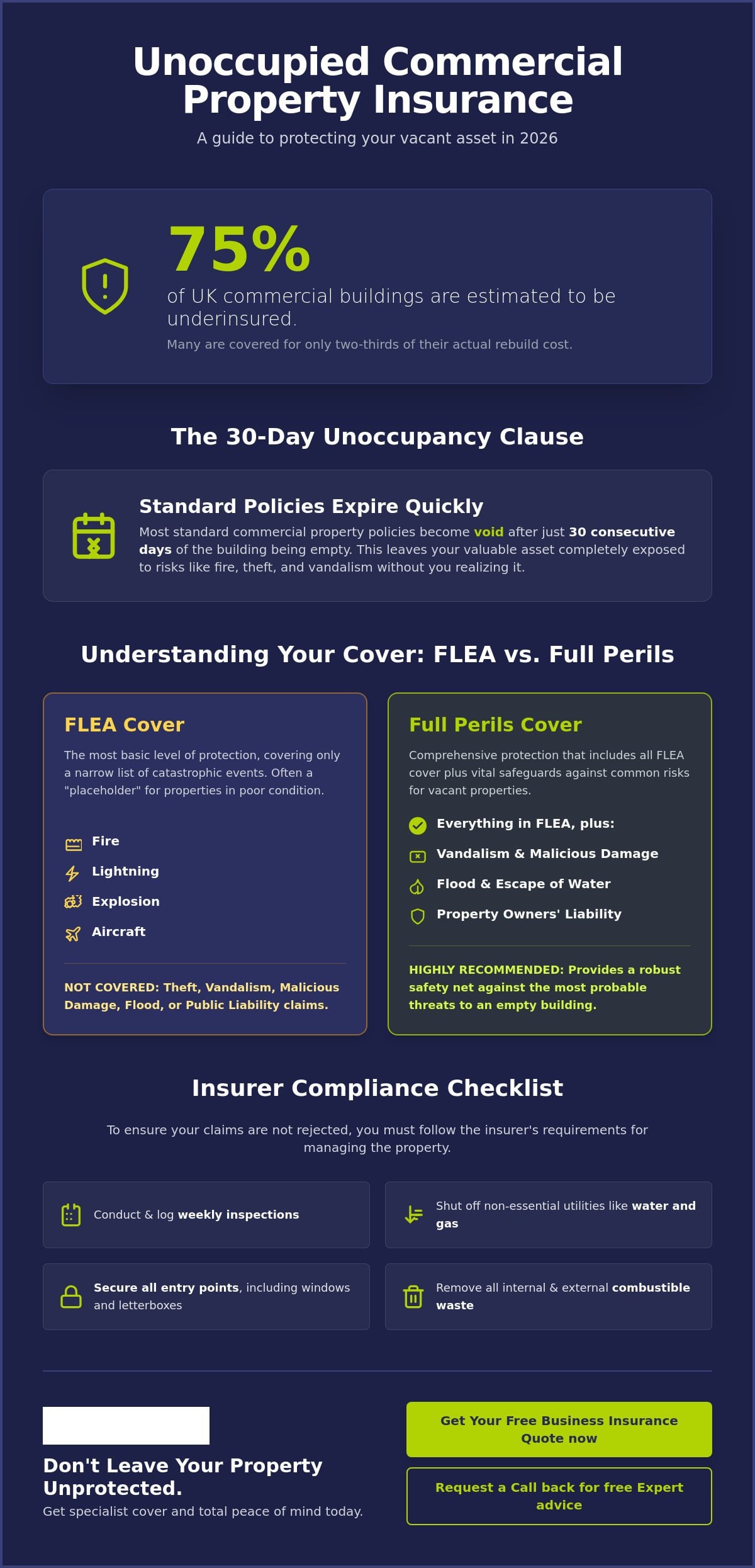

Did you know that an estimated 75% of UK commercial buildings are currently underinsured, with many covered for only two-thirds of their actual rebuild cost? When your premises sit empty, the stakes are even higher. You’re likely worried about restrictive small print or high premiums that don’t seem to offer real security against squatters and vandalism. It’s frustrating to discover that a standard policy often becomes void after just 30 days of unoccupancy, leaving your asset exposed. Finding the right insurance for unoccupied commercial property shouldn’t feel like a gamble with your investment.

