Imagine it’s a Tuesday morning and you’ve just received a formal challenge to a possession notice under the latest UK rental reforms. Without protection, you’re facing solicitor fees that often start at £250 per hour, which can quickly wipe out a year’s worth of rental profit before you even reach a courtroom. You likely already feel that being a landlord in 2026 is more like walking a legal tightrope than managing a simple investment. With the constant shift in tenant rights and the rise in HMRC tax investigations, the margin for error is smaller than ever. Having landlord legal expenses cover explained is no longer just a luxury; it’s a vital tool to keep your business solvent. This guide will show you exactly how this insurance works to cover your legal costs and protect your livelihood from the financial ruin of a long court battle. We will break down the essential policy inclusions and give you a framework to decide if standalone or bundled cover fits your portfolio best.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Key Takeaways

Navigate the 2026 Renters’ Rights landscape with confidence by understanding why specialist legal cover is now a non-negotiable asset for UK landlords.

Get landlord legal expenses cover explained to ensure you can clearly distinguish between solicitor fee protection and rent guarantee policies.

Learn how to safeguard your rental business against the high costs of tenant evictions and the legal complexities of recovering unpaid rent arrears.

Identify the common “Reasonable Prospects” pitfalls that cause claims to be rejected and how to ensure your case meets the required 51% success threshold.

Discover why partnering with a specialist UK broker provides a more reliable, human-centric alternative to standard comparison sites for complex legal protection.

Why Landlord Legal Expenses Cover is Essential in 2026

Landlord legal expenses cover is a specialist insurance policy designed to pay for solicitor fees, court costs, and legal professional expenses during property-related disputes. It falls under the broader category of Legal Expenses Insurance, providing a financial safety net that allows landlords to defend their rights without draining their life savings. Having your landlord legal expenses cover explained early is vital because the legal environment has become significantly more complex for property owners.

The 2026 rental market operates under a strict Renters’ Rights framework that has made DIY evictions virtually impossible. With the total removal of “no-fault” Section 21 notices, every possession claim now requires specific legal grounds and robust evidence. If you make a procedural error, you can’t simply start again without facing significant delays and costs. This policy provides peace of mind through 24/7 legal helplines, giving you immediate access to experts who can review documents and offer advice before a situation escalates into a full-blown court case.

Comparing the cost of a £20,000 court battle to a modest annual premium makes this cover a logical business decision. It shifts the financial risk from your personal bank account to the insurer, ensuring that your landlord legal expenses cover explained by a broker translates into real-world protection when you need it most.

The Rising Cost of Property Litigation

Legal fees in the UK have continued to climb. By 2026, average hourly rates for experienced solicitors range from £300 in regional areas to over £550 in London. Court backlogs remain a persistent issue, meaning disputes that once took three months can now stretch to nine or twelve months. This delay increases the billable hours required for a case. Because all possession claims are now merit-based, you must prove your case in front of a judge, making professional representation a necessity rather than a luxury.

Who Needs Legal Expenses Cover?

First-time landlords are often at the highest risk because they lack experience with the intricate paperwork required by modern regulations. A single mistake on a Gas Safety certificate or a Deposit Protection notice can invalidate a possession claim. For those managing multiple residential letting portfolios, the statistical likelihood of facing a difficult tenant or a lease dispute increases with every property added. Commercial landlords also rely on this cover to handle complex lease breaches and dilapidation claims that involve technical legal arguments.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

What Does Landlord Legal Expenses Insurance Actually Cover?

Legal disputes don’t just consume your time; they can quickly drain your business capital. Having landlord legal expenses cover explained means understanding that this isn’t just a helpline. It’s a robust financial shield that pays for professional representation across several high-risk areas. Whether you’re dealing with a tenant who refuses to leave or a complex dispute with a contractor, the policy steps in to cover the solicitors’ fees, court costs, and witness expenses that would otherwise come out of your pocket.

Most comprehensive policies provide a suite of protections designed for the modern UK rental market. This includes pursuing tenants for rent arrears after they’ve moved out, provided the debt is over a specific threshold, often £250. It also covers legal action for significant property damage where the repair costs exceed the tenancy deposit. If you’re managing a portfolio, you might also find cover for contract disputes with letting agents or tradespeople who haven’t fulfilled their obligations. If you want to ensure your entire property is protected, you can look into residential letting insurance as a foundation.

Eviction and Possession Proceedings

The eviction process is a minefield of strict deadlines and specific paperwork. Your policy supports you through the entire journey, starting with the legal review of your possession notice to ensure it’s valid. If the tenant doesn’t vacate, the insurer appoints a solicitor to handle the court hearing and, if necessary, the appointment of a bailiff to reclaim the property. This cover extends to squatters and unauthorised occupants who have taken up residence without a tenancy agreement. To trigger a valid claim in 2026, you must have served the correct statutory notice, such as a Section 8 or Section 21 equivalent, within the precise timeframes dictated by current housing legislation.

Data from the National Residential Landlords Association (NRLA) often highlights that legal errors in the early stages of eviction are the primary cause of costly delays. Having an expert review your case early prevents these setbacks.

Nuisance and Trespass Protection

Landlords often face legal challenges that don’t involve their own tenants. This cover provides the legal muscle to deal with anti-social behaviour from neighbours that affects your property or pursuing third parties for trespass. If someone is using your land without permission or there’s a boundary dispute, your insurer provides a solicitor to resolve the matter. Often, these issues are settled through mediation, where your legal representative works to find a solution without the need for a full court hearing, saving months of stress.

HMRC and Tax Investigation Support

Landlords are a high-priority target for HMRC in 2026 following the full implementation of digital reporting requirements. A legal expenses policy provides vital defence costs if you’re selected for an audit. This includes “Aspect” enquiries, which focus on a specific part of your tax return, and “Full” enquiries, where HMRC examines your entire financial history for the year. If the case escalates to a tax tribunal, your policy pays for professional representation to argue your case, ensuring you aren’t bullied by complex tax law. If you’re unsure about your current liability levels, it’s worth reviewing your landlord policy options to see where gaps might exist.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

The Reasonable Prospects Rule and Common Policy Exclusions

Understanding landlord legal expenses cover explained involves more than just looking at the premium. The most frequent reason insurers reject a claim is the “Reasonable Prospects of Success” clause. This isn’t a vague term; it’s a strict legal benchmark. For your insurer to fund your case, an independent solicitor must confirm that your claim has at least a 51% chance of winning. If the odds drop below this threshold at any point during the litigation, the insurer can withdraw funding immediately.

Insurers also demand “procedural correctness” before they agree to take on a case. If you haven’t followed the exact legal steps for an eviction or a rent increase, your prospects of success vanish. This becomes even more critical following recent legislative changes such as the Renters’ Rights Act, which have tightened the rules around how landlords must handle disputes and possession orders. If your paperwork is flawed from the start, your insurance won’t fix it after the fact.

Understanding Reasonable Prospects

When you submit a claim, the insurer appoints an expert solicitor to assess the merits of your case. They look for clear evidence that a court will rule in your favour. If there’s a disagreement between your solicitor and the insurer regarding these odds, most policies allow for an “Independent Counsel” to act as a tie-breaker. Their decision is final, ensuring the process remains fair rather than purely financial for the insurer.

What is Typically Excluded?

You can’t buy insurance for a house that’s already on fire. Most policies include a 90-day waiting period from the start date, meaning disputes arising in the first three months aren’t covered. Other common exclusions include:

Legal costs incurred before you received written consent from the insurer to proceed.

Fines, penalties, or damages a court orders you to pay to a tenant.

Disputes that began or were known to you before the policy started.

