With the abolition of Section 21 “no-fault” evictions as of May 1, 2026, a single tenant default could now leave your mortgage repayments in jeopardy for up to eight months. You likely recognize that the traditional safety nets have shifted, making the financial gap during a Section 8 possession process much harder to manage. Choosing rent guarantee insurance with no excess is the most effective way to close that gap entirely. It ensures that when a tenant stops paying, your coverage kicks in immediately without you having to sacrifice the first month of arrears to a costly deductible.

We understand that unexpected fees and legal complexities are the biggest hurdles to a profitable portfolio. This guide will show you how to eliminate out-of-pocket expenses and maintain a consistent cash flow regardless of tenant behavior. You’ll discover the specific benefits of zero-excess protection under the Renters’ Rights Act 2025 and learn how expert legal handling can take the weight of evictions off your shoulders. Just Quote Me for your landlord protection needs to simplify your administration and secure your professional future.

Key Takeaways

- Understand how the 2026 abolition of Section 21 “no-fault” evictions extends the timeline to regain property and why this makes reliable financial protection essential.

- Learn how rent guarantee insurance with no excess removes the standard one-month deductible, ensuring your cash flow remains uninterrupted from the very first missed payment.

- Identify the rigorous tenant referencing and documentation standards needed to secure a valid policy under the latest 2026 regulations.

- Evaluate the true cost-benefit of zero-excess coverage compared to standard policies, especially when facing a Section 8 court process that can last up to eight months.

- Discover the advantage of using an independent broker to access bespoke underwriters and personalized advice that automated online portals cannot provide.

The Risk of Tenant Default in the 2026 UK Rental Market

The UK rental market in 2026 is fundamentally different from previous years. Legislative shifts and persistent economic volatility have created a landscape where even the most diligent landlords face increased financial exposure. For many, the primary concern is no longer just finding a tenant, but ensuring that the income stream remains uninterrupted. Securing rent guarantee insurance with no excess has become a vital strategy to navigate these uncertainties without losing a month of income to a deductible.

Economic Pressures and Rental Arrears

Tenant stability is under pressure. Rising living costs in 2026 mean that disposable income is tighter than ever, leading to a direct correlation with rental arrears. We’ve seen that even high-earning tenants can suddenly become a liability due to unexpected unemployment or shifting market demands. When a tenant defaults, the financial impact isn’t just the lost rent; it’s the disruption to mortgage schedules and maintenance budgets. Rent insurance serves as a buffer against these systemic risks, providing a layer of security that a standard tenancy deposit simply cannot match. It’s no longer enough to rely on a tenant’s history when the broader economic environment is so unpredictable.

