cover.

Core Components of a Comprehensive Office Insurance Policy

Building a comprehensive policy requires a clear understanding of the specific risks your team and property face daily. When looking for office insurance for small business lichfield, you need to look beyond basic fire and theft. A robust package integrates liability, asset protection, and financial continuity into a single, manageable framework. This ensures that a single accident or digital breach doesn’t derail years of hard work. By selecting the right mix of covers, you create a safety net that allows you to operate with confidence in a competitive market.

Liability Protection for Your Staff and the Public

Legal compliance is the first pillar of any office policy. If you employ anyone, Employers’ Liability insurance is a strict legal requirement under the Employers’ Liability (Compulsory) Act 1969. In 2026, the minimum cover level remains £5 million, and failing to hold a valid certificate can result in fines of up to £2,500 for every single day you are uninsured. Beyond legal mandates, Public Liability Insurance is vital if clients, couriers, or members of the public visit your premises. It protects your business against claims for third-party injuries or property damage occurring on-site. You can easily manage these risks by including Employers Liability Insurance in your core bundle to ensure all legal boxes are ticked.

Protecting Your Digital and Physical Assets

Your office is more than just four walls; it’s a hub of high-value technology and sensitive data. With cyber-attacks, particularly ransomware, remaining a major threat in 2026, Cyber Insurance has become a necessity rather than an optional extra. For a micro-business with a turnover under £500k, a £500k policy typically costs between £500 and £1,500 per year. Most insurers now require Multi-Factor Authentication (MFA) and robust data backups as preconditions for cover. Additionally, if your firm provides expert advice, Professional Indemnity Insurance protects you against claims of negligence or errors. Combining these with contents cover ensures your laptops, specialized software, and essential records are protected against theft or accidental damage.

Business Interruption cover is often the most overlooked component of office insurance for small business lichfield. If a localized event like a fire or a flood makes your office unusable, this cover supports your cash flow by replacing lost income and helping with relocation costs. It acts as a vital safety net while you get back on your feet. To find the right balance for your specific sector, you might want to compare options with a local expert who understands the Staffordshire market and can help you avoid the common trap of underinsurance.

Assessing Local Risks: From Bore Street to Wall Island

Lichfield presents a specific set of challenges that automated insurance platforms usually overlook. While the city is a thriving hub for commerce, the local environment dictates your risk profile. In 2026, the overall crime rate in Lichfield sits at 63 crimes per 1,000 people. This statistic highlights why office insurance for small business lichfield must be grounded in local data. Whether your office is tucked away near Bore Street or located in a modern business park by Wall Island, your policy should reflect the actual risks of your immediate surroundings. It’s a mistake to assume all Staffordshire postcodes are treated equally by underwriters.

Security and Theft Prevention in the City Centre

Offices in high-footfall areas like Three Spires or Market Street face different security pressures than those on the outskirts. Theft and property crimes are common concerns in these busy zones, often driven by the city’s status as a retail destination. We recommend implementing physical security measures such as high-quality alarm systems and reinforced entry points. These upgrades don’t just protect your assets; they actively lower your premiums by demonstrating proactive risk management. For those navigating these choices, BIBA’s business insurance guides provide excellent frameworks for understanding how security standards influence your cover.

Environmental factors are equally critical. Staffordshire is an area that regularly experiences flooding, and the average insurance claim for a flooded business in the UK is approximately £70,000. If your office is located near the Minster Pool or other local waterways, an accurate flood risk assessment is essential. A generic policy might not offer the specific flood protection required for these vulnerable postcodes, leaving you exposed to significant financial loss. Addressing these factors early ensures your office insurance for small business lichfield remains robust regardless of the weather.

Logistics and Fleet Insurance for Lichfield Firms

Many Lichfield businesses operate on the city’s periphery or require staff to travel frequently via the A38 and M6 Toll. This creates a different set of liabilities. If your team uses company vehicles or drives their own cars for business purposes, you must ensure you have appropriate Motor Fleet Insurance. Standard personal car insurance doesn’t cover business use on public roads. Additionally, mobile office workers carrying laptops and specialized equipment should consider transit cover to protect these assets while moving between sites. By addressing these logistical risks, you ensure your business remains operational even when your team is on the move.

How to Choose an Office Insurance Broker in Staffordshire

Selecting a partner to manage your office insurance for small business lichfield shouldn’t be a matter of chance. While many platforms offer quick quotes, they often lack the depth required to protect a growing Staffordshire enterprise. You need a structured approach to evaluate potential brokers to ensure they offer more than just a certificate of insurance. In a market where 87.8% of small businesses are reporting stable or growing revenue in 2026, your insurance needs to be as dynamic as your growth. You don’t want a policy that stays static while your liabilities increase.

Follow these five steps to find a broker that fits:

- Audit your specific risks: Start by listing your current headcount and any specialized equipment. Accurate data is essential for calculating Employers Liability Insurance requirements and avoiding underinsurance.

- Verify panel access: Ensure the broker has access to a broad range of UK insurers, not just a handful of preferred providers.

- Check sector expertise: A broker familiar with your industry, whether it’s legal, tech, or retail, will spot coverage gaps you might miss.

- Evaluate claims support: Ask how they handle claims. You want a human advisor who will advocate for you, not an automated portal or a remote call centre.

- Request a bespoke quote: Avoid generic bundles. Your quote should be a direct reflection of your specific office profile and location.

Evaluating Broker Expertise and Access

Independent brokers offer a significant advantage over tied agents. They aren’t restricted to a single insurer’s products, allowing them to scan the market for the most competitive terms and comprehensive cover. Choosing a broker with decades of experience means you’re benefiting from a steady hand that has navigated various market cycles. This is particularly important in 2026 as insurers apply more rigorous underwriting standards despite a generally soft market. Expert advice ensures your risk management practices are presented in the best possible light to underwriters, potentially leading to more favourable terms.

Transparency in Fees and Documentation

Clarity is essential when reviewing your policy. You should look for brokers who are upfront about arrangement fees and administration charges. Hidden costs can quickly erode the value of a seemingly cheap premium. Additionally, ensure your policy allows for mid-term adjustment flexibility. As your business evolves, your office insurance for small business lichfield must adapt without excessive penalties. Whether you’re hiring new staff or investing in high-value tech, your documentation should remain a clear, accurate reflection of your liabilities. You can discuss these requirements with a local advisor to ensure your coverage remains perfectly aligned with your business goals.

Get Your Tailored Office Insurance Quote with Just Quote Me

Securing the right office insurance for small business lichfield shouldn’t be a source of stress. Our team at Just Quote Me is deeply committed to supporting the Lichfield business community, from the startups revitalizing the city centre to the established firms in Fradley Park. We understand that your time is best spent driving your business forward, not deciphering the fine print of insurance contracts. By acting as your trusted advisor, we manage the complex administrative burdens so you can focus on what matters most: your growth and your team.

The Just Quote Me advantage is built on independence and regional expertise. Unlike larger, impersonal agencies, we provide a direct link to a broad panel of UK insurers while maintaining the accessibility of a local service provider. This allows us to find competitive premiums without compromising on the quality of your cover. We pride ourselves on being a pragmatic partner that simplifies the insurance process, providing clear, honest communication at every stage of your journey.