The Importance of Documentation

A successful claim relies on a solid paper trail. A missing inventory or an unsigned tenancy agreement can kill your legal claim instantly. You must maintain records of all tenant communications and ensure all deposits are registered in a government-approved scheme. To stay protected, you must report any potential claim or circumstance that might lead to a dispute within 45 days of becoming aware of it. For comprehensive protection, many landlords pair this cover with residential letting insurance to ensure their physical assets are as secure as their legal ones.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Landlord Legal Expenses vs. Rent Guarantee Insurance

Confusion often arises when discussing landlord legal expenses cover explained in the context of financial protection. While they’re frequently sold together, they serve two distinct purposes. Legal expenses insurance pays for the solicitor and the court fees required to regain possession of your property. Rent guarantee insurance, however, pays the actual monthly rent into your bank account while that legal process unfolds.

Many landlords mistakenly assume that legal cover automatically includes rent protection. This isn’t the case. If a tenant stops paying, legal cover ensures you don’t face a £2,500 bill for a specialist solicitor, but it won’t help you cover the mortgage. Bundling these covers is often 15% to 20% cheaper than buying them separately. This synergy provides a seamless safety net for your cash flow, ensuring that a single bad tenant doesn’t lead to a personal financial crisis.

How Rent Guarantee Complements Legal Cover

Rent guarantee insurance typically features an “indemnity period,” which is the maximum timeframe the insurer will cover your lost income. In the current UK market, this usually spans 6 or 12 months. Most insurers won’t offer rent protection as a standalone product; they require you to have legal expenses cover first. This is because the legal team must be actively working to evict the tenant for the rent claim to remain valid. If you manage a mixed-use portfolio, you might find similar requirements within commercial property insurance policies that include residential elements.

Choosing the Right Level of Protection

Deciding between “Legal Only” and “Full Rent Protection” depends on your financial resilience. If you own the property outright and have a high-equity cushion, legal-only cover might suffice to handle the paperwork. However, for the high percentage of UK landlords who rely on rental income to service a buy-to-let mortgage, full protection is vital. Combined premiums are influenced by the monthly rent amount and the tenant’s credit score. A clean credit check often results in lower rates for the combined package, making it a cost-effective way to secure your business.

Protect your investment today. Get Your Free Business Insurance Quote now or Request a Call back for free Expert advice to discuss your specific needs with our UK-based team.

Securing the Right Protection with Just Quote Me

Choosing the right policy requires more than just a quick search on a price comparison site. At Just Quote Me, we bring 30 years of experience to the UK insurance market, helping property owners find clarity when landlord legal expenses cover explained in standard policy documents feels overly complex. We act as an independent broker, which means our loyalty lies with you rather than a single insurance provider. This independence is vital in 2026, as the regulatory landscape for private rentals continues to shift under updated housing legislation and stricter court protocols.

Our 30-year history means we’ve seen every major change in UK property law since the mid-1990s. This perspective allows us to anticipate how new 2026 mediation rules might impact your legal spend. We work directly with specialist underwriters who possess a deep understanding of the current legal climate. This ensures your landlord insurance isn’t just a generic document but a tailored shield. We help you structure your cover to include the specific legal protections your business requires, from contract disputes to tax investigations.

Expert Advice Over Faceless Algorithms

Algorithms often fail to understand the nuances of a difficult tenant dispute or the specific risks of a multi-property portfolio. Talking to our UK-based team provides a human touch that saves both time and money. We don’t just sell a policy; we assist you during the claims process to ensure you meet all necessary criteria from the outset. For those managing larger estates, we integrate this with broader public liability insurance to provide a cohesive safety net. Our goal is to simplify the heavy lifting so you can focus on managing your properties. We provide a steady hand in a complex market, ensuring you aren’t left to navigate the legal system alone.

Get Your Bespoke Quote Today

The process of securing your business is straightforward and logical. We identify your specific risks, compare the wider market, and secure cover that fits your budget. With new court procedures and mandatory mediation requirements becoming standard in 2026, it’s the right time to review your existing legal protection. If you are currently modernising a property or extending your portfolio, we also provide specialised builders insurance to protect your investment during the renovation phase. Don’t leave your livelihood to chance when professional advice is a phone call away. Our team is ready to do the heavy lifting for you.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Secure Your Rental Portfolio for 2026 and Beyond

Navigating the UK rental market requires more than just finding the right tenants; it demands a robust safety net. With legislative shifts expected throughout 2026, having landlord legal expenses cover explained gives you the clarity needed to protect your property assets. You’ve seen how the “Reasonable Prospects” rule dictates claim success and why separating legal cover from rent guarantees is vital for comprehensive protection. Legal disputes are stressful, but they don’t have to be financially devastating for your business.

Just Quote Me brings over 30 years of industry experience to your side as an FCA Authorised Independent Broker. We’re a human-centric team that understands the nuances of the British property market and the pressures landlords face. You can Get Your Free Business Insurance Quote now to find a tailored policy that fits your budget. If you’re unsure about your specific requirements, Request a Call back for free Expert advice from our UK-based specialists. Taking these simple steps today ensures your rental business remains profitable and protected for years to come.

Frequently Asked Questions

Is landlord legal expenses insurance a legal requirement in the UK?

No, landlord legal expenses cover isn’t a legal requirement in the UK. While the law doesn’t mandate it like motor insurance, most professional landlords view it as essential protection against the rising costs of court proceedings. Since the introduction of the Renters’ Rights Act and subsequent 2026 updates, the complexity of evictions has increased. Carrying this cover ensures you have the financial backing to handle disputes without draining your personal savings.

Does legal expenses cover pay for the tenant’s solicitor if I lose?

Yes, most policies include cover for “adverse costs,” which are the legal fees of the opposing party if a judge orders you to pay them. This is a critical feature because a lost court case could otherwise result in a bill for several thousand pounds. Your policy typically covers these costs up to a set limit, often £50,000 or £100,000, providing a vital safety net for your rental business.

Can I buy legal expenses cover after a dispute with my tenant has already started?

No, you can’t purchase cover for a dispute that’s already in progress. Insurance providers require that the “insured event” or the circumstances leading to the claim happen after the policy start date. Most policies also include a 90 day waiting period at the beginning of the term. If you’re currently facing an issue, it’s too late to insure it, which highlights why having landlord legal expenses cover explained before problems arise is so important.

How much does landlord legal expenses cover typically cost in 2026?

While prices vary based on your portfolio size, basic standalone policies in the UK often start from approximately £60 to £150 per year. Costs can fluctuate depending on whether the cover is a “bolt on” to your buildings insurance or a comprehensive standalone product. According to 2025 industry benchmarks, premiums have remained relatively stable despite inflationary pressures. It’s a small price to pay for access to professional legal teams and 24/7 advice helplines.

What is the difference between Family Legal Protection and Landlord Legal Cover?

Family Legal Protection covers personal issues like consumer disputes or employment tribunals, whereas Landlord Legal Cover specifically targets risks associated with rental properties. You can’t use a standard home insurance legal add on to deal with a tenant eviction or a rent recovery claim. Landlord specific policies include specialized clauses for property damage, squatter eviction, and breach of tenancy agreements that personal policies simply don’t touch.

Will this insurance cover me for disputes regarding my property taxes?

Yes, many comprehensive policies include a “Tax Protection” section that covers professional fees for HMRC investigations into your rental income. This includes representation during full or aspect enquiries into your self assessment tax returns. Given that HMRC opened over 300,000 compliance investigations in recent years, this feature provides peace of mind. It ensures you have an expert accountant or solicitor to handle the paperwork and negotiations on your behalf.

How do I prove my case has a reasonable prospect of success?

Your insurer’s appointed solicitor will review your evidence to determine if there’s a 51% or greater chance of winning the case. This “reasonable prospects” clause is a standard industry requirement for any claim to proceed. You’ll need to provide clear documentation, such as the signed tenancy agreement, evidence of rent arrears, or proof of property damage. If the legal expert believes the case is likely to fail, the insurer won’t fund the litigation.

Does the policy cover the cost of a professional bailiff?

