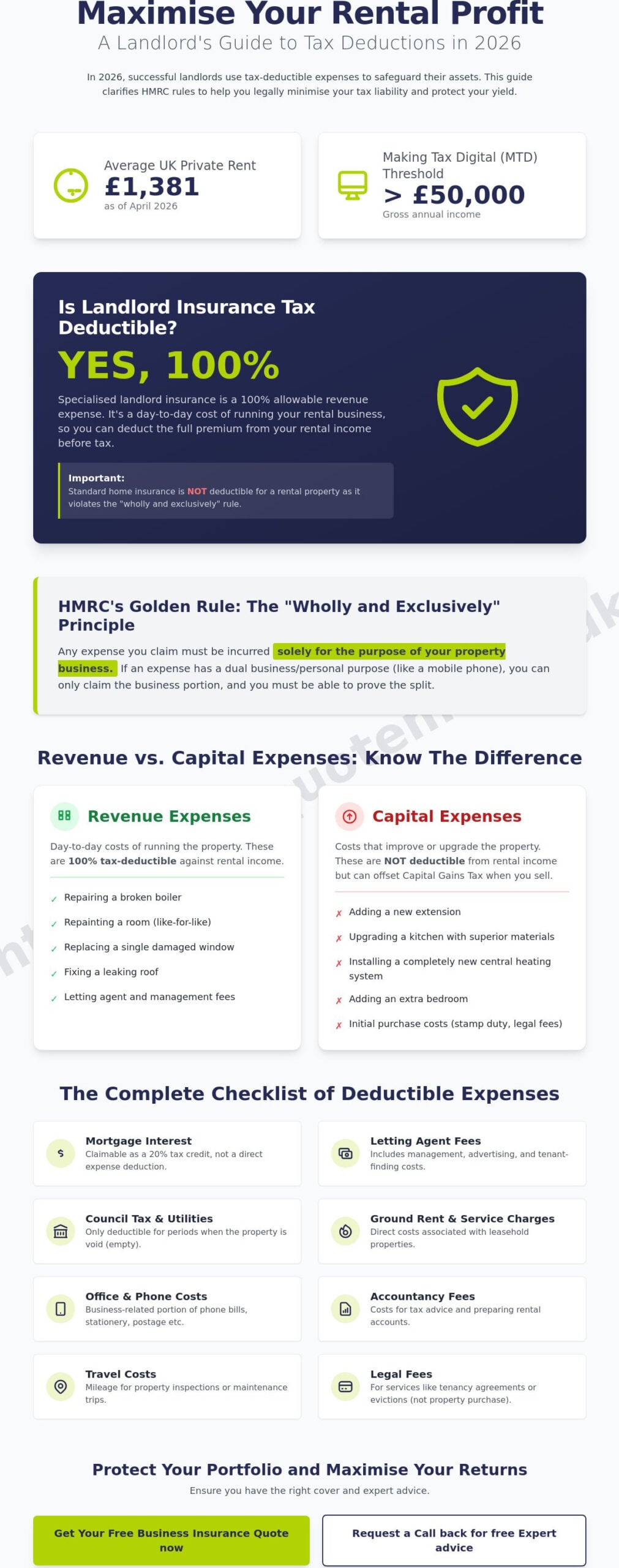

In 2026, the most successful landlords don’t view their premiums as a drain on profit; they see them as a 100% tax-deductible tool for safeguarding their assets. With the average UK private rent reaching £1,381 as of April 2026, protecting your yield is essential. Understanding exactly which tax deductible landlord insurance expenses you can claim is the difference between a thriving portfolio and one burdened by unnecessary costs.

We understand that the rising cost of property management and complex HMRC rules can be overwhelming. It’s perfectly normal to feel concerned about compliance, especially with the Renters’ Rights Act now in full effect. This guide promises to clarify the confusion by providing a definitive list of allowable costs to help you legally minimize your tax liability. We’ll break down the distinction between revenue and capital expenses, explain the 20% mortgage interest tax credit, and prepare you for the Making Tax Digital transition starting in April 2026.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Key Takeaways

- Learn how to apply the HMRC “wholly and exclusively” rule to ensure every claim meets the official standard for property income reporting.

