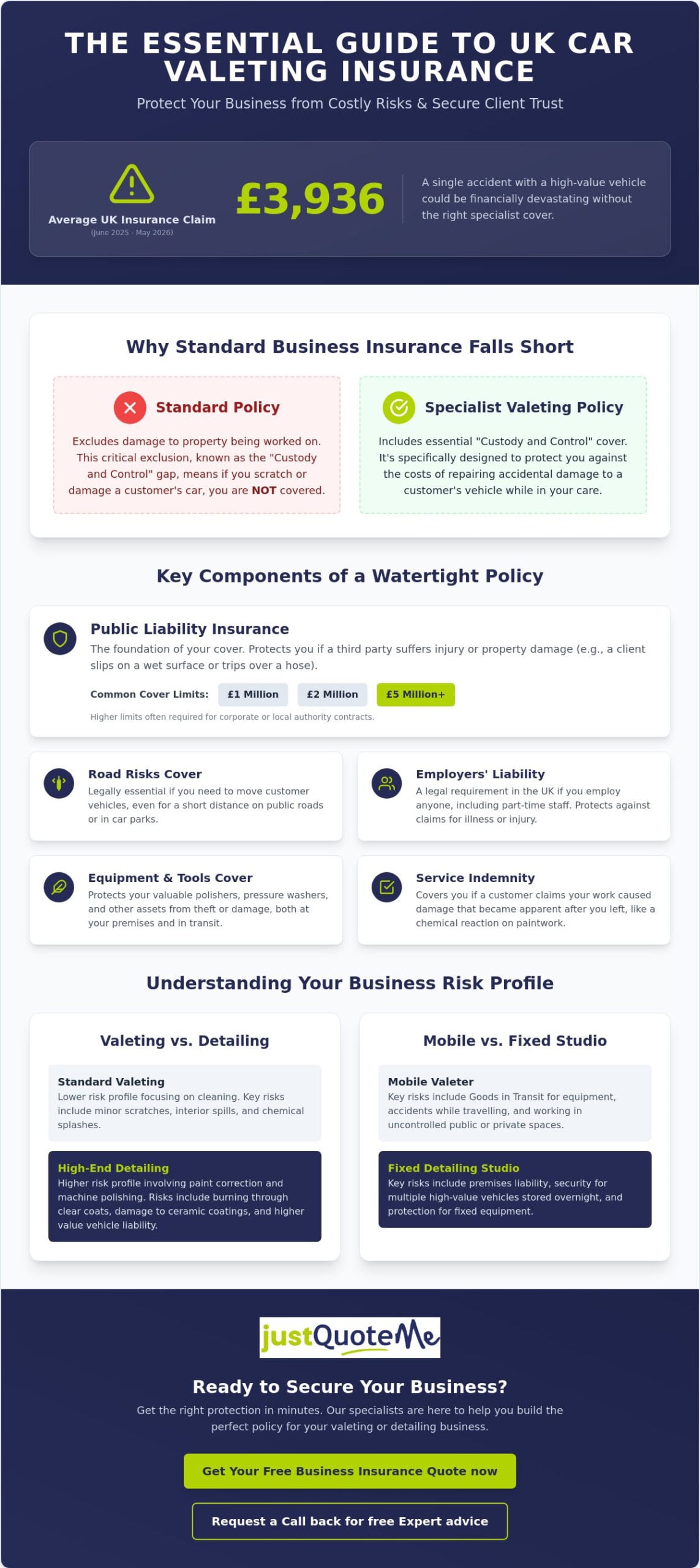

Did you know the average insurance claim for a UK car valeter reached £3,936 between June 2025 and May 2026? For many specialists, the line between a profitable week and a devastating financial loss is often just a single accidental scratch on a bespoke ceramic coating—which might require professional mobile car scratch repair UK—or a spill on a luxury interior. It’s understandable why there’s so much confusion when choosing a valeting business insurance policy, especially when you’re trying to distinguish between standard public liability and essential road risks. You want to focus on the finish, not the paperwork, but you can’t ignore the legalities of the 2026 market.

We’re here to simplify that process and provide the clarity you need to protect your reputation. This guide explains how to build a bespoke policy that satisfies high-end clients and keeps you compliant with UK employment laws. We’ll break down the nuances of mobile setup premiums and explain exactly how to gain peace of mind while driving customer vehicles. From understanding new Euro 7 standards to managing the risks of high-value detailing, we’ll give you a clear roadmap to securing comprehensive cover that works as hard as you do.

Key Takeaways

- Understand why a standard commercial policy falls short and how a specialist valeting business insurance policy provides essential “Custody and Control” protection for vehicles in your care.

- Distinguish between Public Liability and Road Risks cover to ensure you are legally and financially protected while moving customer cars on public roads or within parking areas.

