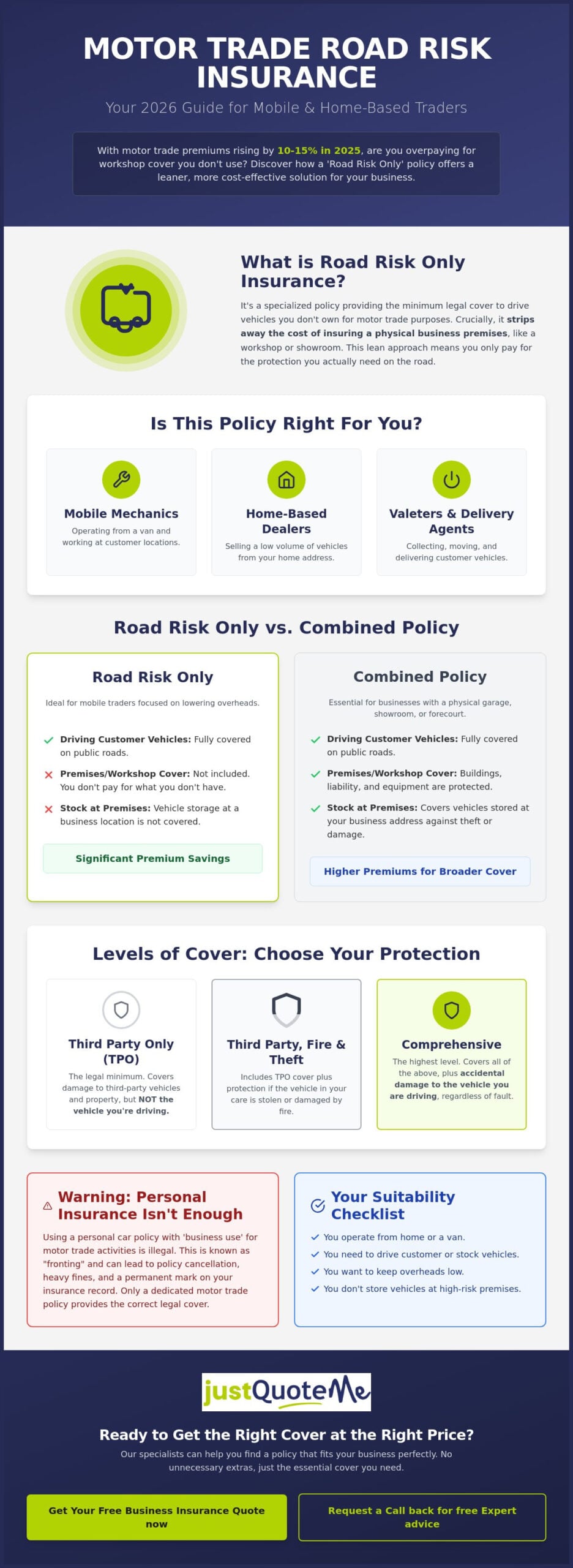

Why are you paying for a brick-and-mortar workshop policy when your entire business operates from a driveway or a mobile van? It’s a common frustration for mobile mechanics and home-based car dealers who find themselves subsidizing the costs of large garages they don’t own. If you’re looking to cut costs, focusing on motor trade road risk insurance only is the most efficient way to stay legal on UK roads while protecting customer vehicles in transit. You shouldn’t have to struggle through a complex market just to find a policy that fits your actual working day.

We understand that the 10-15% premium increases seen in 2025 have made budgeting a challenge for independent traders in 2026. This guide promises to simplify the process, helping you secure the essential protection you need at a price that reflects your specific trade. We will preview the latest MID update grace periods, explain how to manage the removal of the fuel duty freeze in September 2026, and show you how to maintain compliance without the burden of unnecessary premises cover. It’s time to get your business moving with a policy that works as hard as you do.

Key Takeaways

- Learn how to eliminate the overhead of physical premises insurance by choosing a policy tailored specifically for mobile and home-based operations.

- Identify the differences between Third Party Only and Comprehensive protection to ensure customer vehicles are fully covered during transit.

- Discover why motor trade road risk insurance only offers significant premium savings compared to combined policies while meeting all legal requirements.

- Master the essential requirements for the Motor Insurance Database (MID) to avoid penalties and ensure your business remains compliant on UK roads.

- Find out how working with a specialist broker provides access to a wider network of industry underwriters than standard comparison sites.

What is Motor Trade Road Risk Insurance Only?

Motor trade road risk insurance only is a specialized policy designed for professionals who move vehicles as part of their daily business activities but lack a dedicated commercial premises. It provides the legal framework required to drive cars, vans, or motorcycles that you don’t personally own. Unlike a combined policy, which includes cover for a physical workshop or showroom, this option focuses purely on the risks associated with being on the road. It’s a pragmatic solution for those who prioritize efficiency and lower overheads.