- Understand why specialized landlord cover is a 100% allowable revenue expense and how to correctly record your tax deductible landlord insurance expenses.

- Master the critical distinction between day-to-day revenue repairs and capital improvements to avoid common classification errors on your tax return.

- Discover which professional fees, including letting agent costs and legal services, can be legally deducted to further reduce your total tax liability.

- Identify how expert broker advice helps uncover specialized deductible covers while protecting your portfolio from the financial risks of under-insurance.

Understanding Landlord Allowable Expenses: The HMRC Framework for 2026

The year 2026 brings a significant shift in how property owners manage their finances. With the rollout of Making Tax Digital (MTD) on 6 April 2026, landlords earning over £50,000 must transition to digital record-keeping. This shift isn’t just about software; it’s about precision in identifying the HMRC Framework for 2026 requirements. Successfully claiming tax deductible landlord insurance expenses requires a clear understanding of what HMRC allows and what it rejects.

To stay compliant, you must separate your personal finances from your rental business. HMRC expects every penny claimed to serve the business directly. If you manage a portfolio, keeping digital receipts for at least six years is no longer a suggestion; it’s a regulatory necessity under the new MTD rules. This ensures you have a robust audit trail if HMRC ever queries your figures. Being proactive about your documentation now saves significant stress during the January tax season. It’s about building a reliable system that stands up to scrutiny.

The “Wholly and Exclusively” Principle Explained

HMRC’s golden rule is simple: an expense must be incurred “wholly and exclusively” for the purpose of your property business. This means your landlord insurance premium is fully deductible because it protects a business asset. However, the line blurs with dual-purpose costs. For instance, if you use your personal mobile phone for both private calls and tenant management, you can only claim the business portion of the bill. You must have a reliable way to calculate that split, such as itemised billing.

Landlords often trip up on travel costs. While driving to your rental property for an inspection is a valid deduction, adding a personal errand to that trip can complicate your claim. If an expense doesn’t have a clear, separable business purpose, HMRC will likely disallow the entire amount during an audit. It’s always safer to keep business and personal activities distinct to protect your tax position and maintain professional records.

Cash Basis vs. Accruals Accounting in 2026

Most individual landlords now use “cash basis” accounting by default. This method is straightforward; you record income when it hits your bank and expenses when you actually pay them. It’s ideal for smaller portfolios because it mirrors your actual cash flow. However, if your gross rental income exceeds £150,000, you must use the “accruals” method. The 2026 environment prioritises this simplicity for those under the threshold, making it easier to manage quarterly MTD updates without complex adjustments.

Accruals accounting records income and expenses when they are invoiced, not necessarily when money changes hands. This method offers a more accurate picture of long-term profitability but requires more complex bookkeeping. Choosing the right method affects when you can claim your tax deductible landlord insurance expenses, especially if you pay for a multi-year policy upfront. We recommend sticking to the method that best aligns with your portfolio’s size and complexity to ensure long-term peace of mind.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Is Landlord Insurance Tax Deductible? A Detailed Breakdown

Landlord insurance is a 100% allowable revenue expense. Unlike capital expenses, which cover property improvements, revenue expenses are the day-to-day costs of running your rental business. Since insurance is vital for protecting your income stream, HMRC permits you to deduct the full premium from your rental income before calculating your tax bill. This applies specifically to residential letting insurance, which is designed for the unique risks of tenanted properties.

You cannot claim standard home insurance on a rental property. Standard policies are for personal residences; using them for a business asset violates the “wholly and exclusively” rule discussed earlier. HMRC expects you to use professional-grade cover that reflects the commercial nature of your activity. If you manage a portfolio, you can deduct the total cost of a multi-property policy. Simply divide the total premium across your properties or claim it as a single business expense if you report your portfolio income as one entity. Reviewing the official HMRC allowable costs guidance confirms that these premiums are essential for professional risk management.

Deductible Types of Landlord Cover

Core protections like buildings and contents insurance are the most common tax deductible landlord insurance expenses. These policies safeguard the physical structure and any furnishings you provide. Landlords’ liability insurance is equally critical. It covers legal costs and compensation if a tenant or visitor is injured on your property. HMRC considers this a necessary business protection because it manages a risk inherent to your trade as a property owner.