Bespoke Solutions for Every Office Size

No two offices in Staffordshire are identical, which is why we reject the “one-size-fits-all” approach. For office owners and tenants alike, tailoring your Commercial Property Insurance is essential to ensure your physical assets are fully protected. We offer flexible policies that scale alongside your business; as your headcount increases or your equipment inventory grows, your cover adjusts to match your new reality. We position ourselves as a human-centric alternative to automated systems, ensuring you always have access to a knowledgeable professional who understands your specific sector.

Ready to Protect Your Lichfield Office?

Choosing a local, independent broker ensures that your office insurance for small business lichfield is grounded in the reality of the Staffordshire market. You benefit from faster risk assessments, dedicated claims support, and a policy that ticks every legal and professional box. We’ve spent decades building relationships with insurers to ensure our clients receive the most robust protection available in 2026. Don’t leave your livelihood to chance with a generic policy that might fail when you need it most. Take the first step toward comprehensive protection today with a partner who understands your business as well as you do.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Securing Your Business Future in Lichfield

Protecting your livelihood in a competitive market requires more than just meeting basic legal requirements. By addressing the specific security and environmental risks of the Staffordshire region, you’ve already taken the most important step toward long-term stability. Whether you’re navigating the complexities of Employers’ Liability or securing your digital assets against evolving cyber threats, a tailored approach is always the most efficient path. It ensures you aren’t left vulnerable by generic policies that fail to account for local realities.

Choosing the right office insurance for small business lichfield means partnering with a team that values human expertise over automated algorithms. Just Quote Me brings over 30 years of industry experience as an FCA-authorised independent broker. We leverage our access to a broad network of top UK insurers to find the precise cover your office needs. This proactive strategy simplifies your administrative burden and ensures you’re never paying for redundant protection. It’s about providing a steady hand so you can focus on growth.

Ready to safeguard your workspace with a policy built for 2026? You can secure your bespoke insurance quote today and focus on what you do best. We look forward to helping your Lichfield business thrive.

Frequently Asked Questions

Is office insurance a legal requirement for small businesses in Lichfield?

Employers’ Liability insurance is a legal requirement for any Lichfield business that employs staff, with a minimum cover level of £5 million. While other components like Public Liability or contents cover aren’t legally mandated, they’re often required by landlords in a lease or by clients as part of a professional contract. Failing to hold the required legal cover can result in fines of up to £2,500 for every day you remain uninsured.

How much does office insurance typically cost for a small business?

The cost of your policy depends on several factors, including your property’s rebuild value, your location, and your annual turnover. For instance, a small office with a rebuild cost of £200,000 might see premiums around £300, though this varies based on your specific risk management practices. Securing bespoke office insurance for small business lichfield ensures you pay for the exact cover you need rather than a generic, overpriced bundle.

Does my office insurance cover employees working from home in Staffordshire?

Most modern office policies can be extended to cover business equipment used by employees while they work from home. You should check that your Employers’ Liability and contents cover specifically includes remote locations to ensure your team is protected outside the main office. It’s essential to inform your broker if your team’s working patterns change so your policy remains an accurate reflection of your operational risks.

What is the difference between Public Liability and Professional Indemnity for an office?

Public Liability covers your business against claims for physical injury or property damage caused to third parties on your premises. Professional Indemnity protects you against financial losses a client suffers because of errors, omissions, or negligent advice you’ve provided. Both are vital for Lichfield’s service-based firms; however, they address entirely different risks, which is why most businesses choose to include both in their comprehensive policy.

Can I combine my office insurance with other business covers?

You can easily integrate your office policy with other essential protections such as Cyber Liability or Directors and Officers insurance. Combining these covers into a single package often simplifies your administrative processes and can lead to more favourable premium rates. This approach ensures there are no gaps in your protection, providing a seamless safety net that covers your physical assets, digital data, and legal liabilities.

What happens if I need to make a claim on my office insurance policy?

You should contact your insurance broker immediately to start the claims process and receive expert advice on the next steps. They’ll help you gather the necessary evidence, such as incident reports or repair quotes, to ensure your claim is handled efficiently. Having a local Staffordshire broker means you’ll have a dedicated human advocate to manage the communication with insurers, which is often much faster than using automated systems.

Do I need special insurance if my Lichfield office is in a listed building?

Listed buildings require specialized cover because the cost of repairing or rebuilding them using traditional materials and methods is significantly higher than modern properties. Your policy must accurately reflect these restoration costs to avoid the common trap of underinsurance. Insurers will typically require specific details about the building’s Grade status to ensure the premium and cover levels are appropriate for its historical significance.

How often should I review my small business office insurance?

You should review your office insurance for small business lichfield at least once a year or whenever your business undergoes a major change. This includes hiring new employees, moving to a different site, or purchasing expensive new technology. Regular reviews ensure your cover doesn’t become outdated and prevents you from paying for protection that no longer fits your current headcount or the scale of your operations.

Article by

Just Quote Me

JustQuoteMe Ltd is an independent UK insurance brokerage specialising in business and personal insurance solutions. With over 35 years of industry experience, the company provides tailored insurance cover for businesses, landlords, tradespeople, hospitality venues, fleets, and individuals across the UK. Known for its personal service, expert advice, and competitive premiums, JustQuoteMe Ltd works with leading insurers to deliver bespoke policies designed around each client’s unique needs. The company is authorised and regulated by the Financial Conduct Authority (FCA No. 586607) and has built a reputation for trusted, straightforward insurance guidance and long-term client relationships.

