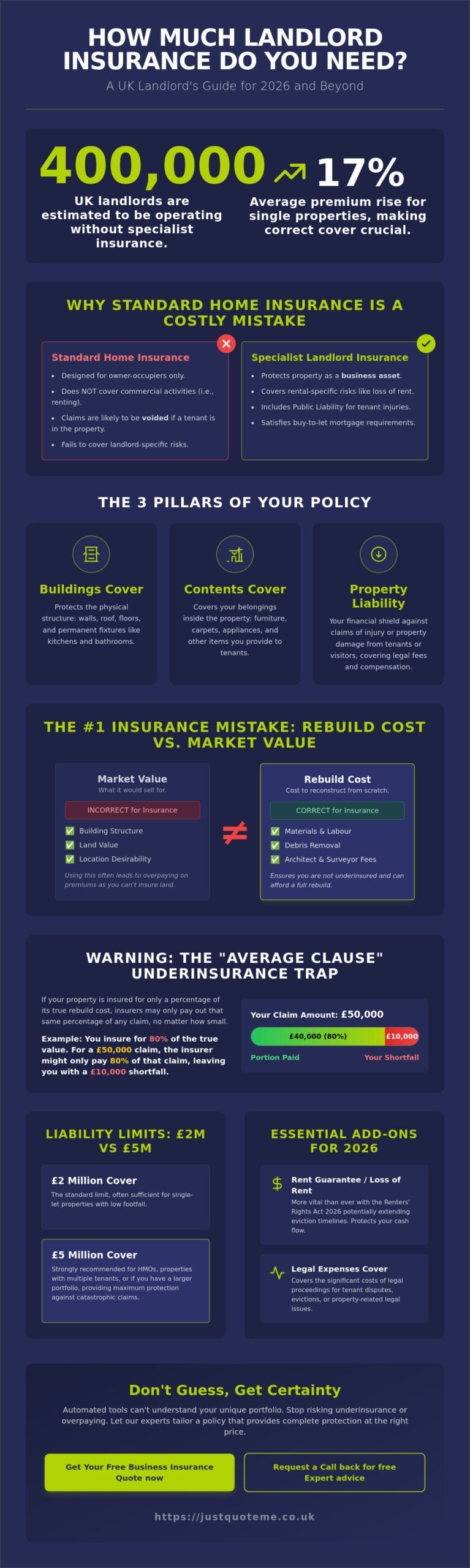

An estimated 400,000 UK landlords are currently operating without any specialized landlord insurance, leaving their entire property portfolio at significant risk. If you are asking yourself “how much landlord insurance do i need uk” in the current market, you are not alone. With premiums rising by an average of 17% for single properties, finding the balance between comprehensive protection and cost efficiency has never been more critical.

It’s frustrating to face rising costs while trying to decipher the technical difference between a property’s market value and its actual rebuild cost. You want to protect your investment without overpaying for coverage you don’t actually need. This guide provides a clear framework to calculate your exact cover limits, ensuring you remain fully compliant with the Renters’ Rights Act 2026. We’ll walk you through building rebuild costs, choosing between £2 million and £5 million public liability limits, and identifying essential add-ons like rent guarantee cover. Rather than guessing your requirements, Just Quote Me to simplify the process. By the end, you’ll have the confidence to secure a policy that fits your specific needs.

- Learn why standard home insurance is inadequate for rental properties and how specialist landlord cover provides the multi-layered business protection you need.

- Master the calculation for how much landlord insurance do i need uk by using rebuild costs instead of market value to prevent the risk of underinsurance.

- Identify whether a £2 million liability limit is enough for your property or if tenant profiles require a £5 million ceiling for total security.

- Understand how the Renters Rights Act 2026 has changed eviction timelines, making loss of rent and legal expenses cover more vital for your cash flow.

- Just Quote Me to access bespoke insurance schemes and expert advice that automated comparison tools simply can’t provide.

Understanding Landlord Insurance: Why “How Much” Matters in 2026

Landlord insurance is more than just a policy; it’s a multi-layered business protection strategy designed for those who treat property as a serious investment. Unlike a standard home policy, it accounts for the specific risks of renting to third parties, such as loss of rent or tenant injuries. If you’re looking for a formal definition of landlord insurance, it’s a specialist contract that shifts the financial burden of property damage and legal liabilities from the owner to the insurer. Using a standard domestic policy for a rental property is a high-stakes gamble that usually results in voided claims because home insurance simply doesn’t cover commercial activities.