Rent guarantee and legal expenses insurance are often overlooked but are entirely deductible. These covers ensure your income continues if a tenant stops paying and provide funds for legal proceedings, such as evictions. Because these costs directly protect your business revenue and resolve legal disputes arising from your tenancy agreements, they meet the strict business-only criteria required for a valid claim. They are essential tools for maintaining financial stability in a changing regulatory market.

Specialised Policies and HMRC Compliance

If your portfolio includes mixed-use buildings, such as a flat above a retail unit, you will likely need commercial property insurance. The premiums for these complex risks remain fully deductible as long as the cover applies to the parts of the building you rent out for profit. Similarly, if a property is empty during a standard renovation period between tenancies, unoccupied property insurance is a valid revenue expense. It protects the asset while you prepare it for the next income-generating period.

For landlords who handle their own repairs and maintenance, insurance for a van and tools is also deductible. If the vehicle is used solely for property maintenance, the entire premium is a business cost. If the vehicle has dual use, you must apportion the cost accurately based on mileage or time spent on business tasks. Getting the right cover is simple when you tailor your policy to your specific portfolio needs.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Revenue vs. Capital Expenditure: Avoiding Costly Tax Mistakes

Distinguishing between revenue and capital costs is a critical skill for any landlord looking to protect their profit margins. While your tax deductible landlord insurance expenses are clearly revenue costs, the money you spend on the building itself requires closer inspection. Getting this wrong doesn’t just mess up your bookkeeping; it can lead to significant issues during an HMRC audit. Revenue expenses are deducted from your rental income in the year they occur, providing immediate tax relief. Capital expenditure, conversely, is offset against your profit when you eventually sell the property, reducing your Capital Gains Tax liability.

HMRC applies the “like-for-like” rule to help landlords navigate these choices. This rule allows you to treat modern equivalents as repairs even if they technically offer a slight upgrade. For example, replacing old single-glazed windows with modern double-glazed units is typically accepted as a repair because double-glazing is now the industry standard. You aren’t adding a new feature; you’re simply maintaining the property to a modern habitable level. Reviewing the HMRC allowable expenses guidance ensures you stay on the right side of this distinction.

What Counts as a Repair (Revenue Expense)?

Revenue expenses are the day-to-day outgoings required to keep your property in its current state. Common examples include repainting walls between tenancies, treating rising damp, or fixing a broken window pane. Safety compliance is also a major factor. Paying for annual boiler services or Mandatory Electrical Investment Condition Reports (EICR) are fully deductible revenue costs. If you hire contractors for these tasks, ensure they have their own builders insurance to protect your investment during the works. These costs directly reduce your taxable profit for the current year, keeping your cash flow healthy.

What Counts as an Improvement (Capital Expenditure)?

Capital expenditure involves works that significantly increase the property’s value or change its footprint. Building a rear extension, converting a loft into a bedroom, or installing a brand-new conservatory all fall into this category. Upgrading materials for purely aesthetic or luxury reasons also counts. If you replace standard laminate worktops with high-end granite, HMRC may view the cost difference as an improvement. Additionally, any repairs carried out on a newly purchased property to make it habitable for the first time are generally treated as capital costs rather than revenue repairs. These expenses are recorded now but only “claimed” when you eventually sell the asset.

When planning these types of value-adding projects, many landlords look for flexible financing solutions; in such cases, you can check out I Need Cash to find a variety of loan products that might suit your investment strategy.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

The Complete Checklist of Other Deductible Rental Expenses

Maximising your tax efficiency requires looking beyond your core buildings and contents cover. While tax deductible landlord insurance expenses form a significant part of your annual claims, HMRC permits the deduction of numerous other operational costs. These expenses must meet the “wholly and exclusively” criteria mentioned earlier, ensuring they serve only your property business. Keeping a comprehensive log of these smaller outgoings can lead to substantial savings when it’s time to submit your quarterly MTD updates in 2026.

