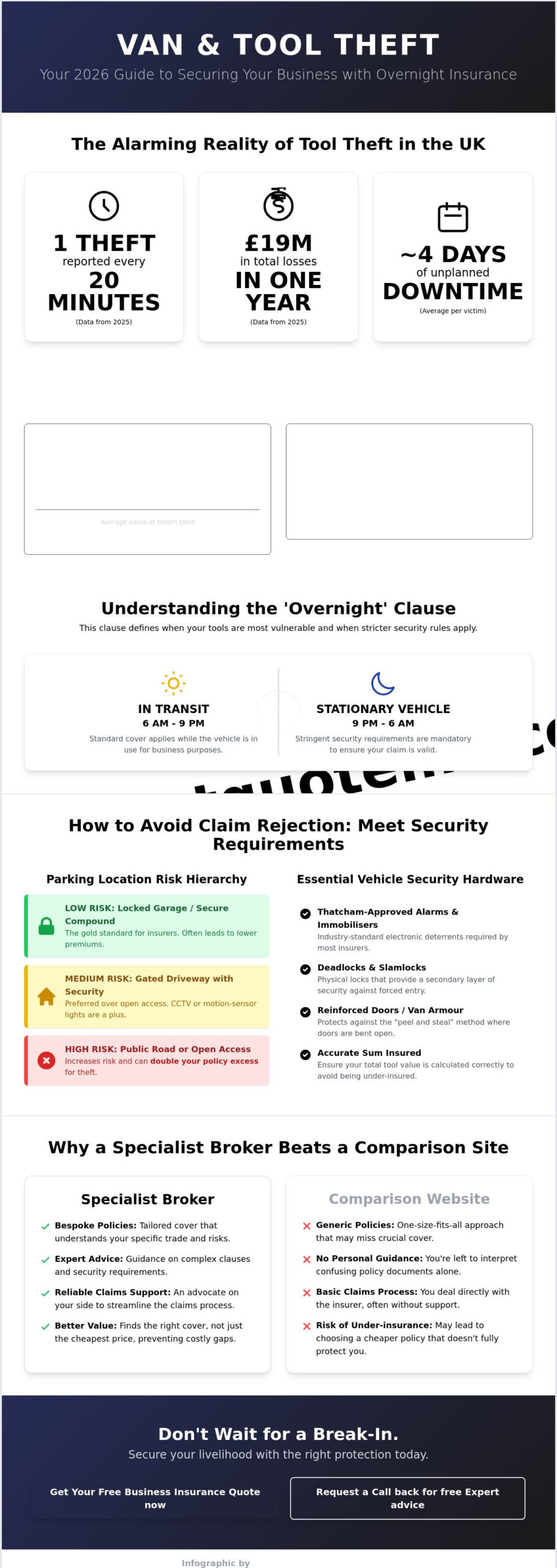

In 2025, a tool theft was reported every 20 minutes across the UK, contributing to a staggering £19 million in total losses for the year. For most professionals, your van isn’t just a vehicle; it’s a mobile workshop and the backbone of your livelihood. You likely already know that the rising cost of power tools makes you a target, and the fear of a break-in is a constant weight on your mind. Securing the right tradesman insurance for tools in van overnight is the only way to protect your business from the four days of average downtime that follows a theft.

We understand that insurance jargon and complex overnight exclusion clauses often feel designed to prevent a payout. You deserve total clarity on what your policy requires to remain valid. This 2026 guide explains how to meet strict security standards, ensure your tools are covered 24/7, and streamline the claims process. We’ll walk you through the essential steps to guarantee that your insurance works for you, allowing you to focus on your trade with the confidence that your equipment is fully protected.

Key Takeaways

- Understand the specific timeframes defined in the “overnight” clause to ensure your tools remain protected between 9 PM and 6 AM.

- Identify the exact security hardware, such as Thatcham-approved alarms and deadlocks, required to satisfy insurer conditions and guarantee a payout.

- Learn how to accurately calculate your sum insured for tradesman insurance for tools in van overnight to avoid the high costs of under-insurance.

- Discover the critical differences between “In Transit” and “Stationary Vehicle” cover to ensure your livelihood is protected 24/7.

- See why a specialist broker provides a more reliable claims experience and better policy customization than a generic comparison website.

The Reality of Tool Theft in the UK (2026): Why Overnight Cover is Essential

The reality of operating a trade business in 2026 is that tool theft has become a persistent threat rather than a rare occurrence. Data from 2025 reveals that a tool theft was reported every 20 minutes across the UK, resulting in over 30,000 recorded offenses. For tradespeople working in Staffordshire and the West Midlands, the risks are particularly concentrated. Urban centres like Birmingham, Wolverhampton, and Stoke-on-Trent remain hotspots for van-related crime as thieves target the high-value equipment essential for local construction and renovation projects. Relying on standard van insurance often leaves you vulnerable; these policies typically focus on the vehicle itself rather than the professional equipment inside.

