Could a single line of faulty code or a misunderstood requirement on a high-stakes project actually bankrupt your business? For many tech professionals, the fear of being sued for a data breach or a delivery delay is a constant background noise. It’s frustrating when recruiters hand you a contract filled with vague insurance jargon that you’re expected to sign immediately. This is why professional indemnity for it contractors is no longer just a checkbox on a list. It’s the most critical cover you can hold in 2026, acting as a strategic asset that validates your professional status and secures your financial future.

We understand that you’d rather focus on your next sprint than decode insurance fine print. You’ll learn exactly why this protection is vital for protecting your assets and meeting specific recruitment requirements. This guide breaks down how to fulfill your contractual obligations, explains the “claims made” nature of modern policies, and ensures you have genuine peace of mind while working on complex systems. We’ll simplify the administrative burden so you can get back to what you do best, knowing your business is fully protected against legal fees and negligence claims.

Key Takeaways

- Understand why professional indemnity for it contractors is the cornerstone of your business protection, covering legal defense and compensation for negligence claims.

- Discover how to navigate complex “claims made” policies and the importance of maintaining continuous cover to protect your past work.

- Identify the specific IT risks covered by these policies, including unintentional data breaches and errors in professional advice or service delivery.

- Determine the right level of cover for your contracts and why a £1 million limit is the standard baseline for most UK IT projects.

- Learn how an independent broker simplifies the process by matching your specific contract requirements with the right insurer from a broad panel of providers.

What is Professional Indemnity for IT Contractors?

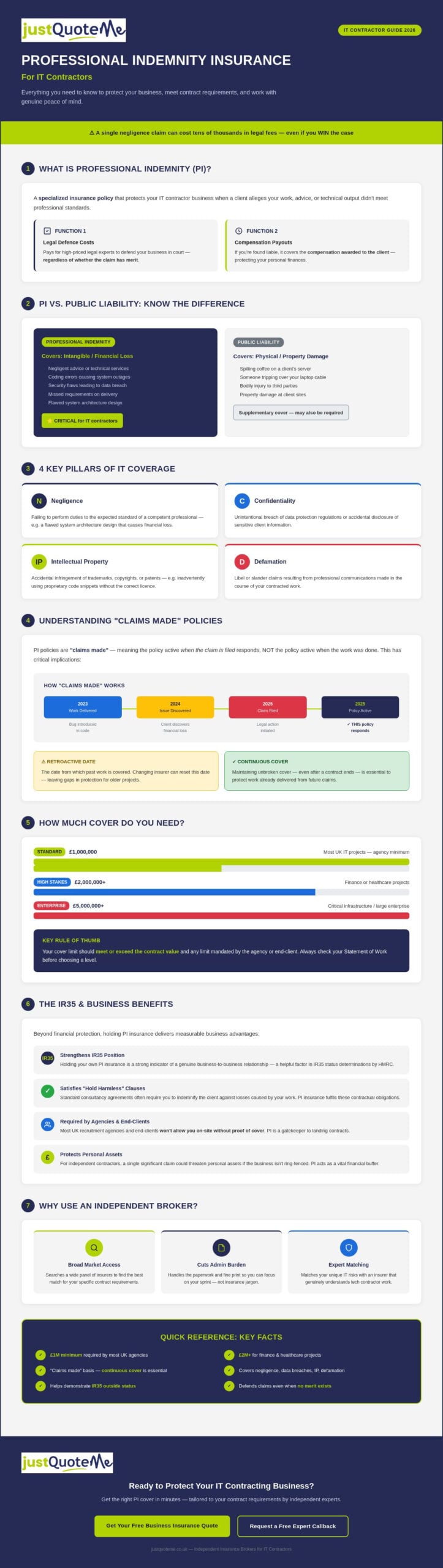

At its core, professional indemnity for it contractors is a specialized insurance policy designed to protect your business when a client alleges that your work didn’t meet professional standards. Whether you’re a software developer, a systems architect, or a cybersecurity consultant, your advice and technical output carry significant weight. If a coding error leads to a system outage or a security flaw results in a data breach, your client may pursue legal action to recover their financial losses. This type of cover, often referred to as What is Professional Indemnity Insurance in broader legal contexts, addresses claims of negligence, errors, or omissions in the services you provide.

The policy serves two primary functions. First, it pays for the high-priced legal experts needed to defend your business in court, regardless of whether the claim has merit. Second, if you’re found liable, it covers the compensation awarded to the client. Beyond financial protection, holding this insurance is a practical necessity for modern contracting. It allows you to satisfy “hold harmless” clauses found in standard consultancy agreements, where you agree to indemnify the client against losses caused by your work. Additionally, having your own professional indemnity for it contractors acts as a strong indicator of a genuine business-to-business relationship, which is a helpful factor in IR35 status determinations.