by jqm | Jun 7, 2026 | Insurance

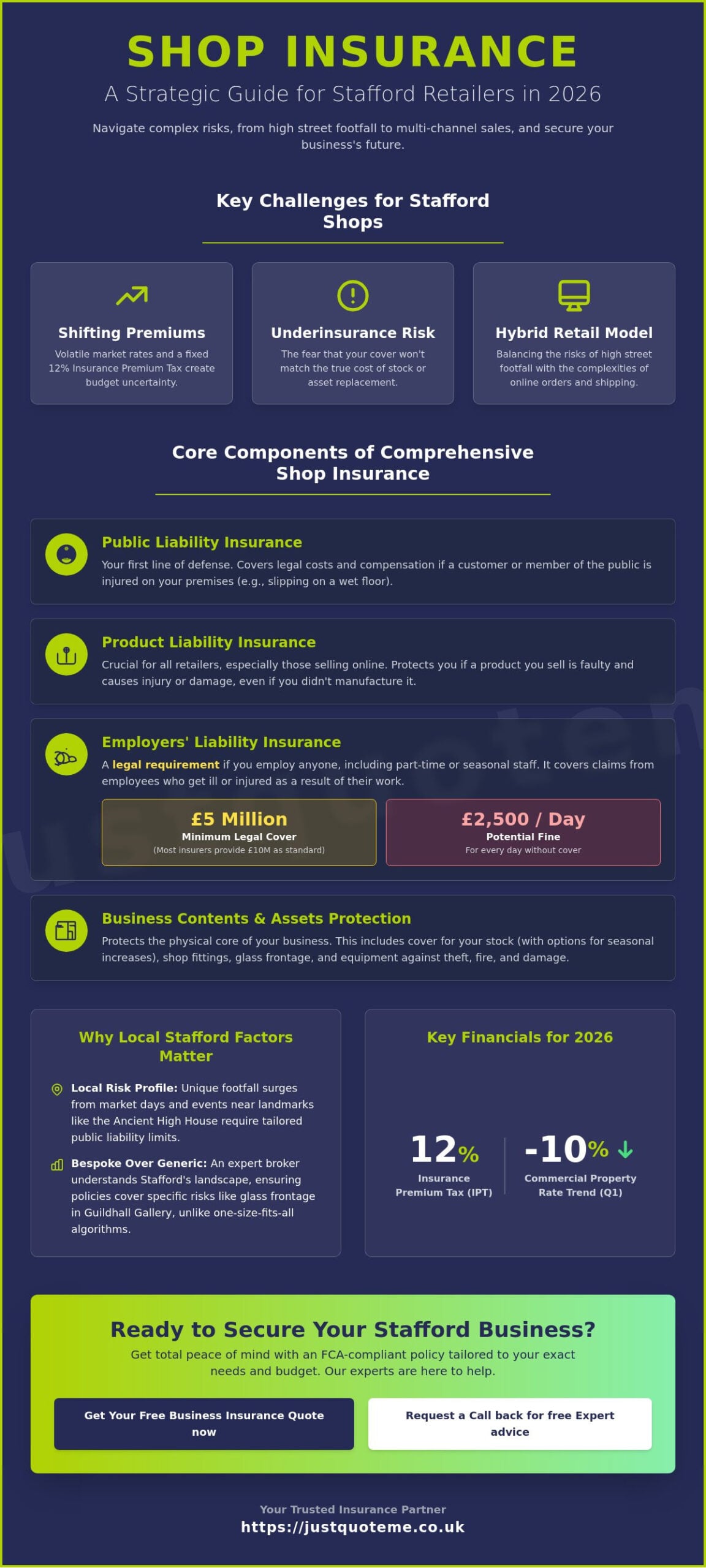

Could a single delivery dispute or a burst pipe on Greengate Street undo years of hard work building your local brand? You’ve likely noticed that securing reliable shop insurance for retail business in stafford has become more complex in 2026. Between shifting premium rates and the need to cover both high street footfall and online orders, the fear of being underinsured is a genuine concern for many Stafford business owners. You want protection that works as hard as you do, without getting lost in a maze of industry jargon or time-consuming forms.

We understand that your time is better spent serving customers than deciphering policy fine print. This guide is designed to clarify your options and show you how bespoke insurance solutions can provide total peace of mind. You’ll discover how to navigate the current 12% Insurance Premium Tax and meet the mandatory £5 million employers’ liability requirements efficiently. We will explore the essential steps to securing FCA-compliant coverage that fits your specific budget while ensuring your Stafford retail business remains fully protected against the unexpected.

Key Takeaways

- Learn how to secure comprehensive shop insurance for retail business in stafford that balances high street presence with modern multi-channel selling risks.

- Identify the core policy components, including Public and Product Liability, that form the frontline of your business protection.

- Understand how local factors like Stafford market days and town centre footfall influence your specific risk profile and coverage needs.

- Discover the best methods for accurately valuing your stock and shop fittings to ensure your 2026 premiums remain both fair and effective.

- Gain insights into how 30 years of local expertise can simplify the quote process by connecting you with a tailored panel of leading UK insurers.

Understanding Shop Insurance for Stafford Retailers in 2026

Shop insurance isn’t just a legal necessity; it’s a strategic shield for your livelihood. For anyone seeking shop insurance for retail business in stafford, it’s vital to recognize that this cover is a bespoke bundle of protections rather than a single document. It merges public liability, employers’ liability, and contents cover into one manageable package. To understand how these components fit into the broader overview of the UK insurance market, you must look at how local risks intersect with national regulations.

The 2026 retail environment in Staffordshire has changed. While the commercial property insurance market experienced a softening trend with rates declining by 10% in the first quarter of the year, other costs like the 12% Insurance Premium Tax (IPT) remain a fixed reality. A local broker helps you capitalize on these market dips. They ensure you don’t fall victim to underinsurance as stock values and replacement costs fluctuate. This proactive approach is exactly what differentiates a professional service from a generic online form.

Why Stafford Shop Owners Need Bespoke Cover

Stafford’s town centre has a unique rhythm. Whether you’re based on Greengate Street or near the historic Ancient High House, your footfall isn’t the same as a shop in a major city. Local events and market days create specific surges in risk that generic algorithms often ignore. A broker who knows the Stafford Borough Council area can tailor your shop insurance to reflect these patterns. They understand that a boutique in the town centre faces different challenges than a business on an industrial estate.

Retail Insurance vs. Standard Business Liability

Standard business liability often leaves gaps that can be devastating for a retailer. A generic policy might cover your basic legal obligations but miss retail-specific essentials like seasonal stock increases or glass frontage protection. If you’re trading in the Guildhall Gallery, your requirements for public liability and contents cover are vastly different from a warehouse operator. Specialised shop insurance for retail business in stafford ensures that specific risks, like theft of money from a till or damage to shop fittings, are included by default. This professional approach moves you from basic compliance to genuine security.

Core Components of a Comprehensive Retail Policy

Building a robust policy for shop insurance for retail business in stafford requires a clear understanding of how different covers interact. Many retailers now operate a hybrid model, selling both on the high street and through digital channels. This dual presence creates a unique risk profile that standard “off the shelf” policies often overlook. By breaking down your coverage into specific components, you ensure that every part of your operation, from the shop floor to the delivery van, remains secure.

Liability Protections: Public vs. Product

Public liability acts as your first line of defence. It covers legal costs and compensation if a customer slips on a wet floor or is injured by a falling display. However, public liability insurance doesn’t cover injuries caused by the products themselves. This is where product liability becomes essential. Even if you don’t manufacture the goods, you can still be held liable for damages if a product you sell is faulty. In a modern retail environment where items are shipped across the country, this protection is vital for maintaining your business’s financial health.

Employers’ Liability: Meeting UK Legal Standards

If you employ anyone, even on a casual or seasonal basis, employers liability insurance is a legally required business insurance in the UK. The law mandates a minimum of £5 million in coverage, though most insurers provide £10 million as standard. Failing to have this in place can result in fines of up to £2,500 for every single day you operate without it. For Stafford retailers hiring extra help during the busy Christmas period or for local festivals, ensuring these staff members are covered is a non-negotiable priority that protects both the employee and the business owner.

Protecting Your Physical Assets

Your shop’s physical assets are often its most significant investment. Contents and stock cover protects your inventory from theft, fire, or accidental damage. For businesses on the Stafford high street, glass and signage cover is particularly important; a smashed window can be an expensive repair that halts trade. Additionally, consider stock in transit cover if you handle your own deliveries. This ensures your goods are protected while moving between your premises and the customer’s door. Managing these diverse risks is simpler when you speak with a specialist broker who can align these protections with your specific business model.

Evaluating Local Risks: From Greengate Street to the Guildhall Gallery

Stafford’s retail geography is diverse. A shop on Greengate Street faces different risks than one tucked away in the Guildhall Gallery. When arranging shop insurance for retail business in stafford, you must account for these nuances. Pedestrianised zones mean high footfall but also restricted vehicle access for deliveries. This can impact your business interruption profile if a supplier cannot reach you during an emergency. Understanding these street-level details is what ensures your policy actually performs when you need it most.

Local infrastructure also plays a role in your risk assessment. The Stafford Borough Council area has seen various regeneration projects that change how people move through the town. If your business is located near a major construction site, your risk of accidental damage or business interruption might temporarily increase. A bespoke policy doesn’t just look at your shop; it looks at the environment surrounding it.