- Learn how to safeguard your professional assets, including high-end polishers and pressure washers, through specialized equipment and “Goods in Transit” coverage.

- Identify the specific risk profiles for mobile setups versus fixed detailing studios, from weather-related damage to premises liability and high-value vehicle storage.

- Discover how to streamline the quoting process by preparing key business data that helps specialist brokers secure the most accurate and efficient cover for your needs.

What is Valeting Business Insurance and Why is it Essential?

A valeting business insurance policy acts as more than just a safety net; it’s a professional credential that separates industry specialists from casual operators. In 2026, the UK car cleaning market has expanded significantly, with drivers spending over £600 million on on-demand services. This growth has led to increased customer scrutiny. Clients now frequently ask for proof of cover before handing over their keys. A standard business policy is usually insufficient because it rarely accounts for the “Custody and Control” of third-party vehicles. If you’re handling someone else’s car, you need a policy that understands the specific liabilities involved in automotive care.

The 2026 market is defined by a rise in mobile valeters, many of whom operate without formal accreditation or proper protection. By securing a comprehensive valeting business insurance policy, you position yourself as a reliable professional. This is especially vital as customer expectations rise and the average claim for car valeters has reached nearly £4,000. Without specialized cover, a single mistake during a routine clean could result in a financial burden that ends your business. Proper insurance manages these complex administrative and financial risks so you can focus on delivering a flawless finish.

The Core Difference Between Valeting and Detailing Insurance

The transition from basic valeting to high-end detailing significantly shifts your risk profile. Detailing often involves paint correction and machine polishing, processes that carry a much higher chance of accidental damage than a simple wash and wax. If you burn through a clear coat with a rotary polisher, the repair costs are substantial. Detailing studios also require higher indemnity limits because they often house multiple high-value vehicles simultaneously. It’s vital to verify that your policy covers chemical damage to specialized ceramic coatings. Many generic providers exclude “damage to the item being worked on,” which is a catastrophic gap for a professional detailer who needs to protect their workmanship.

Public Liability: The Foundation of Your Policy

Public liability is the bedrock of your protection. It covers you if a third party suffers injury or property damage due to your business activities. In a valeting context, this could be a pedestrian tripping over your pressure washer hose or a client slipping on a soapy driveway. To understand the broader legal framework of these protections, you can read more about What is Liability Insurance? and how it functions as a transfer of risk. Most UK providers offer standard limits of £1 million, £2 million, or £5 million. Choosing the right level depends on your specific client base. High-end corporate contracts or local authority work often mandate a minimum of £5 million in public liability insurance to even step onto their premises.

Key Components of a Valeting Insurance Policy

Building a valeting business insurance policy requires a modular approach. You can’t rely on a one size fits all document because your daily risks are unique to the motor trade. While public liability covers your interaction with the public, it doesn’t address the vehicle itself or your legal duties as an employer. You need to ensure your policy includes specific protections that trigger the moment you take possession of a customer’s keys. This prevents gaps that could leave you personally liable for expensive repairs.

If your business employs even one person, perhaps a casual assistant for busy weekends, you must meet the legal requirement for employers’ liability insurance. This isn’t optional. Failing to have this cover in place can result in significant daily fines from the Health and Safety Executive. Beyond legal mandates, you should also consider service indemnity. This component protects you if a customer claims your work caused damage that only became apparent after you finished the job, such as a localized paint reaction or a mechanical issue caused by engine bay cleaning.

Understanding Custody and Control

This is where most standard business insurance fails the valeting sector. Most general liability policies exclude damage to the property you are actually working on. If you drop a bottle of heavy duty degreaser on a customer’s driveway, your public liability covers the driveway repair. However, if that same chemical spills inside a vehicle and ruins a leather seat, only a Custody and Control clause will pay for the interior restoration. Custody and Control is the specific protection for the vehicle under your care, ensuring you aren’t personally liable for accidental damage to a client’s asset.

Road Risks for Valeters

Mobile valeters often move cars to access better lighting or to clear space for equipment. Even if you’re only moving a car five yards on a private driveway, you’re technically in charge of that vehicle. If you’re driving customer cars on public roads to reach a studio, road risks cover is mandatory. You can choose between Third Party Only or Comprehensive cover. For those with a growing team, motor trade insurance or fleet options are often more efficient than individual policies. It’s a pragmatic way to keep your business moving without the administrative headache of managing separate drivers. You can explore tailored insurance packages that consolidate these risks into a single, manageable monthly cost.

Protecting Your Assets: Equipment and Van Insurance

Your equipment is the lifeblood of your daily operation. Modern valeting gear, ranging from high-pressure washers and steam cleaners to specialized dual-action polishers, represents a significant capital investment that often runs into thousands of pounds. While your valeting business insurance policy addresses liability and road risks, you must also ensure your physical assets are protected against theft, fire, and accidental damage. Standard van insurance often falls short in this area. It typically covers the vehicle as a mode of transport but excludes the professional tools and expensive chemicals stored in the rear.