We understand these challenges and want to help you gain total peace of mind while you seek a new tenant. This 2026 guide explains how to secure specialist cover that provides comprehensive protection against fire, theft, and property owners liability. We will walk you through the latest regulatory updates, including the Building Safety Act requirements and the Leasehold Reform changes that impact owners today. You’ll learn the difference between basic FLEA cover and full perils protection, alongside the specific maintenance steps required to ensure your claim is never rejected. We’re here to simplify the complex administrative burden so you can focus on your next move with confidence.

Key Takeaways

- Learn why standard business policies often restrict cover after 30 days and how specialist protection maintains your asset’s value.

- Compare basic FLEA cover against Full Perils to ensure your insurance for unoccupied commercial property includes vital protection for theft and vandalism.

- Master the essential compliance checklist, including the “weekly inspection” logbook, to prevent your claims from being rejected.

- Discover how bespoke brokerage provides a human-centric alternative to automated systems, offering tailored solutions for complex vacant sites.

What is Unoccupied Commercial Property Insurance?

Unoccupied commercial property insurance is a specialist risk product for buildings without active business operations. While this coverage falls under the broad category of What is Property Insurance?, it’s specifically designed for situations where traditional policies stop working. Standard commercial property insurance relies on the assumption that a building is being monitored daily by staff or tenants. Once a building sits empty, that fundamental assumption breaks down, and the risk level for the insurer changes significantly.

Standard insurers often restrict cover or cancel it entirely because vacant sites are magnets for trouble. Without eyes on the ground, a small pipe leak can become a catastrophic flood within days. Squatters or vandals might move in before you even realize the security has been breached. In the wider landscape of property protection, risk is calculated based on occupancy. If you remove the people, the risk of unmanaged damage or criminal activity spikes, which is why a standard policy is no longer sufficient.

Underwriters distinguish between “unoccupied” and “vacant” premises. An unoccupied building might still contain office furniture or stock, suggesting a temporary pause in operations. A vacant building is usually a bare shell with no contents. Both require specialist insurance for unoccupied commercial property, but the specific risks and the premiums will vary based on how empty the site truly is. Bare shells are often higher risks for arson, while furnished offices might attract thieves looking for equipment.

The 30-Day Rule: When Does a Property Become Unoccupied?

Most commercial policies include a specific unoccupancy clause. This usually triggers after 30 consecutive days of the building being empty. Some specialist providers might extend this to 45 or 60 days, but 30 remains the industry standard in 2026. It’s vital that you don’t wait for the 30 days to pass before acting. You should notify your broker the moment a tenant serves notice or as soon as you know the building will be empty. This proactive approach ensures there’s no gap in your protection. Short-term vacancy is handled differently than long-term vacancy, so being clear about your timeline helps us find the most cost-effective solution.

Types of Properties Covered

Specialist cover isn’t just for derelict buildings. It’s a necessity for various modern assets including:

- Retail units: High street shops between leases are highly susceptible to window smashing and graffiti.

- Warehouses: Large, isolated industrial units are prime targets for metal theft, which remains a significant concern for UK landlords.

- Ghost estates: These include new developments or partially occupied office blocks where some floors remain empty while others are active.

Whether it’s a single shop or a massive factory, if the business operations have stopped, the standard policy is no longer enough to protect your investment.

Understanding the Levels of Cover: FLEA vs. Full Perils

When you seek insurance for unoccupied commercial property, you’ll find that policies aren’t created equal. The level of protection you choose directly impacts your financial exposure during the vacancy period. Most insurers offer two distinct tiers of cover. The first is a restricted “basic” option, while the second provides a more comprehensive safety net. Choosing the right one requires a cold assessment of your building’s location, its physical condition, and how long you expect it to remain empty.