Legislative Hurdles for Modern Landlords

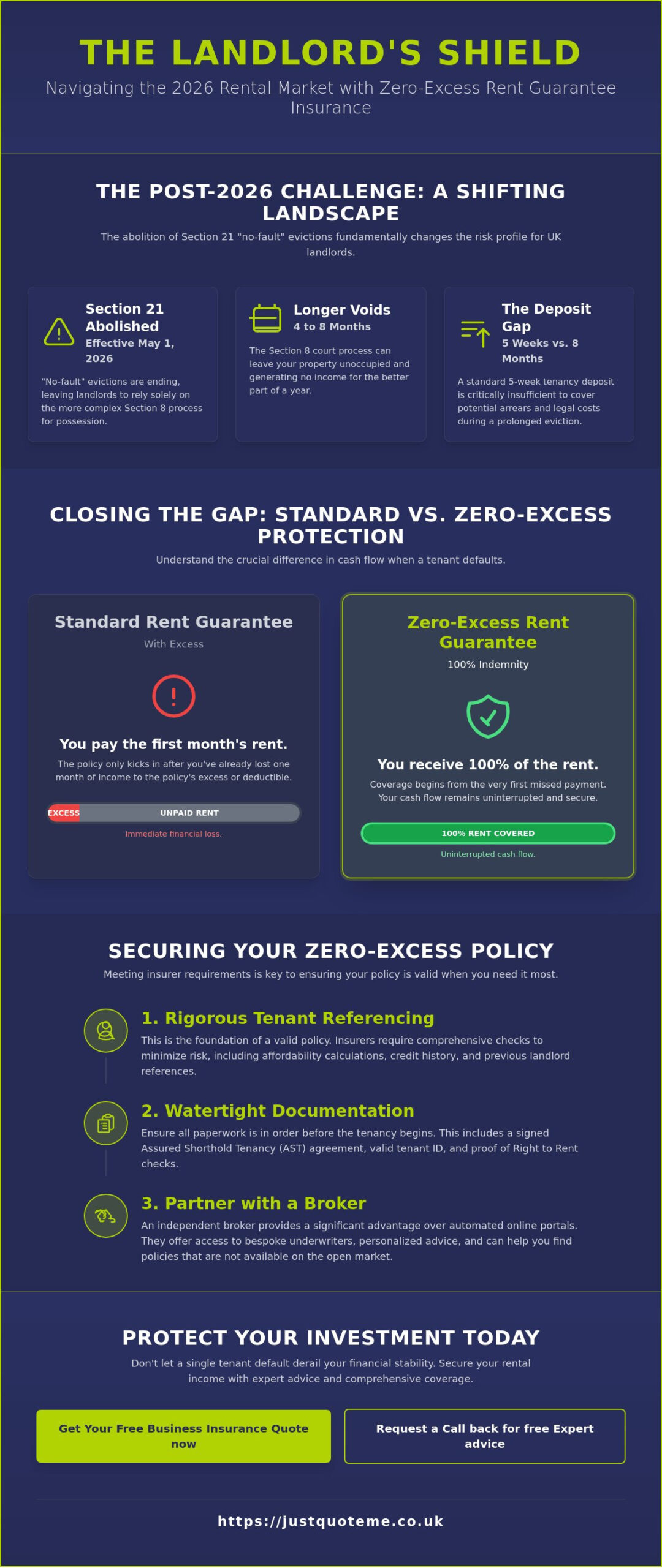

The Renters’ Rights Act 2025 has significantly altered the eviction process. As of May 1, 2026, the abolition of Section 21 “no-fault” evictions means landlords must now rely exclusively on the Section 8 possession process. This change has extended the timeline for regaining property possession to between four and eight months from the first missed payment. Legal expenses have climbed as court hearings become mandatory for most possession orders. Additionally, the 2026 claims process often involves mandatory mediation, adding another administrative layer to an already complex situation. These delays mean that a landlord without protection could be forced to cover mortgage payments out of pocket for the better part of a year.

Traditional deposit protection, usually capped at five weeks’ rent, is insufficient when faced with an eight-month eviction timeline. Without rent guarantee insurance with no excess, a landlord could be looking at thousands of pounds in lost income plus legal fees before the property is back on the market. This financial friction often leads to significant stress, especially for those who rely on rental income to cover mortgage payments. Having a residential letting insurance policy in place provides more than just financial reimbursement. It offers the psychological peace of mind that your investment is protected by experts who handle the legal heavy lifting. You won’t have to navigate the court system alone or worry about how a single tenant’s financial misfortune will impact your own credit standing.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice

What is Rent Guarantee Insurance with No Excess?

Rent guarantee insurance, also known as rent protection, is a specialized policy designed to reimburse landlords if a tenant fails to pay their monthly rent. While standard landlord insurance typically covers physical damage to the property or liability issues, it rarely includes lost income due to tenant default. This is where rent guarantee insurance with no excess steps in to fill the gap. It ensures that your mortgage repayments and maintenance costs don’t fall behind just because a tenant’s circumstances have changed.

