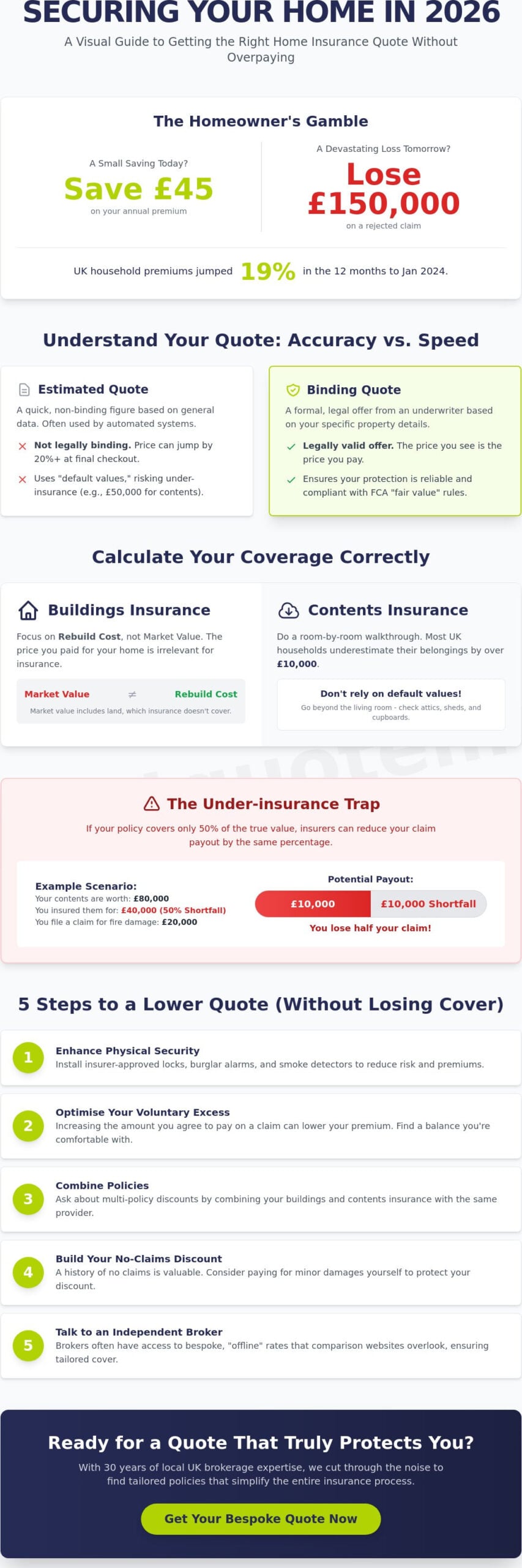

Would you rather save £45 on your annual premium today or lose £150,000 on a claim that gets rejected tomorrow? It’s a gamble many homeowners take without realising. With UK household premiums jumping 19% in the 12 months to January 2024, the search for a competitive home insurance quote has never felt more urgent. However, the lowest price often hides restrictive gaps that leave your most valuable assets at risk. We’ll show you how to secure a quote that offers genuine protection without overpaying for unnecessary extras.

You likely feel the frustration of rising costs and the headache of deciphering complex policy wording. We agree that insurance should be straightforward, not a test of your patience. This guide provides the tools to approach the 2026 market with confidence. You’ll learn the critical difference between rebuild costs and market values, how to avoid the trap of under-insuring high-value items, and how to cut through the noise of time-consuming forms to find real value.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Key Takeaways

- Understand the vital difference between estimated and binding figures to ensure your protection is legally valid and reliable.

- Learn how to accurately calculate rebuild costs and contents value to avoid the financial risks associated with under-insurance.

- Discover why independent brokers often provide access to bespoke, “offline” rates that comparison websites typically overlook.

- Identify five practical steps to lower your home insurance quote, from enhancing physical security to optimising your voluntary excess.

- Find out how 30 years of local UK brokerage expertise can help you secure a tailored policy that simplifies the entire insurance process.

Understanding Your Home Insurance Quote: Accuracy vs. Speed

In 2026, a home insurance quote is far more than a simple price tag. It acts as a sophisticated data snapshot that reflects your property’s specific risk profile against a backdrop of evolving economic factors. Many homeowners mistake an initial estimate for a final price. An estimated quote is a non-binding figure based on general data, while a binding quote is a formal legal offer from an underwriter. Accuracy at the start prevents the frustration of seeing a premium jump by 20% once you reach the final checkout page.