The “only” part of the name is critical. It signifies a lean approach to business protection. It’s built for the mobile mechanic working from a van or the part-time dealer selling vehicles from a home driveway. By stripping away the costs of building insurance and stock-in-trade cover for a fixed location, you ensure that your business expenses remain manageable. Following the 10-15% increase in motor trade premiums during 2025, many traders are switching to motor trade road risk insurance only to maintain their margins in 2026.

This type of cover is the backbone for various sectors. Mobile valeters, delivery drivers, and vehicle collection agents all rely on it to operate legally. Understanding vehicle insurance basics is helpful, but trade policies operate on a different level of liability. They allow you to handle customer assets with the confidence that you’re meeting UK road requirements without paying for a garage you don’t use.

The Road Risk Only Suitability Checklist

Determining if this policy fits your business model is straightforward. If you answer yes to these points, a road risk policy is likely your best option:

- Do you operate your business from a home address or a mobile van?

- Do you need to drive customer vehicles or stock on public highways?

- Are you looking to keep overheads low by excluding buildings and stock-in-trade cover?

- Do you handle a low volume of vehicles that don’t require high-security premises storage?

Why Personal Insurance Isn’t Enough

It’s a common mistake to assume a personal car policy with “business use” is sufficient. Standard domestic policies are designed for social, domestic, and commuting purposes. They specifically exclude any activity related to the motor trade. This means you aren’t covered the moment you pick up a customer’s car for a service or transport a vehicle you intend to sell. Attempting to use a personal policy for these tasks is often viewed as “fronting,” which can lead to cancelled insurance, heavy fines, and a permanent mark on your record. A dedicated trade policy allows you to drive any vehicle for business purposes, ensuring you stay on the right side of the law.

Request a Call back for free Expert advice

Levels of Cover: Choosing the Right Protection for 2026

Selecting the right level of protection is a balancing act between cost management and risk mitigation. While the primary goal of motor trade road risk insurance only is to keep your business lean, choosing the wrong tier can leave you financially exposed. In 2026, with the cost of parts and labor continuing to rise, the level of cover you select determines how much of a loss your business can absorb. There are three standard tiers available to traders.

Third Party Only (TPO) is the legal floor. It covers damage or injury to others but offers zero protection for the vehicle you are driving. This is often the starting point for those looking to meet official trade licence requirements without spending more than necessary. Third Party, Fire and Theft (TPFT) adds a layer of security, protecting you if a vehicle in your care is stolen or damaged by fire. However, for most active traders, Comprehensive cover is the standard. It protects the vehicles you drive against accidental damage, which is vital when handling expensive customer assets.

You must also pay close attention to indemnity limits. This is the maximum amount an insurer will pay for any single vehicle. If you routinely move high-end electric vehicles, which often exceed the £50,000 Luxury Car Tax threshold, a standard £20,000 limit won’t be enough. You can explore these options further when you compare motor trade insurance with an expert who understands these nuances.

Third Party Only (TPO) vs. Comprehensive

TPO might seem sufficient for low-value vehicle delivery or scrap collectors, but it’s rarely enough for service-based trades. If a mobile mechanic or valeter clips a wall while moving a customer’s car, a TPO policy leaves them footing the entire repair bill. Comprehensive motor trade road risk insurance only ensures that accidental damage is covered. While the premium is higher, the cost-to-benefit ratio usually favors Comprehensive cover because it prevents a single mistake from bankrupting a small business.

Optional Extensions for Road Risk Policies

A basic road risk policy covers the driving, but your business likely involves more than just being behind the wheel. Mobile workers should consider adding public liability insurance to protect against claims of injury or property damage at a customer’s site. You can also include tool and equipment cover to protect the specialized gear kept in your van. For home-based dealers, demonstration cover is a vital addition, allowing potential buyers to test drive vehicles under your insurance framework.

Request a Call back for free Expert advice

Road Risk Only vs. Combined Insurance: Which Saves You More?

Choosing between a road risk only policy and a combined motor trade policy is primarily a question of overhead management. For many small businesses, the cost of premises insurance is the single largest administrative burden. By opting for motor trade road risk insurance only, you’re essentially stripping your policy back to its functional core: the ability to drive vehicles legally. This lean approach is particularly effective in 2026, as traders look for ways to offset the 10-15% premium increases seen over the last year. It allows you to pay for the protection you use on the road without subsidizing the high fire and theft risks associated with a physical garage or showroom.