Defining the Zero-Excess Advantage

In most insurance sectors, an excess is the amount you agree to pay toward a claim. If you have a £250 or £500 excess on a rent claim, you’re essentially losing a significant portion of your profit margin for that month. For a single-property landlord, this out-of-pocket cost can be the difference between breaking even and falling into debt. Zero-excess rent guarantee insurance is defined as 100% indemnity, meaning the insurer pays the full amount of the arrears from the very first penny. By removing this financial friction, you receive the total rent owed without any deductions. It makes the recovery process much smoother.

Core Policy Features to Look For

When selecting a policy in 2026, you need to look beyond the premium. Most robust plans offer monthly claim limits between £2,000 and £2,500 to reflect the current market rates. You can typically choose from cover durations of 6, 12, or 15 months. This flexibility is critical. Since evictions can now take up to 8 months, shorter policies might leave you exposed. A high-quality policy will also integrate with legal expenses insurance to ensure you aren’t paying for solicitors out of your own pocket.

The official government guide to renting outlines the legal responsibilities landlords must uphold, and a good policy supports these by including mediation services. These services aim to resolve disputes before they reach the court stage, potentially saving months of lost time. If you’re unsure which level of cover fits your portfolio, you can always explore our tailored landlord solutions to find a match. Combining rent guarantee insurance with no excess with expert legal handling creates a comprehensive safety net for your investment.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice

Comparing Standard vs. Zero-Excess Rent Protection

Choosing between a standard policy and rent guarantee insurance with no excess is more than just a matter of premium cost; it’s a strategic decision about your cash flow. Many landlords find that standard policies, while appearing cheaper on the surface, contain hidden financial friction that only becomes apparent during a claim. These policies often include a one-month excess or a fixed deductible that you must cover before the insurer pays a penny. In a market where margins are already squeezed by taxation and rising maintenance costs, losing a full month of rent to an excess can turn a managed risk into a significant financial setback.

The Financial Breakdown

To understand the real-world impact, consider a hypothetical scenario where a tenant defaults on a property with a monthly rent of £1,200. If the tenant stops paying for three months, the total arrears reach £3,600. With a standard policy carrying a £500 excess, your net payout would be £3,100, leaving you with a £500 shortfall. If the policy has a ‘first month’ excess, you might receive nothing for the initial 30 days of the default. This creates an immediate cash flow gap that you must bridge to meet mortgage obligations. In contrast, rent guarantee insurance with no excess provides the full £3,600. You receive 100% of the rent owed from the very first day of arrears, ensuring your financial planning remains uninterrupted.

Who Benefits Most from No-Excess Cover?

Individual landlords with tight mortgage margins are often the most vulnerable to the “first month” gap. If your rental income is your primary means of paying the property’s mortgage, any delay or deduction in payment can impact your credit standing. Professional landlords managing high-turnover HMOs also benefit significantly. Because the risk of default is distributed across multiple rooms, the frequency of claims can be higher; paying an excess on every claim would quickly erode the portfolio’s annual yield. Institutional investors seeking predictable annual returns also prefer zero-excess models because they eliminate the volatility associated with deductible fees and administration costs.

Beyond the immediate payout, standard policies sometimes hide additional costs in the form of administration fees or limited legal cover. We focus on providing a transparent experience where the value is clear from the start. If you want to avoid the administrative burden of calculating deductibles during a crisis, Just Quote Me for a straightforward, zero-friction solution. By removing the excess, you ensure that your residential letting insurance works exactly as intended: as a complete replacement for your lost income.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice

Eligibility and How to Secure a No-Excess Policy

Securing rent guarantee insurance with no excess requires more than just paying a premium. Because the insurer assumes 100% of the financial risk from day one, the eligibility criteria are rigorous. You must prove that your tenant is financially stable and that the tenancy is legally sound. If you’re switching from a standard residential letting insurance policy, understanding these requirements early prevents claim rejections later. Insurers view the quality of the tenant as the primary indicator of risk, so cutting corners during the initial setup isn’t an option.