Yes, the policy typically covers the costs of professional bailiffs or High Court Enforcement Officers if you need to physically reclaim your property. Once you’ve secured a possession order from the court, these fees are part of the legal process required to finalize the eviction. Having landlord legal expenses cover explained helps you see that it’s not just about the solicitor; it’s about the entire journey from the first notice to the final locks being changed.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Article by

Just Quote Me

JustQuoteMe Ltd is an independent UK insurance brokerage specialising in business and personal insurance solutions. With over 35 years of industry experience, the company provides tailored insurance cover for businesses, landlords, tradespeople, hospitality venues, fleets, and individuals across the UK. Known for its personal service, expert advice, and competitive premiums, JustQuoteMe Ltd works with leading insurers to deliver bespoke policies designed around each client’s unique needs. The company is authorised and regulated by the Financial Conduct Authority (FCA No. 586607) and has built a reputation for trusted, straightforward insurance guidance and long-term client relationships.

If a burst pipe or electrical fire makes your property uninhabitable tomorrow, do you know exactly which policy keeps your mortgage payments on track while the builders are on site? Many UK landlords mistakenly believe that any missed payment is covered by a single policy, but the wrong choice can leave you facing a monthly shortfall of £1,000 or more. It’s a high-stakes gamble, especially as the 2025 Renters’ Rights Act continues to reshape the legal landscape for property owners.

We understand that your rental income isn’t just profit; it’s the foundation of your financial security. This guide explores the critical role of loss of rent insurance for landlords uk, specifically highlighting the differences between damage-related claims and tenant default. You’ll discover how to handle the complexities of 2026 regulations to ensure your cash flow remains protected against every eventuality. We’ll break down the specific coverage triggers and provide a straightforward roadmap to choosing the right protection for your portfolio.

Key Takeaways

Understand the vital distinction between loss of rent and rent guarantee insurance to ensure your income is protected against both property damage and tenant arrears.

Navigate the impact of the Renters Rights Act 2025 and learn why comprehensive loss of rent insurance for landlords uk is essential in the new legislative landscape.

Discover how to accurately calculate your Gross Rental Income and select the appropriate indemnity period to prevent financial shortfalls during lengthy repairs.

Identify the specific “insured perils” that trigger a claim and how insurers define a property as “uninhabitable” in the current UK market.

Learn the advantages of using a specialist broker to secure bespoke landlord cover that offers tailored protection for individual properties or entire portfolios.

Understanding Loss of Rent Insurance in the 2026 UK Market

Landlords entering 2026 face a complex economic environment. While property remains a solid asset, the risk of income interruption has never been higher. Loss of rent insurance for landlords uk serves as a financial safety net when a property becomes uninhabitable due to an insured event, such as a fire, flood, or significant storm damage. It isn’t just about protecting profit. For many, it’s about survival. When the rent stops coming in, your mortgage lender still expects their payment on the first of the month.

The 2026 market is defined by volatility. Repair costs for UK properties rose by 4.2% in the last year alone, and lead times for specialist contractors remain extended. If a kitchen fire renders your flat unliveable, you might face six months of repairs. Without specific cover, you’re forced to cover the mortgage from your personal savings. Just Quote Me focuses on bridging this gap with clear, no-nonsense advice that keeps your portfolio’s cash flow intact during a crisis.

Loss of Rent vs. Rent Guarantee: The Vital Difference

It’s easy to mix these terms up, but the distinction is critical for your balance sheet. Loss of rent is triggered by physical damage to the structure. If a January storm rips tiles from the roof and causes internal flooding, your policy pays the lost income while the building is repaired. In contrast, Rent Guarantee Insurance covers you if a tenant defaults on their payments due to financial hardship. Most comprehensive residential letting insurance plans offer these as separate add-ons. You shouldn’t assume one covers the other.

Who Needs This Protection Most?

High-geared buy-to-let investors are at the top of the list. With mortgage rates remaining significantly higher than the 2010-2020 average, there’s very little “fat” in the monthly budget to absorb a total loss of income. Commercial property owners also face unique risks, especially if they have long-term lease structures that could be voided by a property becoming unusable for an extended period. A damaged warehouse or shop doesn’t just stop rent; it can disrupt an entire supply chain.

We see a high concentration of risk among portfolio owners in Staffordshire and the West Midlands. Managing multiple units across these regions means a higher statistical chance of an incident. Whether you’re letting out a single terrace in Stoke-on-Trent or a commercial unit in Birmingham, loss of rent insurance for landlords uk ensures that a single pipe burst doesn’t bring down your entire business model. Our team understands these local nuances and helps you find the right fit quickly. We believe in providing a human touch that automated algorithms simply can’t match.

What Exactly Does a Loss of Rent Policy Cover?

Loss of rent insurance for landlords uk isn’t a standalone product; it’s a vital extension that works alongside your buildings insurance. It acts as a financial bridge when a property shifts from being a source of income to a liability. While your commercial property insurance pays for the physical repairs to the bricks and mortar, loss of rent cover replaces the money that should’ve landed in your bank account while those repairs take place.

The Standard Insured Perils

For a claim to be valid, the loss of income must result from a specific “insured peril.” These are defined events that cause physical damage to the property. Insurers don’t cover general rental arrears or tenants who simply stop paying; they cover the fallout from physical disasters. Common perils include:

Fire and Explosion: Significant damage from fires or gas explosions that require long-term renovation.

Flood and Escape of Water: These are the most frequent UK claims. According to 2024 industry data, escape of water from burst pipes accounts for nearly 30% of all domestic property claims in Britain.

Natural Disasters: Coverage for lightning strikes and earthquake damage.

Third-Party Malice: Impact damage from vehicles or malicious damage caused by vandals (though damage by the tenants themselves often requires a specific policy add-on).

Having Loss of Rent Cover is frequently a mandatory requirement for UK buy-to-let mortgage providers. They want to ensure your loan repayments remain consistent even if the building is empty for six months due to a flood.

The “Uninhabitable” Threshold

In 2026, loss adjusters use strict criteria to determine if a tenant must vacate. A property doesn’t need to be reduced to rubble to trigger a claim, but it must fail basic safety and living standards. If a kitchen is damaged but the rest of the flat is functional, the insurer might only pay for a partial loss of rent. However, if the damage is structural or affects essential utilities, it’s a total loss scenario.

In a standard UK policy context, a property is deemed uninhabitable if it lacks essential services like running water, sanitation, or heating, or if structural damage presents a verified risk to the occupants’ safety.

Many policies also include coverage for alternative accommodation. In this scenario, your tenant continues to pay you rent, but your insurer pays for them to stay in a hotel or a comparable rental property. This keeps the tenancy agreement active and prevents you from losing a good tenant during the repair process. If you aren’t sure if your current level of protection is sufficient, you can compare residential letting insurance options to find a better fit for your portfolio.

Rent Guarantee & The Renters Rights Act 2025 Impact

The Renters’ Rights Act 2025 represents the most significant shift in the UK private rented sector for decades. By abolishing Section 21 “no-fault” evictions, the government has fundamentally changed how landlords must manage their properties. You can no longer end a tenancy without a specific legal reason. This change makes loss of rent insurance for landlords uk more than just a safety net; it’s now a core part of a risk management strategy. If a tenant stops paying, the legal route to regaining possession is often slower and more complex under the new Section 8 grounds.

Landlords face longer wait times for court dates and stricter evidence requirements. Understanding the distinction between loss of rent and rent guarantee insurance is vital for staying protected. While standard loss of rent covers income lost due to property damage like fire or flood, rent guarantee specifically addresses tenant default. With the 2025 legislation making it harder to remove non-paying tenants quickly, having a policy that covers your mortgage payments during a legal dispute is essential for maintaining your cash flow.

Protecting Income Against Tenant Default

Rent guarantee policies step in the moment a tenant falls into arrears. These policies typically pay the monthly rent for a set period, often up to 12 months, while you work through the eviction process. It’s a logical addition to your residential letting insurance, providing a comprehensive shield against both physical property damage and financial default. Most insurers require a high standard of tenant referencing to validate your cover. This usually involves a credit check, employment verification, and a reference from a previous landlord. If you skip these steps, you might find your claim rejected when you need it most.