Many property owners ask, “how much landlord insurance do i need uk?” while looking at the 2026 market. While the median annual cost currently sits at £284.75, this figure is merely a national benchmark. Your specific requirements depend on the reconstruction value and your liability exposure. Relying on national averages can lead to the “average clause” trap. If your property is insured for only 80% of its true rebuild cost, the insurer may only pay out 80% of any claim, even for minor repairs. This makes precision vital in a market where construction costs and labour rates are rising rapidly.

The Legal vs. Practical Requirement

Technically, landlord insurance isn’t a legal requirement in the UK. However, the practical reality is very different. If you have a buy-to-let mortgage, your lender will mandate a specific level of buildings cover to protect their security. They want to know that if the property is destroyed, the loan can be repaid. Beyond the mortgage, you have a duty of disclosure under FCA regulations. You must inform your insurer that the property is let to tenants rather than being owner-occupied. Failing to provide this information is considered non-disclosure. This can void your policy entirely, leaving you personally liable for catastrophic losses and potentially facing legal action from your lender. For medical professionals, consulting specialists like Mortgages for Doctors can ensure that remortgage terms and insurance requirements are handled with expert precision.

Key Components of a Landlord Policy

A robust residential letting insurance policy typically centers on the “Big Three”: buildings, contents, and liability. These components interact to form your total sum insured. Buildings cover handles the structure itself, including permanent fixtures like kitchens and bathrooms. Contents cover protects your furniture, appliances, and carpets. Liability is your shield against tenant injury claims. Identifying which of these are mandatory for your portfolio is the first step toward total protection. For example, a furnished flat requires a higher contents limit than an unfurnished house. However, both need substantial liability protection because a single injury claim can exceed £1 million. These elements work in tandem to ensure a single accident doesn’t derail your financial future.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Calculating Buildings Insurance: Rebuild Cost vs. Market Value

The most frequent error property owners make when asking “how much landlord insurance do i need uk” is providing the market value of their property instead of its rebuild cost. These two figures are rarely the same. Market value includes the land price and the desirability of the location. The rebuild cost, however, is the actual amount required to reconstruct the building from scratch if it were destroyed. If you insure for the market value, you’ll likely overpay on premiums because the land doesn’t need to be rebuilt. Conversely, if the market value is lower than construction costs, you’ll be dangerously underinsured.

In 2026, calculating this accurately is tougher than before. Construction material prices and skilled labour costs have seen significant inflation, meaning a valuation from even two years ago is likely outdated. You must account for more than just bricks and mortar. A comprehensive sum insured includes professional fees for architects and surveyors, as well as the high cost of debris removal. Clearing a site after a total loss is a massive logistical undertaking that can cost thousands before a single brick is laid. This is why meeting your legal responsibilities for UK landlords requires a realistic assessment of these “hidden” expenses.

The RICS Rebuild Calculator

To get an accurate figure, start with the Building Cost Information Service (BCIS) calculator provided by the Association of British Insurers (ABI). This tool uses Royal Institution of Chartered Surveyors (RICS) data to estimate costs based on your property’s square footage and type. If you own a Victorian or period property in Staffordshire, be cautious. These homes often require specialist materials and heritage craft skills that standard calculators might miss. For listed buildings or non-standard construction, it’s safer to commission a professional Reinstatement Cost Assessment (RCA). Regional variations in the West Midlands construction market also play a role, as local labour rates can fluctuate compared to national averages.

Fixtures, Fittings, and “Permanent” Contents

When defining your buildings sum, don’t forget permanent fixtures. This includes fitted kitchens, bathroom suites, and built-in wardrobes. These are part of the structure, not your contents. You should also value outbuildings, garden walls, and gates. An accurate residential letting insurance policy needs to cover every physical aspect of the investment. If you’re unsure whether an item counts as a fixture or a content, it’s best to ask a specialist broker who understands the nuances of policy wording. Accurate valuation ensures that your claim is paid in full without the penalty of the average clause.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Determining Liability Limits: Is £2 Million Really Enough?

While buildings insurance protects the physical structure, Property Owners Liability is what protects your personal wealth. This cover acts as a shield against claims for compensation if a tenant or visitor is injured on your property due to your perceived negligence. A loose floorboard, a faulty handrail, or even a poorly maintained garden path can trigger a claim that reaches into the millions. When determining how much landlord insurance do i need uk, the liability limit is often the most misunderstood component because it isn’t tied to the property’s value, but to the potential cost of a human injury.

In the UK, £2 million is the absolute baseline for most landlord policies. For a single-occupancy residential let, this is usually sufficient. However, a standard guide to landlord insurance policies will highlight that certain scenarios demand much higher indemnity. If you rent to local authorities, the NHS, or student housing providers, they frequently mandate a minimum of £5 million or even £10 million in liability cover as a contractual requirement. Your risk exposure also shifts based on your tenant profile; high-density Houses in Multiple Occupation (HMOs) naturally carry a higher probability of accidents than a single-family home.

