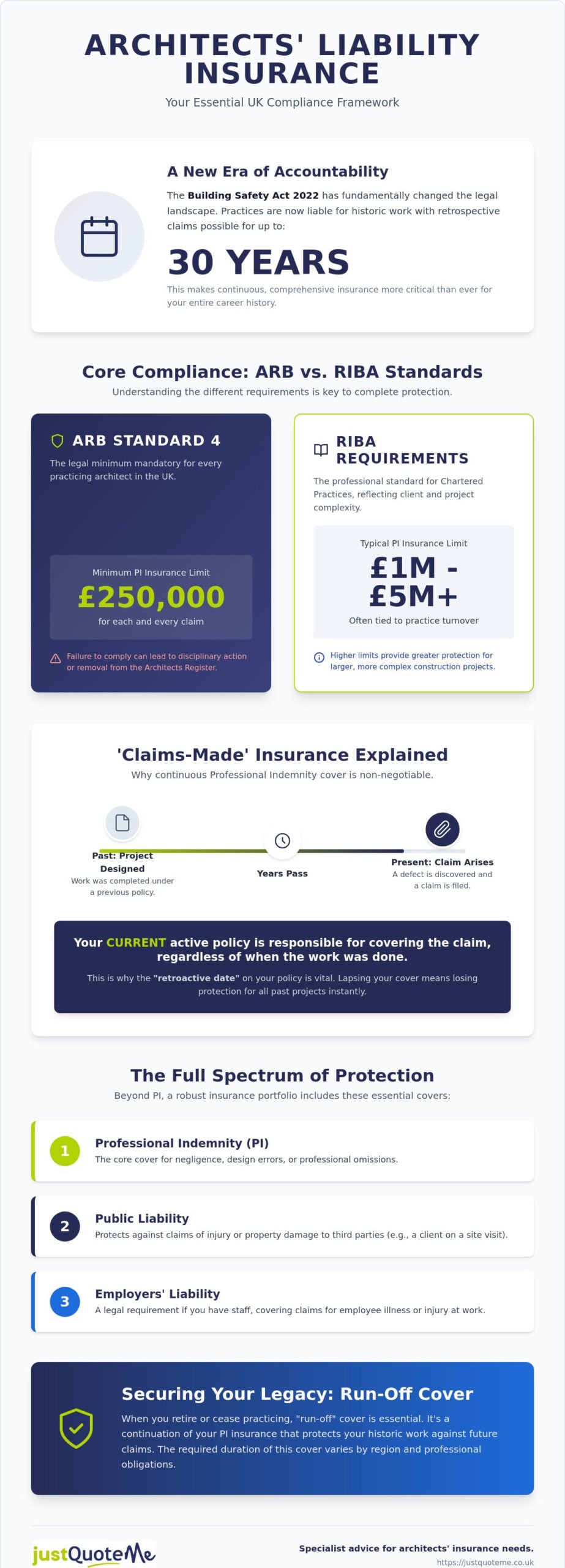

Did you know that the Building Safety Act 2022 now allows for retrospective claims dating back up to 30 years? For a practice owner, this shift transforms your insurance policy from a standard renewal into a vital shield for your entire career history. Meeting the mandatory architects liability insurance requirements isn’t just about ticking a box for the Architects Registration Board (ARB); it’s about protecting yourself against a legal landscape that’s shifted significantly. Since the new Architects Code of Conduct became effective on September 1, 2025, the pressure to maintain precise, compliant cover has never been higher.

It’s understandable if you feel overwhelmed by the hardening market or the conflicting advice between statutory ARB mandates and RIBA recommendations. We understand that you’d rather spend your time on site or at the drawing board than decoding policy fine print. This guide provides a clear compliance framework to help you navigate your professional obligations with confidence. You’ll learn how to distinguish between essential Professional Indemnity (PI) limits, Public Liability, and Employers’ Liability while ensuring your historic work remains fully protected.

Key Takeaways

- Understand the mandatory ARB Standard 4 mandates to ensure your practice remains fully compliant with current UK regulations.

- Learn how the ‘claims-made’ nature of Professional Indemnity insurance affects your long-term risk and why specific indemnity limits are essential.

- Navigate the full spectrum of architects liability insurance requirements by balancing statutory PI cover with Public and Employers’ Liability for comprehensive protection.

- Secure your legacy by identifying the specific run-off cover durations required in your region after you cease practice.

- Simplify the renewal process by working with a specialist who understands the nuances of RIBA recommendations versus mandatory statutory minimums.

