The lowest quote on a comparison site feels like a win until a £5 million claim arrives and you discover a hidden exclusion. It’s a common worry for UK business owners in 2026, especially as you try to balance rising operational costs with the need for robust protection. You want cheap public liability insurance, but you don’t want to gamble with your livelihood. We understand that the average small business premium now sits between £115 and £155 per year. While the market is currently softening, securing a deal that satisfies both your budget and your clients requires a tactical approach.

This article explains how to drive down your insurance costs without stripping away essential cover. We will explore how to leverage current market trends and avoid the jargon that leads to rejected claims. You will learn how to secure a policy that offers genuine peace of mind at a price that makes sense for your bottom line.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Key Takeaways

- Learn why public liability is a vital commercial requirement for securing contracts, even when it isn’t legally mandated.

- Understand how your specific trade and annual turnover levels directly dictate the premium you pay.

- Discover how to secure cheap public liability insurance by bundling policies and demonstrating proactive risk management to insurers.

- Identify the hidden traps in budget policies, such as high excesses, that can leave your business financially exposed during a claim.

- Find out why using an independent broker provides access to exclusive markets and tailored cover that comparison sites often miss.

What is Public Liability Insurance and Why is Cost Rising?

Public liability insurance serves as a financial safety net for your business. It steps in if a client, delivery driver, or passerby suffers an injury or property damage due to your business activities. While it’s not a legal requirement in the UK, most clients will refuse to let you on-site without a valid certificate. To get a better grasp of the legalities, you can read about what is public liability and how it relates to civil law. In 2026, the search for cheap public liability insurance has intensified as businesses face a complex economic environment.

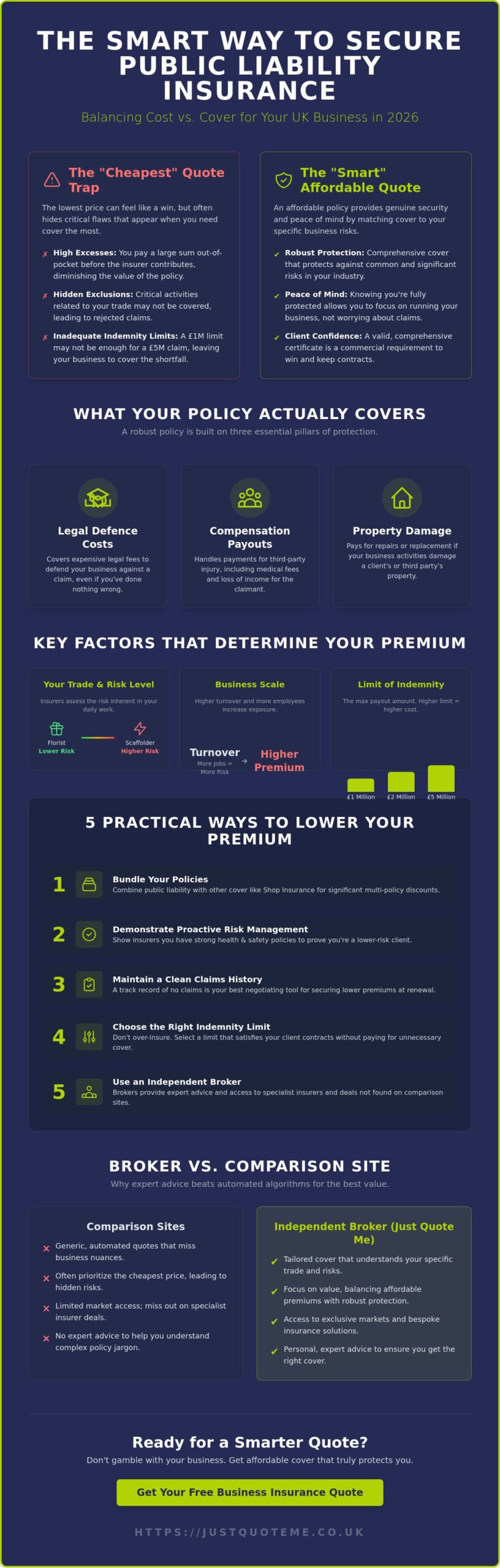

The cost of cover is shifting. While some sectors saw premium reductions of 11% to 20% at the end of 2025, other areas are under pressure. Rising costs for building materials and specialist labour mean that property damage claims are more expensive to settle than they were two years ago. When repair costs go up, insurers eventually pass those expenses on to the policyholder. This makes it crucial to distinguish between a “cheap” policy that cuts corners and an “affordable” policy that provides genuine security.