Addressing Footfall and Public Access Risks

Pedestrianised streets in the town centre are hubs of activity. During peak times, such as the annual Christmas Lights Switch-on or regular market days, your public liability exposure increases significantly. Historic buildings, while charming, often feature uneven floors or narrow staircases. These are prime areas for slips and trips. You need a policy that acknowledges these specific environmental factors. It is also the perfect time to ensure your Employers’ Liability (EL) insurance is up to date. Your staff will be under more pressure during these high-traffic local events, and their protection is a legal priority.

Stock and Asset Protection in Staffordshire

Environmental risks are just as critical as footfall. Businesses located near the River Sow, particularly those around Victoria Park or the lower end of the town, should pay close attention to flood risk assessments. While the town has seen improvements in flood defences, insurers still scrutinise postcodes in these zones. Protecting your physical premises with commercial property insurance ensures you aren’t left footing the bill for water damage or structural repairs.

Security is another local variable. Stafford retailers often benefit from collaborating with local business crime reduction partnerships. These initiatives help lower the risk of theft and vandalism. By demonstrating proactive risk management, you present a much better profile to underwriters. This local knowledge is something a national call centre simply cannot provide. It is about understanding the street-level reality of trading in Staffordshire and choosing shop insurance that reflects that reality.

How to Customise Your Shop Insurance Quote

Customising your shop insurance for retail business in stafford isn’t a task to be rushed. It’s about ensuring the figures on your policy match the reality of your shop floor. One of the most misunderstood aspects of retail insurance is the “Average Clause”. If you insure your stock for £50,000 but the actual replacement value is £100,000, you’re 50% underinsured. In the event of a claim, the insurer may only pay out 50% of your loss, even for a minor incident. Accuracy is your best defence against a significant financial shortfall.

You should also evaluate the need for seasonal stock increases. As we discussed regarding Stafford’s local events like the Christmas Lights Switch-on, your inventory levels likely fluctuate throughout the year. Most bespoke policies allow for automatic increases in stock cover during peak periods. This ensures you aren’t paying for high levels of cover in quieter months while remaining fully protected when your stock rooms are full. It’s a pragmatic way to manage your premiums without compromising on security. To ensure your policy is perfectly aligned with your trading patterns, you can get a customised quote today that reflects your specific needs.

Calculating Your Sums Insured Correctly

A common mistake is valuing stock at its retail price. Your sums insured should reflect the “replacement cost,” which is what it would cost you to buy the items again from your suppliers. This also applies to your shop fittings and specialised equipment. In the 2026 market, replacement costs can shift due to supply chain changes, so regular reviews are essential. Don’t rely on valuations from several years ago. A quick consultation with your broker can help you adjust these figures to prevent the trap of underinsurance, especially as property insurance rates have seen a 10% decline recently, potentially freeing up budget for better contents protection.

Optional Extras for Modern Retailers

Modern Stafford retailers often face risks that go beyond physical damage. If you collect customer data or sell through a website alongside your physical shop, cyber insurance is no longer optional. It protects you against the costs of data breaches and digital business interruption. Additionally, consider legal expenses cover. This provides a safety net for employment disputes or lease disagreements, which can be particularly complex for businesses in historic town centre properties. These “add-ons” transform a basic policy into a comprehensive shield for your entire business operation.

Securing Your Stafford Business with Just Quote Me

Choosing the right partner for your shop insurance for retail business in stafford involves more than just comparing premiums. With over 30 years of local Staffordshire experience, Just Quote Me provides a level of insight that automated algorithms simply cannot replicate. We don’t just process data; we understand the local retail landscape. Our team bridges the gap between small business owners and a panel of the UK’s leading insurers, ensuring you get the weight of a national provider with the care of a local neighbour. For a streamlined experience that removes the guesswork, Just Quote Me to secure your business future.

Our approach is intentionally human-centric. When an incident occurs, you don’t want to navigate a complex phone menu or wait days for an automated response. You want a steady hand to manage the administrative burden so you can focus on your customers. We handle the claims process with the same efficiency we use to secure your policy, acting as your advocate to ensure fair and fast resolutions. This reliability is why so many Stafford retailers trust us to manage their professional risks year after year.

Why Choose a Local Independent Broker?

National call centres lack the regional context required for accurate underwriting. We know Stafford’s high streets, from the pedestrianised town centre to the surrounding business parks, intimately. This regional expertise translates into more precise risk assessments, which often leads to more competitive premiums for our clients. By choosing a local independent broker, you’re also reinvesting in the Staffordshire economy. You’re partnering with a team that visits the same shops and supports the same local events that you do. It’s a pragmatic choice that benefits both your bottom line and your community.

Get Started with Your Retail Protection

We’ve streamlined our process to respect your time. Whether you need shop insurance or specialized employers liability insurance, we make the transition frictionless. Our role is to simplify the complex legal requirements and financial protections, providing you with a clear path to FCA-compliant security. Protecting your investment shouldn’t be a source of stress; it should be a source of confidence. We invite you to experience the difference that expert, local advice makes for your retail operation.

Future-Proof Your Stafford Retail Presence

Securing the right shop insurance for retail business in stafford is more than just a regulatory hurdle. It’s a strategic move to safeguard your livelihood against local risks and the common pitfalls of underinsurance. By choosing a bespoke policy that accounts for both your physical presence on the high street and your online operations, you ensure that your business remains resilient throughout 2026 and beyond. A tailored approach means you aren’t paying for unnecessary extras while keeping your core assets fully protected.

Just Quote Me acts as your trusted advisor, leveraging over 30 years of industry experience to find the right fit for your shop. As an FCA-authorised independent broker, we provide access to a broad network of top UK insurers, giving you the benefit of competitive local pricing and high-level protection. We handle the complex administrative burdens so you can stay focused on your customers and your growth. Protect your Stafford business today with a partner who values your success. We look forward to helping your retail brand thrive in our local community.

Frequently Asked Questions

What is the most important insurance for a shop in Stafford?

Public Liability Insurance is widely considered the most critical cover for any customer-facing business. It protects your livelihood against legal claims for injury or property damage sustained by visitors on your premises. While not legally mandated like Employers’ Liability, many landlords in Stafford town centre require this protection as a standard condition of your commercial lease.

Is Employers’ Liability insurance mandatory for my small retail business?

Yes, Employers’ Liability is a legal requirement if you employ at least one person, including part-time or seasonal staff. You must maintain a minimum of £5 million in coverage to comply with UK law, though we typically provide £10 million as a standard baseline. Operating without this cover can result in fines of up to £2,500 for every day your business remains unprotected.

How much public liability cover should a typical Stafford shop have?

Most Stafford retailers choose between £2 million and £5 million in public liability cover depending on their specific risk exposure. If you participate in local events or street markets, organisers often specify a minimum limit of £5 million. We recommend reviewing your specific footfall and contract obligations with a broker to ensure your chosen indemnity limit provides sufficient financial security.

Can I combine my physical shop and online store under one policy?

You can certainly secure shop insurance for retail business in stafford that covers both your high street presence and your digital sales channels. This unified approach ensures your stock is protected whether it is in your shop window or a separate storage area awaiting dispatch. It also allows you to integrate cyber liability to defend against data breaches and online business interruption.