Legal Expenses and Eviction Support

The cost of regaining possession can escalate quickly. Solicitor fees, court costs, and bailiff charges often run into thousands of pounds. A robust insurance policy covers these legal expenses, ensuring you don’t have to drain your savings to enforce your rights. By 2026, many insurance providers will update their terms to include mandatory mediation costs. This aligns with new court requirements designed to settle disputes before they reach a full hearing.

Solicitor Fees: Coverage for specialist legal representation to navigate complex Section 8 proceedings.

24/7 Legal Helpline: Immediate access to expert advice to prevent small disagreements from becoming full-scale legal battles.

Mediation Support: Funding for independent mediation, which is set to become a standard requirement for 2026 possession cases.

Securing loss of rent insurance for landlords uk ensures that your business remains viable even when the legal landscape shifts. It provides the professional support needed to handle difficult tenants without the emotional and financial strain of going it alone. Just Quote Me can help you find a policy that meets these new legislative standards, giving you a steady hand in a changing market.

Calculating Your Coverage: Indemnity Periods and Sums

Calculating the right level of loss of rent insurance for landlords uk starts with an accurate assessment of your Gross Rental Income. This figure represents the total amount of rent you expect to receive before any expenses, such as mortgage payments or management fees, are deducted. If your monthly rent is £1,200, your annual sum insured needs to be at least £14,400. Many landlords make the mistake of only insuring the profit, but you’ll still have fixed costs to cover if the building becomes uninhabitable.

Under-insurance is a frequent trap that leads to reduced payouts. If you tell your insurer your rental income is £15,000 but it’s actually £20,000, you’re 25% under-insured. In the event of a claim, the insurer might apply the “Condition of Average,” meaning they’ll only pay 75% of your lost rent. You’ve got to be precise with these figures to ensure your financial security isn’t compromised when you need it most.

Selecting the Right Indemnity Period

The indemnity period is the maximum length of time your insurer will pay out for lost rent. While a 12-month period might seem sufficient, it rarely covers major incidents like a total loss fire or severe flood. According to 2023 industry data, rebuilding a property in the UK often takes between 18 and 24 months. You must factor in debris removal, architect plans, and the UK planning permission process, which typically takes 8 to 13 weeks for standard applications but can stretch much longer for complex sites. Your indemnity period should always exceed the worst-case repair time to ensure you aren’t left paying the mortgage out of pocket while the property is still a shell.

Avoiding Claim Rejection

Insurers expect you to be proactive with property care. They won’t pay out if the loss of rent is caused by gradual deterioration or a clear lack of basic upkeep. You’ll need to provide clear documentation to support a claim, such as current Assured Shorthold Tenancy (AST) agreements and up-to-date rent ledgers. Without these, proving the exact loss becomes a difficult and lengthy process.

Safety standards also play a massive role in claim approval. Ensuring your gas and electrical safety certificates are current doesn’t just keep you legal; it protects your policy. This is where public liability insurance overlaps with property management. If a tenant is injured due to poor maintenance, you face both a liability claim and a potential rejection of your rent loss claim. Keeping your property in good repair is your best defense against a denied payout.

Ready to secure your rental income with expert advice? Contact Just Quote Me today for a straightforward, professional insurance solution.

Securing Bespoke Landlord Cover with Just Quote Me

Securing the right loss of rent insurance for landlords uk requires more than a simple comparison site search. Property portfolios often involve unique risks that standard policies overlook. As an independent broker with over 30 years of industry experience, Just Quote Me bridges the gap between complex property needs and competitive market rates. We tap into a broad network of top UK insurers, ensuring you don’t pay for unnecessary extras while maintaining robust protection for your rental income. Our independence is your advantage; we work for you, not the insurance companies.

The Personal Touch in a Digital World

Automated algorithms frequently struggle with complex property risks, such as mixed-use buildings or portfolios with varying tenancy types. These digital tools often default to higher premiums or refuse cover entirely when a situation doesn’t fit a pre-set box. We take a different approach. Based in Staffordshire and serving the West Midlands, our team applies local expertise to every application. Our commitment to the “Just Quote Me” philosophy means we strip away the jargon and provide a straightforward, human-centric service. We handle the heavy lifting, negotiating directly with underwriters to find the most efficient solution for your specific circumstances.

Next Steps for Your Property Protection

To secure your 2026 income and beyond, you’ll need to prepare specific documentation. Start by gathering your current rental figures, property rebuild values, and tenancy agreements. If you employ staff for maintenance or administration, it’s vital to consult on additional protections. You should consider employers liability insurance to meet your legal obligations and protect your workforce. Having these details ready allows us to build a more accurate profile of your business.

When you’re ready to proceed, our process is designed to be fast and logical. You won’t be stuck in a phone queue or forced to fill out endless, repetitive forms. Instead, we focus on the essentials:

Provide your property portfolio details and total annual rental income.

Discuss any specific concerns, such as long-term void periods or malicious damage.

Receive a tailored quote that consolidates your loss of rent insurance for landlords uk into one manageable policy.

Don’t leave your financial stability to chance. Request your bespoke quote today and experience the clarity of a professional, no-nonsense insurance partnership. We’re here to ensure your investment remains profitable, regardless of what the future holds.

Protecting Your Rental Income in 2026 and Beyond

Navigating the UK rental market in 2026 requires more than just finding the right tenants. With the full implementation of the Renters’ Rights Act 2025, landlords face a regulatory landscape that demands robust financial protection. Securing comprehensive loss of rent insurance for landlords uk ensures that your property investment remains viable even when unexpected damage makes your building uninhabitable. It’s about more than just a policy. It’s about choosing the correct indemnity period to cover the time it actually takes to rebuild or repair. At Just Quote Me, we bring over 30 years of industry experience to the table. As an FCA-authorised independent broker, we provide access to top-tier UK insurance panels to find coverage that fits your specific portfolio. Don’t leave your rental income to chance when the market shifts. Get Your Bespoke Landlord Insurance Quote from Just Quote Me. We’re here to help you secure your future with a straightforward, no-nonsense approach to protection.

Frequently Asked Questions

Is loss of rent insurance a legal requirement for UK landlords?

Loss of rent insurance isn’t a legal requirement under UK law. However, most buy-to-let mortgage lenders make this cover a mandatory condition of your loan agreement. They require this protection to ensure you can still meet your mortgage repayments if a fire or flood makes the property uninhabitable for your tenants. Without it, you’re personally responsible for those monthly costs even if your income stream disappears overnight.

What is the difference between loss of rent and rent guarantee insurance?

Loss of rent insurance covers your income specifically when a property is damaged by an insured event, such as a fire or a burst pipe. Rent guarantee insurance is different because it protects you if a tenant stays in the property but stops paying their rent. It’s important to choose loss of rent insurance for landlords uk if you want to protect against physical damage, as rent guarantee won’t pay out for structural issues that force a tenant to move out.

How long does an indemnity period need to be for a residential property?

Your indemnity period should ideally be at least 24 months to account for potential planning delays and modern construction timelines. While many basic policies offer 12 months, data from the Association of British Insurers indicates that major structural repairs often take longer than a year to complete. A 36-month period is even safer for older properties or complex buildings, providing a vital buffer while you wait for the property to be fully restored and re-let.

Can I claim loss of rent if my property is only partially damaged?

You can claim for partial damage if the incident makes the property legally uninhabitable or prevents the tenant from using essential areas. If a kitchen fire makes the home unusable, your policy triggers even if the rest of the house is fine. The insurer pays the proportion of rent lost while those specific repairs are carried out. You’ll need to prove the damage was caused by a peril listed in your policy, such as impact or water escape.

Does loss of rent insurance cover periods when the property is naturally vacant?

Standard policies don’t cover natural rental voids or gaps between different tenancies. This insurance is designed to replace income lost due to physical damage from unexpected events like storm damage or vandalism. If your property is empty because a lease ended and you haven’t found a new tenant yet, you’ll need to cover those costs yourself. It’s a business risk that insurers view as separate from physical property damage claims.