The Core Components of a Public Liability Policy

A robust policy is built on three pillars. First, it covers legal defence costs. Even if you’ve done nothing wrong, defending a claim in court is expensive. Second, it handles compensation payouts, which include medical fees and loss of income for the claimant. Finally, it covers property damage. Whether you’re a cleaner who accidentally ruins a carpet or a builder involved in a major structural mishap, these costs can easily reach six figures without insurance.

Why Businesses are Desperate for Lower Premiums in 2026

Small business overheads are under more scrutiny than ever. With the UK insurance market projected to reach $836.5 billion by 2033, the industry is growing, but so are the risks. AI integration and cyber threats are adding new layers of complexity to standard business operations. Many owners look for cheap public liability insurance to keep their margins healthy. Just Quote Me helps by cutting through the noise of automated algorithms. We find bespoke solutions that fit your specific trade, ensuring you don’t pay for cover you don’t need. You can find more details on our public liability insurance service page.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Factors That Determine the Price of Your Insurance Quote

Insurers don’t pick numbers out of a hat. They use complex actuarial data to decide your premium, and your trade is often the most significant factor. A florist working in a controlled environment faces far lower risks than a scaffolder working at height. If your work involves dangerous equipment, heat, or high altitudes, the insurer expects a higher likelihood of a significant claim. This is where finding cheap public liability insurance becomes a balancing act between the lowest price and the specialist expertise required for your specific industry.

Your business scale also dictates the cost. A firm with a £50,000 turnover has fewer interactions with the public than one turning over £5 million. More jobs mean more opportunities for an accident to occur. Similarly, your employee count changes the risk profile. While you might be looking for a basic policy, having more staff often correlates with a higher volume of work and increased public liability exposure. A clean claims history is your best tool for negotiation. If you’ve operated for five years without a single incident, you’re in a much stronger position to secure a discount. This track record highlights the role of liability insurance in your broader asset protection strategy. It isn’t just an overhead; it’s a shield for your business capital.

Location and Territorial Limits

Where you work changes what you pay. Rates in London are often higher due to increased legal costs and higher settlement values. However, if you’re based in the West Midlands or Staffordshire, you might find more competitive local rates. Working on-site at various locations is generally riskier than working from a fixed base. For those with a permanent physical presence, dedicated Shop Insurance often provides a more cost-effective way to bundle public liability with other essential covers. You should speak with a broker to ensure your territorial limits actually cover where you work.

The Limit of Indemnity: £1m, £2m, or £5m?

The limit of indemnity is the maximum amount the insurer will pay for a single claim. While a £1 million limit might seem like enough, it’s often the bare minimum. Most public sector contracts and local authority projects require a minimum of £5 million in cover. Choosing a lower limit might help you find cheap public liability insurance today, but it could cost you a lucrative contract tomorrow. We often find that the price difference between £2 million and £5 million of cover is surprisingly small, making the higher limit a better long-term value.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

The Hidden Risks of Choosing the Cheapest Policy

“I just need the certificate to get on-site.” It’s a phrase we hear often from contractors looking for cheap public liability insurance. While getting the paperwork sorted is necessary for access, viewing insurance as a mere box-ticking exercise is a dangerous gamble. If a policy is priced significantly below the market average of £115 to £155, the insurer has likely stripped away essential protections or inflated the excess to an unmanageable level. You might save a few pounds today, but the long term cost of an inadequate policy can be devastating.

A high policy excess is one of the most common traps. You might save £20 on your annual premium, but if the policy carries a £500 or £1,000 excess, you’ll be paying out of pocket for minor accidents that a better policy would have covered in full. When you consider the factors that determine insurance price, remember that the lowest upfront cost often hides the highest eventual liability. There’s also the risk of “unrated” insurers. These companies aren’t backed by the same financial guarantees as established UK providers, meaning they could potentially fold before your claim is settled, leaving you to face the legal costs alone.