If you use a letting agent to manage your portfolio, their fees are fully allowable. This includes “find-a-tenant” services, tenant referencing, and monthly management percentages. For many, the cost of outsourcing these administrative burdens is worth the peace of mind, especially as it directly reduces your taxable profit. Similarly, utility bills like water, gas, and electricity are deductible if you’re the one responsible for paying them, which is common in Houses in Multiple Occupation (HMOs).

Professional and Legal Services

Legal fees are a necessary part of modern property management. You can deduct the costs associated with drafting tenancy agreements or renewing existing contracts. If you face the unfortunate situation of tenant disputes or evictions, the legal fees and court costs are also allowable revenue expenses. Professional fees for accountants who prepare your rental accounts or provide tax advice are equally deductible.

Your business protection should also be accounted for. If you employ staff, such as a dedicated gardener or cleaner, you’re legally required to have employers liability insurance, and this premium is a valid business cost. Additionally, maintaining public liability insurance protects you from third-party injury claims on your premises and is a 100% deductible expense. If you’re unsure which specialized covers you need for your staff or business, speak with our team for tailored advice.

Travel and Subsistence Rules

HMRC allows you to claim for travel specifically related to your property business. This includes trips for inspections, maintenance, or meeting with contractors. For the 2026 tax year, you can use the approved mileage rates, which typically stand at 45p per mile for the first 10,000 miles. However, the “main purpose” test is vital. If the primary reason for your journey is business, you can claim the cost. If you combine a property visit with a personal trip, you can only claim the portion of the journey that is strictly business-related.

Be careful with your starting point. HMRC is strict about where your business “base” is located. If you manage your properties from a home office, your mileage generally starts from your front door. However, if you have a separate office, the commute to that office isn’t deductible. Only the travel from your business base to the rental properties counts toward your tax deductible landlord insurance expenses and other related claims. Keeping a precise mileage log is the best way to avoid HMRC penalties during an audit.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Strategic Risk Management: Why Expert Broker Advice Saves Landlords Money

Choosing the right policy is about more than just finding the lowest premium. While your tax deductible landlord insurance expenses lower your overall tax bill, the primary goal is protecting your capital. Relying on generic comparison sites often leads to under-insurance, a risk that an estimated 400,000 UK landlords are currently taking. When a claim is rejected due to incorrect cover or a failure to disclose specific tenancy types, the small saving on the premium becomes a massive financial liability. An independent broker acts as a steady hand, ensuring your policy is bespoke and fully compliant with HMRC standards.

Positioning your insurance as a proactive profit-protection strategy rather than a mere administrative burden changes your financial outlook. Expert advice helps you identify specialised covers, such as rent guarantee or legal expenses, which we’ve already confirmed are fully deductible. By maximising these claims, you’re effectively using HMRC-approved methods to subsidise a more robust safety net for your portfolio. It’s a pragmatic approach that prioritises long-term stability over short-term pennies.

The Broker Advantage vs. Comparison Sites

Automated systems are designed for simplicity, but they often miss the nuances of professional property management. They might not ask the right questions about your tenant’s employment status or the specific construction of your building, leading to policies that are technically non-compliant. Regional expertise is particularly valuable for landlords with properties in Staffordshire. Understanding the local market in Newcastle-under-Lyme and Stone allows a broker to provide accurate rebuild valuations and risk assessments that generic algorithms ignore.

Just Quote Me simplifies this entire process by managing the complex administrative burdens for you. We understand that your time is better spent growing your portfolio than decoding policy wording. By sourcing landlord insurance that fits your specific needs, we ensure that every pound spent is a valid business expense. This human-centric approach provides a level of security that a computer script simply can’t match.

Securing Your 2026 Property Portfolio

As you prepare for the 2026 tax year, accuracy in your records is paramount. With Making Tax Digital (MTD) arriving in April 2026 for those earning over £50,000, your digital audit trail must be flawless. Ensure all your tax deductible landlord insurance expenses are recorded quarterly to stay ahead of the new requirements. If you started receiving rental income in the 2025/26 tax year, don’t forget the registration deadline for Self-Assessment on 5 October 2026.