Will my insurance cover legal fees for evicting a non-paying tenant?

Loss of rent cover doesn’t typically include legal fees for evictions unless you’ve specifically added Legal Expenses protection to your policy. These are separate products designed to handle the costs of regaining possession of your property through the court system. We recommend checking your policy schedule for these extras, as legal costs for a standard eviction in the UK can often exceed £1,500 depending on the complexity of the case.

How has the Renters Rights Act 2025 affected rent protection claims?

The Renters Rights Act 2025 has abolished Section 21 “no-fault” evictions, which means landlords must now provide specific grounds for possession. This change has increased the average time it takes to regain a property, making loss of rent insurance for landlords uk more important than ever. With court processes potentially taking longer under the new rules, having a robust policy helps bridge the financial gap while you navigate the updated legal framework and mandatory ombudsman requirements.

Can I add loss of rent cover to an existing landlord insurance policy?

You can usually add this cover to your existing policy by requesting a mid-term adjustment from your insurance provider. Most brokers allow you to tailor your protection at any point during the year, though it’s often simplest to bundle it during your annual renewal. We can help you integrate this into a bespoke package that includes buildings and liability cover, ensuring there are no gaps in your protection that could leave you out of pocket.

Article by

Just Quote Me

JustQuoteMe Ltd is an independent UK insurance brokerage specialising in business and personal insurance solutions. With over 35 years of industry experience, the company provides tailored insurance cover for businesses, landlords, tradespeople, hospitality venues, fleets, and individuals across the UK. Known for its personal service, expert advice, and competitive premiums, JustQuoteMe Ltd works with leading insurers to deliver bespoke policies designed around each client’s unique needs. The company is authorised and regulated by the Financial Conduct Authority (FCA No. 586607) and has built a reputation for trusted, straightforward insurance guidance and long-term client relationships.

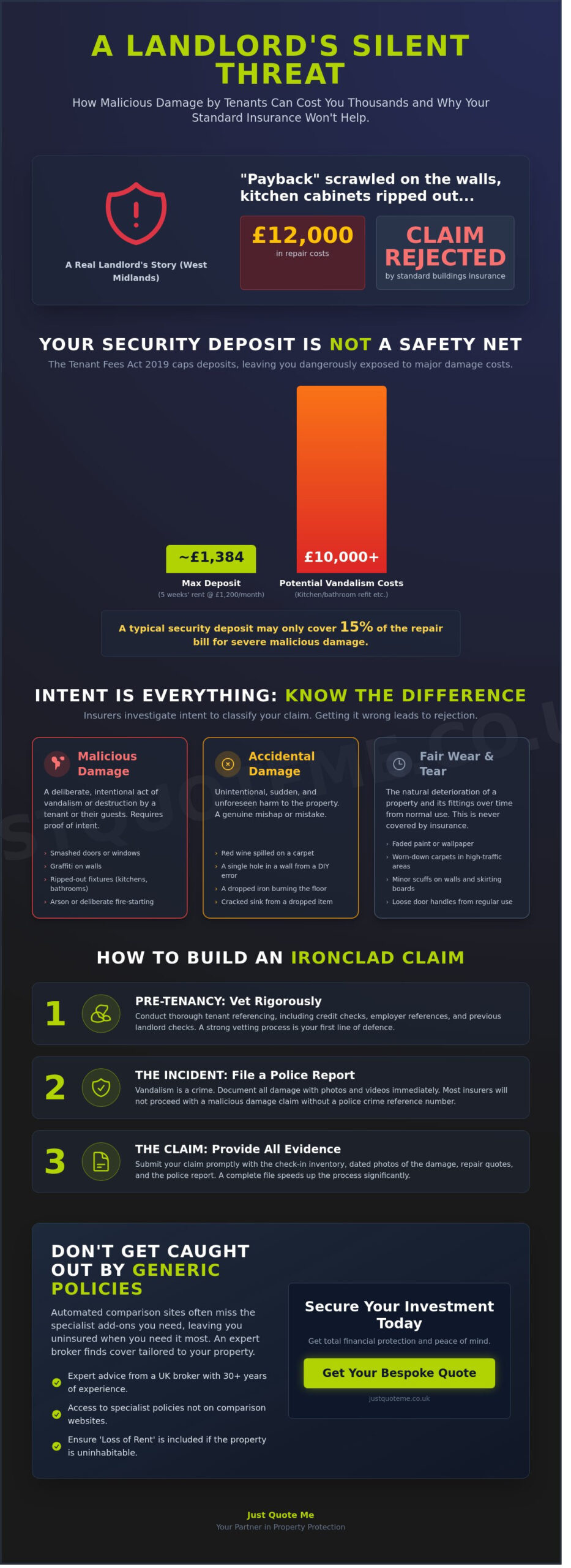

Imagine walking into your rental property after a difficult eviction only to find kitchen cabinets ripped from the walls and “payback” scrawled across the living room plaster. For one landlord in the West Midlands, this nightmare recently resulted in a £12,000 repair bill that their standard buildings insurance completely rejected. It’s a sobering reminder that while most tenancies end smoothly, the financial impact of a disgruntled tenant can be devastating to your bottom line.

You likely already understand that a standard security deposit rarely covers the cost of intentional vandalism. This is where specialist malicious damage by tenant insurance cover becomes your most vital safety net. At Just Quote Me, we believe insurance shouldn’t be a guessing game, especially when your hard earned capital is at risk. We’ll help you navigate the complexities of 2026 policy requirements, from the necessity of obtaining police reports to avoiding common exclusion traps. This guide explains how to secure total financial protection and provides the clear steps needed to ensure your investment remains protected, giving you the peace of mind you deserve.

Key Takeaways

Understand why standard buildings insurance often falls short and how specialist malicious damage by tenant insurance cover protects your investment from intentional harm.

Learn to distinguish between accidental damage and malicious intent to avoid common claim pitfalls like ‘fair wear and tear’ rejections.

Discover how to secure your rental income with ‘Loss of Rent’ extensions that trigger if tenant damage leaves your property uninhabitable.

Get a step-by-step roadmap for handling claims correctly, from conducting essential tenant referencing to filing police incident reports.

Explore the benefits of using an independent UK broker with 30 years of expertise to find tailored coverage that automated comparison sites often miss.

Understanding Malicious Damage by Tenant Insurance Cover

Malicious damage occurs when a person lawfully permitted to be on your property intentionally causes harm or destruction to the structure or its contents. Unlike accidental damage, which covers spills or mishaps, this involves a deliberate act of sabotage. Many landlords assume their basic buildings policy protects them, but most standard products exclude these acts. Securing specific malicious damage by tenant insurance cover is essential because insurers typically view intentional damage by an invited guest as a manageable risk that requires a specialist policy or a specific extension.

The financial impact is often compounded by a heavy psychological toll. Discovering a trashed property leads to extreme stress and significant downtime where no rent is collected. A broker plays a critical role here. We identify which insurers include this protection as a standard feature in residential letting insurance and which require it as an optional extra. This ensures you don’t face a rejected claim during an already difficult period.

The Legal Context: Malicious Damage Act and Landlord Rights

The legal framework for these claims often draws from the Malicious Damage Act 1861, which provides the foundation for how Vandalism and property destruction are prosecuted in the UK. In the context of insurance claims for 2026, intent is defined as the proven, conscious decision by a tenant to cause physical harm to the property, which clearly distinguishes it from wear and tear or simple negligence. Landlords have the legal right to pursue criminal charges or civil litigation, but these processes are slow and expensive. Specialist insurance provides the immediate funds needed to restore the property while legal proceedings take place in the background.