Statutory and Professional Insurance Obligations for UK Architects

For any UK architect, professional survival depends on more than just design talent; it rests on maintaining your status on the Architects Register. The Architects Registration Board (ARB) oversees this through a strict set of rules known as the Architects Code: Standards of Conduct and Practice. Standard 4 explicitly mandates that all architects must have adequate and appropriate insurance. Failing to meet these architects liability insurance requirements isn’t a minor administrative slip. It can lead to formal disciplinary action, public reprimands, or even permanent removal from the Register.

The current regulatory climate, shaped by the new Architects Code that became effective on September 1, 2025, places the burden of proof on the practitioner. You must demonstrate that your cover is sufficient for the specific risks associated with your projects. While the ARB sets the legal floor, professional bodies like the RIBA often set the ceiling. These organisations frequently demand higher indemnity limits and broader policy terms to maintain chartered status, reflecting the increased complexity of modern construction projects.

Understanding ARB Standard 4 Requirements

The ARB defines “adequate and appropriate” cover based on the nature and value of your work. At its core, this means holding Professional Indemnity Insurance with a minimum limit of £250,000 for each and every claim. This mandatory minimum applies to every practicing architect in the UK, regardless of whether you’re a sole practitioner or part of a large firm.

During the annual retention process, you’re required to confirm that your policy meets these standards. It’s a proactive duty; you don’t just wait for a claim to happen. You must ensure your policy covers the full scope of your professional activities, including any historic work that might still be subject to legal action under the Building Safety Act 2022.

RIBA vs. ARB: Navigating Overlapping Standards

While the ARB’s £250,000 limit is the legal baseline, RIBA Chartered Practices usually face more rigorous demands. RIBA requirements are often tied to practice turnover, and for many, a limit of £1 million or £5 million is the standard expectation from clients and the institute alike.

A critical distinction in Professional Indemnity Insurance

Professional Indemnity Insurance: The Core Requirement

Professional Indemnity Insurance (PII) is the cornerstone of any practice’s risk management strategy. It addresses financial losses resulting from alleged negligence, design errors, or omissions in your professional advice. While earlier we discussed the ARB’s legal mandates, understanding the technical mechanics of Professional Indemnity Insurance is what actually keeps your practice solvent during a dispute.

Unlike most other insurance types, PI operates on a ‘claims-made’ basis. This means the policy you have active today must cover the claim, regardless of when the design work was originally completed. If you’ve been practicing for a decade, your 2026 policy is responsible for designs you drafted in 2016. This makes the continuity of cover and the “retroactive date” on your certificate vital. If you let your cover lapse, you lose protection for all past projects instantly.

In 2026, insurers remain cautious about specific risks. You’ll likely find strict exclusions or high deductibles regarding cladding and fire safety. Notably, the Wren Insurance Association’s shift away from cladding renewal terms in July 2026 illustrates how quickly the market can change. You must verify that your policy aligns with the latest Statutory and Professional Insurance Obligations to avoid gaps in coverage that could lead to personal liability. If you’re unsure how these exclusions affect your current policy, you can speak with a specialist to review your practice’s specific needs.

Determining the Right Limit for Your Practice

The ARB’s £250,000 minimum is often insufficient for modern projects. A minor design error in a residential block can easily exceed this limit once legal fees and remedial costs are tallied. When calculating your architects liability insurance requirements, look beyond turnover. Consider the total value of the projects you’ve designed over the last 15 to 30 years. The Building Safety Act 2022 has extended the liability period significantly, meaning your ‘worst-case scenario’ now has a much longer tail.

Common PI Clauses and Endorsements

The Liability Trinity: Public, Employers, and Cyber Cover

While Professional Indemnity (PI) is the most discussed aspect of your risk profile, it doesn’t exist in a vacuum. A robust approach to architects liability insurance requirements must account for the physical and digital risks that occur outside of your design software. Relying solely on PI is a dangerous gamble. If a member of the public trips over your equipment during a site survey, or if a disgruntled former employee steals your proprietary BIM data, a PI policy won’t offer a penny of protection.

Understanding this “Liability Trinity” is essential for modern practice management. While the Architects Registration Board PII Guidance focuses primarily on the indemnity needed for professional advice, your broader legal and commercial survival depends on addressing these three additional pillars.

Public Liability for Site Visits and Surveys

Every time you step onto a construction site or visit a client’s property, you’re exposed to physical risk. Public Liability insurance protects your practice if your actions cause injury to a third party or damage to their property. It isn’t just for large firms; even a sole practitioner conducting a simple measured survey needs this cover.