Common Exclusions in Budget Public Liability Policies

Budget policies are often riddled with narrow definitions that leave builders or tradesmen vulnerable. For example, many low-cost options include strict height and depth restrictions. If your policy limits work to 2 metres and you’re working on a 3-metre scaffold, your cover is effectively void. Similarly, the use of heat is a major sticking point. “Cheap” policies frequently exclude welding, soldering, or blowtorch work unless you pay an additional premium. For comprehensive protection that covers the full scope of a project, a Contractors All Risk Insurance policy might be a more appropriate investment than a basic liability certificate.

Cheap vs. Comprehensive: A Comparison

Imagine a “bare bones” policy costing £10 per month versus a bespoke policy at £15 per month. That extra £5 usually buys you lower excesses, higher indemnity limits, and fewer exclusions. For consultants or service-based firms, it also provides the opportunity to bundle essential add-ons. Combining your liability with Professional Indemnity Insurance ensures that both physical accidents and professional errors are covered. If your business sells or distributes physical goods, it’s equally important to understand where your public liability ends and your product liability insurance begins, as budget policies rarely make this distinction clear. Investing in cheap public liability insurance is only a success if the policy actually pays out when you need it most.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

5 Practical Ways to Secure Cheap Public Liability Insurance

Securing a competitive rate doesn’t mean you have to settle for inferior cover. By taking a proactive approach to how you present your business to underwriters, you can unlock discounts that automated systems often overlook. There’s power in being a well-prepared applicant. Here are five practical methods to reduce your premiums while maintaining the high level of protection your business deserves.

- Optimise your trade description: Be specific about what you do. If you’re listed as a general contractor but only perform domestic decorating, you’re likely paying a premium for risks you don’t actually face.

- Bundle your insurance: Combining different types of cover is one of the most effective ways to find cheap public liability insurance. For instance, if you have any staff, you’re legally required to have employers liability insurance. Purchasing these together usually results in a lower total cost than buying them separately.

- Pay the full amount annually: Monthly direct debits often come with interest rates that can add 10% to 15% to your total bill. Paying upfront eliminates these finance charges and simplifies your accounting.

- Demonstrate risk management: Show the insurer you’re a safe bet through documented procedures and safety accreditations.

- Adjust your voluntary excess: Taking on a slightly higher portion of the initial claim cost can significantly lower your ongoing premium.

Risk Assessments and Safety Accreditations

Insurers look for evidence that you take safety seriously. Memberships in trade bodies or holding safety accreditations signal to an underwriter that you’re a low-risk prospect. A risk assessment is a proactive tool that proves business competence to an insurer. By keeping these documents updated and available, you’re in a much better position to negotiate. If you haven’t reviewed your safety protocols lately, you should get a specialist quote to see how your improved standards affect your rate.

Adjusting Your Voluntary Excess

The relationship between your excess and your premium is a simple mathematical trade-off. By increasing your voluntary excess from £250 to £500, you reduce the insurer’s potential payout on small claims, which they reward with a lower premium. However, you must find a “sweet spot” where the savings are meaningful but the excess remains affordable if you need to claim. This is particularly relevant in high-risk sectors; for example, firms seeking Security Insurance often use higher excesses to manage the costs of specialized liability cover. Always ensure you have the funds set aside to cover the excess at a moment’s notice.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Why an Independent Broker Beats a Comparison Site for Price

Comparison sites offer speed, but they often sacrifice the depth required for complex business risks. While they might show a low price, they rarely provide the context needed to ensure your cover is actually valid. Just Quote Me has spent over 30 years building a reputation with a panel of top-tier UK insurers. This longevity gives us access to “Broker-Only” markets. These are specialist insurers who avoid comparison platforms to focus on businesses that require a more considered approach. By tapping into these exclusive markets, we often secure cheap public liability insurance that isn’t available to the general public.

Bespoke policy tailoring is where a human advisor truly adds value. Instead of a generic package that might include irrelevant add-ons, we strip away the excess. You only pay for the specific protection your business requires. Whether you’re a tradesman or a professional consultant, we ensure your policy reflects your actual turnover and activities. Having a broker on your side during a claim also provides a level of advocacy that a faceless call centre cannot match. We act as your voice, dealing with the insurer so you don’t have to navigate the stress of a claim alone.