The Legal and Financial Necessity

Most UK recruitment agencies and end-clients won’t allow you on-site without proof of cover. They typically mandate a minimum limit of £1 million, though high-stakes projects in finance or healthcare often require £2 million or more. This isn’t just a bureaucratic hurdle. Defending a professional negligence claim in the UK can easily cost tens of thousands of pounds in legal fees alone, even if you eventually win the case. Without insurance, these costs fall directly on your business. For many independent contractors, a single significant claim could threaten personal assets if the business isn’t properly ring-fenced. Your policy acts as a vital buffer, ensuring that a professional mistake doesn’t become a personal financial disaster.

PI vs. Public Liability: Knowing the Difference

It’s easy to confuse different types of insurance, but the distinction between Professional Indemnity (PI) and Public Liability (PL) is sharp. Public liability is concerned with physical outcomes. If you spill coffee on a client’s server or someone trips over your laptop cable, PL covers the resulting bodily injury or property damage. You can read more about this in our guide: What Is Public Liability Insurance?

In contrast, Professional Indemnity focuses on the intangible. It covers the financial loss a client suffers because of your professional advice or technical services. As an IT contractor, your biggest risks are usually digital and financial rather than physical. While you might need both to satisfy a contract, PI is almost always the more critical cover for the specific risks associated with software delivery, system design, and IT consultancy.

What Does Professional Indemnity Actually Cover in IT?

While the broad definition of professional indemnity for it contractors focuses on professional negligence, the actual scope of protection is much more granular. It’s designed to mirror the specific risks you face in a digital environment. For instance, if you’re a software engineer, your policy doesn’t just cover generic mistakes. It covers the financial fallout from a specific bug that brings down a client’s e-commerce platform during a peak trading period. This protection ensures that your business can survive the legal and compensatory demands that follow such an event.

A comprehensive policy typically addresses four key pillars of risk:

- Negligence: Failing to perform your duties to the standard expected of a competent professional, such as a flawed system architecture design.

- Confidentiality: An unintentional breach of data protection regulations or the accidental disclosure of sensitive client information.

- Intellectual Property: Accidental infringement of trademarks, copyrights, or patents, which can happen if you inadvertently use proprietary code snippets without the correct license.

- Defamation: Libel or slander claims resulting from professional communications, reports, or public-facing documentation.

You can find more detailed breakdowns of these triggers in resources dedicated to professional indemnity insurance for IT contractors, which highlight how these protections apply specifically to consultancy and freelance roles.

Common IT Claim Scenarios

Real-world claims often stem from mismanaged expectations or technical oversights. Missed deadlines hurt. Imagine a scenario where a software bug in a bespoke CRM results in the loss of several days of sales data. The client could sue for the lost revenue and the high cost of manual data recovery. Project management failures are equally common. If you’re leading a cloud migration and miss a critical milestone, causing the client to pay penalties to their own customers, they’ll likely look to your insurance to cover those costs. Even technical advice can backfire; recommending a server configuration that proves insufficient for a client’s traffic load can lead to a claim for “unfit” advice.

The Cyber Overlap: Data and Security Errors

There’s often confusion about where PI ends and cyber cover begins. In 2026, the distinction is vital for your risk management strategy. Professional Indemnity covers your errors, such as misconfiguring a firewall or failing to patch a known vulnerability in a system you manage. However, it generally won’t cover the costs of a malicious ransomware attack or a brute-force hack if your work was flawless. For protection against external threats and the recovery costs of a breach, you should consider Cyber Insurance as a separate but complementary layer. If you’re unsure which risks your current contract exposes you to, it’s a good idea to consult with a specialist broker who understands the nuances of the tech sector.

Understanding the Fine Print: Claims Made and Retroactive Dates

Professional indemnity for it contractors operates on a “claims made” basis, which is a fundamental departure from how most people understand insurance. If you’re used to car or home insurance, you likely expect your policy to cover an event as long as it happened while the policy was active. Professional Indemnity doesn’t work that way. For a claim to be valid, your policy must be live both when you did the work and when the claim is actually filed against you. This distinction is critical because a client might not notice a system vulnerability or a coding error until months, or even years, after you’ve finished the project.

This timing requirement is why maintaining continuous cover is the only way to stay protected. If you let your policy lapse for even a week while switching providers, you create a “gap” that could leave you exposed for all your past work. To fully grasp the mechanics, you must first understand What Professional Indemnity Actually Covers, but more importantly, you need to understand when that protection is triggered. Without a live policy at the moment a legal letter arrives, you’re effectively uninsured for everything you’ve ever done.