Does shop insurance cover my stock while it is being delivered?

Standard contents insurance usually only protects your inventory while it is inside your business premises. To protect goods while they are being moved in your own vehicles or by a courier, you must add “Goods in Transit” cover. This is a vital addition for Stafford shops that handle local home deliveries, ensuring your investment is protected against theft or damage on the road.

What happens if my shop in Stafford is flooded or damaged by fire?

Buildings and contents insurance will cover the physical costs of repairs and stock replacement following a fire or flood. However, you also need Business Interruption cover to protect your income while your shop is unable to trade. This ensures you can continue to pay fixed costs, such as rent and staff wages, while your premises are being restored to a workable condition.

How can a Stafford insurance broker save me money compared to online sites?

A local broker saves you money by providing a precise risk assessment that prevents the costly mistake of underinsurance. Unlike automated systems, we understand the specific geography of Stafford and can identify discounts based on your actual security measures. This pragmatic approach ensures you only pay for the protection you need while maintaining access to a broad panel of leading UK insurers.

What information do I need to provide for a shop insurance quote?

To obtain an accurate quote for shop insurance for retail business in stafford, you will need to provide your full business address and an estimated replacement value for your stock and fittings. You should also have your annual turnover, employee numbers, and five years of claims history ready. Details regarding your shop’s physical security, such as alarm grades and shutter types, are also essential for securing the best rates.

Article by

Just Quote Me

JustQuoteMe Ltd is an independent UK insurance brokerage specialising in business and personal insurance solutions. With over 35 years of industry experience, the company provides tailored insurance cover for businesses, landlords, tradespeople, hospitality venues, fleets, and individuals across the UK. Known for its personal service, expert advice, and competitive premiums, JustQuoteMe Ltd works with leading insurers to deliver bespoke policies designed around each client’s unique needs. The company is authorised and regulated by the Financial Conduct Authority (FCA No. 586607) and has built a reputation for trusted, straightforward insurance guidance and long-term client relationships.

by jqm | Jun 6, 2026 | Insurance

Did you know that 46% of UK commercial properties are currently underinsured, often by as much as 40%? In a city like Stoke-on-Trent, where historic pottery-era buildings sit alongside modern developments, getting your valuation wrong is a common and costly mistake. You’re likely already feeling the pressure of rising construction costs and the upcoming April 2026 business rates revaluation. It’s frustrating to deal with national call centers that don’t understand the structural nuances of a Victorian factory or the specific risks of the North Staffordshire landscape.

We’re here to help you secure your investment with expert advice on finding bespoke commercial property insurance stoke-on-trent in this evolving market. This guide provides a straightforward roadmap to navigating 2026 regulatory changes, ensuring your policy includes vital protections like loss of rent and liability. You’ll learn how to achieve an accurate property valuation and why a local contact is your best asset for claims support. We will show you how to move past generic coverage to find a solution that’s as unique as your business premises.

Key Takeaways

- Learn why rising rebuild costs in 2026 require a shift in how you calculate your property’s sum insured to avoid significant financial gaps.

- Discover how to effectively manage the unique insurance risks associated with Stoke-on-Trent’s industrial heritage and older pottery-era buildings.

- Identify the essential core coverages, from buildings and stock to machinery, that form a complete shield for your business assets.

- Find out how a professional 2026 Reinstatement Cost Assessment helps you secure competitive rates for commercial property insurance stoke-on-trent.

- Understand the value of a local, independent brokerage that offers personal claims support and access to a wide network of specialist UK insurers.

Understanding Commercial Property Insurance in Stoke-on-Trent for 2026

Commercial property insurance in Stoke-on-Trent serves as a multi-layered shield for your business. It protects your physical assets, such as buildings and stock, while also securing your business income against unforeseen disruptions. In 2026, the landscape for Property insurance has changed significantly. Rebuild costs across Staffordshire have risen, with construction material prices seeing a 2% increase as of January 2026. This shift means that standard “sum insured” calculations from previous years are often no longer accurate. If you haven’t adjusted your policy recently, you might be among the 46% of UK businesses that are currently underinsured. It’s a risk that can leave you with a significant financial gap when you need support the most.

Whether you’re an owner-occupier running a local business or a landlord managing a diverse portfolio, your requirements differ. A shop owner needs to protect their inventory and foot traffic risks, while a landlord focuses on loss of rent and property maintenance liabilities. Choosing a local broker over an automated online algorithm is vital for complex Stoke properties. Algorithms often fail to account for the structural intricacies of our city’s heritage buildings. A human-centric approach ensures your commercial property insurance stoke-on-trent is built on facts, not generic data. We manage the complex administrative burdens so you don’t have to, providing a steady hand in a fluctuating market.

Who Needs This Coverage in the Potteries?

The diverse economic makeup of Stoke-on-Trent means various sectors require specialized protection. Retailers in the Hanley and Longton shopping districts must prioritize shop insurance to cover high-value stock and public liability. Meanwhile, commercial landlords managing multi-tenanted industrial units in Fenton or Burslem need robust policies that handle complex lease agreements and common area liabilities. We also see a rise in business owners operating out of converted pottery works. These heritage buildings require a nuanced understanding of traditional construction methods to ensure the coverage is actually valid in the event of a total loss.

The Shift in 2026 Insurance Requirements

This year, insurers are placing an increased focus on ESG (Environmental, Social, and Governance) compliance. Properties with better energy efficiency ratings or sustainable materials often see more favorable premiums. Additionally, the integration of smart building technology in modern warehouses is starting to influence rates, as these systems can detect leaks or fires before they become catastrophic. One of the most critical lessons for 2026 is the danger of using “Market Value” as an insurance metric. Market value fluctuates with the economy, but “Reinstatement Cost” reflects the actual expense of rebuilding your property from the ground up. In a market where 70% of properties are underinsured, prioritizing reinstatement cost is the only way to truly secure your investment.

Core Coverage: What Your Policy Must Include

A robust policy for commercial property insurance stoke-on-trent isn’t just about the bricks and mortar. It’s a complex assembly of different protections that work together to safeguard your financial future. While many business owners focus solely on the building’s physical structure, a comprehensive policy must address the risks to your contents, your legal responsibilities, and your ongoing income. Unlike generic online products, a bespoke policy ensures that the specific nuances of your property type are reflected in the fine print.

The Association of British Insurers guide to commercial property insurance highlights that these policies typically combine several types of cover into one package. For Stoke-on-Trent business owners, this includes:

- Buildings Insurance: This covers the cost of repairing or rebuilding the structure after damage from fire, lightning, or explosions. In our region, specific attention must be paid to flood and subsidence risks.

- Contents and Stock: If you’re an owner-occupier, this protects your machinery, furniture, and any improvements made to the premises.

- Loss of Rent: For landlords, this is vital. It ensures you still receive income if a covered event, like a fire, makes the property uninhabitable for your tenants.

- Property Owners’ Liability: This protects you if a third party is injured on your property and holds you legally responsible.

If you’re unsure which specific components your building requires, you can speak with a local expert to tailor your policy to your exact needs.

Essential Liability Protections

Liability is often where the line between “standard” and “bespoke” insurance becomes clear. Every property owner has a “Duty of Care” to anyone entering their premises, whether they’re a tenant, a delivery driver, or a visitor. Public liability insurance is the cornerstone of this protection, handling the legal costs and compensation claims arising from accidental injury or property damage. If you employ staff to manage or maintain your properties, employers liability insurance is a legal requirement in the UK. Even if you only have one part-time caretaker, failing to have this cover can lead to significant fines and unprotected legal claims.