The risk profile for a mobile trader is fundamentally different from that of a fixed-site business. Insurers often view mobile professionals as a lower risk for large-scale theft because they don’t have a single location where dozens of high-value vehicles are gathered. Reading through a commercial vehicle insurance guide can help you understand these liability differences, but the practical result is a lower premium for those who don’t need a combined policy. Consider a mobile valeter compared to a fixed-site car wash. The valeter only needs to cover the vehicle while it’s being moved or worked on at a customer’s home. The car wash owner, however, must insure the building, the specialized machinery, and the high volume of cars parked on-site at any one time.

When “Road Risk Only” is the Correct Choice

This policy is the tactical choice for traders whose business doesn’t rely on a commercial lot. If you’re a home-based trader using your own driveway for a small amount of stock, a road risk policy provides the legal cover you need for test drives and collection. Mobile mechanics who carry out repairs at a customer’s location also benefit, as their primary risk is the transit of the vehicle rather than the storage of it. It’s also the ideal solution for part-time traders who balance car sales with a 9-5 job, providing a professional safety net without the corporate price tag.

Transitioning to a Combined Policy

There comes a point where a business might outgrow a road risk policy. If you start holding more than five or six high-value vehicles at a single location, the risk of a single fire or theft event could be devastating. Road risk policies generally don’t cover vehicles when they’re parked at your business premises; they’re designed for transit. If you’ve recently moved into a dedicated unit or workshop, it’s time to talk to us about a combined policy. We help you bridge this gap during your expansion, ensuring your growing stock is protected while keeping your transition costs as low as possible.

Request a Call back for free Expert advice

Eligibility and Managing Your Policy via the MID

Securing motor trade road risk insurance only requires meeting specific criteria that underwriters use to assess risk. Most providers look for drivers aged 25 or over, though some specialist schemes exist for younger traders with significant experience. You’ll typically need to have held a full UK driving license for at least one year. It’s also vital to understand that certain risks are often excluded from standard motor trade road risk insurance only policies. This includes the handling of hazardous goods or operating in postcodes with exceptionally high theft rates. If your business involves high-performance sports cars, you must ensure your indemnity limits reflect their value, especially with the Luxury Car Tax threshold for zero-emission vehicles rising to £50,000 as of April 1, 2026.

The Motor Insurance Database (MID) is the most critical administrative tool for any motor trader. It is a central record used by the police and the DVLA to identify uninsured vehicles. As a trader, it’s your legal responsibility to keep this database updated with every vehicle in your possession, including stock and customer cars you’re driving under your policy. Failing to manage this effectively can lead to immediate police interest and avoidable fines.

The MID: Your Legal Obligation

While there is technically a grace period of up to 14 days to add a newly acquired vehicle to the MID, as confirmed in May 2026, we strongly recommend doing it immediately. If you’re stopped by the police and the vehicle isn’t on the database, you face the risk of vehicle seizure. In 2026, the integration between the MID and roadside cameras is faster than ever. Updating your list takes only a few minutes through your insurer’s portal, providing instant peace of mind and keeping your business compliant.

Factors That Affect Your Road Risk Premium

Your premium isn’t just based on your trade; it’s influenced by your personal and professional profile. Your location plays a major role, specifically where vehicles are kept overnight. Even without premises insurance, insurers want to know if stock is on a secure driveway or parked on a public road. Your driver history, including any penalty points or previous claims, will also shift the cost. Finally, your estimated annual turnover and the number of vehicles you handle help insurers gauge the level of activity. If you’re unsure how these factors apply to you, talk to our specialist team for a clear breakdown.

Request a Call back for free Expert advice

Securing Your Motor Trade Quote with Just Quote Me

Just Quote Me brings 30 years of experience to the UK insurance market, providing a steady hand for traders in an increasingly complex sector. We understand that finding motor trade road risk insurance only isn’t always straightforward on generic comparison sites. Those platforms often use rigid algorithms that struggle with the nuances of part-time trading or mobile services. This often leads to inflated premiums or, worse, inadequate protection that leaves you vulnerable. As an independent broker, we have direct access to a broad network of specialist UK motor trade underwriters. This allows us to negotiate on your behalf, ensuring your policy reflects the actual risks of your business without forcing you to pay for unnecessary extras.

Our approach is grounded in bespoke advice. We don’t believe in one-size-fits-all solutions. Instead, we look at your specific vehicle throughput and trade type to find the most efficient path to coverage. By stripping away the administrative burdens, we help you maintain your margins in a year where external costs like fuel duty and parts inflation are putting pressure on the bottom line. You get the authority of an industry expert with the accessibility of a partner who genuinely cares about your business success.

