Is your motor trade insurance actually protecting your livelihood, or is it just a costly paperwork exercise that leaves you exposed to a single administrative oversight? We know that keeping up with the industry’s moving parts is a full-time job in itself. Between the 12% Insurance Premium Tax and the transition from the old MID to the new Navigate system, the legal jargon can feel designed to trip you up. It’s frustrating to face rising premiums just because you’re a new trader or you’re trying to manage a growing fleet in a complex 2026 market.

You deserve a straightforward partner who simplifies these burdens so you can focus on the workshop or the showroom. This guide will help you master the complexities of motor trade insurance by breaking down exact cover levels and the latest legal requirements. We’ll explore bespoke cost-saving strategies that help you manage rising overheads like the increased National Living Wage of £12.71 per hour. From understanding road risk to managing the Motor Insurers’ Bureau’s latest digital platforms, we’re providing the pragmatic roadmap you need to secure your business for the year ahead.

Key Takeaways

- Identify why standard business car insurance often isn’t enough for automotive professionals and how to avoid costly coverage gaps.

- Master the three pillars of motor trade insurance to ensure your road risks, liabilities, and premises are fully protected.

- Discover the legal essentials of the Road Traffic Act and your mandatory obligations under the new Navigate database system.

- Uncover practical strategies to reduce your annual premiums through effective No Claims Bonus management and risk assessment.

- Understand the benefits of choosing a local broker with regional expertise in Staffordshire for a truly bespoke policy.

What is Motor Trade Insurance and Who Actually Needs It?

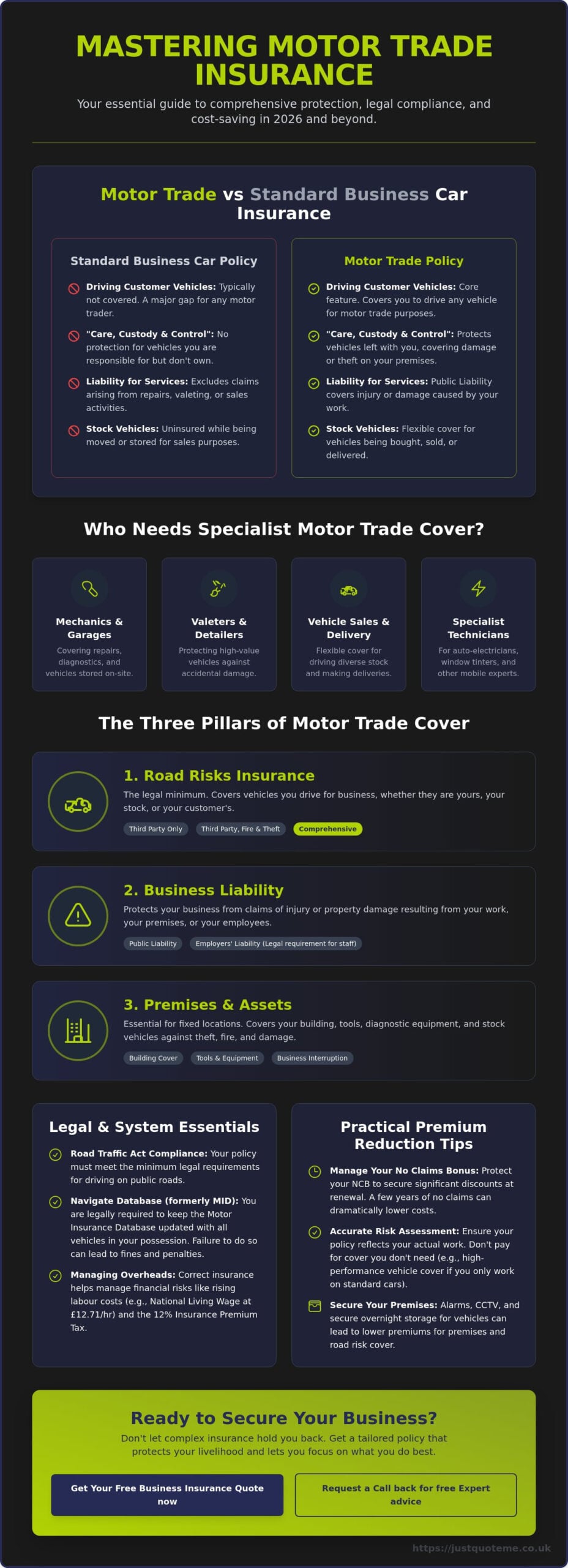

Motor trade insurance is the essential safety net for your automotive business. In 2026, this isn’t just a luxury; it’s a legal and operational necessity. Under the Road Traffic Act, you must have insurance to drive any vehicle on public roads, regardless of who owns it. If you’re moving a customer’s car from a driveway to your workshop, a personal policy won’t cover you. You need a policy that recognizes you’re handling someone else’s property for profit.