Business Interruption and Income Security

Income security is frequently overlooked in basic policies. In the current Stoke market, where rental yields are high but rebuild times can be lengthy due to material shortages, calculating the correct indemnity period is crucial. An indemnity period is the length of time the insurer will pay for loss of rent. While 12 months used to be the standard, many 2026 policies now favor 24 or 36 months to account for planning delays and construction timelines. Your policy should also include “Alternative Accommodation” clauses for commercial tenants, ensuring their business can continue elsewhere while your property is repaired. This maintains the tenant relationship and secures your long-term investment.

Navigating Stoke-on-Trent’s Unique Property Risks

Stoke-on-Trent presents a property landscape unlike any other in the West Midlands. The city is currently in a state of transition, where 19th-century pottery works are being repurposed into creative studios and vast industrial sites are evolving into modern logistics hubs. This mixture of old and new creates specific challenges for anyone seeking commercial property insurance stoke-on-trent. National insurers often rely on automated data that flags older postcodes as high risk without understanding the local context. We bridge that gap by using regional expertise to present a clearer picture to underwriters, ensuring your premiums reflect the actual risk rather than a generic algorithm’s guess.

Insuring Stoke’s Older Industrial Assets

Many of the city’s commercial units carry listed building status or are located within conservation areas in towns like Burslem and Longton. These heritage assets require specialized underwriting because traditional policies don’t account for the high cost of period-accurate materials. If a fire damaged a historic kiln or a brick-built factory, the reinstatement requirements from the local authority could far exceed a standard rebuild estimate. We work directly with you to address outdated electrical systems and fire safety measures, negotiating with specialist insurers who understand non-standard construction. This human-centric approach ensures you aren’t penalized for the city’s industrial history while maintaining the integrity of your investment.

Environmental and Geographic Factors

Stoke’s geography also plays a significant role in your risk profile. Properties near the River Trent or the extensive canal network require careful flood risk assessments. Since the Environment Agency estimates that one in six UK properties is at risk of flooding, it’s vital to use local knowledge to challenge generic maps that might unfairly inflate your premiums. Beyond water risks, the region’s historical mining activity introduces a potential for subsidence that modern algorithms often exaggerate. We help you navigate these geographic factors by providing insurers with detailed maintenance records and professional surveys that prove your property’s stability.

The city centre’s ongoing regeneration also means many sites are either under renovation or awaiting new tenancies. During these periods, vacant property risks such as arson, vandalism, or water damage become a primary concern. Whether you’re involved in a major development project requiring contractors all risk insurance or you’re managing a site between leases, we ensure your coverage remains continuous. We manage the complex administrative burdens of these transitions so you can focus on your investment’s growth without worrying about gaps in your protection.

How to Secure Competitive Rates in the 2026 Market

The UK commercial property insurance market is currently in a “soft cycle” as of early 2026, providing a unique window for Stoke business owners to optimize their overheads. Data from Q1 2026 shows that property insurance rates decreased by 10% on average, but these reductions aren’t automatic. Insurers are applying greater scrutiny to risk management, rewarding those who provide detailed evidence of property maintenance and security. To capitalize on this, you should consider consolidating your various holdings into a single commercial property insurance policy. Portfolio consolidation often triggers volume discounts and eliminates the coverage gaps that occur when managing multiple individual renewals.

Leveraging an independent broker is your most effective tool for accessing competitive rates. We provide access to “broker-only” schemes and specialist markets that don’t appear on automated comparison platforms. These niche underwriters often have a higher appetite for the specific risks found in North Staffordshire, such as converted industrial units. By presenting a professional risk profile to these markets, we can often secure terms that reflect the actual quality of your building rather than a generic postcode average. If you’re looking to reduce your costs while improving your protection, request a review of your current property portfolio to see where savings can be made.

The Dangers of Underinsurance in 2026

Underinsurance is the #1 threat to Stoke property owners. With construction material prices approximately 2% higher in January 2026 than in the previous year, valuations from even 18 months ago are likely obsolete. If your property is undervalued, insurers apply the “Condition of Average” clause during a claim. This means if you’ve only insured the building for 70% of its true reinstatement cost, the insurer is entitled to pay out only 70% of any claim, regardless of its size. A professional 2026 Reinstatement Cost Assessment (RCA) is essential to ensure your commercial property insurance stoke-on-trent provides the full financial protection you expect.

Risk Management as a Premium Lever

Modern underwriters are increasingly focused on data-led risk assessments. Implementing robust security measures, such as high-grade locks and monitored CCTV systems, can act as a direct lever to lower your annual premiums. Regular maintenance is equally vital; keeping a digital log of roof inspections, electrical testing, and fire suppression servicing proves to an insurer that you’re a proactive owner. For landlords, your tenant vetting process also plays a role. Demonstrating that you lease to established businesses with good track records reduces the perceived risk of “moral hazard” and can help us negotiate more favorable rates on your behalf.

Bespoke Insurance Solutions from Just Quote Me

Just Quote Me brings over 30 years of independent brokerage expertise to the Staffordshire business community. While newer competitors might offer generic digital services, we provide a deep-rooted history of reliability that national call centres simply can’t match. We understand that commercial property insurance stoke-on-trent requires a nuanced approach that considers both the city’s industrial past and its commercial future. Our independent status means we aren’t tied to a single provider; instead, we access a broad network of the UK’s top insurers, from household names like Aviva to specialist underwriters who focus exclusively on non-standard heritage buildings.

Our personality is defined by a pragmatic, human-centric attitude toward the industry. We act as your trusted advisor, managing the complex administrative burdens so you don’t have to. When you face the challenges of the 2026 market, such as shifting rebuild costs or new regulatory requirements, we provide the steady hand needed to keep your investment secure. This partnership extends far beyond the initial quote. In the event of a claim, we act as your advocate, ensuring the process is efficient and that you receive the full support your policy promises. We believe in plain, honest communication that puts your business’s security first.

Why Stoke Businesses Choose an Independent Broker

The value of human-to-human advice is indispensable in today’s increasingly automated market. When you choose an independent broker, you’re opting for a personalized experience where your specific risks are understood in detail. We know the Stoke-on-Trent landscape because we are part of it. We recognize the difference between a modern warehouse in a logistics hub and a converted pottery works in Burslem. This regional expertise allows us to challenge generic risk assessments and negotiate better terms on your behalf. We handle the paperwork and the negotiations with underwriters, allowing you to focus your energy on growing your business while knowing your assets are fully protected.

Get Started with Your Tailored Protection

Securing a bespoke policy is a straightforward and efficient process. To ensure we can provide the most accurate advice during your consultation, it’s helpful to have your latest Reinstatement Cost Assessment and any maintenance logs ready. We’ll walk you through the specifics of your property to identify any potential gaps in your current coverage, such as inadequate loss of rent periods or overlooked liability risks. Our goal is to provide a frictionless experience that moves you quickly from inquiry to complete peace of mind. Your investment deserves more than a standard algorithm; it deserves a policy built by experts who understand your sector.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Secure Your Stoke Property Investment for the Future

Navigating the complexities of the 2026 property market doesn’t have to be a solo effort. By focusing on accurate reinstatement costs and understanding the specific risks of the Potteries, you can ensure your business remains resilient against any disruption. Finding the right commercial property insurance stoke-on-trent is about more than just a certificate; it’s about securing a partner who understands the local landscape and the nuances of your specific sector. We prioritize human-to-human service over automated systems to ensure your coverage is as precise as it is reliable.