By understanding property insurance principles, it becomes evident that specialized protection is necessary for mobile business assets. A standard motor policy rarely accounts for the full replacement value of a professional kit. This is where tradesman insurance for tools in van overnight becomes a critical safety net. It bridges the gap between vehicle protection and business continuity, ensuring that a single night of criminal activity doesn’t end your career.

The “Peel and Steal” Epidemic

Thieves in 2026 continue to use the “peel and steal” method, a technique where the side or rear doors of a van are physically forced and folded down to bypass factory locks. Older van models are at a higher risk because they lack the structural reinforcements found in newer, security-focused designs. There’s also been a noticeable shift toward targeting high-value cordless battery systems. These items are compact, expensive, and easily resold, making them a primary target for organized theft rings operating under the cover of darkness.

Calculating the True Cost of Stolen Tools

The financial impact of a break-in extends far beyond the price of a replacement drill. While the average value of stolen tools per incident reached £1,300 in 2025, the total bill for your business is often much higher. You must account for both direct and indirect expenses to understand the full scale of the risk.

- Direct costs: Replacement of power tools, hand tools, and specialized diagnostic equipment, plus the cost of repairing van damage.

- Indirect costs: Contract penalties for missed deadlines, the daily expense of hiring temporary equipment, and the long-term impact of increased insurance premiums.

The majority of victims face a significant disruption to their livelihood, as the average tool theft victim was forced to take 3.97 days of unplanned downtime in 2024.

Understanding the ‘Overnight’ Clause: What Counts as Secure?

The “overnight” clause is often where claims succeed or fail. In the world of tradesman insurance for tools in van overnight, this term doesn’t just describe a time of day; it’s a specific contractual window, usually between 9 PM and 6 AM. During these hours, your tools transition from being “In Transit” to being in a “Stationary Vehicle.” This distinction is vital because the security requirements for a stationary van are significantly more stringent. If a theft occurs during this period, your insurer will look for proof that you met the specific storage conditions outlined in your policy documents.

Insurers categorize parking locations based on a clear hierarchy of risk. A locked, private garage is the gold standard and often results in lower premiums or more favorable terms. Gated driveways with motion-sensor lighting provide a secondary layer of protection that many underwriters prefer over open access. Conversely, parking on a public road is viewed as high risk. Many policies include a “100-metre rule,” which requires the vehicle to be parked within a certain distance of your home or temporary lodging. If you’re working away and staying at a hotel, you must ensure the parking area meets the policy’s criteria, or you might find your cover is void.

Parking Requirements and Your Premium

Choosing to park on a public road doesn’t just increase the likelihood of a break-in; it can also double your policy excess for overnight theft. Insurers reward proactive security. Utilizing a driveway with visible Police-approved van security measures, such as CCTV or perimeter lighting, strengthens your position during a claim. If you’re unsure if your current parking setup meets the grade, it’s a good idea to review your business insurance options with a specialist.

The Definition of “Locked and Secured”

In the eyes of an insurer, “locked” often goes beyond simply pressing a button on your key fob. Many modern policies require secondary security measures to be active for a claim to be valid. This might include high-security deadlocks or internal tool vaults bolted to the chassis. A vehicle must be forcibly entered for most theft claims to be considered, meaning there must be clear physical evidence of a break-in, such as a smashed window or a damaged lock. Relying solely on factory-fitted central locking is rarely enough for high-value tool cover in 2026. Internal bulkheads also play a role by preventing thieves from accessing the cargo area through the cab, providing an extra layer of defense that underwriters value.

Security Requirements to Avoid Claim Rejection

Securing a policy for tradesman insurance for tools in van overnight is only the first step. To ensure a claim is actually paid out, you must adhere to the specific hardware standards dictated by your underwriter. Most insurers view Thatcham-approved alarms and immobilisers as the industry gold standard. These systems undergo rigorous testing to ensure they can withstand sophisticated theft attempts. If your van only relies on a factory-fitted alarm that isn’t Thatcham Category 1 or 2 certified, you might find your theft cover is restricted or completely invalid.

Visible deterrents play a role, but stickers claiming “no tools left in this vehicle” aren’t enough to satisfy a claims adjuster. Professional thieves often ignore these signs, knowing that many tradespeople find it impractical to unload heavy kit every evening. Instead, underwriters look for physical proof of security. This includes high-quality locks and internal storage solutions that provide a secondary layer of defense. While protecting your physical assets is vital, it’s also worth ensuring your broader business is secure. For example, Public Liability Insurance works alongside your tool cover to protect you from the financial consequences of accidents or injuries that occur once you’re back on the tools.

