What if a single structural change to your rental property could instantly invalidate your entire insurance policy? Many owners are surprised to find that their standard cover often fails the moment a project exceeds basic cosmetic work. If you are searching for landlord insurance for property undergoing renovation, you likely already feel the pressure of the 30-day unoccupancy limit. It’s a common anxiety, especially since 43% of landlords reported a void period in early 2026. You deserve to know that your capital is safe while the builders are on-site.

This guide will show you how to protect your investment and avoid policy voids while your rental property is being renovated. We’ll explain the vital distinctions between structural and cosmetic definitions and how to maintain liability cover for both workers and the public. You will also learn how to transition smoothly back to standard let property cover once the keys are handed back. Getting the right protection shouldn’t be a complex administrative burden; Just Quote Me for a pragmatic solution that keeps your project moving forward.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Key Takeaways

- Understand why standard policies often fail during building works and how to avoid the “unoccupied” clause trap.

- Discover what specialist renovation insurance covers, including protection for the existing structure and materials stored on-site.

- Learn how to distinguish between cosmetic and structural refurbishments when arranging landlord insurance for property undergoing renovation.

- Get a practical pre-renovation checklist to ensure your contractors are properly insured and your mortgage lender is informed.

- Find out how to access a broad network of UK insurers to secure bespoke protection that standard high-street policies can’t offer.

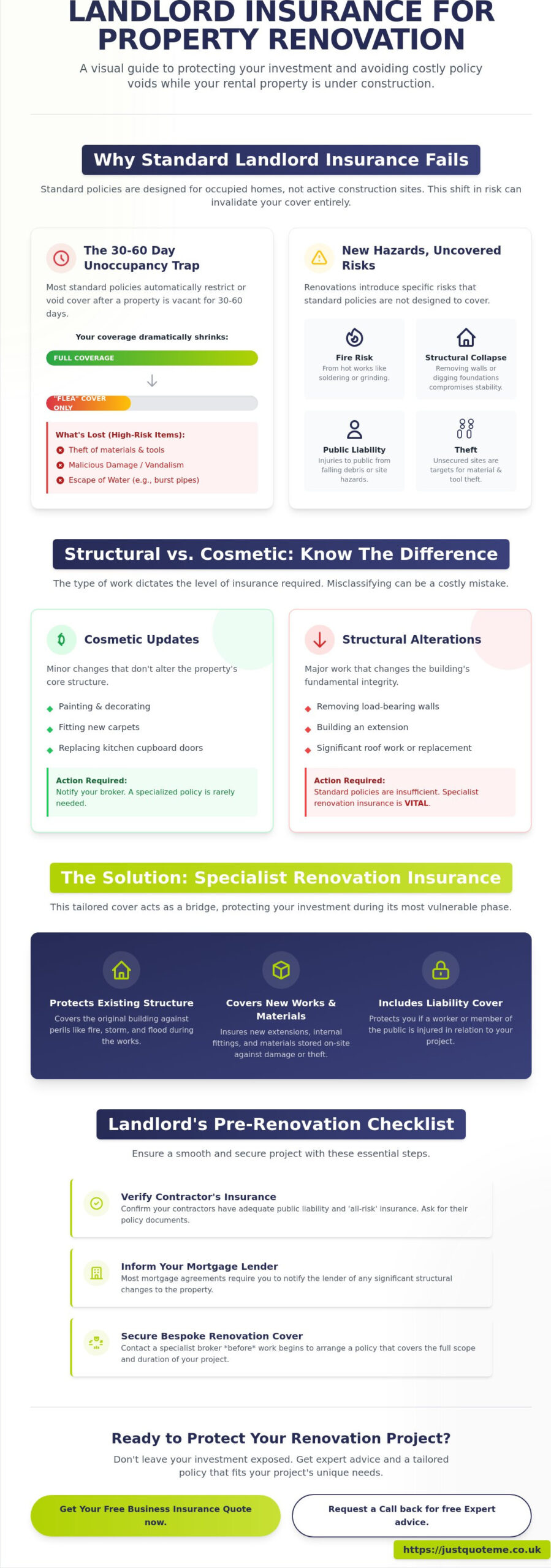

Why Standard Landlord Insurance Fails During Property Renovations

Standard landlord insurance serves a specific purpose: protecting a property that’s occupied and maintained by a tenant. Once you introduce builders, scaffolding, and vacant rooms, the risk profile shifts entirely. Most standard policies aren’t built to handle construction sites. Insurers price their risk based on the property being a home, not a workplace. Failing to update your policy to landlord insurance for property undergoing renovation leaves you exposed to a total policy void if you need to make a claim. Understanding Property Insurance Basics is helpful here; it shows that insurance is a contract based on the disclosure of all material facts. A renovation is a significant material change that your insurer must know about. Specialized landlord insurance for property undergoing renovation ensures that your investment remains protected during these high-risk periods.