Faceless Algorithms vs. Expert Advice

Automated systems are binary; they often flag businesses as “high risk” based on a single keyword or postcode. This can lead to inflated premiums or outright rejections for perfectly safe operations. As a local specialist in Staffordshire and the West Midlands, we understand the local business landscape. We can speak directly to underwriters to explain your safety protocols and specific risk profile. This human intervention often results in a fairer price and more robust cover than any algorithm can provide.

Ready to Lower Your Business Insurance Costs?

The transition from searching for “cheap” insurance to finding “smart” insurance is about value. It’s about knowing your business is safe without overpaying for the privilege. We’ve helped thousands of UK businesses navigate the complexities of the 2026 market with honesty and efficiency. By choosing a partner who understands your trade, you gain both competitive rates and the peace of mind that your policy will perform when you need it most.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Secure Your Business Future Today

Securing cheap public liability insurance doesn’t have to be a race to the bottom that leaves your assets exposed. By focusing on proactive risk management and choosing the right indemnity limits for your specific trade, you can protect your livelihood without overspending. We’ve explored how avoiding the hidden traps of budget policies and opting for bespoke tailoring ensures that your cover remains valid when it matters most. As an FCA-authorised independent broker with over 30 years of UK industry experience, Just Quote Me provides the specialist knowledge that automated algorithms lack. We leverage our access to a top-tier panel of UK insurers to find competitive rates that generic sites often miss.

Don’t leave your business protection to chance. Whether you need to meet a £5 million contract requirement or simply want a more efficient way to manage your overheads, we’re here to help. You can start your journey to better cover by speaking with our team today. We look forward to helping your business thrive with the right protection in place.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Frequently Asked Questions

Is the cheapest public liability insurance always the best option?

No, the lowest price rarely guarantees the best protection. While you might save money on your monthly premium, budget policies often feature high excesses of £500 or more and narrow exclusions that could leave you footing the bill for a claim. It’s vital to ensure the policy actually covers your specific trade activities before committing to the cost.

How can I get cheap public liability insurance as a sole trader?

The most effective way for a sole trader to secure cheap public liability insurance is to pay your premium annually and provide a precise trade description. Avoiding monthly interest charges and ensuring you aren’t rated for high-risk activities you don’t perform can lead to significant savings. Bundling your liability with other covers, such as tools or professional indemnity, also typically reduces the total cost.

Will my premium go down if I have a health and safety policy?

Yes, insurers often view businesses with documented health and safety policies as lower-risk prospects. By proving you have proactive risk management in place, you give underwriters the confidence to offer more competitive rates. Documented risk assessments and safety accreditations serve as tangible proof of your business competence and can lead to lower annual premiums.

Can I change my public liability cover mid-year to save money?

You can switch providers at any time, but you should check for cancellation fees in your current contract first. If you find a significantly better rate elsewhere, the savings might outweigh the exit costs. However, it’s usually most efficient to review your options 30 days before your renewal date to avoid administrative penalties and gaps in cover.

What is the average cost of public liability insurance in the UK for 2026?

As of March 23, 2026, the average annual cost for small businesses in the UK typically falls between £115 and £155. While some low-risk businesses can find cover from around £50 per year, high-risk trades or those with large turnovers may pay £500 or more. Your specific premium depends on your claims history and the level of indemnity you choose.

Does “cheap” insurance cover me for working on larger construction sites?

Budget policies often include restrictive clauses that prevent work on major construction sites or at specific heights. Many low-cost certificates are designed for domestic work and exclude high-risk environments. You must verify that your policy meets the specific contractual requirements of the site manager, which often include a minimum of £5 million in cover.

Why is my public liability quote so high compared to last year?

Rising labour and material costs have increased the average value of property damage claims throughout 2025 and into 2026. If your business turnover has increased or you’ve moved into a higher-risk postcode, insurers will adjust your premium accordingly. Even without a claim, industry-wide inflation means insurers must increase rates to remain solvent and meet FCA requirements.

How does an independent broker find cheaper rates than a comparison site?

Brokers have access to specialist “broker-only” markets that are not available on public comparison tools. Instead of relying on a generic algorithm, a broker manually negotiates with underwriters to find cheap public liability insurance that is tailored to your specific risks. This personal touch ensures you don’t pay for unnecessary add-ons that automated systems often include by default.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.