Tenant Referencing Requirements

Insurance providers mandate a professional reference check for every adult tenant named on the agreement. This involves a formal credit search to identify CCJs or insolvencies, employment verification to confirm a stable income, and references from previous landlords. If a tenant’s income is less than 2.5 times the monthly rent, a guarantor is usually required to bridge the gap. This guarantor must pass the same level of scrutiny. The quality of these references directly dictates whether you qualify for a zero-excess product, as insurers only offer this level of protection to the most reliable tenant profiles.

The Application Process

Securing your policy involves a logical four-step sequence. First, conduct the professional reference check through an approved agency before the tenant moves in. Second, ensure you have a valid written tenancy agreement in place; under the 2026 regulations, these are typically periodic tenancies from day one. Third, obtain your quote for rent guarantee insurance with no excess through a specialist broker who can access exclusive underwriters. Finally, maintain meticulous records of rent statements and all tenant correspondence. It’s important to be aware of the 90-day waiting period. If you apply for cover for an existing tenant who has already moved in without prior insurance, most providers won’t allow a claim for defaults occurring within the first three months. This prevents landlords from seeking cover only after a tenant starts struggling.

You can switch to a zero-excess policy mid-tenancy, provided the tenant has a clear payment history for at least the last six months. Documentation is everything in the 2026 market. If you’re ready to secure your income, get started with a specialist landlord policy today to ensure you’re fully eligible before the next rent due date.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice

The Broker Advantage: Finding Bespoke Rent Protection

While many direct insurers promote a one-size-fits-all product, they often lack the flexibility to offer truly bespoke terms. Independent brokers act as a bridge to “broker-only” underwriters who specialize in high-value, zero-friction products. These specialist providers often reserve their best rent guarantee insurance with no excess deals for brokers because they trust the intermediary’s ability to verify tenant referencing and property standards. This access allows you to secure a policy that isn’t just a generic template; it’s a precise financial tool tailored to the specific risks of your portfolio. By working with a broker, you gain access to a wider market of underwriters who are willing to provide full indemnity without the standard deductibles found on comparison sites.

Personalised Support vs. Automated Systems

In the middle of a stressful tenant dispute, an automated online portal is a poor substitute for a knowledgeable advisor. You need a steady hand to help interpret complex policy wording and ensure your claim documentation is flawless. We provide regional expertise across the West Midlands and Staffordshire, offering a human-centric alternative to impersonal algorithms. A broker understands the local market nuances and can advocate on your behalf if a claim becomes complicated. This level of support simplifies the administrative burden. It allows you to focus on managing your properties while we handle the technicalities with the insurer. We don’t just provide a policy; we manage the complex administrative burdens so you don’t have to.

Customising Cover for Unique Portfolios

Standard portals often struggle with non-standard properties or diverse tenant types. If your portfolio includes HMOs or properties with specific architectural features, a broker can customize your cover to include risks that generic policies might exclude. This is particularly relevant for landlords who also manage commercial assets, such as those requiring thatched pub insurance or shop cover. A broker ensures that your rent guarantee insurance with no excess integrates seamlessly with your broader residential letting insurance, creating a cohesive safety net that leaves no room for unexpected out-of-pocket costs.

Your Next Steps for Secure Income

As we manage the regulatory changes of 2026, the value of predictable cash flow is higher than ever. Choosing a zero-excess policy is a pragmatic decision that eliminates the “first month” financial gap and protects your ROI against the extended timelines of the Section 8 process. Having the right protection in place is the foundation of long-term stability. Just Quote Me is here to ensure that your insurance works for you, providing the security you need in an evolving market. Secure your income today and eliminate the friction of tenant defaults.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice

Secure Your Rental Income for the Long Term

The 2026 rental market demands a proactive approach to income protection. With the Section 21 “no-fault” eviction process now a thing of the past, the financial burden of tenant default falls more heavily on landlords. By opting for rent guarantee insurance with no excess, you ensure that your cash flow remains consistent and your investment stays profitable. You don’t have to navigate these complex legislative changes alone. Our team provides the expert guidance needed to bridge the gap between missed payments and legal resolution.