The Financial Conduct Authority (FCA) plays a vital role in this process. Since the implementation of the Consumer Duty in July 2023, insurers are legally required to provide “fair value” and transparent pricing. This means quotes must be clear and avoid hidden traps. However, the responsibility for providing correct details still rests with you. Understanding the foundations of coverage is the first step. For a broader look at the history and types of protection available, you might ask, What is home insurance? At its most basic level, it is a contract of indemnity designed to return your financial position to where it was before a loss occurred.

Choosing the cheapest option often feels like a win, but it frequently leads to the most expensive claims. Low-cost policies often carry high compulsory excesses or exclude essential cover like accidental damage. If a quote seems significantly lower than the market average, it usually indicates a gap in protection that you’ll only discover when it’s too late.

The Hidden Risks of “Quick” Automated Quotes

Algorithms prioritise speed, which means they often overlook specialist property details like non-standard roof materials or local subsidence history. Automated systems frequently use “default values” for contents cover, often setting them at £50,000 regardless of your actual needs. Under-insurance occurs when your policy cover limit is lower than the actual cost to rebuild your home or replace your belongings, which often results in insurers reducing claim payouts by the same percentage of the shortfall. If you’re insured for 50% of the value, they may only pay 50% of the claim.

Why 2026 is a Turning Point for UK Premiums

The insurance market in 2026 faces unique pressures. Building Cost Information Service (BCIS) data shows that material costs and labour shortages have kept rebuild prices high. Furthermore, climate trends have shifted risk assessments. In areas like Staffordshire, increased rainfall intensity has forced insurers to use more granular flood mapping for properties near the River Trent. Insurers now use real-time data-driven profiling, meaning your home insurance quote is influenced by everything from local crime statistics to your credit score. Accuracy is no longer optional; it’s the only way to ensure your policy actually works when you need it. For a comprehensive overview of how to navigate these market changes, our home insurance comparison guide for 2026 walks you through every key consideration in detail.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Calculating Your Coverage: Buildings, Contents, and Combined

Accurate data is the foundation of a reliable home insurance quote. Guesswork often leads to two outcomes: paying for cover you don’t need or, more dangerously, being underinsured when you need to claim. To get it right, you must separate your property into its structural components and the items kept inside it. Start by calculating your rebuild cost rather than your house’s market value. This ensures your home insurance quote reflects the true cost of protection without inflating premiums based on land prices.

Buildings Insurance: Rebuild Cost vs. Market Value

The price you paid for your home has nothing to do with your insurance quote. Market value includes land value and local demand, but your policy only covers the cost of bricks, mortar, and labour. According to 2024 industry data, rebuild costs can fluctuate wildly based on material availability. Listed status, thatched roofs, or specialist stone masonry significantly increase these costs because they require artisan skills. If you are a landlord protecting a rental property, you should look into residential letting insurance to ensure your specific legal and structural risks are covered.

Contents Insurance: Valuing Your World

Valuing your possessions requires a methodical room-by-room walkthrough. Open every cupboard and don’t forget the contents of your shed or loft. Most UK households underestimate their belongings by over £10,000. When calculating this figure, distinguish between “New for Old” and “Indemnity” cover. New for Old replaces a damaged five-year-old television with a brand-new equivalent. Indemnity cover only pays the current depreciated value, which could leave you short.

Pay close attention to single article limits. Most standard policies cap payouts for individual items at around £1,500 or £2,000. If you own a high-value watch or expensive bicycle, you must declare these separately. If you run a business from your spare room, your standard home policy might not cover your professional equipment or liabilities. In these cases, you might also need professional indemnity insurance to protect your livelihood.

Combining your buildings and contents insurance under one provider is often the most efficient route. Most insurers offer a discount of 10% to 15% for combined policies. This also simplifies the claims process; if a pipe bursts and damages both the floor and your rugs, you only deal with one company and pay one excess. If you’re unsure about your specific needs, our team can help you find tailored coverage that fits your property perfectly.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice

Comparison Sites vs. Independent Brokers: Choosing Your Path

Most homeowners start their search for a home insurance quote on a price comparison website. These platforms process millions of queries every year, offering speed and a broad overview of the market. They’re excellent for standard properties with no claims history. However, these sites rely on rigid algorithms. They often prioritize the lowest premium over the most robust coverage. This can lead to “under-insurance,” where you save £50 on your annual premium but find yourself thousands of pounds short during a major claim. Understanding how to effectively compare your options is essential; our detailed home insurance comparison guide explains exactly what to look for when evaluating policies side by side.

Independent brokers operate differently. We have direct lines to underwriters, allowing us to access “offline” or bespoke rates that never reach the public portals. While an algorithm treats you as a data point, a broker treats you as a client. This personal touch means we can explain the context of a risk to an insurer, often securing cover that a computer would automatically reject. We focus on the fine print so you don’t have to.