The entry-level option is known in the UK industry as FLEA cover. This acronym stands for Fire, Lightning, Explosion, and Aircraft. It represents the bare minimum level of vacant cover available. While FLEA policies are often the most affordable, they are intentionally narrow. They won’t protect you against common risks like a burst pipe or a smashed storefront. For many landlords, this level of cover is a “placeholder” used only when a building is in such poor condition that underwriters refuse to offer anything more robust.

Full Perils is the comprehensive alternative. This level of insurance for unoccupied commercial property adds protection for theft, vandalism, and flood damage. Given that vacant buildings are prime targets for criminal activity, the jump from FLEA to Full Perils is usually a wise investment. Property Owners Liability protects the landlord against injury claims from trespassers or the public. This is arguably the most critical component of any vacant property policy because legal claims for personal injury can far exceed the physical cost of rebuilding.

Property Owners Liability for Vacant Sites

Landlords often mistakenly believe they owe no duty of care to people who enter their property without permission. In reality, UK law requires you to maintain a safe environment even for unauthorised visitors. While you are managing Business Rates on Empty Commercial Property, you must also consider your legal exposure. Common hazards like falling masonry, loose floorboards, or poorly secured fencing can lead to massive compensation claims. This protection functions similarly to Public Liability Insurance, ensuring that a single accident doesn’t lead to financial ruin while your building is between tenants.

Full Perils: Is the Extra Premium Worth It?

The extra cost for Full Perils is usually justified by the risk of “Malicious Damage.” In areas with high vacancy rates, a building can be stripped of lead and copper piping in a single night. Furthermore, escape of water remains the most frequent cause of major vacant property claims. A small leak in an empty warehouse can go unnoticed for weeks, rotting floorboards and damaging the building’s foundations. Comprehensive policies can also include bespoke additions like glass cover and legal expenses. If you’re unsure which tier fits your specific risk profile, it’s worth speaking with an independent broker who can assess your site’s unique vulnerabilities.

The Unoccupancy Clause: Why Standard Policies Often Fail

Most landlords assume their existing coverage remains in force as long as they keep paying the premiums. However, standard business policies contain a “hidden” unoccupancy clause that fundamentally alters your protection once a building is empty for more than 30 days. Without warning, your comprehensive cover can drop to “Fire Only” or “FLEA” levels. This happens because the risk profile changes the moment a tenant leaves. When there are no eyes on the building, a minor issue like a slipped tile or a small leak can escalate into a total loss before anyone notices. Insurers view this lack of supervision as a breach of the original risk agreement, which is why they restrict their liability so aggressively.

The danger of “Non-Disclosure” is perhaps the greatest threat to your investment. If you fail to notify your insurer that a property is vacant, you risk voiding the entire policy. In the event of a claim, an adjuster will look for signs of long-term unoccupancy, such as a pile of unopened mail or disconnected utilities. According to guidance from the Royal Institution of Chartered Surveyors (RICS), understanding these technical triggers is vital for maintaining valid protection. Silence is never a strategy; it’s a fast track to a rejected claim.

Consider a common scenario: a burst pipe in a vacant office block during a winter freeze. Under a standard policy that has reverted to restricted cover, the insurer would likely reject the claim because “escape of water” is no longer a covered peril. You’d be left to pay for the floor replacements and structural drying out of your own pocket. Specialist insurance for unoccupied commercial property is designed to bridge this exact gap, ensuring that these common risks remain covered even when the building is silent.

The Risk of Vandalism and Squatters

UK law treats squatters in non-residential buildings differently than in residential ones. While squatting in a house is a criminal offence, occupying a commercial building is often treated as a civil matter, making eviction a slow and expensive process. Specialist insurance provides the legal support needed to navigate these evictions. Beyond squatters, vacant land and buildings are prime targets for fly-tipping. The cost of clearing tonnes of illegally dumped waste from a commercial site can reach thousands of pounds, a cost that standard policies rarely mention but specialist vacant cover can address.