At Just Quote Me, we bring over 30 years of industry experience to every client relationship. As an FCA-authorised and regulated broker, we provide transparent, straightforward advice and direct access to an extensive network of top UK insurers. We manage the administrative weight and the complex negotiations so you don’t have to. Request a Call back for free Expert advice today to see how we can tailor a policy to your exact needs. Your property is one of your most significant assets, and we’re here to make sure it’s protected with the precision and local insight it deserves.

Frequently Asked Questions

Is commercial property insurance a legal requirement in the UK?

No, commercial property insurance isn’t a legal requirement in the UK, but it’s nearly always a mandatory condition of your mortgage or lease agreement. While the law doesn’t force you to protect your building, it does mandate Employers’ Liability Insurance if you have any staff. Protecting your physical assets is a pragmatic business decision to ensure you don’t face total financial loss after a fire or flood.

Does commercial property insurance cover my tenants’ belongings?

No, your policy only covers the structure and any contents or machinery that you own as the landlord. Your tenants are responsible for insuring their own stock, equipment, and personal belongings. It’s standard practice to include a clause in your lease agreement requiring tenants to maintain their own contents and liability insurance. This clear separation of responsibility prevents disputes during the claims process.

What happens to my insurance if my commercial property in Stoke becomes vacant?

Standard policies usually reduce or cancel coverage once a property sits empty for more than 30 consecutive days. If your building in Stoke becomes vacant between tenancies, you must notify your broker immediately to arrange unoccupied property insurance. This specialized cover addresses higher risks of vandalism, arson, and undetected water leaks. You’ll likely need to perform regular inspections and ensure the property is fully secured to maintain valid protection.

How often should I update my property valuation for insurance purposes?

You should review your property valuation annually to account for construction inflation and material cost increases. Since construction prices were 2% higher in January 2026 than the previous year, older valuations are likely inaccurate. Significant renovations or extensions also trigger the need for an immediate update. Keeping your valuation current is the most effective way to avoid the “Condition of Average” clause and ensure full claim payouts.

Can I include public liability and buildings insurance in one policy?

Yes, most insurers allow you to bundle buildings, contents, and public liability into a single, comprehensive policy. This consolidation often results in lower total premiums and simplifies your administration by having one renewal date. When arranging commercial property insurance stoke-on-trent, we typically recommend this combined approach to ensure there are no gaps between your physical asset protection and your legal liability coverage.

How does the ‘reinstatement cost’ differ from the ‘market value’ of my building?

Reinstatement cost is the total expense required to rebuild your property from scratch, including labor, materials, and professional fees. In contrast, market value is simply the price a buyer would pay for the property in the current real estate market. For insurance purposes, you must use the reinstatement cost. In Stoke, heritage buildings often have a reinstatement cost that far exceeds their market value due to specialized masonry and period-accurate materials.

What specific information do I need to provide for a Stoke-on-Trent commercial quote?

To secure an accurate quote for commercial property insurance stoke-on-trent, you’ll need the property’s full address, construction year, and details of any heritage listings. You should also provide information about the current tenants’ business activities, existing security measures like CCTV or shutters, and your claims history from the last five years. Having a recent professional reinstatement cost assessment ready will help us find the most competitive rates from our network of top UK insurers.

How can an independent broker save me money compared to comparison sites?

Independent brokers access “broker-only” markets and specialist schemes that comparison sites can’t reach. We save you money by presenting your specific risk profile to underwriters in a way that highlights your proactive maintenance and security. Instead of a generic algorithm-based price, you get a rate based on the actual quality of your property. We also ensure you don’t pay for unnecessary add-ons while preventing costly underinsurance errors.

Article by

Just Quote Me

JustQuoteMe Ltd is an independent UK insurance brokerage specialising in business and personal insurance solutions. With over 35 years of industry experience, the company provides tailored insurance cover for businesses, landlords, tradespeople, hospitality venues, fleets, and individuals across the UK. Known for its personal service, expert advice, and competitive premiums, JustQuoteMe Ltd works with leading insurers to deliver bespoke policies designed around each client’s unique needs. The company is authorised and regulated by the Financial Conduct Authority (FCA No. 586607) and has built a reputation for trusted, straightforward insurance guidance and long-term client relationships.

by jqm | Jun 5, 2026 | Insurance

Did you know that 93% of UK properties are currently insured for the wrong amount, with 70% being dangerously underinsured? For a tradesperson in the West Midlands, this isn’t just a statistic; it’s a significant risk to your livelihood. You’re likely already managing the 2026 National Living Wage increases and rising material costs, so the last thing you need is a rejected claim because of fine print you didn’t understand. Securing the right general builder insurance staffordshire is about more than just ticking a box for a local contract. It’s about ensuring your business survives a theft or a site accident.

We understand that you want straightforward protection without the headache of complex jargon. You’ll discover how to manage the 2026 regulatory landscape, including the transition of the Building Safety Regulator to an independent body and the new Future Homes Standards. This guide provides a clear path to comprehensive cover, from public liability to hired-in plant. We’ll show you how to protect your tools from regional theft trends and obtain the FCA-regulated advice your building business deserves.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Key Takeaways

- Understand why generic policies often fail during complex claims and how to tailor your cover to the 2026 regulatory environment in the West Midlands.

- Identify the essential legal requirements for Employers Liability and why Public Liability remains the non-negotiable foundation for every building project.

- Find out how to structure your general builder insurance staffordshire to include Contractors All Risk, protecting both your materials and your reputation on-site.

- Gain insights into managing regional risks, from the structural complexities of period properties in Stone to the specific insurance criteria required for Stafford new builds.

- Learn how to simplify the quote process by focusing on expert-led human oversight rather than automated systems to ensure no detail is missed.

Why General Builders in Staffordshire Need Bespoke Insurance in 2026

The construction industry in Staffordshire has entered a more regulated era in 2026. With the Building Safety Regulator (BSR) operating as an independent body since January and the introduction of the Future Homes Standard in March, general builders face stricter compliance hurdles than ever before. Relying on a generic policy is a gamble that rarely pays off. These “off-the-shelf” options often fail to account for the specific site risks found in Stafford or Newcastle-under-Lyme, leaving you vulnerable during complex claims. When the fine print doesn’t align with the 2026 Construction Products Regulations, your business bears the financial brunt.

Securing high-value contracts now requires more than just a basic liability insurance certificate. Local developers and authorities demand proof of comprehensive cover that reflects current labor costs, which have risen following the April 2026 National Living Wage increase. While employers liability insurance remains a legal mandate if you hire apprentices or laborers, other covers are commercially essential for survival. Without tailored general builder insurance staffordshire, a single rejected claim regarding non-compliant materials or a safety breach could permanently halt your operations.

The Risks of General Building in the West Midlands

Site accidents remain a primary concern for the HSE in the West Midlands, with falls from height still accounting for a significant portion of local incidents. The financial fallout for a sole trader can be devastating without a robust safety net. Tool theft and site vandalism are also persistent trends across Staffordshire, making specific plant and machinery cover vital. Local building regulations, often managed by partnerships like Central Building Control, mean your insurance must accurately reflect the standards and scale of the projects you undertake. If your policy doesn’t match the project’s complexity, you’re effectively uninsured.