Theft from mobile vans remains a common pain point for UK valeters. Criminals often target these vehicles because they know they contain high-value, portable equipment that is easily resold. Ensuring you have the right commercial coverage is part of following broader UK government rules on business insurance, which emphasize the importance of maintaining adequate protection for all business activities. For fixed detailing studios, “Plant and Machinery” cover becomes essential to protect heavy-duty installations like hydraulic lifts or industrial lighting systems that cannot be easily moved.

Van and Tools Insurance for Mobile Valeters

A mobile setup requires specialized van and tools insurance to bridge the gap left by standard motor policies. This should include “Goods in Transit” cover, which is vital for protecting high-value waxes and ceramic coatings that could be damaged or stolen during transit. To satisfy insurer requirements and potentially lower your premiums, consider this security checklist for your van:

- Install high-quality deadlocks or slam locks on all loading doors.

- Use a GPS tracking system to monitor the vehicle’s location 24/7.

- Ensure professional tool chests are bolted directly to the vehicle floor.

- Never leave expensive equipment in the van overnight if it isn’t parked in a secure, locked compound.

Covering Professional Detailing Studios

If you operate from a permanent unit, your risks shift toward the property itself. You will likely need commercial property insurance to protect the building and your “Stock and Contents.” Detailing studios often hold high volumes of flammable chemicals and expensive consumables that need specific fire and spill protection. It’s also vital to verify if your policy includes business interruption cover. If a fire or flood makes your studio unusable, this protection helps cover your lost income and ongoing fixed costs while you find a temporary location or rebuild your facility.

Mobile Valeting vs. Fixed Studio: Different Risks, Different Policies

The choice between a mobile setup and a fixed studio dictates the structure of your valeting business insurance policy. While both models focus on automotive care, the environments in which they operate present distinct liabilities. Mobile operators thrive on flexibility but face unpredictable public spaces. Fixed studios offer a controlled environment yet concentrate high-value risks, such as fire hazards and overnight storage liabilities, under one roof. As you scale from a single van to a dedicated unit, your policy must evolve to reflect these shifting exposures.

Mobile Valeting Considerations

For mobile operators, the primary challenge is the lack of a perimeter. Working on a client’s driveway or in a public car park means you’re constantly managing public footfall. A pedestrian tripping over a trailing hose or slipping on runoff is a constant risk. This is why many mobile professionals start with tradesman insurance as a foundation. You must also consider the weather; wind can carry abrasive chemicals onto neighboring vehicles or property, leading to unexpected claims. Mobile operators face a heightened risk of environmental liability due to uncontrolled chemical runoff into public drainage systems. Without the right protection, these “Mobile Risk Factors” can quickly escalate into costly legal disputes.

Detailing Studio and Unit Risks

Once you move into a permanent workshop, your responsibilities as an occupier increase. You’ll need employers liability insurance if you have staff working in the unit, as workshop environments carry inherent risks from electrical equipment and chemical exposure. Fire is a significant concern for studios due to the concentration of bulk chemicals, pressurized containers, and high-powered lighting. If you store customer vehicles overnight, you need the UK equivalent of “Garage Keepers” liability to ensure those assets are covered against theft or damage while on your premises.

Additionally, if your business specializes in larger commercial vehicles or HGVs, you may need to account for working at height. Using scaffolding, platforms, or even tall ladders to reach the roofs of trucks introduces a risk profile that standard valeting policies might exclude. Scaling your business safely means identifying these gaps before they become an issue. You can tailor your insurance to your specific setup to ensure every aspect of your operation, whether mobile or fixed, remains fully protected.

How to Get the Best Valeting Business Insurance Quote

Securing a valeting business insurance policy shouldn’t be a matter of guesswork. While generic comparison sites are convenient for standard car insurance, they often lack the technical depth required for the professional motor trade. These platforms frequently overlook the nuances of “Custody and Control” or the specific risks associated with high-end mobile detailing. A specialist approach ensures that your premiums are based on your actual risk profile rather than a generic industry average. This prevents you from paying for cover you don’t need while ensuring you aren’t left exposed during a claim.

To obtain an accurate and competitive quote, you need to have specific business data ready. Insurers typically require your estimated annual turnover, the maximum value of any single vehicle handled at one time, and your total employee count. Accuracy here is vital to avoid under-insurance. Additionally, remember that if your business earns over £1,000 annually, you’re legally required to register with HMRC. For those who started as a sole trader in May 2026, the deadline to register for Self Assessment is October 5th, 2027. Keeping your legal and tax status in order is a foundational step in proving your business’s legitimacy to insurers.