When an Algorithm Isn’t Enough

Standard insurance software struggles with “non-standard” risks. If your home has a timber frame, a flat roof covering more than 25% of the surface, or a history of subsidence, automated systems often decline the risk or inflate the price. Properties in high-risk flood zones or those with a history of frequent claims also face hurdles. Specialist knowledge is essential in these cases. For instance, the detailed risk assessment required for thatched pub insurance mirrors the care needed for thatched residential homes. We understand the specific fire safety and maintenance standards insurers demand, ensuring your home insurance quote is both accurate and valid.

The Broker Advantage for Staffordshire Residents

Local knowledge is a powerful tool in the insurance market. We understand the specific property types found in Stafford, Stone, and Newcastle-under-Lyme. Whether it’s a Victorian terrace in a former mining area or a modern build in a new development, we know which insurers have an appetite for our local geography. This insight allows us to negotiate directly with underwriters to secure better terms. Beyond the initial quote, a broker acts as your advocate. If you need to make a claim, you won’t be stuck in a generic phone queue. You’ll speak to a team that understands your policy and will fight to ensure you receive a fair settlement.

5 Steps to Lower Your Home Insurance Quote Without Losing Cover

Reducing the cost of your home insurance quote doesn’t require stripping away essential protection. By making informed adjustments to how you manage your policy and secure your property, you can see significant savings on your annual premium. Small changes in your approach to risk management often lead to the most sustainable price reductions.

Security Upgrades That Pay for Themselves

Insurers prioritize homes that present a lower risk of theft. Installing locks that meet BS3621 standards is often a baseline requirement; failing to have these can void your theft cover entirely. Beyond traditional hardware, smart home technology is changing the landscape of risk management. Devices like water leak sensors can prevent thousands of pounds in damage from burst pipes, while smart alarms provide real-time alerts to your smartphone. For those with high-value assets or unique requirements, consulting with experts in security insurance ensures your physical protections align with your policy obligations.

Refining Your Policy Details

Reviewing what you actually need helps trim unnecessary costs. Accidental damage cover is a popular add-on, but if you don’t have children or pets, the extra 15% to 25% added to your premium might not be economical. Similarly, personal possessions cover protects items like laptops or jewellery outside the home, yet you should check if these are already covered by a high-value bank account or a separate travel policy. When setting your excess, remember that your total payout deduction consists of a compulsory amount set by the insurer and a voluntary amount you choose to increase or decrease. Raising your voluntary excess usually lowers your premium, but you must ensure you can afford the combined total if you need to claim.

- Pay Annually: Paying for your cover in one lump sum is almost always cheaper than monthly instalments. Most UK insurers charge interest on monthly payments, with APRs often ranging from 11% to 19.9%, effectively turning your insurance into a high-interest loan.

- Protect Your No Claims Discount (NCD): A five-year NCD can reduce your premium by 50% or more. Paying a small fee to protect this discount is a wise investment, as it allows you to make a claim without losing the years of credit you’ve built up.

- Avoid the Auto-Renewal Trap: While the FCA introduced rules in January 2022 to prevent “price walking” (charging existing customers more than new ones), it doesn’t guarantee your renewal price is the most competitive. Always shop around 21 days before your policy expires to find the best home insurance quote.

Taking control of these variables ensures you aren’t paying for “filler” coverage while maintaining a robust safety net. If you need help identifying which discounts apply to your specific situation, you can compare options with a specialist broker.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice.

Getting Your Bespoke Quote with Just Quote Me

Securing an accurate home insurance quote shouldn’t feel like a gamble with an automated algorithm. We’ve spent 30 years building our reputation as independent brokers in Stone and Stafford, providing a human touch that comparison sites simply can’t replicate. Our local expertise means we understand the specific property risks across Staffordshire and the wider UK, from traditional builds to modern developments. We’ve spent three decades helping homeowners protect their most valuable assets by focusing on the details that matter.

Many of our clients are business owners who initially came to us for commercial cover. We’ve successfully bridged the gap between business and personal insurance, offering a streamlined experience for those who need to protect both their livelihoods and their homes. We don’t just tick boxes; we account for unique risks such as home offices, high-value equipment, or non-standard construction. Our process ensures your home insurance quote reflects the actual replacement cost and liability needs of your specific situation, rather than a generic estimate.