Why Brokers Are Essential for Vacant Risks

Automated comparison sites are built for “standard” risks, and they often struggle with the nuances of high-risk unoccupancy. They can’t account for the specific security measures you’ve taken or the unique history of your site. While Commercial Property Insurance serves as the foundation, vacant risks require a human touch. A broker like Just Quote Me negotiates directly with underwriters to find terms that reflect your actual risk management. We understand that every empty building has a story, and we make sure the underwriters hear it so you get the best possible terms for your insurance for unoccupied commercial property.

Insurer Requirements: A Checklist for Managing Your Empty Premises

Securing insurance for unoccupied commercial property isn’t a “set and forget” process. It’s a conditional contract that remains valid only if you actively manage the risks associated with an empty building. Underwriters in 2026 are increasingly strict about these conditions because they know that a well-maintained vacant site is significantly less likely to suffer a total loss. If you fail to meet these specific requirements, you might find your claim rejected exactly when you need support the most. You should view these steps as a mandatory partnership with your insurer to protect your asset’s value.

To maintain your coverage, you must follow a set of physical security and maintenance protocols. These usually include:

- Sealing letterboxes: This prevents the buildup of junk mail, which signals unoccupancy to criminals, and reduces the risk of arson through the front door.

- Changing locks: You can’t be certain how many copies of keys former tenants or contractors might hold. Changing the barrels is a standard requirement for many specialist policies.

- Removing waste: Internal and external rubbish must be cleared to remove fuel for potential fires and to discourage fly-tipping.

- Utility management: Non-essential services should be disconnected at the mains, leaving only power for security alarms or essential heating systems.

If you need help understanding the specific fine print of your policy, you can contact our expert team for a clear explanation of your obligations.

The Weekly Inspection Protocol

The “Weekly Inspection” is the most frequent point of failure in vacant property claims. Most policies for insurance for unoccupied commercial property require a competent person to visit the site every seven days. During these visits, you must check the roof for damage, ensure all windows are secure, and walk the perimeter to look for signs of attempted entry. Crucially, you must maintain a written logbook of these visits. This log serves as your primary evidence for a loss adjuster, proving that you’ve been diligent in your “duty of care.” While you can use professional security firms, DIY inspections are usually acceptable as long as the documentation is thorough and consistent.

Preventing the “Escape of Water”

Water damage remains a leading cause of claims for empty buildings. Insurers typically give you two choices: drain the water system entirely and turn off the stopcock, or maintain a constant minimum temperature (usually between 5 and 7 degrees Celsius) throughout the winter months. Draining the system is often the safer, more cost-effective mandatory condition. In 2026, many landlords are also installing smart leak detection sensors that alert their phones the moment moisture is detected. These proactive measures not only protect your building but can also help in negotiating more favourable terms during your next renewal.

Securing a Bespoke Quote with Just Quote Me

Finding the right insurance for unoccupied commercial property requires more than a simple search engine query. It demands a partner who understands the specific risks of the UK market in 2026. Just Quote Me has spent 30 years as an independent broker, building a reputation for reliability and straightforward advice. We don’t rely on automated algorithms that see every empty building as a generic risk. Instead, we use our industry expertise to present your property in the best possible light to underwriters. This personalized approach is especially valuable for complex cases, such as buildings undergoing major renovations where the risk profile shifts every few weeks.

Our process is designed for efficiency and clarity. We start by listening to your specific needs, then we use our established relationships with top UK insurers to find a policy that survives where standard cover fails. We handle the administrative burden so you can focus on managing your portfolio. Whether you’re a local investor with a single vacant shop or a developer with a diverse commercial estate, we provide the steady hand you need in a complex market. We’re a human-centric alternative to automated systems, ensuring you get the protection your asset deserves.

Why Staffordshire Landlords Trust Just Quote Me

Regional expertise is a cornerstone of our service. We provide a personalized alternative to impersonal national firms, offering deep knowledge of the local landscape in Stone, Stafford, and Newcastle-under-Lyme. We understand the nuances of the West Midlands property market, from high street occupancy trends to industrial park security concerns. This local insight allows us to secure better terms for our clients because we can explain the context of a site to an underwriter. Many of our clients also benefit from our expertise in Landlord Insurance, allowing them to manage their entire portfolio through one trusted advisor.