You can actively lower your premiums by demonstrating a commitment to professional standards. Holding recognized industry certifications and maintaining a clean no-claims history are effective ways to reduce costs. Investing in high-grade security locks or tracking systems for your van also signals to underwriters that you’re a lower risk. A bespoke policy is always preferable to an off-the-shelf product because it allows you to tailor protections to your specific workflow, whether you’re a mobile operator or a studio owner.

The Role of an Independent Broker

Just Quote Me serves as a knowledgeable advisor in a complex market. We don’t rely on automated algorithms; instead, we access a panel of leading UK insurers to negotiate rates on your behalf. This human-centric approach is vital when you’re dealing with technical clauses like service indemnity or road risks. Our team provides the expert advice needed to ensure your policy has no hidden exclusions. With deep regional expertise across Staffordshire and the West Midlands, we understand the local market conditions that affect your business. We act as a steady hand, managing the administrative weight of insurance so you can stay focused on the workshop floor. Just Quote Me to simplify your renewal process and secure the most robust cover available.

Next Steps for Your Valeting Business

Your reputation is built on the quality of your finish, and your business should be built on the quality of your protection. Take a moment to review your current cover. If you’ve recently upgraded your equipment or moved to a new unit, your old policy might no longer be fit for purpose. We’re here to help you bridge those gaps and provide the security you need to satisfy high-end clients.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Secure Your Professional Reputation Today

Your success in the detailing industry relies on the trust you build with every vehicle you touch. By prioritizing a robust valeting business insurance policy, you ensure that accidental damage to expensive coatings or unexpected road risks don’t derail your hard work. This guide has highlighted the essential nature of “Custody and Control” and the importance of safeguarding your high-value equipment. These protections are what allow you to operate with confidence and attract premium clients who demand proof of professional cover. It’s about more than just staying legal; it’s about building a resilient foundation for your future growth.

Just Quote Me provides the steady hand you need in a complex insurance market. With over 30 years of industry experience, we act as an FCA-authorised independent broker with specialist knowledge of motor trade and liability risks. We understand the nuances of your daily operations and work to simplify the administrative burden. You can partner with a trusted advisor today to ensure your business remains protected and compliant. Take the next step toward total peace of mind and protect what you’ve built.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Frequently Asked Questions

Do I need insurance to start a mobile valeting business in the UK?

While insurance isn’t a legal requirement for sole traders without staff, it is essential for protecting your livelihood. Most professional clients won’t hire you without seeing a valid valeting business insurance policy first. It manages the risk of accidental damage that could otherwise bankrupt a new startup before it gets off the ground.

What is “Custody and Control” and why is it vital for valeters?

Custody and Control is a specific extension that covers items in your care that you don’t own. For valeters, this means the vehicle itself. Without this clause, you are personally liable for any damage caused to a customer’s car while you’re working on it, which is a risk most professionals simply can’t afford to take.

Does public liability insurance cover damage to the car I am cleaning?

Standard public liability insurance does not cover the vehicle you are cleaning. It protects you against claims for third party injuries or damage to property like a client’s garage or driveway. To cover the car you’re polishing or vacuuming, you must ensure your policy includes a Custody and Control provision as part of your motor trade cover.

Is employers liability insurance mandatory for a valeting business?

Employers liability insurance is a legal requirement if you employ anyone, even on a casual or part-time basis. Failing to have this cover can lead to significant daily fines from the Health and Safety Executive. It protects your business if an employee is injured or falls ill due to their work for you, providing vital security for your team.

Can I get insurance that covers me for both mobile and studio-based valeting?

You can certainly secure a hybrid policy that covers both mobile and studio-based activities. We specialize in building bespoke valeting business insurance policy packages that adapt as your business grows. This ensures you’re protected whether you’re working on a customer’s driveway or in your own dedicated detailing unit with specialized lighting and equipment.

How much does a valeting business insurance policy typically cost?

The cost varies based on your turnover, the value of vehicles you handle, and your claims history. While basic liability cover can be affordable, the price reflects the level of protection you choose. It’s helpful to remember that the average claim for UK valeters between June 2025 and May 2026 was £3,936, making a robust policy a sensible investment for any professional.

Does my policy cover me to drive customer vehicles on the road?

You are only covered to drive customer vehicles if your policy includes specific Road Risks cover. This is a separate component from public liability. If you need to move cars on public roads or even just reposition them in a car park, you must verify that this protection is active on your certificate to remain legally compliant.

What happens if I accidentally damage a high-value ceramic coating?

Accidental damage to specialized finishes like ceramic coatings is typically covered under service indemnity or custody and control clauses. These parts of your policy are designed for professional detailers who perform complex paint correction and protection. Having this cover ensures you can rectify mistakes and maintain your reputation without facing a devastating financial loss.