Why Deposits Are Rarely Enough for Malicious Acts

The Tenant Fees Act 2019 restricted most security deposits in England to a maximum of five weeks’ rent. For a property with a monthly rent of £1,200, the deposit is capped at approximately £1,384. This amount is quickly exhausted if a tenant rips out kitchen units, destroys bathroom suites, or smashes internal doors. Repair costs for these acts of sabotage can easily exceed £10,000. While the Deposit Protection Service (DPS) provides a mechanism for recovery, it’s designed for minor disputes rather than major structural damage. Comprehensive malicious damage by tenant insurance cover acts as the only reliable safety net when repair bills dwarf the available deposit funds.

Standard deposits rarely cover more than 15% of a major renovation cost.

Insurance covers the gap between the deposit and the total repair bill.

Policies can also cover the loss of rent while the damage is being repaired.

Malicious Damage vs. Accidental Damage: Knowing the Difference

Understanding the line between a mistake and a deliberate act is vital for any landlord. The core difference lies in intent. Accidental damage happens through clumsiness or a genuine mishap, while malicious damage is a purposeful act of destruction. Having the right malicious damage by tenant insurance cover ensures you aren’t left paying for a tenant’s anger or criminal activity. Insurers look closely at the evidence to decide which category applies to your claim.

Fair wear and tear remains the most common reason for claim rejection in the UK rental market. Property naturally ages. Frayed carpet edges, faded paintwork, and loose door handles are part of a building’s lifecycle. In the UK, strict deposit protection schemes ensure that security deposits cover damage beyond normal wear and tear, not fair wear and tear itself. Landlords, particularly in areas like Staffordshire and the West Midlands, must provide clear proof of intent or negligence for any deductions. If an insurer determines the damage is simply the result of a long tenancy, they won’t pay out.

Insurers investigate the “moment of damage” to find the trigger. A single hole in a wall might be a DIY error. Ten holes in a row suggest a deliberate attack. Grey areas often emerge during domestic disputes or when a tenant’s guest causes trouble. If a partner kicks a door in during an argument, most providers classify this as malicious, though they usually require a police crime reference number before proceeding with the claim.

Common Examples of Malicious Acts

Arson and Fire: Purposefully setting fire to curtains or floorboards.

Sanitary Ware Destruction: Smashing toilets, sinks, or baths with heavy tools.

Graffiti: Spray-painting walls or floors to ruin the aesthetic of the home.

Intentional Flooding: Blocking drains and leaving taps running to cause structural rot.

Cannabis farms represent a specific, high-risk sub-category of malicious damage. Criminal tenants often bypass electricity meters and install heavy ventilation, leading to scorched ceilings and severe mould. Revenge damage is another primary trigger for this cover. When a landlord serves an eviction notice, some tenants react by destroying the property out of spite before they leave. This is why specialized malicious damage by tenant insurance cover is a necessity rather than a luxury.

What Counts as Accidental Damage?

Accidental damage covers the “oops” moments of daily life. This includes spilling red wine on a new carpet, dropping a heavy cast-iron pan on a ceramic hob, or putting a foot through the ceiling while retrieving suitcases from the loft. These incidents lack the “intent to harm” that defines malicious acts.

Because the risks differ, premiums for these add-ons vary. Accidental damage is often cheaper because it’s more common and usually less expensive to fix than a gutted kitchen. A comprehensive residential letting insurance policy typically treats these as two distinct sections. Separating them allows you to choose the level of protection that fits your specific tenant demographic. If you want to ensure your investment stays profitable, it’s worth checking your policy documents today.

What Does Landlord Insurance for Malicious Damage Actually Cover?

Standard policies provide a vital safety net for deliberate acts of destruction. This isn’t about a spilled glass of wine on a carpet or a scuffed skirting board; it’s about smashed windows, kicked-in doors, or graffiti. A robust malicious damage by tenant insurance cover typically handles the financial burden of restoring your property to its original state after a tenant intentionally causes harm. It covers the cost of professional contractors and the materials needed for repairs.

Insurers set a limit of indemnity, which is the maximum amount they’ll pay for a claim. For residential units, this often starts at £500,000, though it can scale significantly for multi-property portfolios. If you manage 15 properties across Staffordshire, your policy should be structured to reflect the aggregate risk across the entire portfolio. This ensures that one major incident doesn’t exhaust your total coverage limits.

One of the most valuable components is the ‘Loss of Rent’ extension. If the damage is so severe that the property is uninhabitable, this extension triggers. It replaces the income you lose while the property is being repaired. For instance, if a house in Stoke-on-Trent requires eight weeks of structural work, the insurer covers the missing rental payments, keeping your mortgage commitments on track.

Buildings vs. Contents: Protecting Every Asset

Buildings cover protects the ‘shell’ of your investment. This includes the walls, floors, roofs, and fixed units like fitted kitchens or bathrooms. However, landlords with furnished lets must ensure their contents are specifically named in the malicious damage clause. Without this, you might find the walls are covered but the destroyed sofas and appliances are not. For those managing retail or office spaces in the West Midlands, a specialized commercial property insurance policy is often required to handle the higher reinstatement costs associated with business premises.

The Crucial Exclusions: What Insurers Won’t Pay For

Understanding what landlord insurance covers is as much about knowing the limitations as the benefits. Insurers won’t pay for ‘gradual damage’ or issues resulting from a lack of maintenance. If a tenant slowly ruins a property through neglect over several years, it’s rarely covered by a malicious damage claim. It has to be a specific, intentional act.

The ‘unoccupied property’ rule is another common pitfall. If your property sits empty for more than 30 consecutive days, many insurers suspend or limit your malicious damage by tenant insurance cover. You must notify your broker if a property is vacant for an extended period. Finally, damage caused by squatters or people ‘unlawfully on the premises’ often falls under standard vandalism. This is a separate category from damage caused by a person named on the tenancy agreement, often carrying different excess amounts.

How to Protect Your Property and Handle a Malicious Damage Claim

Securing the right malicious damage by tenant insurance cover is only half the battle. You also need to follow strict protocols to ensure your policy remains valid when you need it most. Most insurers view professional tenant referencing not just as a recommendation, but as a warranty. This means if you fail to conduct a comprehensive check, including credit history and previous landlord references, your claim could be rejected outright. These checks act as your first line of defence, filtering out high-risk applicants before they ever hold a key.

Risk Mitigation: Preventing Damage Before It Happens

Regular inspections are a non-negotiable requirement for most UK landlords. To satisfy the ‘reasonable care’ clause found in most policies, you should aim to inspect the property at least every six months. These visits allow you to spot early warning signs of neglect or unauthorised alterations before they escalate into a total loss. Documenting these visits provides a paper trail that proves you’ve been a responsible property owner.

While you’re focusing on property damage, don’t forget broader risks. Having public liability insurance protects you if a tenant or visitor is injured on your premises due to a maintenance failure. It provides a vital safety net for your wider portfolio and ensures you aren’t left vulnerable to personal injury claims.

The First 24 Hours: Emergency Response Checklist

If you discover your property has been trashed, your actions in the first 24 hours are critical for a successful claim. Follow these steps immediately:

Step 1: Contact the police. Malicious damage is a criminal act, not just a civil dispute. You must obtain a Crime Reference Number (CRN) immediately. Without this number, most insurers won’t even open a file for a malicious damage claim.

Step 2: Document the scene. Take high-resolution photos and video evidence of every room. Do this before any cleanup begins. Capture close-ups of specific damage and wide shots of the entire area.

Step 3: Notify Just Quote Me. Contact us to initiate the claim. We provide expert guidance on what temporary repairs you can make to secure the property without compromising the evidence needed by the insurer.

The Role of Evidence and the Loss Adjuster

Your ‘Inventory and Schedule of Condition’ is your most powerful piece of evidence. This document, signed by the tenant at the start of the tenancy, proves the property’s original state. When assessing a claim under your malicious damage by tenant insurance cover, an insurer will often appoint a loss adjuster. Their job is to determine if the damage was truly intentional or simply ‘fair wear and tear’.