Essential Hardware Upgrades for 2026

The choice between deadlocks and slamlocks is a common point of confusion. Slamlocks are designed for multi-drop couriers and engage automatically when the door shuts. However, for overnight protection, most insurers specifically require external deadlocks. These require a manual turn of a key, making them much harder to bypass via electronic hacking or the “peel and steal” methods discussed earlier. Internal tool chests bolted to the vehicle floor provide an additional barrier. Even if a thief breaches the van, they face a second, time-consuming challenge to access your high-value cordless systems.

Smart security is also becoming a standard requirement for high-sum insured policies. Electronic tool tracking using professional GPS units or even consumer-grade devices like Apple AirTags can aid in recovery. Some modern policies may even offer premium discounts if you integrate van-integrated CCTV that uploads footage to the cloud in real-time.

Evidence Needed After a Break-In

If the worst happens, the quality of your evidence determines the speed of your payout. An adjuster’s first request will almost always be for clear photos of the forced entry. You need to show exactly how the security was bypassed. It’s also mandatory to report the theft to the police within 24 hours. A crime reference number is an absolute requirement for any claim involving criminal activity. Without this official record, most insurers will refuse to process the file, regardless of the security measures you had in place.

How to Choose the Right Level of Tool Cover

Selecting the right level of protection is just as critical as the physical locks on your van doors. Many professionals fall into the trap of under-insuring their assets to save on monthly premiums, but this often leads to significant financial shortfalls during a claim. When arranging tradesman insurance for tools in van overnight, you must set an accurate “Sum Insured” that reflects the total replacement cost of your kit. If you claim for £5,000 worth of stolen tools but your total inventory is actually worth £10,000, an insurer may apply the “condition of average,” potentially halving your payout because you were only 50% insured.

You also need to distinguish between owned tools and hired-in plant. Standard tool policies generally cover items you own personally or through your business. However, if you frequently rent specialized machinery or larger equipment for specific jobs, these assets usually require different handling. For comprehensive protection on larger projects involving rented kit, you might consider Contractors All Risk Insurance to bridge the gap between your personal tools and project-specific machinery.

Calculating Your Total Tool Value

When calculating your total value, you’ll need to choose between “New for Old” and “Indemnity” cover. New for Old is the preferred choice for most, as it pays out the cost of a brand-new equivalent regardless of the age of your stolen gear. Indemnity cover, or market value, accounts for depreciation, meaning you’ll receive less for a three-year-old combi drill than you originally paid. Don’t forget the “small stuff” during this calculation. While a single screwdriver isn’t expensive, a full set of hand tools, high-quality drill bits, and consumables can easily total thousands of pounds.

The Importance of Itemised Receipts

A vague description like “box of tools” is a primary reason for claim delays or lower payouts. Insurers require specific evidence to verify your loss. Digital inventory management is the most efficient way to handle this. Use your smartphone to take photos of serial numbers and store digital copies of your receipts in the cloud. This ensures you have instant access to proof of ownership even if your physical records are lost or damaged. If you’ve purchased tools second-hand or lack VAT receipts, keep detailed photographic evidence of the tools in your possession and records of their current market value.

Specialized diagnostic kit or high-end surveying equipment often exceeds standard single-item limits, which can be as low as £500. If you carry expensive tech, you must declare these items specifically to ensure they aren’t capped during a claim. To get a policy tailored to your specific inventory, you can request a personalized insurance review from our team today.

Why a Bespoke Broker is Better than a Comparison Site

Algorithms and automated comparison sites are built for speed, but they often lack the nuance required to secure effective tradesman insurance for tools in van overnight. When you use a generic search engine to find cover, you’re essentially being grouped into a broad risk category that doesn’t account for the specifics of your business or your location. An independent broker provides a human element that’s invaluable during the application process and even more critical when you need to make a claim. We don’t just sell you a policy; we act as a partner who understands that your tools are the lifeblood of your career.

Our team understands the regional crime trends affecting Staffordshire and the West Midlands. We know that a tradesperson operating in urban centres like Birmingham or Wolverhampton faces different challenges than someone based in more rural areas. By leveraging this local expertise, we can point you toward specialist underwriters who actually understand the “van life” of a tradesman. This specialized knowledge ensures that your policy isn’t just a piece of paper, but a robust legal agreement designed to protect you when things go wrong.