Professional motor trade insurance differs from standard vehicle insurance because it accounts for the unique risks of the automotive industry. Whether you’re a full-time dealership owner or a part-time mobile mechanic, your policy must reflect the reality of your daily operations. Standard personal policies often explicitly exclude business activities like repairs or sales. This leaves you personally liable for any accidents or damage if you don’t have the right professional cover in place. The distinction between a hobbyist and a professional is often found in the quality of their insurance.

Common Trades That Require Specialist Cover

The scope of the motor trade is broader than many realize. It’s not just about traditional garages. Common professionals who need this cover include:

- Mechanics and garages: This applies whether you operate from a fixed premises or a mobile van. You need protection for the work you perform and the vehicles in your care.

- Car valeters and detailing specialists: Handling high-value assets for cosmetic work requires protection against accidental damage or theft.

- Vehicle sales and delivery: Auction houses, independent traders, and delivery drivers need flexible cover to drive various stock vehicles.

- Auto-electricians and window tinting professionals: Specialized technicians often handle customer cars in varied environments and need liability protection.

The Legal Reality of “Care, Custody, and Control”

When a client hands you their keys, you assume “care, custody, and control” of that vehicle. This is a critical legal distinction. If a car is damaged while sitting in your garage or during a diagnostic road test, you are responsible for the loss. Motor trade insurance provides the necessary framework to handle these claims without bankrupting your business. Most policies utilize an “any driver” structure for employees, allowing your team to move vehicles efficiently. This flexibility is the backbone of a functional workshop. To protect your team and your reputation, you should also ensure you have employers liability insurance if you have any staff members, even on a casual basis.

Understanding these requirements is the first step toward a secure business. It’s about more than just a certificate; it’s about having the right level of public liability insurance to protect against third-party claims while you work. By choosing a tailored approach, you ensure that your specific trade niche is covered without paying for unnecessary extras.

The Three Pillars of Motor Trade Cover: Road Risks, Liability, and Premises

A robust motor trade insurance policy isn’t a one-size-fits-all product. It’s built on three distinct pillars that can be combined or selected individually depending on how you operate. For mobile traders, road risks might be the primary focus. For established garages, the physical premises and expensive diagnostic equipment require equal attention. Building your policy modularly ensures you only pay for the protection your specific business model requires.

Road Risks: Third Party vs. Comprehensive

This is the foundational element required for anyone driving vehicles they don’t own. You have three main choices. Third Party Only is the minimum legal requirement, covering damage to others but leaving your stock or customer cars unprotected. Third Party, Fire and Theft adds a layer of security against those specific risks. Comprehensive cover is the gold standard, protecting vehicles in your care even if an accident is your fault. When selecting a level, check your indemnity limits carefully. If you regularly handle high-end EVs or performance cars, a standard limit might not be enough to cover a total loss in a high-value claim.

Business Liability: Public and Employers Liability

Liability cover protects you from the financial fallout of accidents involving people rather than just metal. Public liability insurance is vital if customers visit your site or if you work on-site at their homes. It covers injury or property damage caused by your business activities. If you have any employees, including part-time or casual staff, employers liability insurance is a legal mandate. This ensures you’re covered if a staff member is injured while working. You should also consider sales and service indemnity. This protects you if a customer claims your workmanship was faulty after they’ve left the garage. These aren’t just suggestions; they are core legal insurance requirements that keep your professional reputation intact.

Combined Motor Trade: Protecting the Workshop

For those with a fixed location, a combined policy brings everything under one roof. This includes cover for your buildings and specialized equipment through plant and machinery insurance. If you’re a mobile technician, your livelihood depends on your kit, making van and tools insurance a non-negotiable addition. We also recommend business interruption cover. This provides a financial cushion if a fire or flood forces your garage to close temporarily. If you aren’t sure which combination fits your specific trade, it’s worth speaking with a specialist advisor to build a modular plan that doesn’t waste your budget on unnecessary extras. This pragmatic approach allows you to scale your motor trade insurance as your business grows.

Motor Trade Insurance vs. Standard Business Car Insurance: A Critical Comparison

Many entrepreneurs starting out in the automotive world mistakenly assume that adding “business use” to a personal policy is enough. This confusion often stems from search queries like “business insurance car” which lead to products designed for office workers or sales reps rather than mechanics or dealers. While both products involve driving for work, they serve entirely different legal and operational purposes. Understanding this critical comparison is the only way to ensure your policy isn’t voided the moment you file a claim.

The fundamental trigger for needing motor trade insurance is the profit motive. Standard business car insurance is an extension of a personal policy. It allows you to drive your own vehicle to different sites or meetings. It doesn’t, however, cover you for handling, repairing, or selling vehicles that belong to other people or your business stock. If you’re using a personal policy to conduct trade activities, you’re likely driving uninsured in the eyes of the law. This can lead to heavy fines, seized vehicles, and a permanent black mark on your insurance history.