The 30-60 Day Unoccupancy Trap

Insurers view a property without a permanent resident as a high-risk asset. Most standard landlord policies include a clause that limits coverage if the property is vacant for more than 30 or 60 consecutive days. Once this threshold is crossed, many insurers strip your protection back to “FLEA” cover only. This covers Fire, Lightning, Explosion, and Aircraft. While these are serious events, this limited cover removes protection for the most common renovation risks. You lose cover for theft, malicious damage, and escape of water from burst pipes. In a renovation setting, these are the very incidents most likely to occur.

Structural Alterations vs. General Maintenance

It’s vital to distinguish between cosmetic updates and structural changes. Cosmetic work like painting, fitting new carpets, or replacing kitchen cupboard doors typically falls under general maintenance. You should still notify your broker, but these rarely require a specialized policy shift. Structural work is different. If you’re removing load-bearing walls, adding an extension, or performing roof work, you’re changing the integrity of the building. Standard residential letting insurance is usually insufficient for these projects. Without the correct disclosure, your insurer can argue that the risk has changed so much that the original policy is no longer valid.

Renovations introduce specific hazards that standard policies often ignore:

- Fire risk: Hot works like soldering or grinding significantly increase the chance of accidental fires.

- Structural collapse: Removing walls or digging foundations can compromise the entire building’s stability.

- Theft: Unsecured sites are prime targets for the theft of expensive building materials and tools.

- Liability: You may be held responsible if a member of the public is injured by falling debris or site hazards.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Specialist Cover: What Renovation Insurance Includes in 2026

Specialist renovation insurance acts as a tactical bridge between standard property protection and a full construction policy. While Standard Insurance Coverage typically focuses on the risks associated with a finished, occupied home, renovation cover accounts for the unique hazards of an active site. It provides a flexible framework that adapts as your project evolves from a stripped-back shell to a completed rental unit. Obtaining landlord insurance for property undergoing renovation ensures that your capital isn’t left exposed during the most vulnerable stage of your investment’s lifecycle.

Protecting the Existing Structure and New Works

One of the most significant gaps in standard policies is the failure to distinguish between the “shell” of the building and the “works in progress.” Specialist cover protects the original structure against traditional perils like fire and storm while simultaneously covering the new extensions, materials, and internal fittings. This is where contractors all risk insurance becomes essential. It covers the cost of repairing or replacing work that’s damaged before completion, such as a newly installed roof destroyed by a gale or copper piping stolen before the property is secured.

Correct valuation is critical in 2026. With high inflation affecting construction materials and labor, you must insure the property for its rebuild cost rather than its market value. Your policy should reflect the total value of the existing building plus the total contract value of the renovations. Securing comprehensive development cover ensures that if a total loss occurs mid-build, you have sufficient funds to clear the site and start again.

Liability Risks During the Renovation Phase

Even if your property is empty, your legal responsibilities don’t disappear. In fact, they often increase. Public liability insurance is a core component of renovation cover, protecting you against claims from third parties. This includes neighbors whose property might be damaged by your contractors or even trespassers who injure themselves on your site. Once a renovation begins, the property effectively becomes a construction site, shifting the liability from standard domestic risks to those associated with active building hazards.

Consider these key inclusions for a 2026 specialist policy:

- Materials on-site: Protection for expensive items like boilers, kitchens, and timber before they’re fitted.

- Unfixed materials off-site: Cover for items stored in a garage or warehouse prior to installation.

- Environmental standards: Support for meeting new 2026 EPC and environmental compliance during the rebuild.

- Alternative accommodation: Liability protection if a structural failure impacts a neighboring property’s habitability.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Navigating Structural vs. Cosmetic Refurbishments

Choosing the right landlord insurance for property undergoing renovation depends heavily on the scope of work you intend to carry out. Insurers generally categorize projects into two brackets: cosmetic and structural. Minor refurbishments, such as installing a new bathroom suite, replacing kitchen cabinets, or refreshing the internal décor, are often seen as low-risk. In many cases, these only require a simple policy note to your existing provider. However, the moment you move a load-bearing wall or alter the roofline, you have crossed a threshold into major works. These projects require a dedicated policy shift to reflect the increased risk of building failure or prolonged exposure to the elements.