Independent Broker vs. Comparison Sites

Automated comparison sites often leave dangerous gaps in your protection. They don’t understand the nuances of a renovation project in Stone or the specific requirements of a Staffordshire Moorlands development. Just Quote Me offers a human-centric alternative to these faceless systems. Our team uses decades of industry experience to ensure your builders insurance is functional rather than just cheap. Having a local office in Stone means you have a partner who understands the regional market and provides direct, pragmatic support when a claim arises. We manage the administrative burden so you can focus on the build.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Essential Liability Cover: Protecting Your Building Business

Liability cover is the safety net that prevents a single error from bankrupting your firm. While many providers offer a standard £1 million limit, Staffordshire projects often require more. If you’re working on a local authority contract or a high-value private development, a £2 million or £5 million limit is frequently the baseline. It’s crucial to look beyond the price tag; many policies contain restrictive clauses regarding “working at height” or “depth limits” that generic sites fail to highlight. If your scaffolding exceeds a specific height or your groundworks go deeper than the policy allows, you’re effectively operating without cover. Ensuring your general builder insurance staffordshire accounts for these technicalities is vital for long-term security.

Public Liability for Staffordshire Builders

Public Liability (PL) insurance covers you if a third party is injured or their property is damaged because of your work. Imagine a scenario where a ladder slips on a site in Stafford, injuring a passerby, or a burst pipe causes extensive water damage to a period property in Stone. Without robust Public Liability Insurance, these incidents could result in legal fees and compensation costs that most small businesses simply can’t absorb. We focus on providing policies that don’t just meet the minimum requirements but offer genuine protection against the specific risks found on West Midlands building sites.

Employers Liability and Sub-Contractors

If you hire any staff, even on a casual basis, having insurance isn’t just a choice. It’s a legal requirement for employers’ liability insurance under the Employers’ Liability (Compulsory Insurance) Act 1969. The distinction between sub-contractors is where many builders get caught out. Bona-fide sub-contractors usually provide their own insurance and materials, whereas labour-only sub-contractors work under your direction and must be covered by your policy. Failing to correctly identify these roles can lead to significant fines. You can find more detail on Understanding Employers Liability Insurance to ensure your team is protected correctly.

Professional Indemnity (PI) is another vital layer, especially for builders who offer design-and-build services. If a client claims your professional advice or design led to a financial loss, PI covers the legal defense and any damages awarded. It’s an essential component for any builder moving into more complex project management. You can explore Professional Indemnity Insurance to see if your current contracts require this level of protection. For a policy that covers every angle of your liability, it’s best to consult with a specialist broker who understands the local trade.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Beyond Liability: Contractors All Risk and Specialist Protection

Liability insurance protects you against damage to others, but it does not cover the work you have already completed or the gear you use every day. If a storm destroys a half-finished extension or a fire breaks out on a site in Newcastle-under-Lyme, you need more than just public liability. This is where comprehensive general builder insurance staffordshire expands to protect your own assets. Without specific cover for the project itself, you could be forced to restart a build at your own expense, potentially wiping out your profit margins or worse.

Contractors All Risk Insurance Details are essential for any builder undertaking major renovations or new builds. This policy protects the physical works, on-site materials, and temporary structures like site huts against fire, flood, and storm damage. For mortgage-backed renovations, lenders usually insist on this cover because it protects their financial stake if the property is damaged mid-build. It ensures that if the worst happens, the funds are available to repair the damage and continue the project without delay.

Contractors All Risk Explained

CAR insurance acts as a safety net for the entire construction site. It covers everything from the bricks and timber waiting to be used to the structural elements already in place. Many builders find this cover a prerequisite when tendering for larger contracts in Stafford or Stone. It provides peace of mind to both the builder and the client, ensuring that environmental factors or accidental damage won’t derail the project’s timeline or budget.

Protecting Your Equipment and Plant

Plant and machinery are significant investments, and their loss can bring a project to a standstill. If you use excavators, mixers, or dumpers, Plant and Machinery Insurance is vital. Hired-in plant is a particular risk; most hire agreements make you responsible for the replacement cost and the ongoing hire fees until the item is replaced. This can quickly run into thousands of pounds that most small firms aren’t prepared for. Following Health and Safety Executive (HSE) construction guidance helps manage site hazards, but it doesn’t stop a determined thief.

In the West Midlands, van and tool theft remain persistent challenges for the trade. Insuring your kit through van and tools insurance isn’t just about the cost of a drill. It’s about the lost work days and the stress of replacing specialized equipment while your project sits idle. Finally, business interruption cover can provide a lifeline if a major incident halts your work, helping you maintain cash flow and pay your bills while you get back on your feet.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Navigating Staffordshire Building Projects: Regional Risks

Staffordshire offers a diverse range of building opportunities, but each comes with its own localized risks. If you’re renovating a period property in Stone, you’re dealing with structural complexities that don’t exist in modern housing. These older buildings often require specialized materials and techniques, which can significantly inflate reinstatement costs if things go wrong. With average rebuild costs in the UK rising by 3-5% in 2026, ensuring your general builder insurance staffordshire accurately reflects these values is essential to avoid the trap of underinsurance.

Contrast this with the new build developments around Stafford. Here, developers and main contractors set rigorous insurance criteria that you must meet before even stepping onto the site. They often require specific indemnity levels and proof of comprehensive cover that includes hired-in plant. Meeting these high standards isn’t just about compliance; it’s a competitive advantage that proves your reliability. For those involved in roofing or multi-storey extensions, Specialist Insurance for Working at Height is a critical addition. Standard policies often exclude or limit these activities, yet they represent some of the highest risks in the trade.

Local Contract Compliance

Working with Staffordshire County Council or other regional authorities usually involves meeting pre-defined insurance mandates. Local contractors prefer working with builders who have verified, comprehensive cover because it reduces their own liability. Using a broker with a deep understanding of the local market ensures your policy isn’t just a generic template. We know how regional project scales and specific site risks influence the type of protection you need to win and keep local contracts. It’s about building a reputation for professional reliability alongside your physical structures.

Regional Crime Trends and Prevention

Site security is a major factor in determining your premium, especially within the West Midlands. Insurers often require specific measures, such as secure fencing or GPS tracking on plant, before they’ll provide cover. Your specific postcode in Staffordshire can affect your costs, as some areas show higher frequencies of tool and equipment theft. For remote sites, such as those near ongoing HS2 works, practical prevention like heavy-duty locks and overnight removals are often mandatory policy conditions. If you’re unsure if your current site security meets your insurer’s requirements, you should speak to a specialist at Just Quote Me today.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Securing Your Trade: How to Get the Right Builder Insurance Quote

The process of securing general builder insurance staffordshire shouldn’t feel like a second job. At Just Quote Me, we’ve refined our approach to ensure that speed never comes at the expense of accuracy. While automated comparison sites rely on rigid algorithms that often miss the nuances of your specific trade, we combine efficient technology with expert human oversight. This means your policy is reviewed by someone who understands the difference between a residential extension in Lichfield and a commercial renovation in Stafford, ensuring every risk is accounted for before you sign on the dotted line.