When Business Car Insurance is Sufficient

There are specific scenarios where a standard policy with business use is all you need. These typically involve professionals who don’t touch the mechanics or ownership of a vehicle as part of their service. You’re likely safe with standard cover if you are:

- A consultant or sales representative traveling between multiple fixed work sites.

- A professional using your own car to attend meetings or visit clients.

- An occasional business user in a non-automotive trade, such as a florist or an accountant.

When You Must Switch to Motor Trade Insurance

If your business involves “care, custody, and control” of vehicles that aren’t your personal daily driver, you’ve crossed into the motor trade. This transition is mandatory for anyone buying and selling vehicles for profit, even if you’re operating as a “driveway trader” from home. You also need this specialist cover if you collect or deliver customer cars for servicing, as a standard policy won’t protect the customer’s asset while you’re behind the wheel.

Operating a repair, recovery, or valeting business also requires this professional level of protection. As your business scales from a solo operation to a larger garage, you’ll also need to integrate other protections like employers liability insurance to cover your team. Don’t wait for a rejected claim to realize you’ve outgrown your personal policy. Making the switch ensures that your livelihood is protected by a policy designed for the risks you actually face every day.

How to Secure the Best Rates and Manage Your MID Duties

Securing competitive rates for your motor trade insurance in 2026 requires a proactive approach to risk management. Insurance premiums have remained high due to the increased complexity of vehicle repairs and the standard 12% Insurance Premium Tax (IPT). Underwriters prioritize traders who can demonstrate stability and a clear history of safety. This means your No Claims Bonus (NCB) is your most valuable asset. If you’re transitioning from a personal policy to a professional one, some specialist brokers can mirror your personal NCB to help reduce your initial trade premium.

Physical security also plays a massive role in how an insurer views your business. Installing Thatcham-approved trackers on stock vehicles or upgrading your workshop’s CCTV and perimeter fencing can lead to direct discounts. Avoid the common pitfall of “fronting,” where a more experienced driver is named as the lead on a policy actually used by a younger or higher-risk trader. This is considered insurance fraud. It will lead to your policy being cancelled, making it nearly impossible to secure affordable cover in the future.

Mastering the Motor Insurance Database (Navigate)

In April 2024, the Motor Insurance Database (MID) was replaced by a more streamlined system called “Navigate.” Despite the system update, your legal obligations remain strict. You must register any vehicle in your possession for more than 14 days on this database. This includes trade plates and all stock vehicles intended for sale or repair. Failing to do so doesn’t just risk a fine; it makes the vehicle appear uninsured to police Automatic Number Plate Recognition (ANPR) cameras, which can lead to immediate roadside seizure.

Managing Navigate effectively is about administrative consistency. We recommend a weekly audit of your stock list to ensure every vehicle is accounted for. This digital record is the primary tool used by the Motor Insurers’ Bureau (MIB) to enforce the UK’s common framework for motor insurance. Accurate reporting protects you from unnecessary police stops and ensures your claims process remains smooth if an incident occurs. If you’re managing multiple vehicles, you might find motor fleet insurance a more efficient way to handle your database duties.

Cost-Saving Strategies for New and Part-Time Traders

If you’re just starting out or running a part-time operation from home, you can lower your costs by being selective with your policy terms. Restricting your driver list to individuals over the age of 25 with at least two years of driving experience is one of the fastest ways to drop your premium. While “any driver” policies offer convenience, they carry the highest risk profile for insurers.

Choosing a higher voluntary excess can also make your annual payments more manageable. However, you must ensure you have the cash reserves to cover this excess if you need to claim. Be honest about your projected turnover and the total value of the vehicles you handle. Overestimating these figures leads to unnecessarily high premiums, while underestimating them could result in a “pro-rata” reduction of any claim payout. To find a policy that balances these factors perfectly, you can compare motor trade insurance options with our expert team today.

Finding Bespoke Motor Trade Solutions in Staffordshire and the West Midlands

Choosing motor trade insurance shouldn’t feel like a gamble with an algorithm. While automated aggregators offer speed, they often lack the depth required for complex automotive businesses in 2026. A specialist independent broker understands that a mobile mechanic in Stone has different risks than a large dealership in the center of Stafford. By leveraging a human-centric approach, we move beyond generic data points to build a policy that reflects your actual daily operations. We act as a steady hand in a complex market, managing the administrative weight so you can focus on your customers.

Working with an independent broker gives you access to a broad network of UK underwriters. This competition is vital for securing competitive pricing, especially as repair costs and parts availability continue to fluctuate. We don’t just provide a certificate; we provide a partnership. This means we’re here to help when you need to update your Navigate records or when you’re considering expanding your fleet. Our goal is to simplify the insurance process, making it a frictionless part of your business growth rather than a hurdle.