The duration of the project also dictates your cover options. A two-week kitchen refit carries a different risk profile than a six-month basement excavation. For longer projects, you may need specialist renovation insurance that accounts for building code compliance and the potential for phased handovers. If your renovation is part of a wider development, you must also ensure that your Planning Permission and Building Regulations approval are in place, as many insurers will void a claim if the work is found to be unauthorized.

When a Minor Refit Becomes a Major Risk

The tipping point between “light” and “heavy” refurbishment often occurs when the property is no longer watertight. If you’re “opening up” the building by removing windows or sections of the roof, standard cover is no longer sufficient. Light refurbishment policies offer a cost-effective middle ground for landlords who are doing more than just painting but aren’t yet into major structural territory. To stay protected, follow this simple assessment checklist:

- Are you altering the external footprint of the building?

- Will the property be unsecured or open to the weather at any point?

- Are you hiring subcontractors who require their own liability oversight?

- Does the project value exceed 20% of the property’s total rebuild cost?

Specialist Protection for Complex Projects

For large-scale works, you must look beyond standard letting policies. Many UK renovations involve Joint Contracts Tribunal (JCT) agreements, which dictate specific insurance requirements for both the employer and the contractor. In these instances, securing professional builders insurance is often a contractual necessity. This ensures that the liability is clearly defined between your own interests and those of the construction firm.

Phased renovations present a unique challenge. If you’re renovating one flat in a block while others remain tenanted, you need a policy that balances contractors all risk insurance with active landlord liability. This prevents gaps in cover that could arise if a renovation accident in an empty unit causes damage to a tenanted one. Managing these complexities is where a specialist broker adds the most value, ensuring your landlord insurance for property undergoing renovation is fit for purpose throughout every phase of the build.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Managing Your Risks: A Landlord’s Pre-Renovation Checklist

Securing the right landlord insurance for property undergoing renovation is only the first step in protecting your capital. You must also implement a rigorous risk management strategy to ensure your cover remains valid throughout the build. Before any demolition begins, notify your mortgage lender. Most UK lenders require formal notification of major works, and failure to inform them can lead to a technical breach of your mortgage deed. You should also document the property’s current state. Take high-resolution photographs of every room, external wall, and the roof. These images serve as vital evidence if a dispute arises regarding whether damage was pre-existing or caused by the renovation process.

Schedule regular site visits, at least once a week, to ensure the property remains safe and secure. Insurers often require these inspections as a condition of your cover. During these visits, check that the site is tidy, waste is being managed, and no flammable materials are left near heat sources. In 2026, insurers are placing greater emphasis on legal compliance; ensure you have up-to-date fire safety protocols and that all gas and electrical certificates are maintained where applicable. This proactive approach not only protects the building but also demonstrates to your provider that you are a responsible risk, which can help when you seek competitive insurance rates for future projects.

Vetting Your Contractors and Their Cover

Never assume your builder’s insurance is sufficient to protect your interests. You must verify their public liability and employers liability certificates before they set foot on-site. Specifically, check the limit of indemnity; a £2 million limit may seem high, but it can be quickly exhausted in a major structural claim. If they are using subcontractors, you must ensure that tradesman insurance is active for every individual firm involved. Relying solely on a contractor’s policy is a dangerous gamble; if their policy lapses or they breach a condition, you could be left with no recourse for damage they cause to your property.

Securing the Site to Reduce Premiums

A secure site is a cheaper site to insure. Implement visible security measures like heavy-duty perimeter fencing and smart, battery-operated site alarms that alert your phone to unauthorized entry. For plumbing works, ensure your policy includes “Trace and Access” cover. This is essential for locating the source of a leak behind walls or under floors without you bearing the full cost of the destructive search. High-quality site management and clear fire safety protocols, such as “hot works” permits for any welding or soldering, significantly reduce the likelihood of a catastrophic claim. By treating the renovation as a professional workplace rather than a DIY project, you maintain the integrity of your landlord insurance for property undergoing renovation. To better understand the technical and compliance standards required for such professional sites, you can visit The Testing Lab PLC.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Securing Bespoke Protection with Just Quote Me

Just Quote Me brings over 30 years of experience to the UK property and construction insurance market. We understand that a renovation project isn’t just a building site; it’s a significant financial commitment that requires a specialized safety net. Finding the right landlord insurance for property undergoing renovation shouldn’t feel like an administrative burden. We provide access to a broad network of top UK insurers, many of whom don’t offer their specialized products through standard high-street brokers or automated platforms. Our role is to bridge the gap between standard landlord insurance and the specific, high-risk requirements of a property under development.