Why Staffordshire Traders Trust Just Quote Me

While we serve professionals across the country, our local expertise in Stone, Stafford, and the wider West Midlands gives us a unique perspective. We pride ourselves on a personalized service that prioritizes human interaction over automated chatbots. When you contact us, you’ll speak directly to an expert who understands the local trade environment and the specific challenges you face. Our commitment to efficiency means we work quickly to get you covered and on the road. We know that in the motor trade, time is money, and we aim to make your insurance experience as frictionless as possible.

Next Steps for Your Trade Protection

Securing your trade protection is a simple process when you have the right details ready. You’ll need to provide your driving licence, evidence of your trade activities, and the maximum value of the vehicles you expect to handle. We use this information to find the most competitive motor trade road risk insurance only rates available. Our team ensures your indemnity limits are accurate, protecting you against the rising costs of vehicle repairs seen throughout 2026. Taking action now ensures your business remains legal, professional, and protected against the unexpected.

Request a Call back for free Expert advice

Protect Your Trade and Drive Your Business Forward

Choosing motor trade road risk insurance only is a tactical decision that aligns your overheads with your actual business model. By focusing on essential road protection and diligent MID management, you ensure your mobile or home-based operation remains both legal and lean throughout 2026. You’ve seen how stripping away premises cover can safeguard your margins while still providing the comprehensive protection required for customer vehicles in transit. It’s about paying for the cover you use, not the buildings you don’t own.

With 30+ years of industry experience, Just Quote Me stands as an FCA-authorised independent broker dedicated to simplifying your administrative burdens. We provide direct access to top-tier UK underwriters, ensuring you receive a policy that fits your professional needs without the corporate bloat. You don’t have to manage these complexities alone; we’re here to provide the steady hand and expert advice your business deserves. Partner with an expert today and stay focused on what you do best. Your business has the potential to thrive, and the right insurance partner makes that journey much smoother.

Request a Call back for free Expert advice

Frequently Asked Questions

Is road risk insurance a legal requirement for motor traders?

Yes, road risk insurance is the minimum legal requirement for any individual or business driving vehicles they don’t personally own on public roads. If you move customer cars or drive stock for your trade, you must have this cover to comply with the Road Traffic Act. Operating without it can lead to heavy fines, the seizure of vehicles, and a permanent mark on your commercial insurance record.

Can I get motor trade road risk insurance for a part-time business?

You can certainly secure a policy for a part-time venture as long as you can prove you are running a legitimate business for profit. Many insurers offer specialist schemes for those who sell cars or offer mobile repairs alongside another job. It is an excellent way to maintain professional standards and legal compliance without the high overheads associated with a full-time commercial garage or showroom.

Does road risk only insurance cover my own personal vehicles?

Most policies allow you to include your own personal vehicles, provided they are declared to your insurer and added to the Motor Insurance Database. This allows you to manage all your driving under one professional policy, often simplifying your administration. You must ensure that the policy includes “Social, Domestic and Pleasure” use for these specific vehicles, as trade-only cover may restrict your personal use during evenings and weekends.

What is the average cost of motor trade road risk insurance only in 2026?

The cost of your policy depends on several factors, including your location, driving history, and the types of vehicles you handle. While we don’t provide fixed pricing, the industry has seen premium increases of 10-15% recently due to the rising costs of parts and labor. Opting for motor trade road risk insurance only remains the most cost-effective choice for mobile traders because it excludes the expensive premiums required for physical business premises.

Can I add public liability to a road risk only policy?

Yes, adding public liability is a standard and highly recommended extension for most road risk policies. It protects your business if you accidentally cause injury to a member of the public or damage their property while you are working. For mobile mechanics or valeters working on a customer’s driveway, this extra layer of protection is vital for covering risks that occur when you aren’t actually behind the wheel.

Does comprehensive road risk insurance cover the tools in my van?

A standard comprehensive policy covers damage to the vehicle you are driving but does not usually include the tools or equipment kept inside. If you are a mobile professional, you will need to add a specific tools and equipment extension to protect your gear against theft or damage. This ensures that your specialized diagnostic tools or valeting equipment are financially protected while you are traveling between different jobs.

What happens if I forget to update a vehicle on the MID?

Failing to update the Motor Insurance Database can result in your vehicle being flagged by police roadside cameras, leading to immediate stops and potential seizure. While a 14-day grace period exists for some acquisitions, it’s safer to update the database the moment you take possession of a vehicle. Keeping your motor trade road risk insurance only records current is the most effective way to avoid unnecessary fines and police interest during your working day.

Can I get road risk insurance if I am under 25?

Securing cover for traders under 25 is possible, though it often requires a specialist underwriter and may carry stricter terms or higher excesses. Most standard insurers prefer drivers with at least one year of experience and a clean license. If you are a younger trader, working with an independent broker is the best way to find a provider that understands your specific trade and is willing to offer a competitive quote.