Local Knowledge for Staffordshire Businesses

Staffordshire businesses benefit from regional expertise that national providers simply can’t match. We provide tailored advice for builders and tradesmen who manage diverse vehicle fleets alongside their primary trade. Whether you need face-to-face support in Newcastle-under-Lyme or specific guidance on how local trade patterns affect your premium, our team is on the ground. We understand how regional crime data impacts your risk profile, and we use that knowledge to present your business to underwriters in the best possible light.

Get Your Bespoke Quote Today

The process of securing your cover should be direct and efficient. We’ve refined our system to move you quickly from an initial inquiry to a fully active policy. In a market where motor trade insurance premiums saw significant increases in 2025, having a partner who knows where to find value is essential. We look at the specifics of your experience, your security measures, and your business goals to ensure you aren’t overpaying for generic cover. Take the first step toward a more secure automotive business by connecting with our expert team for a personalized assessment.

Securing Your Automotive Future in 2026

Protecting your automotive business requires more than just a basic policy; it demands a strategic understanding of your legal obligations and risk profile. You now know the critical distinction between standard business car insurance and professional motor trade insurance. By mastering your Navigate database duties and choosing a modular approach to road risks and liability, you ensure your livelihood remains secure against rising industry costs. Whether you’re a mobile mechanic or a large dealership, staying compliant is the only way to avoid the pitfalls of voided cover.

Just Quote Me brings over 30 years of industry experience to your side. As an FCA-authorised independent broker, we provide access to a broad network of top UK insurers, ensuring you receive a policy tailored to your specific trade niche. We move beyond automated systems to offer the pragmatic, human-centric advice that Staffordshire and West Midlands businesses rely on. Don’t leave your workshop’s future to chance when you can partner with a steady hand to manage your administrative burdens. We’re ready to help you drive your business forward with confidence.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Frequently Asked Questions

Can I drive any car with a motor trade insurance policy?

A motor trade insurance policy doesn’t grant you permission to drive every vehicle on the road. It covers vehicles owned by your business or those in your care for trade purposes, such as customer repairs or stock for sale. You must specifically list your personal vehicles on the policy if you intend to drive them for non-business reasons. Always check your schedule to confirm your specific indemnity limits.

What is the minimum age for a motor trade insurance policy in 2026?

Most insurers set the minimum age at 21, though you’ll find much better rates once you reach 25. Younger traders often face higher premiums and stricter restrictions on the engine size or vehicle value they can drive. If you’re under 25, you might need to provide more evidence of your trade experience to secure a professional motor trade insurance policy.

Do I need motor trade insurance if I only work on cars part-time?

You definitely need a specialist policy if you handle customer vehicles for profit, regardless of how many hours you work. Standard personal insurance doesn’t cover any activity related to the motor trade. Operating without the correct cover, even as a part-time mobile mechanic, leaves you legally exposed and risks your personal policy being voided if an accident occurs during business activities.

How do I add or remove vehicles from the Motor Insurance Database (MID)?

You manage your vehicle records through the “Navigate” portal, which is the current platform for the Motor Insurance Database. You’re legally required to add any vehicle you hold for more than 14 days. This includes trade plates and stock. Keeping this updated ensures that police ANPR cameras recognize the vehicle as insured, preventing unnecessary stops and potential vehicle seizures.

Does motor trade insurance cover my personal tools and equipment?

Standard road risks policies don’t cover your personal tools or diagnostic equipment by default. To protect these assets, you must add specific “van and tools” or “premises and machinery” cover to your plan. This is essential for mobile mechanics whose livelihood depends on expensive kits that are frequently at risk of theft or damage while on location.

What happens if I drive a customer vehicle without motor trade insurance?

Driving a customer’s vehicle without the correct cover means you’re driving uninsured. This is a serious legal offense that results in fixed penalty fines, six points on your license, and the immediate seizure of the vehicle by the police. Beyond the legal penalties, you’ll be personally liable for any damage caused to the customer’s car or third-party property.

Is public liability included in a standard road risks policy?

Public liability isn’t included in a basic road risks policy. Road risks cover only allows you to drive vehicles on public highways. To protect against claims of injury or property damage occurring at your place of work or a customer’s home, you must add public liability as a separate component. Most professional traders combine these for comprehensive protection.

Can I use my motor trade policy for social, domestic, and pleasure use?

You can use your trade policy for personal trips if you have specifically added “social, domestic, and pleasure” (SD&P) use to your cover. Not all motor trade insurance policies include this automatically. If it’s not listed on your certificate, you’re only covered for business-related driving. It’s vital to confirm this extension if you plan to use a stock vehicle for personal errands.