Standard indemnity limits usually start at £1 million, but many commercial contracts or local authority projects will insist on £2 million or £5 million as a minimum. It’s a relatively low-cost addition that prevents a single accident from becoming a practice-ending event. Learn more about Public Liability Insurance to see how it integrates with your existing design cover.

Employers Liability and Statutory Compliance

If you have any staff, Employers’ Liability (EL) is a legal requirement under the Employers’ Liability (Compulsory Insurance) Act 1969. This isn’t optional. The law mandates a minimum of £5 million in cover, though most insurers provide £10 million as standard.

This requirement isn’t limited to full-time architects. You must cover freelancers, interns, and even part-time administrative staff. Failing to hold EL can result in fines of up to £2,500 for every single day you’re without it. Understanding Employers Liability Insurance is the first step in ensuring your practice remains on the right side of UK law.

Cyber Risks in Modern Architectural Practices

Architectural design has moved almost entirely into the digital space, making Building Information Modelling (BIM) systems a prime target for cybercriminals. A data breach can lead to the loss of sensitive client blueprints or the theft of intellectual property. Cyber insurance covers the heavy costs of data recovery, legal fees, and the mandatory client notifications required under GDPR. It’s becoming an increasingly vital component of Bespoke Cyber Insurance for Professionals

Run-off Cover: Meeting Post-Practice Requirements

Retirement or the closure of a practice doesn’t signal the end of your professional exposure. In fact, for many, it’s the beginning of a decade-long period of “tail risk.” Because Professional Indemnity Insurance operates on a claims-made basis, you must have a policy active at the moment a claim is made, not just when the work was performed. If you cease practicing today but a design flaw is discovered in three years, you’ll be personally liable for the damages unless you’ve secured run-off cover.

Meeting the architects liability insurance requirements for run-off isn’t just a matter of professional prudence; it’s a regulatory mandate. The Architects Registration Board (ARB) requires architects to maintain run-off cover for a minimum of six years in England, Wales, and Northern Ireland. In Scotland, this requirement is five years. However, many legal experts suggest that 12 years of cover is the safer choice. This is because contracts signed “under seal” carry a 12-year limitation period, and the Building Safety Act 2022 has pushed some liability windows even further.

The Long Tail of Architectural Liability

The statute of limitations for contract and tort claims creates a significant lag between the completion of a project and the emergence of a dispute. If your practice merges or closes, your liability typically follows you. Without run-off protection, your personal assets could be at risk from projects you haven’t thought about in years. This is why the ARB views run-off cover as a non-negotiable part of the Architects Code. It ensures that clients aren’t left without recourse and that architects aren’t left financially devastated by historic errors.

Securing Cost-Effective Run-off Protection

Securing run-off cover in a hard insurance market can be challenging, as insurers have become more selective about the risks they’ll carry for inactive professionals. Premiums for run-off usually start at a percentage of your last full premium and often decrease annually as the likelihood of a claim from older projects diminishes. Some insurers offer a single “upfront” premium to cover the entire six or twelve-year period, which can simplify your financial planning as you exit the profession.

If you’re planning your retirement and need to understand how to structure your exit without leaving gaps in your cover, you can Request a Call back for free Expert advice. Managing these final architects liability insurance requirements

Simplifying Your Insurance with Just Quote Me

Meeting the complex architects liability insurance requirements in a hardening 2026 market doesn’t have to be a source of anxiety. While automated online platforms offer speed, they often lack the nuance required to ensure your policy actually stands up to ARB scrutiny or the extended liability periods of the Building Safety Act. Algorithms don’t understand the specific risks of your project history. We do. At Just Quote Me, we act as your steady hand, managing the administrative burden so you can focus on your designs.

We bring 30 years of experience to the table. This deep industry knowledge allows us to look beyond the surface of a standard application. We understand how the mandates discussed earlier in this guide impact your daily operations. By working with an independent broker, you gain an advocate who knows how to present your practice’s risk profile to insurers in the best possible light. This often results in more competitive premiums and broader coverage than a generic search engine could ever provide.

Why a Bespoke Approach Beats ‘Off-the-Shelf’ Policies

Off-the-shelf policies frequently leave architects under-insured. This is a risk you can’t afford. Conversely, you might be paying for unnecessary extras that don’t apply to your specific sector. We take a different approach. By tailoring your Bespoke Professional Indemnity Insurance, we ensure every clause aligns with your turnover, project risk, and specific RIBA Chartered Practice obligations. We don’t just provide a certificate; we help you navigate the compliance documentation needed for your annual ARB retention. Our team assists with policy wordings to ensure you aren’t caught out by the fine print during a claim.