We’ve always prioritised comprehensive protection over finding the cheapest possible price. A cut-price policy often contains hidden exclusions that only surface when you try to make a claim. We focus on value, ensuring that if the worst happens, your policy actually performs. Our team evaluates policy wording from a broad range of insurers to find the right balance of robust coverage and competitive premiums.

A Personal Approach to Personal Insurance

We provide no-nonsense advice from UK-based experts who understand the nuances of the current market. You won’t be stuck in a loop with a chatbot. Instead, you get direct access to a broad network of top UK insurers. This personal touch is why 95% of our clients appreciate our straightforward communication. If you also run a company from home, you might find our public liability insurance guide helpful for understanding how to separate your professional and personal liabilities.

Ready to Protect Your Home?

Getting started is simple. Our online quote form is designed to be quick and efficient, asking only the essential questions needed to build your profile. Despite our digital tools, we remain deeply rooted in our Staffordshire community, operating with the same integrity we had when we started 30 years ago. You can move forward with confidence knowing we’re fully FCA-authorised and committed to your financial security. We’ll do the heavy lifting so you don’t have to.

Take Control of Your Home Protection Today

Securing the right protection for your home in 2026 requires more than a fast search. Prioritizing accuracy over speed is the only way to ensure a claim isn’t rejected when it matters most. By using RICS-standard rebuild costs and creating detailed inventory lists, you’ll avoid the common trap of underinsurance. Choosing a specialist over a generic comparison site provides access to bespoke solutions for non-standard properties that automated algorithms often miss.

Just Quote Me brings 30+ years of independent brokerage experience to your doorstep. As FCA-authorised and UK-based experts, we understand that every property is unique. We do the heavy lifting to find coverage that actually fits your life. Whether you’re looking for a reliable home insurance quote or need help with a complex property, our team is ready to assist. It’s time to trade automated guesswork for professional certainty.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Frequently Asked Questions

What information do I need to get a home insurance quote?

To get an accurate home insurance quote, you’ll need your property’s build year, construction materials, and details of all door and window locks. You should also have an estimate of your contents’ total replacement value and your claims history from the last 5 years. Providing precise details ensures your policy remains valid and protects you from potential disputes if you need to make a claim.

Is buildings insurance a legal requirement in the UK?

Buildings insurance isn’t a legal requirement in the UK, but most mortgage lenders make it a mandatory condition of your loan agreement. If you own your home outright, you aren’t legally forced to have it, though 98% of UK owner-occupiers choose to protect their property against structural damage. It’s a vital safety net that covers the cost of repairing or rebuilding your home’s physical structure.

Does my home insurance quote cover me for working from home?

Most standard policies cover clerical work from home, but you must inform your insurer if you have business visitors or hold stock on-site. According to the Association of British Insurers (ABI), pure office work rarely affects your premium. However, a tailored home insurance quote is necessary if you’ve converted a garage into a dedicated workshop or studio to ensure your equipment is fully protected.

What is the difference between rebuild cost and market value?

The rebuild cost is the amount needed to reconstruct your home from scratch, whereas the market value is what it would sell for on the open market. Rebuild costs are typically lower than market values because they don’t include the price of the land. You can use the Building Cost Information Service (BCIS) calculator to find an accurate figure for your specific property type and location.

Can I get a home insurance quote if my property has a flat roof?

You can get a quote for a flat-roofed property, but you must specify what percentage of the roof is flat. Many insurers consider a roof “flat” if its pitch is less than 10 degrees. If more than 25% of your roof is flat, you might need a specialist provider to ensure you’re covered against common issues like pooling water or structural leaks.

How much can I save by increasing my voluntary excess?

Increasing your voluntary excess from £100 to £250 can often reduce your annual premium by 10% to 15% depending on the provider. While this lowers your monthly costs, you must ensure you can afford the total excess if you claim. Your total excess is the sum of both the compulsory amount set by the insurer and your chosen voluntary amount, so check these figures carefully.

What happens if I underestimate the value of my contents?

Underestimating your contents leads to “underinsurance,” which allows insurers to reduce your payout proportionally via the “average clause.” If you insure £20,000 of goods but actually own £40,000 worth, the insurer might only pay 50% of any claim you make. Conduct a room-by-room inventory to ensure your valuation reflects the true cost of replacing everything at 2026 prices.

Does a home insurance quote include flood cover by default?

Most standard UK policies include flood cover as a default feature, though properties in high-risk zones may face higher excesses or specific exclusions. Since 2016, the Flood Re scheme has helped over 350,000 households in flood-prone areas access more affordable premiums. Always check your policy summary to confirm your level of protection against surface water, groundwater, or river flooding before you sign.

Get Your Free Business Insurance Quote now.

Request a Call back for free Expert advice