As an FCA-authorised independent broker with over 30 years of industry experience, we provide more than just a policy. We offer a steady hand and access to a broad network of top UK insurers to find the specific terms that fit your portfolio. Our goal is to simplify your administrative burden and provide the security you need to grow your business with confidence. Protect your professional future and ensure your monthly payments are never in doubt. Just Quote Me for expert landlord protection and experience the reliability of a partner who understands your needs. We’re ready to help you thrive in this new regulatory environment.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice

Frequently Asked Questions

Is rent guarantee insurance the same as landlord insurance?

No, these are two distinct types of protection. Standard landlord insurance focuses on the physical structure of your building and your liability as a property owner. In contrast, rent guarantee insurance with no excess specifically protects your income stream by replacing lost rent if a tenant defaults. Most professional landlords choose to hold both policies to ensure they’re covered for both property damage and the sudden loss of monthly rental payments.

Does “no excess” mean I get every penny of the missing rent back?

Yes, you’ll receive the full amount of the monthly rent owed up to the specific limits stated in your policy. While standard policies often deduct the first month’s rent as an excess, a no-excess policy ensures you don’t lose that initial income. As long as the claim falls within your monthly payout cap, which is often around £2,500, you’ll receive 100% of the arrears without any deductions or out-of-pocket costs.

Can I get rent guarantee insurance for a tenant who is already in arrears?

No, you can’t obtain cover for a tenant who is already failing to pay their rent. Insurers require that the tenancy is “clear” at the point the policy begins. If your tenant has already missed a payment, they’re considered a known risk and will be excluded from new coverage. This is why it’s vital to secure your policy at the start of a tenancy or while the tenant is fully up to date.

What legal expenses are covered under a rent protection policy?

Most policies cover a wide range of costs associated with regaining possession of your property. This typically includes solicitor fees, court filing costs, and the expenses related to professional bailiffs if they’re required. Legal cover often reaches limits between £50,000 and £100,000. These funds are essential for navigating the Section 8 process, especially as court hearings have become a mandatory requirement for most evictions in the 2026 market.

How long does it take for a rent guarantee claim to be paid?

Payouts usually begin once a full month of rent has been missed and the claim has been verified. While the initial administration can take a few weeks, most insurers aim to align their payments with your original rent due dates thereafter. Using a specialist broker can often speed up this process, as they help ensure all your documentation is correct from the first submission, reducing the chance of back and forth delays.

Do I need a new policy every time I get a new tenant?

You don’t necessarily need a brand-new policy, but you must notify your insurer and provide new referencing for the incoming tenant. Each tenant must pass the specific credit and background checks to remain eligible for rent guarantee insurance with no excess. If you fail to update the policy details or reference the new tenant correctly, your cover will be void. It’s best to treat every new tenancy as a fresh application.

Will this insurance cover my legal costs if I have to go to court?

Yes, the legal expenses portion of the policy is specifically designed to cover court-related costs. Since the abolition of Section 21 evictions, landlords must attend court hearings to secure a possession order under Section 8. Your insurance will pay for the legal representation required to present your case. This ensures you aren’t forced to pay thousands of pounds in legal fees just to regain control of your own rental property.

Can I buy rent guarantee insurance as a standalone policy?

Yes, many providers offer rent protection as a standalone product, though it’s frequently purchased as an add-on to buildings insurance. Buying it standalone gives you the flexibility to choose a specialist underwriter who offers better terms, such as a zero-excess clause. We often recommend reviewing standalone options if your current buildings provider doesn’t offer the high-limit rent protection or legal support required for the modern 2026 rental landscape.