Public Liability vs. Employers Liability

Many landlords don’t realize they may be legally required to hold more than just public liability. If you employ anyone to help maintain your portfolio, such as a regular gardener, a cleaner for communal areas, or even a part-time property manager, you likely need employers liability insurance. Under UK law, if you’re deemed an employer, you must have at least £5 million in EL cover or face fines of up to £2,500 per day. A comprehensive policy often bundles these together, ensuring that if a contractor is injured while working on your property, your business remains solvent.

The Cost of Litigation in 2026

Legal fees in 2026 have continued to trend upwards, making the “defence costs” portion of your liability cover more vital than ever. It’s not just about the final settlement; it’s about the cost of proving you weren’t at fault. For landlords in areas like Newcastle-under-Lyme and Stone, where property types vary from Victorian terraces to modern developments, the legal nuances of maintenance disputes can become complex. Your liability limit must be high enough to cover both the potential damages awarded to a claimant and the substantial legal fees required to defend your position in court. Without adequate limits, a single protracted legal battle could exceed a basic £1 million policy limit in months.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Assessing Optional Extras: Loss of Rent and Tenant Risks

Once you’ve secured your buildings and liability limits, the next step in answering “how much landlord insurance do i need uk” involves protecting your cash flow. Loss of rent cover is designed to reimburse you if a fire or flood makes your property uninhabitable. To calculate this sum insured, you must multiply your monthly rental income by the “indemnity period.” While 12 months was once the standard, the 2026 market demands more caution. Major repairs often face delays due to planning permission or contractor availability, so many landlords now opt for 24 or 36 months to ensure their mortgage payments remain covered during a long-term rebuild.

The implementation of the Renters’ Rights Act 2026 on May 1, 2026, has fundamentally changed the risk landscape. With the abolition of Section 21 “no-fault” evictions, regaining possession of a property now requires specific legal grounds under Section 8. This shift typically extends the timeline for evicting non-paying tenants, making rent guarantee insurance a necessity rather than a luxury. When assessing your policy, check if it covers accidental damage caused by tenants or if you need to add malicious damage protection. Malicious damage is rarely included in basic policies but is vital if you want protection against intentional vandalism.

Tenant Type and Risk Profiling

Your choice of tenant directly impacts your premium and the level of cover required. Data shows that employed tenants typically attract lower premiums, while student lets or those on housing benefits can increase the average cost due to perceived higher risks. HMOs require even higher indemnity limits because the footfall and shared facilities increase the likelihood of both accidental damage and liability claims. If your portfolio includes flats above shops or offices, you may need to integrate commercial property insurance to cover the mixed-use nature of the building. Each tenant profile requires a bespoke approach to ensure no gaps in protection exist.

Legal Expenses and Home Emergency Cover

Legal expenses cover is another critical “extra” that has gained importance in 2026. With the new tribunal processes following the Renters’ Rights Act, legal fees can quickly spiral. A limit of £50,000 for legal expenses was standard, but many professionals now suggest higher limits to handle protracted disputes. For landlords with properties in Stafford or surrounding areas, adding 24/7 home emergency cover provides a pragmatic solution for urgent repairs like burst pipes or boiler failures. This doesn’t just protect the building; it ensures you meet your legal obligation to provide a safe, habitable home. To ensure your optional extras are correctly weighted for your specific risks, speak with an insurance expert today.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Expert Advice: Customising Your Policy with Just Quote Me

Comparison sites often provide a generic answer to how much landlord insurance do i need uk based on broad averages. This approach is risky. It ignores the unique characteristics of your property and the specific tenant risks you face. An independent broker like Just Quote Me offers a level of accuracy that automated systems can’t match. We don’t rely on “one size fits all” algorithms. Instead, we use our 30-year heritage in Staffordshire and the West Midlands to assess your risk profile with precision. This regional expertise is vital for accurately valuing properties in local areas where construction styles and labour costs vary significantly.

One of the biggest advantages of working with a specialist is accessing bespoke insurance schemes. These aren’t available on the high street or on standard comparison tools. These schemes are often tailored to specific sectors, providing more robust protection at competitive rates. We help you navigate the “Average Clause” trap mentioned in previous sections. By providing expert valuation advice, we ensure your rebuild cost reflects current material prices. This prevents insurers from reducing your claim payout due to underinsurance. It’s about securing your investment with a steady hand in a complex market where guessing “how much landlord insurance do i need uk” could cost you thousands.