Loss adjusters look for specific indicators of intent, such as holes kicked into internal walls, doors pulled off hinges, or paint poured onto carpets. Because they are impartial experts, having a detailed, dated inventory makes it much harder for an insurer to dispute the cause of the damage. We recommend keeping digital copies of all receipts and inventories to ensure they are accessible during the claims process.

Price comparison websites operate on rigid algorithms that often exclude complex risks. If you’re a landlord, you need more than a generic policy generated by a computer. Just Quote Me brings 30 years of experience across the Staffordshire and West Midlands insurance markets to help you secure the right protection. We understand that finding reliable malicious damage by tenant insurance cover is often difficult when your property houses high-risk occupants like students or DSS tenants. While automated sites might reject these applications or inflate premiums, an independent broker negotiates directly with underwriters to find a fair solution.

When a “tenant nightmare” happens, you don’t want to wait in a digital queue or talk to a chatbot. You need a real person who understands the local market and your specific situation. We provide a human-centric service that prioritizes your peace of mind during stressful claims. Our experts handle the heavy lifting, ensuring you aren’t left stranded when property damage occurs. We know the nuances of the local area, from Stone to Birmingham, giving us an edge over faceless national corporations.

Tailored Solutions for Every Property Type

We assist landlords with unique and complex portfolios. This includes specialized thatched pub insurance or mixed-use buildings that combine commercial units with residential flats. We conduct annual policy reviews to ensure your cover reflects current economic shifts. For instance, ensuring your limits meet projected 2026 rebuild costs is vital to prevent underinsurance. This proactive approach saves you significant time and money, especially during complex claims where every detail matters. A bespoke brokerage ensures your policy remains fit for purpose as the market evolves.

Get Your Quote: The No-Nonsense Approach

Securing malicious damage by tenant insurance cover shouldn’t be a box-ticking exercise. Our philosophy is built on being quick, transparent, and expert-led. We don’t believe in wasting your time with endless forms. Instead, we encourage landlords to consolidate their requirements. You might link your residential portfolio with shop insurance or other commercial policies to secure more competitive premiums. This streamlined method reduces your administrative burden and ensures there are no gaps in your protection. Contact our Stone-based team for a bespoke landlord insurance quote today.

Secure Your Rental Portfolio Against Intentional Risks

Protecting your investment requires more than just a standard policy. You need to know the clear difference between accidental mishaps and deliberate acts of destruction to ensure your property remains a viable asset. By securing comprehensive malicious damage by tenant insurance cover, you guarantee that intentional harm doesn’t result in a devastating financial blow. We’ve explored how proactive management and specific policy wording can save you thousands in repair costs while keeping your business running smoothly.

Our team offers 30+ years of independent brokerage experience. We are FCA-authorised experts who connect you with an extensive network of top UK underwriters to find the right fit for your specific needs. We don’t use faceless, automated algorithms. Instead, we provide personal, honest advice that addresses the unique challenges UK landlords face in 2026. We’re ready to help you navigate the insurance market with confidence and clarity so you can focus on your tenants.

Is malicious damage by tenants covered as standard in landlord insurance?

Malicious damage by tenants isn’t usually included as standard in a basic landlord buildings insurance policy. Most insurers treat it as an optional add-on that you must specifically request. Without this specific malicious damage by tenant insurance cover, you may find yourself liable for the full cost of repairs if a tenant intentionally harms your property. Always check your policy schedule for exclusions related to intentional acts by residents.

Do I need a police report to claim for malicious damage by my tenant?

You’ll almost certainly need a police crime reference number to process a claim for malicious damage. Since malicious damage is a criminal act under the Criminal Damage Act 1971, insurers require formal documentation to prove the damage was intentional rather than accidental. You should report the incident to the police immediately upon discovery. This official record acts as vital evidence for your insurance provider during the claims process.

Can I deduct malicious damage costs from the tenant’s deposit?

You can deduct the costs of repairing malicious damage from the security deposit, provided you have sufficient evidence. You’ll need a clear check-in inventory and a final check-out report to prove the damage occurred during the tenancy. If the repair costs exceed the deposit amount, which is capped at five weeks’ rent for most UK tenancies under the Tenant Fees Act 2019, you’ll need to claim through your insurance.

What is the difference between malicious damage and vandalism in insurance?

In insurance terms, malicious damage is caused by someone who has a legal right to be in the property, such as your tenant or their guests. Vandalism refers to damage caused by trespassers or burglars who have entered the property illegally. It’s a crucial distinction because many standard policies cover vandalism by intruders but require a specific extension for malicious damage by tenant insurance cover to protect against those you’ve let into the home.

Does insurance cover damage caused by a tenant’s sub-letter or guest?

Most comprehensive landlord policies extend malicious damage cover to include the tenant’s guests or invited visitors. However, if your tenant has sub-let the property without your permission, your insurance might be voided entirely. Standard UK tenancy agreements usually prohibit sub-letting for this reason. You should ensure your policy covers all lawful occupants to avoid gaps in protection when your tenant’s associates cause intentional harm to the structure or contents.

Will my insurance pay for loss of rent if the property is damaged maliciously?

Your insurance will typically pay for loss of rent if the malicious damage makes the property uninhabitable for future tenants. This is usually claimed under a Loss of Rent section of your policy rather than the buildings cover itself. If the damage requires major structural repairs that take weeks to complete, this cover ensures you don’t lose out on your monthly income while the property sits empty during the restoration process.

What happens if the damage is discovered after the tenant has already moved out?

You can still make a claim if you discover damage after the tenant leaves, but you must do so immediately. Most insurers set a strict time limit, often 30 days, for reporting incidents after a tenancy ends. Your check-out report, conducted within 24 to 48 hours of the keys being returned, serves as the primary evidence. If you wait too long to inspect the property, the insurer might argue the damage happened while the building was vacant.

Is damage caused by a cannabis farm considered malicious damage?

Damage from cannabis cultivation is generally classified as malicious damage, but it’s a high-risk area that many insurers treat separately. The 2023 UK crime data shows a rise in residential grow ops, which cause extensive water damage and electrical alterations. Because the costs often exceed £10,000 per incident, some policies have specific illegal cultivation of drugs clauses with unique limits or higher excesses. Check your policy wording to ensure this risk is covered.

Article by

Just Quote Me

JustQuoteMe Ltd is an independent UK insurance brokerage specialising in business and personal insurance solutions. With over 35 years of industry experience, the company provides tailored insurance cover for businesses, landlords, tradespeople, hospitality venues, fleets, and individuals across the UK. Known for its personal service, expert advice, and competitive premiums, JustQuoteMe Ltd works with leading insurers to deliver bespoke policies designed around each client’s unique needs. The company is authorised and regulated by the Financial Conduct Authority (FCA No. 586607) and has built a reputation for trusted, straightforward insurance guidance and long-term client relationships.

If a tenant trips on a loose carpet tile this afternoon, would your current buildings policy stop a £50,000 legal claim from reaching your personal savings? Many UK property owners mistakenly believe their standard cover is enough, yet 2026 regulations have made health and safety obligations stricter than ever. It’s a genuine worry to feel that one minor maintenance oversight could lead to a lengthy court case, which is why understanding landlord liability insurance for tenant injury is now a critical part of your risk management strategy.

We understand that you want to manage your properties with confidence rather than the constant fear of litigation. You deserve a policy that acts as a robust safeguard for your livelihood. We’ll show you exactly how to protect your assets and your reputation by securing cover that includes both expert legal defence and compensation awards. This guide breaks down your specific legal obligations for 2026 and provides practical, no-nonsense steps to reduce the likelihood of a claim before it ever reaches a solicitor’s desk.

Key Takeaways

Learn how to safeguard your assets and reputation by understanding exactly what landlord liability insurance for tenant injury covers, from legal fees to compensation.

Navigate your specific legal obligations under the Occupiers Liability Act and understand how UK courts define negligence in 2026.

Evaluate your current coverage to see why a £5 million indemnity limit is becoming the essential benchmark for UK residential property owners.

Master proactive “Defence of Care” strategies and inspection routines to identify hazards before they lead to costly litigation.