Why a Broker Beats an Online Comparison Site

Algorithms often struggle with the nuances of structural works. Online comparison sites are designed for standard risks; they rarely account for the complexities of a basement conversion or a phased roof replacement. We offer professional risk assessment consultations that look at your unique property and project timeline. Our regional expertise in Staffordshire and the West Midlands allows us to understand the specific nuances of local property stock, from Victorian terraces to modern apartment blocks. Once your project reaches completion and the building inspector provides the final sign-off, we manage the seamless transition back to standard residential letting insurance, ensuring you’re never left with a gap in cover.

Finalizing Your Cover and Starting Your Project

The process of getting a bespoke quote through Just Quote Me is designed to be efficient and straightforward. We don’t just set your policy and walk away. We understand that construction projects rarely go exactly to plan. If your project timeline changes or you decide to increase the scope of the works mid-build, we handle the mid-term adjustments on your behalf. This human-centric approach removes the stress of dealing with call centers and automated systems. We act as your steady hand in a complex market, managing the administrative weight so you can focus on the successful delivery of your build.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Secure Your Property Project Today

Navigating the transition from a rental home to a construction site requires more than just a standard policy. You’ve learned that standard cover often fails during building works due to unoccupancy clauses and structural exclusions. By choosing landlord insurance for property undergoing renovation, you ensure that both the existing structure and the new works remain protected against fire, theft, and liability claims. As an FCA-authorised firm with over 30 years of industry experience, Just Quote Me provides the specialized knowledge needed to bridge this gap. We offer direct access to top UK insurers that high-street brokers often miss; this gives you a steady hand in a complex and evolving market. Don’t let administrative burdens or insurance gaps stall your progress or threaten your capital. Secure your investment with expert landlord cover today so you can focus on completing your build and welcoming new tenants with total confidence.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Frequently Asked Questions

Can I keep my existing landlord insurance during a renovation?

You usually cannot maintain a standard policy without making significant changes. Standard landlord insurance is designed for tenanted properties, and insurers view a construction site as an entirely different risk. You must notify your provider before work begins; they will likely require you to switch to specialized landlord insurance for property undergoing renovation to ensure your building remains protected while it is vacant and under construction.

What happens if a fire occurs while the property is empty for works?

If you haven’t disclosed the renovation to your insurer, they may reject the claim entirely due to a “material change in risk.” If you have the correct cover in place, a fire is typically covered as a core peril. However, if you rely on a standard policy that has lapsed into “unoccupied” status, you might only have basic fire cover while losing protection against theft or water damage.

Do I need different insurance for structural vs. non-structural renovations?

Yes, the type of work dictates the level of cover required. Cosmetic updates like new flooring or painting often only require a simple notification to your broker to keep the policy valid. Structural changes, such as loft conversions or removing load-bearing walls, introduce risks like building collapse. These projects necessitate a dedicated renovation policy that accounts for the increased complexity and liability of major works.

Is renovation insurance more expensive than standard landlord insurance?

Renovation policies generally carry higher premiums because the risks on a building site are much greater than in a tenanted home. Factors such as the presence of “hot works,” unsecured materials, and the lack of a permanent resident increase the likelihood of fire or theft. While the cost is higher, it is a vital investment to prevent your standard policy from being voided during the project.

How long can a property be unoccupied for renovations before cover is restricted?

Most standard policies trigger unoccupancy restrictions after 30 to 60 consecutive days. Once this window passes, your insurer will likely reduce your cover to basic perils only. For any project exceeding this timeframe, you must secure landlord insurance for property undergoing renovation to maintain full protection for the duration of the build.

Does renovation insurance cover my builders’ tools and equipment?

No, your property insurance typically protects the building and the materials that will permanently form part of the structure. It does not cover the tools, plant, or equipment owned by your contractors. You must verify that your builder has their own active tradesman insurance to cover their assets and their own liability while working on your site.

What is the difference between renovation insurance and Contractors All Risk?

Renovation insurance focuses on the existing structure and your liability as the property owner. Contractors all risks insurance is a more comprehensive product that covers the “works in progress” and materials on-site against physical loss or damage. For larger developments, having both ensures that the “shell” of the building and the new construction are equally protected from start to finish.

How do I switch back to normal landlord insurance once the work is done?

You should contact your broker as soon as you receive the final completion certificate from your building inspector. We will then update your policy details to reflect that the property is ready for let. This ensures you have the correct tenant-based liability and rent guarantee protections in place before your first residents move in.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.