Finalising your preparations involves a quick review of your current protections. Check that your cover reflects the latest average UK private rent of £1,381 to ensure your rent guarantee levels are sufficient. Comprehensive cover is the foundation of a profitable property business, providing the peace of mind you need to navigate a changing regulatory environment. Taking these steps now ensures you’re both legally protected and tax-efficient for the year ahead.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Future-Proof Your Property Business for 2026

Managing a successful rental portfolio in 2026 requires more than just collecting rent; it demands a precise approach to financial compliance and risk management. With the arrival of Making Tax Digital on 6 April 2026, the importance of accurate digital record-keeping cannot be overstated. By correctly identifying your tax deductible landlord insurance expenses and distinguishing between revenue repairs and capital improvements, you protect your profit margins while staying on the right side of HMRC.

Just Quote Me provides the steady hand you need in this complex market. With over 30 years of industry experience and FCA-authorised expert advice, we specialise in delivering bespoke cover for multi-property portfolios. We handle the administrative complexities so you can focus on growing your investments with confidence. Our team ensures that your insurance isn’t just a regulatory requirement, but a strategic tool for long-term profitability. Take control of your property’s financial health today and move forward with a partner who understands your sector.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Frequently Asked Questions

Is landlord insurance a legal requirement for UK landlords in 2026?

No, there is no specific UK law requiring landlords to have specialist insurance, but it’s often a mandatory condition of buy-to-let mortgage agreements. Operating without it leaves you personally liable for property damage or legal claims. Most professionals view it as an essential safeguard for their investment rather than an optional cost. It ensures you have the financial backing to handle major incidents without depleting your personal savings.

Can I deduct my mortgage interest payments as an allowable expense?

You cannot deduct mortgage interest directly from your rental income to reduce your taxable profit. Instead, you receive a 20% tax credit on your mortgage interest payments. This rule has been standard since April 2020 and remains the protocol for the 2025-2026 tax year. It’s vital to calculate this credit separately on your Self-Assessment return to ensure your tax bill is accurate.

What happens if I forget to claim an allowable expense on my tax return?

You can generally amend your Self-Assessment tax return within 12 months of the original filing deadline. If you discover an error after this window, you may be able to claim “overpayment relief” for up to four years. Proactive bookkeeping is the best way to avoid missing out on legitimate deductions like tax deductible landlord insurance expenses. Keeping digital records updated quarterly will help prevent these omissions in the future.

Is rent guarantee insurance tax-deductible under HMRC rules?

Yes, rent guarantee insurance is a fully allowable revenue expense because it directly protects your business income. This type of cover is one of many tax deductible landlord insurance expenses that help reduce your overall liability. It ensures your cash flow remains stable even if a tenant defaults on their payments, meeting the “wholly and exclusively” criteria for professional property management.

Can I claim for my own time spent doing repairs on the property?

You cannot claim a monetary value for your own time or labour when performing repairs. HMRC only allows you to deduct the actual cost of materials used or the fees paid to third-party contractors. While you can’t pay yourself a salary for maintenance, any insurance premiums covering your tools remain deductible. This makes it more tax-efficient to hire qualified professionals for complex maintenance tasks.

Are the fees I pay to an insurance broker tax-deductible?

Yes, any professional fees or service charges paid to a broker to arrange your cover are 100% tax-deductible. These costs are considered part of the administrative overhead of running a professional property business. Including these fees ensures you aren’t paying more tax than necessary on your rental yields. It’s a legitimate cost of securing expert advice for your portfolio rather than relying on generic automated systems.

How do I claim for replacement furniture in a furnished let?

You claim for furniture through the “Replacement of Domestic Items Relief” rather than as a standard repair. This allows you to deduct the cost of replacing sofas, beds, or white goods on a like-for-like basis. You cannot claim for the initial cost of furnishing a property for the first time, as HMRC views that as a capital expense. The relief only applies when you replace an existing item with a modern equivalent.

Do I need to keep physical receipts for all my landlord expenses?

You don’t need to keep physical paper receipts as long as you have legible digital copies. HMRC accepts scanned images or digital invoices, which is especially helpful for the Making Tax Digital transition starting in April 2026. You must retain these records for at least six years to ensure you can provide evidence during a potential audit. Moving to a digital-first system now will simplify your future reporting requirements.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice