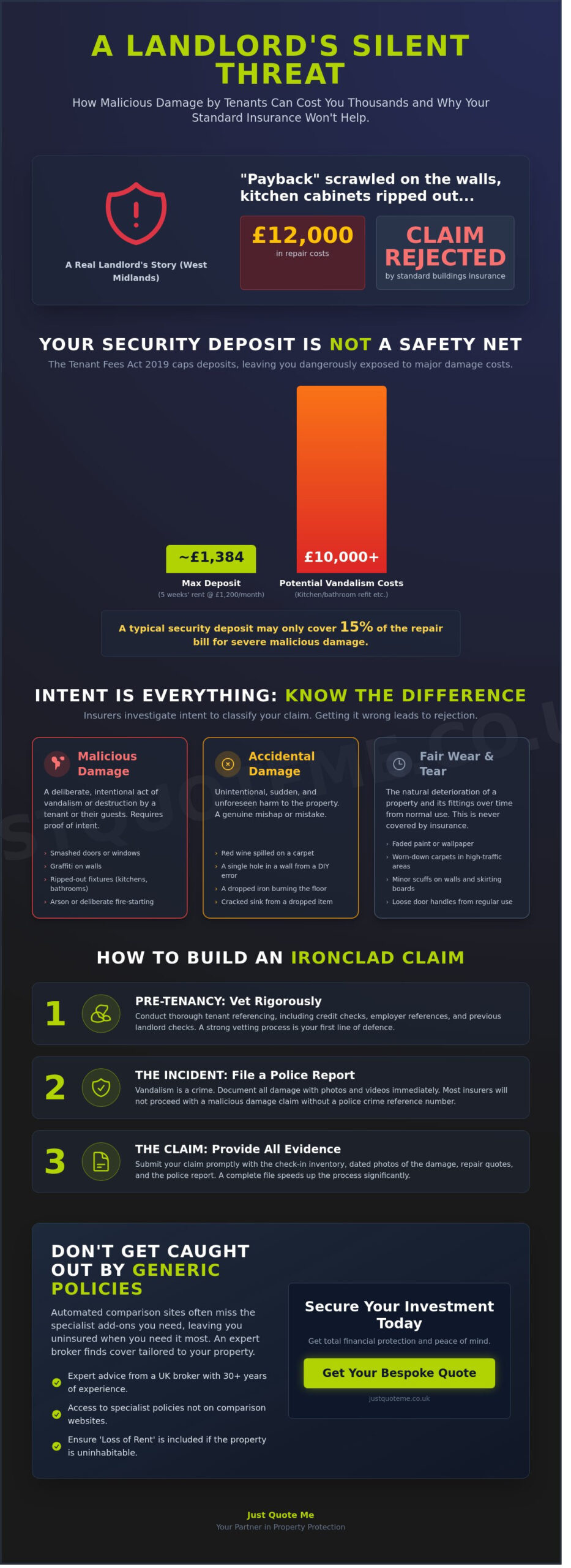

Imagine walking into your rental property after a difficult eviction only to find kitchen cabinets ripped from the walls and “payback” scrawled across the living room plaster. For one landlord in the West Midlands, this nightmare recently resulted in a £12,000 repair bill that their standard buildings insurance completely rejected. It’s a sobering reminder that while most tenancies end smoothly, the financial impact of a disgruntled tenant can be devastating to your bottom line.

You likely already understand that a standard security deposit rarely covers the cost of intentional vandalism. This is where specialist malicious damage by tenant insurance cover becomes your most vital safety net. At Just Quote Me, we believe insurance shouldn’t be a guessing game, especially when your hard earned capital is at risk. We’ll help you navigate the complexities of 2026 policy requirements, from the necessity of obtaining police reports to avoiding common exclusion traps. This guide explains how to secure total financial protection and provides the clear steps needed to ensure your investment remains protected, giving you the peace of mind you deserve.

Key Takeaways

- Understand why standard buildings insurance often falls short and how specialist malicious damage by tenant insurance cover protects your investment from intentional harm.

- Learn to distinguish between accidental damage and malicious intent to avoid common claim pitfalls like ‘fair wear and tear’ rejections.

- Discover how to secure your rental income with ‘Loss of Rent’ extensions that trigger if tenant damage leaves your property uninhabitable.

- Get a step-by-step roadmap for handling claims correctly, from conducting essential tenant referencing to filing police incident reports.

- Explore the benefits of using an independent UK broker with 30 years of expertise to find tailored coverage that automated comparison sites often miss.

Understanding Malicious Damage by Tenant Insurance Cover

Malicious damage occurs when a person lawfully permitted to be on your property intentionally causes harm or destruction to the structure or its contents. Unlike accidental damage, which covers spills or mishaps, this involves a deliberate act of sabotage. Many landlords assume their basic buildings policy protects them, but most standard products exclude these acts. Securing specific malicious damage by tenant insurance cover is essential because insurers typically view intentional damage by an invited guest as a manageable risk that requires a specialist policy or a specific extension.

The financial impact is often compounded by a heavy psychological toll. Discovering a trashed property leads to extreme stress and significant downtime where no rent is collected. A broker plays a critical role here. We identify which insurers include this protection as a standard feature in residential letting insurance and which require it as an optional extra. This ensures you don’t face a rejected claim during an already difficult period.

The Legal Context: Malicious Damage Act and Landlord Rights

The legal framework for these claims often draws from the Malicious Damage Act 1861, which provides the foundation for how Vandalism and property destruction are prosecuted in the UK. In the context of insurance claims for 2026, intent is defined as the proven, conscious decision by a tenant to cause physical harm to the property, which clearly distinguishes it from wear and tear or simple negligence. Landlords have the legal right to pursue criminal charges or civil litigation, but these processes are slow and expensive. Specialist insurance provides the immediate funds needed to restore the property while legal proceedings take place in the background.

Why Deposits Are Rarely Enough for Malicious Acts

The Tenant Fees Act 2019 restricted most security deposits in England to a maximum of five weeks’ rent. For a property with a monthly rent of £1,200, the deposit is capped at approximately £1,384. This amount is quickly exhausted if a tenant rips out kitchen units, destroys bathroom suites, or smashes internal doors. Repair costs for these acts of sabotage can easily exceed £10,000. While the Deposit Protection Service (DPS) provides a mechanism for recovery, it’s designed for minor disputes rather than major structural damage. Comprehensive malicious damage by tenant insurance cover acts as the only reliable safety net when repair bills dwarf the available deposit funds.

- Standard deposits rarely cover more than 15% of a major renovation cost.

- Insurance covers the gap between the deposit and the total repair bill.

- Policies can also cover the loss of rent while the damage is being repaired.

Malicious Damage vs. Accidental Damage: Knowing the Difference

Understanding the line between a mistake and a deliberate act is vital for any landlord. The core difference lies in intent. Accidental damage happens through clumsiness or a genuine mishap, while malicious damage is a purposeful act of destruction. Having the right malicious damage by tenant insurance cover ensures you aren’t left paying for a tenant’s anger or criminal activity. Insurers look closely at the evidence to decide which category applies to your claim.

Fair wear and tear remains the most common reason for claim rejection in the UK rental market. Property naturally ages. Frayed carpet edges, faded paintwork, and loose door handles are part of a building’s lifecycle. In the UK, strict deposit protection schemes ensure that security deposits cover damage beyond normal wear and tear, not fair wear and tear itself. Landlords, particularly in areas like Staffordshire and the West Midlands, must provide clear proof of intent or negligence for any deductions. If an insurer determines the damage is simply the result of a long tenancy, they won’t pay out.

Insurers investigate the “moment of damage” to find the trigger. A single hole in a wall might be a DIY error. Ten holes in a row suggest a deliberate attack. Grey areas often emerge during domestic disputes or when a tenant’s guest causes trouble. If a partner kicks a door in during an argument, most providers classify this as malicious, though they usually require a police crime reference number before proceeding with the claim.

Common Examples of Malicious Acts

- Arson and Fire: Purposefully setting fire to curtains or floorboards.

- Sanitary Ware Destruction: Smashing toilets, sinks, or baths with heavy tools.

- Graffiti: Spray-painting walls or floors to ruin the aesthetic of the home.

- Intentional Flooding: Blocking drains and leaving taps running to cause structural rot.

Cannabis farms represent a specific, high-risk sub-category of malicious damage. Criminal tenants often bypass electricity meters and install heavy ventilation, leading to scorched ceilings and severe mould. Revenge damage is another primary trigger for this cover. When a landlord serves an eviction notice, some tenants react by destroying the property out of spite before they leave. This is why specialized malicious damage by tenant insurance cover is a necessity rather than a luxury.

What Counts as Accidental Damage?

Accidental damage covers the “oops” moments of daily life. This includes spilling red wine on a new carpet, dropping a heavy cast-iron pan on a ceramic hob, or putting a foot through the ceiling while retrieving suitcases from the loft. These incidents lack the “intent to harm” that defines malicious acts.

Because the risks differ, premiums for these add-ons vary. Accidental damage is often cheaper because it’s more common and usually less expensive to fix than a gutted kitchen. A comprehensive residential letting insurance policy typically treats these as two distinct sections. Separating them allows you to choose the level of protection that fits your specific tenant demographic. If you want to ensure your investment stays profitable, it’s worth checking your policy documents today.

What Does Landlord Insurance for Malicious Damage Actually Cover?

Standard policies provide a vital safety net for deliberate acts of destruction. This isn’t about a spilled glass of wine on a carpet or a scuffed skirting board; it’s about smashed windows, kicked-in doors, or graffiti. A robust malicious damage by tenant insurance cover typically handles the financial burden of restoring your property to its original state after a tenant intentionally causes harm. It covers the cost of professional contractors and the materials needed for repairs.

Insurers set a limit of indemnity, which is the maximum amount they’ll pay for a claim. For residential units, this often starts at £500,000, though it can scale significantly for multi-property portfolios. If you manage 15 properties across Staffordshire, your policy should be structured to reflect the aggregate risk across the entire portfolio. This ensures that one major incident doesn’t exhaust your total coverage limits.

One of the most valuable components is the ‘Loss of Rent’ extension. If the damage is so severe that the property is uninhabitable, this extension triggers. It replaces the income you lose while the property is being repaired. For instance, if a house in Stoke-on-Trent requires eight weeks of structural work, the insurer covers the missing rental payments, keeping your mortgage commitments on track.

Buildings vs. Contents: Protecting Every Asset

Buildings cover protects the ‘shell’ of your investment. This includes the walls, floors, roofs, and fixed units like fitted kitchens or bathrooms. However, landlords with furnished lets must ensure their contents are specifically named in the malicious damage clause. Without this, you might find the walls are covered but the destroyed sofas and appliances are not. For those managing retail or office spaces in the West Midlands, a specialized commercial property insurance policy is often required to handle the higher reinstatement costs associated with business premises.

The Crucial Exclusions: What Insurers Won’t Pay For

Understanding what landlord insurance covers is as much about knowing the limitations as the benefits. Insurers won’t pay for ‘gradual damage’ or issues resulting from a lack of maintenance. If a tenant slowly ruins a property through neglect over several years, it’s rarely covered by a malicious damage claim. It has to be a specific, intentional act.

The ‘unoccupied property’ rule is another common pitfall. If your property sits empty for more than 30 consecutive days, many insurers suspend or limit your malicious damage by tenant insurance cover. You must notify your broker if a property is vacant for an extended period. Finally, damage caused by squatters or people ‘unlawfully on the premises’ often falls under standard vandalism. This is a separate category from damage caused by a person named on the tenancy agreement, often carrying different excess amounts.

How to Protect Your Property and Handle a Malicious Damage Claim

Securing the right malicious damage by tenant insurance cover is only half the battle. You also need to follow strict protocols to ensure your policy remains valid when you need it most. Most insurers view professional tenant referencing not just as a recommendation, but as a warranty. This means if you fail to conduct a comprehensive check, including credit history and previous landlord references, your claim could be rejected outright. These checks act as your first line of defence, filtering out high-risk applicants before they ever hold a key.

Risk Mitigation: Preventing Damage Before It Happens

Regular inspections are a non-negotiable requirement for most UK landlords. To satisfy the ‘reasonable care’ clause found in most policies, you should aim to inspect the property at least every six months. These visits allow you to spot early warning signs of neglect or unauthorised alterations before they escalate into a total loss. Documenting these visits provides a paper trail that proves you’ve been a responsible property owner.

While you’re focusing on property damage, don’t forget broader risks. Having public liability insurance protects you if a tenant or visitor is injured on your premises due to a maintenance failure. It provides a vital safety net for your wider portfolio and ensures you aren’t left vulnerable to personal injury claims.

The First 24 Hours: Emergency Response Checklist

If you discover your property has been trashed, your actions in the first 24 hours are critical for a successful claim. Follow these steps immediately:

- Step 1: Contact the police. Malicious damage is a criminal act, not just a civil dispute. You must obtain a Crime Reference Number (CRN) immediately. Without this number, most insurers won’t even open a file for a malicious damage claim.

- Step 2: Document the scene. Take high-resolution photos and video evidence of every room. Do this before any cleanup begins. Capture close-ups of specific damage and wide shots of the entire area.

- Step 3: Notify Just Quote Me. Contact us to initiate the claim. We provide expert guidance on what temporary repairs you can make to secure the property without compromising the evidence needed by the insurer.

The Role of Evidence and the Loss Adjuster

Your ‘Inventory and Schedule of Condition’ is your most powerful piece of evidence. This document, signed by the tenant at the start of the tenancy, proves the property’s original state. When assessing a claim under your malicious damage by tenant insurance cover, an insurer will often appoint a loss adjuster. Their job is to determine if the damage was truly intentional or simply ‘fair wear and tear’.

Loss adjusters look for specific indicators of intent, such as holes kicked into internal walls, doors pulled off hinges, or paint poured onto carpets. Because they are impartial experts, having a detailed, dated inventory makes it much harder for an insurer to dispute the cause of the damage. We recommend keeping digital copies of all receipts and inventories to ensure they are accessible during the claims process.

Don’t leave your investment to chance. Get a tailored quote for landlord insurance today and protect your property from the unexpected.

Finding Bespoke Landlord Cover with Just Quote Me

Price comparison websites operate on rigid algorithms that often exclude complex risks. If you’re a landlord, you need more than a generic policy generated by a computer. Just Quote Me brings 30 years of experience across the Staffordshire and West Midlands insurance markets to help you secure the right protection. We understand that finding reliable malicious damage by tenant insurance cover is often difficult when your property houses high-risk occupants like students or DSS tenants. While automated sites might reject these applications or inflate premiums, an independent broker negotiates directly with underwriters to find a fair solution.

When a “tenant nightmare” happens, you don’t want to wait in a digital queue or talk to a chatbot. You need a real person who understands the local market and your specific situation. We provide a human-centric service that prioritizes your peace of mind during stressful claims. Our experts handle the heavy lifting, ensuring you aren’t left stranded when property damage occurs. We know the nuances of the local area, from Stone to Birmingham, giving us an edge over faceless national corporations.

Tailored Solutions for Every Property Type

We assist landlords with unique and complex portfolios. This includes specialized thatched pub insurance or mixed-use buildings that combine commercial units with residential flats. We conduct annual policy reviews to ensure your cover reflects current economic shifts. For instance, ensuring your limits meet projected 2026 rebuild costs is vital to prevent underinsurance. This proactive approach saves you significant time and money, especially during complex claims where every detail matters. A bespoke brokerage ensures your policy remains fit for purpose as the market evolves.

Get Your Quote: The No-Nonsense Approach

Securing malicious damage by tenant insurance cover shouldn’t be a box-ticking exercise. Our philosophy is built on being quick, transparent, and expert-led. We don’t believe in wasting your time with endless forms. Instead, we encourage landlords to consolidate their requirements. You might link your residential portfolio with shop insurance or other commercial policies to secure more competitive premiums. This streamlined method reduces your administrative burden and ensures there are no gaps in your protection. Contact our Stone-based team for a bespoke landlord insurance quote today.

Secure Your Rental Portfolio Against Intentional Risks

Protecting your investment requires more than just a standard policy. You need to know the clear difference between accidental mishaps and deliberate acts of destruction to ensure your property remains a viable asset. By securing comprehensive malicious damage by tenant insurance cover, you guarantee that intentional harm doesn’t result in a devastating financial blow. We’ve explored how proactive management and specific policy wording can save you thousands in repair costs while keeping your business running smoothly.

Our team offers 30+ years of independent brokerage experience. We are FCA-authorised experts who connect you with an extensive network of top UK underwriters to find the right fit for your specific needs. We don’t use faceless, automated algorithms. Instead, we provide personal, honest advice that addresses the unique challenges UK landlords face in 2026. We’re ready to help you navigate the insurance market with confidence and clarity so you can focus on your tenants.

Get a bespoke Landlord Insurance quote from our UK experts and let us simplify your coverage today. It’s a straightforward way to safeguard your future and your property.

Frequently Asked Questions

Is malicious damage by tenants covered as standard in landlord insurance?

Malicious damage by tenants isn’t usually included as standard in a basic landlord buildings insurance policy. Most insurers treat it as an optional add-on that you must specifically request. Without this specific malicious damage by tenant insurance cover, you may find yourself liable for the full cost of repairs if a tenant intentionally harms your property. Always check your policy schedule for exclusions related to intentional acts by residents.

Do I need a police report to claim for malicious damage by my tenant?

You’ll almost certainly need a police crime reference number to process a claim for malicious damage. Since malicious damage is a criminal act under the Criminal Damage Act 1971, insurers require formal documentation to prove the damage was intentional rather than accidental. You should report the incident to the police immediately upon discovery. This official record acts as vital evidence for your insurance provider during the claims process.

Can I deduct malicious damage costs from the tenant’s deposit?

You can deduct the costs of repairing malicious damage from the security deposit, provided you have sufficient evidence. You’ll need a clear check-in inventory and a final check-out report to prove the damage occurred during the tenancy. If the repair costs exceed the deposit amount, which is capped at five weeks’ rent for most UK tenancies under the Tenant Fees Act 2019, you’ll need to claim through your insurance.

What is the difference between malicious damage and vandalism in insurance?

In insurance terms, malicious damage is caused by someone who has a legal right to be in the property, such as your tenant or their guests. Vandalism refers to damage caused by trespassers or burglars who have entered the property illegally. It’s a crucial distinction because many standard policies cover vandalism by intruders but require a specific extension for malicious damage by tenant insurance cover to protect against those you’ve let into the home.

Does insurance cover damage caused by a tenant’s sub-letter or guest?

Most comprehensive landlord policies extend malicious damage cover to include the tenant’s guests or invited visitors. However, if your tenant has sub-let the property without your permission, your insurance might be voided entirely. Standard UK tenancy agreements usually prohibit sub-letting for this reason. You should ensure your policy covers all lawful occupants to avoid gaps in protection when your tenant’s associates cause intentional harm to the structure or contents.

Will my insurance pay for loss of rent if the property is damaged maliciously?

Your insurance will typically pay for loss of rent if the malicious damage makes the property uninhabitable for future tenants. This is usually claimed under a Loss of Rent section of your policy rather than the buildings cover itself. If the damage requires major structural repairs that take weeks to complete, this cover ensures you don’t lose out on your monthly income while the property sits empty during the restoration process.

What happens if the damage is discovered after the tenant has already moved out?

You can still make a claim if you discover damage after the tenant leaves, but you must do so immediately. Most insurers set a strict time limit, often 30 days, for reporting incidents after a tenancy ends. Your check-out report, conducted within 24 to 48 hours of the keys being returned, serves as the primary evidence. If you wait too long to inspect the property, the insurer might argue the damage happened while the building was vacant.

Is damage caused by a cannabis farm considered malicious damage?

Damage from cannabis cultivation is generally classified as malicious damage, but it’s a high-risk area that many insurers treat separately. The 2023 UK crime data shows a rise in residential grow ops, which cause extensive water damage and electrical alterations. Because the costs often exceed £10,000 per incident, some policies have specific illegal cultivation of drugs clauses with unique limits or higher excesses. Check your policy wording to ensure this risk is covered.