The Just Quote Me Advantage

We believe in personalised risk assessments. Whether you own a single terrace or a diverse portfolio of HMOs and flats, we manage the administrative burden for you. We can often consolidate multiple properties into a single policy. This simplifies your renewals and ensures consistent cover across your entire investment. If you have mixed-use units, we can also integrate commercial property insurance to cover the retail or office elements of your building. This human-centric approach ensures you aren’t just a policy number. You’re a partner with a protected future, managed by experts who understand the nuances of the 2026 property market.

Next Steps for UK Landlords

To ensure your property remains fully protected, follow these steps:

- Review your current rebuild cost. Compare it against 2026 inflation rates to ensure your sum insured is still accurate and covers debris removal and professional fees.

- Check your liability limits. Ensure they meet the requirements of your tenancy agreements, especially if you deal with local authorities or the NHS.

- Audit your optional extras. Make sure you have adequate rent guarantee and legal expenses cover to handle the complexities of the Renters’ Rights Act 2026.

Our team is ready to help you navigate these calculations. Don’t leave your property investment to chance with an automated quote. Just Quote Me to find a policy that offers genuine security and value.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Protect Your Portfolio with Precise Coverage

Securing your property investment requires more than a standard policy; it demands a precise calculation of rebuild costs and a deep understanding of your legal exposure. As construction costs fluctuate and the Renters’ Rights Act 2026 reshapes the market, answering “how much landlord insurance do i need uk” is no longer a matter of guesswork. By focusing on accurate reinstatement values rather than market prices, you avoid the financial trap of underinsurance and ensure your cash flow remains resilient against unexpected tenant disputes.

Just Quote Me brings over 30 years of brokerage experience and regional expertise to your side. As an FCA Authorised and Regulated broker, we provide access to top UK insurer panels and bespoke schemes that automated systems overlook. We manage the administrative complexity so you can focus on growing your business with confidence. Partner with a trusted advisor to secure your future today.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Frequently Asked Questions

How much landlord insurance is the minimum required by UK mortgage lenders?

Most UK mortgage lenders require you to have buildings insurance for 100% of the property’s rebuild cost. This ensures their financial interest is protected if the building is destroyed. When calculating how much landlord insurance do i need uk for a mortgage, check your offer document. It often specifies that the policy must be index-linked to keep pace with construction inflation.

Can I use my standard home insurance if I only rent out one room?

No, you cannot rely on a standard home insurance policy if you receive rent, even for a single room. Most domestic insurers consider this a change in risk that could void your policy. You must either add a lodger extension or switch to a specialist policy. This covers the specific liabilities associated with having a tenant in your home.

What is the “Average Clause” in landlord insurance and how do I avoid it?

The “Average Clause” is a penalty used by insurers when a property is underinsured. If you insure your building for 50% of its true rebuild cost, the insurer will only pay 50% of any claim, even for small repairs. To avoid this, use the RICS rebuild calculator or a professional surveyor to ensure your sum insured is 100% accurate.

Do I need different insurance for an HMO compared to a standard buy-to-let?

Yes, Houses in Multiple Occupation (HMOs) require specialist insurance because the risks are higher than a standard family let. HMO policies account for increased footfall, higher liability exposure, and specific fire safety regulations. Insurers often require higher indemnity limits for these properties to reflect the complexity of managing multiple unrelated tenants under one roof.

How does the 2026 Renters Rights Act affect my landlord insurance needs?

The 2026 Renters Rights Act abolished Section 21 “no-fault” evictions, meaning you now need specific legal grounds to regain possession. This change makes legal expenses cover and rent guarantee insurance essential. Since evictions may take longer through the courts, having a policy that covers your lost income and legal fees is now a critical part of your risk management strategy.

Is loss of rent cover based on my gross or net rental income?

Loss of rent cover is typically based on your gross rental income. This is the total amount of rent you receive before any expenses, such as mortgage payments or management fees, are deducted. When deciding how much landlord insurance do i need uk, ensure your sum insured covers the full annual rent to maintain your cash flow during major property repairs.

Does landlord insurance cover me if the property is unoccupied for 30 days?

Most standard landlord policies allow for a 30-day unoccupancy period between tenants. If your property remains empty for longer, you must notify your insurer to arrange unoccupied property cover. Failing to do so can lead to restricted coverage. This often excludes risks like theft, vandalism, or water damage while the building is vacant.

Should I include contents insurance if I am letting an unfurnished house?

Yes, you should still consider a limited amount of contents insurance even for unfurnished lets. This covers items you own that aren’t part of the building’s structure, such as carpets, curtains, and white goods. A basic contents limit of £5,000 is often sufficient to protect your investment in these essential fixtures against fire or flood damage.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.