Start Your 2026 Compliance Journey Today

Securing your cover for the year ahead is a quick and efficient process. We pride ourselves on providing straightforward, jargon-free insurance advice that cuts through the noise of the current market. By leveraging our deep relationships with a panel of specialist UK insurers, we help you meet all architects liability insurance requirements without overcomplicating your overheads. We believe in a human-centric service that prioritizes your practice’s long-term security over a quick transaction. Whether you are a sole practitioner or a growing firm, we ensure your cover is as precise as your drawings.

Protect Your Professional Legacy

Adhering to architects liability insurance requirements is a career-long duty that safeguards your reputation and your financial future. The regulatory environment in 2026 is more demanding than ever, requiring a balance between mandatory ARB minimums and the long-term protections necessitated by the Building Safety Act. Whether you’re managing the daily risks of site visits or planning a secure exit from the profession with run-off cover, a precise policy is your most important tool.

Just Quote Me acts as your trusted advisor, drawing on 30 years of industry experience to simplify these complex requirements. As an FCA-authorised independent broker, we provide direct access to top UK insurers, ensuring you secure comprehensive protection tailored to your unique workload. We manage the administrative burdens so you can focus on the architectural excellence your clients expect. Get the peace of mind that comes from a steady hand in a hardening market.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Frequently Asked Questions

Is Professional Indemnity Insurance a legal requirement for UK architects?

Yes, holding Professional Indemnity Insurance is a mandatory requirement for all architects registered with the Architects Registration Board (ARB). Under Standard 4 of the Architects Code, you must have adequate and appropriate cover to practice. While it’s a professional mandate rather than a criminal law, failing to maintain cover will lead to your removal from the Register. This effectively ends your legal right to use the title ‘architect’ in the UK.

What is the minimum level of PI insurance required by the ARB?

The ARB mandates a minimum indemnity limit of £250,000 for each and every claim. This level is the absolute legal floor for any practicing architect. However, most commercial contracts and professional bodies like the RIBA suggest much higher limits. You should assess your architects liability insurance requirements based on your specific project values rather than just relying on this statutory minimum, as modern litigation costs can quickly exceed this amount.

How long must an architect maintain run-off cover after retiring?

You are required to maintain run-off cover for a minimum of six years if you practice in England, Wales, or Northern Ireland. For those in Scotland, the requirement is five years. Because architectural liability has a ‘long tail’, many professionals choose to extend this cover to twelve years. This aligns with the limitation period for contracts signed under seal, providing a more robust safety net against delayed claims.

Does my PI insurance cover me for cladding and fire safety claims in 2026?

Coverage for cladding and fire safety is currently highly restricted in the UK insurance market. Many standard policies now include specific exclusions or much higher deductibles for these risks. Following the Building Safety Act 2022, insurers have become increasingly cautious. You must check your policy schedule carefully. If your current provider excludes these areas, you may need to seek a specialist endorsement to ensure your architects liability insurance requirements are fully met.

What is the difference between Public Liability and Professional Indemnity for architects?

Professional Indemnity covers financial losses caused by errors in your design or professional advice. In contrast, Public Liability protects you against claims for physical injury to third parties or accidental damage to their property. For example, if you provide a faulty structural design, PI responds. If you knock over a valuable vase or a client trips over your tripod during a site survey, Public Liability provides the necessary protection.

Can I practice as an architect without being registered with the ARB?

No, you cannot legally call yourself an architect or practice under that title in the UK without ARB registration. The title ‘architect’ is protected by the Architects Act 1997. To remain registered, you must comply with all professional standards, including mandatory insurance obligations. Practicing without registration is a criminal offence that can result in prosecution and significant fines, regardless of your qualifications or previous experience level.

What happens if I cannot find affordable PI insurance in the current market?

If you’re struggling with high premiums, don’t simply stop your cover, as this violates ARB rules. The ‘hardening’ market has made renewals difficult for many small practices. In these cases, it’s best to work with an independent broker who can access a wider panel of specialist insurers. They can often help reframe your risk profile or find alternative providers that don’t appear on standard automated comparison platforms.

Do I need insurance if I am only doing small residential extensions?

Yes, insurance is mandatory regardless of the size or complexity of your projects. Even a minor error in a residential extension can lead to significant remedial costs or structural issues that exceed your personal assets. The ARB doesn’t differentiate between large scale developments and small domestic works when it comes to insurance. Every registered architect must hold adequate cover to protect both themselves and their clients from potential financial loss.