Claims Made vs. Claims Occurring

Timing matters more than the mistake itself. In a “claims occurring” model, you look back at who insured you on the date of the incident. In the “claims made” model used for professional indemnity for it contractors, the current insurer handles the claim regardless of when the error happened, provided it occurred after your “Retroactive Date.” This is why you must notify your broker the second a “circumstance” arises. If a client expresses dissatisfaction or hints at a financial loss, don’t wait for a formal lawsuit. Early notification prevents “late notification” exclusions, which insurers use to deny claims if they feel you sat on bad news for too long.

The Importance of Retroactive Cover

Your Retroactive Date is essentially your policy’s “memory.” It marks the earliest point in time from which your insurer agrees to cover your work. When you start your first policy, this date is usually the inception date. However, if you switch insurers, you must ensure your new provider honors your original Retroactive Date. Letting this date reset to the present day effectively wipes out the protection for every line of code you’ve written in the past.

This is particularly vital if you move from one limited company to another or if you’re an IT freelancer moving between high-stakes contracts. Continuous cover is the gold standard. If you decide to stop contracting or retire, you’ll need “run-off cover.” This specialized extension keeps your professional indemnity active for several years after you’ve stopped working, ensuring that delayed claims from old projects don’t come back to haunt your retirement funds.

How Much Professional Indemnity Cover Do You Need?

Choosing the right limit for your professional indemnity for it contractors policy often feels like a balancing act between cost and compliance. In the UK, the most common baseline is £1 million. This figure isn’t arbitrary; it’s the standard minimum required by the vast majority of recruitment agencies and end-clients. However, simply opting for the baseline without analysis can be a mistake. You must evaluate the potential financial impact of your “worst-case scenario.” If a bug in your code causes a national retailer’s checkout system to fail during a holiday sale, the resulting loss of revenue could far exceed a million-pound limit.

When reviewing your options, you’ll encounter two different ways insurers apply these limits: “Any One Claim” and “Aggregate.” We always recommend “Any One Claim” for tech professionals. This means the full limit of your policy is available for every individual claim made against you during the year. In contrast, an “Aggregate” limit is the total amount the insurer will pay for all claims combined within the policy period. If you face two separate legal issues in one year, an aggregate limit could leave you underinsured for the second event.

Evaluating Contractual Requirements

Contracts from major UK financial institutions or government bodies often demand higher limits, frequently reaching £2 million or £5 million. You shouldn’t settle for less than what your contract specifies, as failing to maintain the required level of cover is often a breach of contract in itself. If you’re curious how these requirements compare to other industries, you can see how different sectors manage risk in our guide to Tradesman Insurance. While a plumber might only need cover for physical damage, your liability is tied to the massive financial throughput of your client’s digital systems.

Cost Drivers for IT Insurance

Several factors influence the premium you’ll pay. Your specific tech stack is a primary driver. A contractor providing high-level cybersecurity consultancy or managing cloud infrastructure for banks represents a higher risk than a front-end web designer. Your annual turnover also plays a role, as it acts as a proxy for the volume and scale of the work you handle. While it’s tempting to opt for a higher excess to lower your monthly payments, remember that you must be able to pay that amount out of pocket if a claim arises. To ensure you aren’t overpaying for cover you don’t need, it’s best to get a tailored insurance quote that reflects your actual daily risks.

Why Use an Independent Broker Like Just Quote Me?

Choosing the right professional indemnity for it contractors is about more than just finding the lowest premium. While automated comparison sites might offer speed, they often lack the nuance required to interpret the specific insurance clauses in a complex IT consultancy agreement. By working with an independent broker, you gain access to a broad panel of the UK’s leading insurers. This means we aren’t tied to a single provider’s criteria. Instead, we compare multiple policies to find the one that aligns perfectly with your specific tech stack and contractual obligations. When a contract requires a specific “Any One Claim” limit or a unique retroactive date, we know exactly which insurer can accommodate those needs.

One of the most significant advantages of a broker is the ability to create a cohesive protection strategy. Rather than managing multiple separate policies, we can help you build a bespoke solution that combines Professional Indemnity with Employers Liability Insurance and Cyber cover. This integrated approach ensures there are no gaps in your protection, particularly in the “grey areas” between professional error and external security breaches. If you ever need to make a claim, you won’t be directed to an automated call centre. You’ll have a human partner to manage the administrative burden and advocate for your interests with the insurer.

The Value of Expert Advice

In the professional indemnity market, a “cheap” policy often translates to insufficient cover or restrictive exclusions. We’ve spent 30 years supporting contractors across the Staffordshire and West Midlands region, giving us a deep understanding of the local and national contracting landscape. We help you navigate the fine print, ensuring your policy doesn’t just look good on paper but actually performs when it matters. Our goal is to simplify the complex administrative hurdles that often distract you from your core work. When the paperwork becomes a distraction, Just Quote Me to secure a steady hand in a complex market.