Next Steps: Get Your Protection in Place

To secure the best possible terms for your insurance for unoccupied commercial property, you’ll need a few key details ready. Ensure you have an accurate rebuild value, a list of current security measures, and the specific reason for the vacancy. Having this information prepared allows us to work quickly on your behalf. We believe in plain, honest communication and providing immediate value to every property owner we serve. Don’t leave your vacant assets to chance; get the specialist cover you need today.

Protect Your Investment with Specialist Cover

Managing an empty building requires a proactive approach to risk management. You now understand why standard policies often fail after the 30-day unoccupancy trigger and why maintaining a strict inspection log is non-negotiable. By choosing the right level of insurance for unoccupied commercial property, you protect yourself against the high costs of vandalism, theft, and legal liability claims. You don’t have to manage these complex administrative burdens alone.

Just Quote Me acts as your steady hand in a complex market. With over 30 years of industry experience, we’re an FCA-authorised independent broker with access to a broad network of top UK insurers. We provide the expert advice and tailored solutions that automated systems simply cannot match. We’re ready to help you secure your assets and gain total peace of mind during this transition period.

Get Your Free Business Insurance Quote now

Request a Call back for free Expert advice

Frequently Asked Questions

Is unoccupied commercial property insurance more expensive than standard cover?

Yes, premiums for unoccupied commercial property are usually higher than those for occupied buildings. Insurers view vacant sites as higher risks because there aren’t staff on-site to spot maintenance issues or deter criminals. While the cost increases, this specialist cover ensures your asset remains protected against perils that standard policies would exclude after the building sits empty for 30 days.

How long can a commercial property remain unoccupied under insurance?

Most standard policies only allow for 30 days of unoccupancy before they restrict or cancel cover. With specialist insurance for unoccupied commercial property, you can protect your building for much longer periods, often up to 6 or 12 months. It’s essential to keep your broker updated on your timeline so they can negotiate extensions with underwriters as your search for a new tenant continues.

Do I need insurance if my vacant building is being renovated?

Yes, you need specialist cover, but you must inform your insurer about the works. Renovation significantly changes the risk profile due to the presence of contractors, tools, and structural changes. You’ll likely need a policy that combines unoccupied property protection with renovation-specific terms to ensure you’re covered for both the vacancy and the active construction risks on-site.

Can I get insurance for a partially occupied commercial building?

Yes, we can arrange cover for buildings where some units are active while others remain empty. These multi-unit blocks require a bespoke approach to ensure the vacant sections don’t void the policy for the entire site. We work with underwriters to create a hybrid solution that reflects the actual occupancy levels and security measures currently in place.

What happens to my insurance if I find a new tenant?

Once a new tenant signs the lease and moves in, you should immediately notify your broker to switch back to a standard commercial landlord policy. This usually results in a lower premium and broader coverage terms. Your specialist unoccupied policy will be adjusted to reflect that the building is no longer at high risk from long-term vacancy.

Does unoccupied insurance cover the cost of removing squatters?

Comprehensive unoccupied policies often include legal expenses cover, which assists with the costs of evicting squatters. Since occupying a commercial building is a civil matter in the UK, the legal process is often slow and expensive. Having this protection in place ensures you have the financial support needed to regain control of your premises and clear any resulting damage or waste.

What is the “FLEA” level of insurance for vacant properties?

FLEA cover is the most basic tier of insurance for unoccupied commercial property, covering only Fire, Lightning, Explosion, and Aircraft. It’s frequently used for buildings in poor condition where full protection isn’t an option. While it’s an affordable choice, it leaves you exposed to common risks like theft, vandalism, and escape of water, which are only covered under Full Perils policies.

Are inspections mandatory for unoccupied commercial property insurance?

Yes, regular inspections are almost always a mandatory condition of your policy. Most insurers require a thorough site visit every seven days to check for signs of damage or intrusion. You must document these visits in a logbook. A loss adjuster will ask for this evidence if you ever need to make a claim for damage that occurred while the building was empty.