Discover the benefits of using a specialist broker to access tailored underwriting and human expertise that automated comparison sites often miss.

What is Landlord Liability Insurance for Tenant Injury?

Landlord liability insurance for tenant injury is a specialized form of protection designed specifically for property owners. It doesn’t just cover the building; it protects the person or business behind the property. This coverage is essential because UK law, specifically the Occupiers’ Liability Act 1957 and 1984, places a strict duty of care on landlords to ensure their premises are safe for anyone entering them. To understand the broader context of these policies, you can read more about What is Landlord Liability Insurance? on Wikipedia.

The core purpose of this insurance is to cover legal costs and compensation if a tenant or visitor is injured due to your negligence. Negligence might include failing to fix a broken floorboard, ignoring a damp issue that leads to respiratory illness, or leaving a faulty electrical circuit unrepaired. In the UK market, indemnity limits usually start at £2 million, but many professional landlords opt for £5 million or £10 million to account for the rising costs of medical care and legal fees. If a court awards a claimant £3 million and your limit is only £2 million, you’re responsible for the remaining £1 million yourself.

Property Owners Liability vs. Public Liability

You’ll often hear these terms used interchangeably in the rental sector. While they’re similar, the distinction lies in the “trigger” for a claim. Standard public liability insurance often focuses on active business operations. Property Owners Liability triggers based on “ownership-based negligence.” It focuses on the physical state of the property rather than your daily activities. This policy protects you against claims from a wide range of people, including the tenants named on the lease, their guests, visiting tradesmen, and even trespassers who might be injured by a structural hazard.

Why Buildings Insurance Alone is a Dangerous Risk

Many landlords fall into the “Total Loss” fallacy. They think that because they’ve secured residential letting insurance to cover the bricks and mortar against fire or flood, they’re fully protected. This is a dangerous assumption. Standard buildings insurance focuses on the asset, not the legal liabilities attached to it. Most basic policies specifically exclude third-party bodily injury claims unless a liability add-on is present.

If a tenant trips on a frayed carpet and suffers a life-changing spinal injury, your buildings insurance won’t pay the legal fees to defend you or the settlement to support the victim. Property Owners Liability is the financial shield for your personal or business assets. Without it, a single lawsuit could force the sale of your entire portfolio to cover the debt.

Covers legal defense costs regardless of the claim’s outcome.

Pays out for medical expenses and loss of earnings for the injured party.

Fulfills requirements often set by mortgage lenders and local authorities.

Securing the right landlord liability insurance for tenant injury ensures that a physical defect in your property doesn’t lead to a total financial collapse. It’s a straightforward way to manage the inherent risks of being a property owner in a litigious environment.

While this insurance covers your professional risks, personal financial planning is just as critical for long-term stability. For those interested in securing their family’s future against end-of-life expenses, The Paul Group offers specialized final expense life insurance for seniors.

The Legal Reality: Duty of Care and Negligence in 2026

The legal landscape for UK property owners has shifted significantly. Under the Occupiers Liability Act 1957, you have a statutory “common duty of care” to ensure your tenants are reasonably safe while using your property. Negligence occurs when you breach this duty. In court, a judge looks for three things: a duty of care existed, that duty was breached, and the breach directly caused the injury. If a tenant slips on a leaking pipe you failed to fix, the liability sits squarely on your shoulders.

The rise of “No Win, No Fee” legal services has made it easier for tenants to pursue claims for even minor slips or trips. While UK law is your primary concern, the principles of liability are becoming more stringent worldwide. This aligns with UK legal principles, where any contractual clauses seeking to absolve landlords of their statutory duty of care or liability for negligence are typically deemed void, underscoring your non-negotiable responsibilities. In Britain, the Homes (Fitness for Human Habitation) Act 2018 empowers tenants to take direct legal action if a property is unsafe, making landlord liability insurance for tenant injury a vital safeguard.

Understanding Your Statutory Obligations

Safety compliance isn’t just about avoiding local council fines. It’s your primary shield against injury claims. If a tenant is injured by a faulty boiler and you don’t have a valid Gas Safety Record, proving you weren’t negligent is almost impossible. You’re also responsible for common areas like hallways and stairwells in HMOs or multi-unit blocks. A digital paper trail of every repair and inspection is your first line of defence. For those managing multiple properties, securing residential letting insurance provides a safety net when paperwork alone isn’t enough.

The Burden of Proof in Tenant Injury Claims

Tenants must prove you were aware of a hazard, or should’ve been aware of it through regular inspections. You aren’t expected to be perfect, but you must be proactive. The courts use the “reasonable care” standard. If a tenant reports a loose floorboard and you ignore it for 14 days, you’ve likely failed that test.

Consider a 2022 case where a tenant tripped on a loose stair carpet. The landlord had been notified via email two weeks prior but hadn’t sent a contractor. The resulting fall led to a fractured ankle and a £50,000 compensation payout. This demonstrates why landlord liability insurance for tenant injury is a non-negotiable part of modern property management. It covers the legal fees and the settlement costs that could otherwise bankrupt an individual landlord. If you’re concerned about your current level of protection, you can Just Quote Me to find a policy that fits your specific needs.

Evaluating Your Coverage: How Much Protection is Enough?

Deciding on an indemnity limit isn’t a guessing game; it’s a calculation based on your specific risk profile. Several factors influence how much protection you need. The size of your property portfolio, the location of your units, and the demographic of your tenants all play a role. For example, a large multi-unit block in a high-traffic urban area carries a higher statistical risk of accidents than a single-family home in a rural setting. By 2026, a £5 million indemnity limit is expected to become the industry standard for UK residential landlords. This shift is driven by the rising costs of long-term care settlements and private medical treatments that courts now frequently award.

One of the most overlooked aspects of a claim is the cost of legal fees. Even if a claim for a minor trip is settled for £15,000, the associated legal defence costs, expert witness fees, and court charges can easily exceed £50,000. If you’re relying on a generic, off-the-shelf policy, you might find these costs are capped or restricted. Choosing a bespoke policy through a specialist broker ensures that your landlord liability insurance for tenant injury is robust enough to cover both the compensation and the professional fees required to defend your reputation.

Residential vs. Commercial Liability Needs

Commercial properties involve a higher level of complexity due to increased footfall. If you own a building with a ground-floor retail unit, your risk profile changes the moment a member of the public enters the premises. For mixed-use properties, it’s often necessary to integrate shop insurance to ensure every square inch of the building is protected. The nature of the business tenant is vital. A quiet accounting office presents a much lower risk than a fast-paced restaurant with wet floors and hot surfaces.

What is Typically Excluded?

Understanding what your policy won’t cover is just as important as knowing what it will. Most landlord liability insurance for tenant injury policies exclude intentional acts or “deliberate neglect.” If you’re aware of a broken floorboard and choose not to fix it for six months, an insurer may refuse to pay out. Additionally, liability for your staff is a separate matter. If you employ a property manager or a cleaner, you’re legally required to hold Employers Liability Insurance. Finally, if you provide professional consultancy or advice as part of your service, you’ll need Professional Indemnity Insurance to cover errors in judgment or advice.

Getting your coverage levels right from the start saves you from financial ruin later. It’s about finding that balance between a premium that fits your budget and a limit that actually protects your assets when things go wrong.

Proactive Risk Management: Preventing Injuries and Claims

Preventing a claim is always better than filing one. While landlord liability insurance for tenant injury provides a vital financial safety net, your primary goal is to maintain a safe environment. You build a “Defence of Care” by proving you took every reasonable step to prevent harm. This doesn’t just mean fixing things when they break; it requires active, documented oversight.

Mid-term inspections are your best tool here. Property managers who conduct quarterly walkthroughs identify 40% more potential hazards than those who only visit at renewal, according to 2023 industry data. These visits let you spot a loose floorboard or a flickering stairwell light before they cause a fall. If a claim does arise, having a record of these regular checks demonstrates that you’re a responsible, proactive landlord.