Get Your Free Quote Today

Securing the right professional indemnity for it contractors for 2026 shouldn’t be a stressful experience. Our process is designed for efficiency and clarity, providing you with direct access to specialists who understand the unique risks of software development, cloud migration, and IT consultancy. We provide the expert guidance you need to sign your next contract with total confidence, knowing your financial future and professional reputation are fully protected.

Request a Call back for free Expert advice

Secure Your Professional Future and Technical Reputation

Securing the right professional indemnity for it contractors is about more than just checking a box for a recruiter. It’s about building a resilient foundation for your business. We’ve explored how maintaining continuous cover and understanding your retroactive date prevents dangerous gaps in your protection. You now know that while £1 million is the standard industry baseline, your specific tech stack and the financial scale of your projects should dictate your final limits. These details ensure that a single coding error or system failure doesn’t derail your career or your finances.

As an FCA-authorised independent broker with over 30 years of industry experience, we provide the specialized knowledge needed to navigate these technical complexities. We offer expert advice tailored specifically to the nuances of the UK IT contracting landscape. Our team manages the administrative weight of your professional protection so you can focus on delivering exceptional results for your clients. Ready to safeguard your business? Partner with an insurance specialist today. You’ve worked hard to build your expertise; let us provide the steady hand that protects it.

Frequently Asked Questions

Do I need professional indemnity insurance if I work through an umbrella company?

You may still need your own policy even if your umbrella company provides basic cover, as their group policies often have lower limits or high excesses. If your specific contract requires a higher limit or specific “any one claim” wording, you’ll need your own professional indemnity for it contractors to remain compliant. Having your own policy ensures you control the level of protection and the retroactive dates, which is vital for long-term security.

Can I cancel my professional indemnity insurance between contracts?

You shouldn’t cancel your insurance between contracts due to the “claims made” nature of these policies. If you stop your cover, you effectively end protection for all your past work. If a former client files a claim during your gap in cover, you’ll be personally liable for legal fees and compensation. Maintaining continuous cover is the only way to safeguard your previous projects and ensure you aren’t left exposed during a lull in work.

What is the difference between professional indemnity and cyber liability?

The primary difference is that professional indemnity covers your professional errors, whereas cyber liability covers external attacks and data recovery. If you misconfigure a cloud database and data leaks, PI usually responds. If a hacker uses a brute-force attack to steal that same data, a cyber policy is required. As an IT professional, you often need both to address the full spectrum of modern digital risks and contractual requirements.

How much does professional indemnity insurance cost for a sole trader IT contractor?

Premiums are determined by your specific turnover, tech stack, and risk profile rather than a flat fee. Insurers evaluate your annual turnover and the complexity of the projects you handle. High-risk areas like financial systems or medical software naturally command higher premiums than basic web development or UI design. We recommend getting a personalized quote to find a price that accurately reflects your business and provides the protection you need.

What happens if a client claims against me for a mistake I made two years ago?

Your current insurer will handle the claim provided you’ve maintained continuous cover since the error occurred. This is why you must never let your professional indemnity for it contractors lapse when moving between insurers or taking a break. As long as your “Retroactive Date” precedes the mistake, your current provider will step in to manage the legal defence and any settlements, protecting your business from historical liabilities.

Is professional indemnity insurance tax-deductible for my limited company?

Yes, professional indemnity premiums are a fully tax-deductible business expense for UK limited companies. HMRC recognizes professional insurance as a cost incurred “wholly and exclusively” for the purpose of your trade. By paying for your policy through your business account, you reduce your taxable profit and lower your Corporation Tax liability. This ensures your business remains compliant and protected while maximizing your tax efficiency as an independent contractor.

What is “Any One Claim” cover, and is it better than aggregate cover?

“Any One Claim” cover is superior because it provides the full policy limit for every individual claim made during the year. Aggregate cover is a total limit for the entire policy period. If you have a £1 million aggregate limit and face two separate legal issues, the first claim could deplete the pot for the second. “Any One Claim” is the preferred choice for IT professionals due to this more robust level of protection.

Does professional indemnity insurance cover IR35 investigations?

Standard policies don’t typically cover the legal costs of an investigation, though they do help demonstrate a genuine business status. While holding your own insurance is a strong indicator of being “outside IR35,” the legal fees for an HMRC enquiry usually require a specific legal expenses extension. You should check if your policy includes tax enquiry cover or if you need to add it as a separate protection layer for complete peace of mind.

Request a Call back for free Expert advice