Tailored Policies for Specific Trades

Every trade has a unique risk profile. A plumber’s kit, filled with expensive diagnostic tech and specialized pressing tools, requires a different approach than a landscaper who might be more concerned about hired-in plant or heavy machinery. As your business grows and you add more vans or employees to your fleet, your insurance needs to evolve with you. We help you adjust your cover levels dynamically, ensuring you’re never paying for protection you don’t need or leaving yourself exposed. This customized approach is why many professionals view Tradesman Insurance as a holistic shield for their entire operation, rather than just a mandatory expense.

The Just Quote Me Advantage

With over 30 years of experience navigating UK insurance law, Just Quote Me provides the reliability that automated systems simply can’t match. We offer direct access to expert advice for professionals in Stone, Stafford, and Newcastle-under-Lyme, giving you a local point of contact who knows your area. Just Quote Me acts as a steady hand in a complex insurance market, managing the administrative burdens and fine-print negotiations so you can stay on the tools and focus on your work. We handle the paperwork and the difficult conversations with underwriters, ensuring that if you do experience a break-in, the claims process is as fast and frictionless as possible.

Securing Your Tools and Your Future

Protecting your livelihood in 2026 requires a proactive approach that blends physical security with precise policy compliance. As we’ve explored, ensuring your van meets Thatcham standards and maintaining a rigorous digital inventory are the most effective ways to guarantee your claim is settled without delay. By respecting the specific time and distance requirements of the overnight clause, you turn your insurance from a basic requirement into a robust safety net for your professional kit. Don’t let the threat of theft disrupt your business or your peace of mind.

Finding the right tradesman insurance for tools in van overnight is a straightforward process when you have the right partner. With over 30 years of experience and access to a broad network of top UK insurers, Just Quote Me provides the FCA-authorised expert advice needed to navigate this complex market. We act as a steady hand, managing the administrative burdens so you can stay on the tools and focus on your work. Take the next step in securing your professional future today.

Get Your Free Business Insurance Quote now

Frequently Asked Questions

Is tool insurance valid if my van is parked on the street overnight?

Street parking is generally permitted, provided you meet the specific security conditions and “distance from home” rules outlined in your policy schedule. While off-street parking is preferred, most tradesman insurance for tools in van overnight options cover public roads if the vehicle is locked and within the required 100-metre radius of your home. You should check your specific terms for any “garage requirement” that might apply to high-value kits.

What is the maximum value of tools I can insure in a single van?

Coverage levels typically range from £1,000 to £10,000 depending on the specific provider and your business requirements. It is vital to set an accurate “sum insured” that reflects the total replacement cost of your kit to avoid the “condition of average” during a claim settlement. If your professional equipment exceeds these standard limits, specialist underwriters can often arrange higher levels of protection.

Does my insurance cover tools stolen from a hired van?

Many professional policies extend cover to tools stored in a hired van, provided you notify your broker of the temporary vehicle change. The same security standards, such as ensuring the vehicle is locked and forcibly entered, will apply to the rental. You should verify that your policy includes “hired-in plant” or temporary vehicle clauses before leaving your professional equipment in a van you do not own.

Do I need to have specific locks fitted to my van for the insurance to be valid?

Insurers typically require more than just factory-fitted locks; many mandate Thatcham-approved deadlocks for a policy to remain valid. These manual locks are harder to bypass than electronic systems and provide the physical proof of forced entry necessary for a successful claim. Always check your policy wording to see if specific hardware upgrades are a condition of your cover.

Will my tools be covered if they are stolen while I am working on-site?

Your tools are generally covered while on-site, provided the vehicle remains locked and secured whenever you are away from it. Theft from a building or the site itself usually requires a different type of cover, such as a site-specific extension or contractors all risks insurance. For the van-based portion of your work, ensuring the alarm is active and doors are deadlocked is essential for maintaining your protection.

What is the difference between “new for old” and “wear and tear” tool cover?

“New for old” cover provides a payout equivalent to the cost of a brand-new replacement for your stolen item, regardless of its age. “Wear and tear,” or indemnity cover, accounts for depreciation and pays only the current market value of the used tool. Choosing a new-for-old policy ensures you aren’t left out of pocket when you need to replace a three-year-old power tool with a modern equivalent.

Can I get insurance for tools left in my van if I don’t have a garage?

You can certainly obtain cover without a garage by declaring your actual parking arrangements, such as a private driveway or a public road, during the quote process. Insurers will evaluate the risk based on your location and may require additional hardware like internal vaults to compensate for the lack of a garage. Having the right tradesman insurance for tools in van overnight ensures you are protected regardless of your storage facilities, provided you follow the agreed security protocols.

How long does it typically take to settle a tool insurance claim?

Most straightforward tool insurance claims are settled within five to ten working days once all evidence is submitted. This speed relies on you providing a crime reference number and proof of ownership immediately. Just Quote Me manages the communication with underwriters to ensure your settlement is processed as efficiently as possible, helping you return to work without unnecessary delays.